Post updated to present Showcase sponsor, Fintech71 and latest Showcase addition, FinTech Innovation Lab.

—

To prepare for our expanded FinovateFall conference in September, we’re taking a look at some of the new additions during Discussion Days September 13 and 14. Today, we’re previewing our Showcase of Accelerators, Incubators, and Innovation Labs on the 14th.

FinovateFall 2017’s showcase on accelerators, incubators, and innovation labs features demos from startups representing each of our accelerators, with the audience selecting the most innovative startup based on “biggest impact in startup ecosystem.” Here is a sampling of the accelerators and incubators whose startups will be represented during our showcase.

Fintech71

We lead off with our Showcase sponsor, Fintech71. One of the newest fintech accelerators to emerge on the scene, Fintech71’s goal is to attract fintech startups to Ohio and grow the innovation pipeline for the state’s private sector stakeholders. Backed by companies such as KeyBank, Progressive, and Fifth Third, Fintech 71 provides innovative entrepreneurs with a $100,000 investment for up to 6% equity, daily 1-on-1 mentor support, as well as access to participating companies and “millennial talent” thanks to nearby Ohio State University.

Fintech71 will begin its inaugural class on September 10. Up to 12 startups will participate in the 10-week program, which will be based in Columbus, Ohio. “Ohio’s ranking as a Top 5 Fortune 500 and Top 5 Fortune 1000 headquarter destination is not without reason,” Fintech71 executive director Matt Armstead said, adding, “We aim to leverage Ohio’s tech-savvy talent, attractive cost of doing business, and established industry strength to make Ohio a global hotspot for fintech innovation and growth.

Citi Ventures

Citi Ventures is the “innovation engine” of Citi. The division invests in startups, supports new technologies, and tests new products and services in its Innovation Labs and businesses. Citi Ventures made its first investment in July 2010, and saw its first portfolio company exit (Silver Tail acquired by EMC) two years later. Citi Ventures launched its first fintech accelerator in Tel Aviv in 2013.

- Founded in 2010 by Debby Hopkins

- Headquartered in Palo Alto, California

- Notable Startups: Linkable Networks (FF12), Ayasdi (FF14), Feedzai (FE14), Betterment (FF11), Chain (FD15), BlueVine (FF14), Plaid (FD14), Pindrop Security (FF12)

In 2017, Citi Ventures began the year appointing a new chief, Vanessa Colella, who was also named Chief Innovation Officer of Citi. Citi Ventures launched its Citi University Partnerships in Discovery program in February and in May, the venture capital arm of Citi leveraged the technology from portfolio company (and Finovate alum) Chain, to launch Citi Connect for Blockchain integrated with Nasdaq Linq.

FinTech Innovation Lab

Fintech Innovation Lab specializes in early and growth-stage fintech companies, helping these startups get access to some of the biggest financial services companies in the world. With programs in New York, Hong Kong; Dublin, Ireland; and London, the Lab’s alums have raised $530 million in VC funding since graduating from the accelerator program – more than $460 million from the New York lab alone. FinTech Innovation Lab is sponsored by Partnership Fund for New York City and Accenture.

- Founded in 2012 by Maria Gotsch and Robert Gach

- Headquartered in New York City, New York

- Notable Startups: AlphaPoint (FE15), Atsora (FE14), BehavioSec (FF15), Big Data Scoring (FF15), BillGuard (FS12), bondIT (FF16), Dashlane (FE13), DeMystData (FA12), EverSafe (FF14), ForwardLane (FS16), Logical Glue (FE16), MaxMyInterest (FF14), Modelshop (FD17), Narrative Science (FF13), PhotoPay (FE15), RevolutionCredit (FF13), True Office (FE13), Uniken (FF16)

Last month, FinTech Innovation Lab celebrated its seventh anniversary, as a new class of startups – including Finovate/FinDEVr alums BehavioSec, DemystData, and Modelshop – demonstrated their technologies at the Lab’s annual Demo Days event. The occasion encouraged FinTech Innovation Lab co-founder Robert Gach to note that many of the technologies that have been seen at the Lab have anticipated trends ranging from big data analytics to the blockchain. “We expect this year’s innovations will experience a similar trajectory,” Gach said.

Omidyar Network RegTech Accelerator

Omidyar Network is an active impact investor that provides both financial and human capital to entrepreneurs in five main focus areas: education, emerging technology, governance and citizen engagement, property rights, and financial inclusion. The firm, launched by eBay founder Pierre Omidyar, has a special interest in “entrepreneurs who share our commitment to advancing social good at the pace and scale the world needs today.”

- Founded in 2004 by Pierre and Pam Omidyar

- Headquartered in Redwood City, California

- Notable Startups: Digi.me, Entrepreneurial Finance Lab (FA12), Lenddo, Prosper (FS09), RevolutionCredit (FF13), Tandem Bank

Earlier this year, Omidyar Network teamed up with Finovate alum Twilio as the firm launched its Impact Fund to support social impact programs. In February, Omidyar Network invested $2.9 million in an initiative to support the development of civic technology platforms in Latin America. In total, Omidyar Network has committed more than $900 million in for-profit investments and non-profit grants since inception.

Startupbootcamp NY

With partners including Mastercard, Santander, and Route 66 Ventures, Startupbootcamp NY provides fintech startups with seed funding, professional mentorship, New York City office space, and access to a worldwide network of fintech investors and businesses. The program’s areas of focus includes advanced analytics, blockchain technology, financial inclusion, identity & authentication, investments & personal finance, mobile security, P2P lending, and payments.

- Founded in 2o1o by Alex Farcet, Carsten Kolbeck, Patrick de Zeeuw, and Ruud Hendriks

- Headquartered in London, U.K.

- Notable Startups: BankGuard (FE17), bondIT (FF16), Dragon Wealth Asia (FA13), investUP (FE16), InvoiceSharing (FE17), iproov (FE17)

An accelerator network with a global reach, Startupbootcamp sponsors events in more than 100 cities every year. It has more than 460 startups in its portfolio, more than 70% of which received funding. Startupbootcamp was named Best Accelerator 2014 in the European Tech Startup Awards. In addition to its fintech accelerators in New York, London, Singapore, and Mumbai, Startupbootcamp also provides programs in e-commerce (Amsterdam), insurance (London), and IoT (Barcelona).

Techstars

Since its inception, Techstars has accelerated more than 1,000 companies, with an active or acquired rate of 90%. The firm has provided $3.7 billion in total funding to startups with a total market capitalization of more than $9 billion. “We fund technology oriented companies, typically web-based or other software companies,” Techstars explains in an FAQ, “but we’ve funded companies that don’t quite fit that mold as well.”

- Founded in 2006 by David Cohen, Brad Feld, David Brown, and Jared Polis

- Headquartered in Boulder, Colorado

- Notable Alums: Remitly, DigitalOcean, ImpulseSave (FF12), Realty Mogul, Good April (FS13), Market IQ (FF13), Bitfusion, Zighra (FF13), Robinhood,

Techstars just celebrated the 10th anniversary of its Techstars Startup Weekend. Also this month, Techstars announced the addition of more than 100 companies to its Worldwide Network. In June, Techstars teamed up with GINCO to launch the Techstars Dubai Accelerator, which opens this month and will begin its first class in January. Techstars introduced a new accelerator in Paris in March, partnering with venture capital firm, Partech Ventures.

The upcoming Showcase of Accelerators, Incubators, and Innovation Labs at FinovateFall will feature demos from each of our featured accelerators. To be a part of our Discussion Days audience at FinovateFall, be sure to register and save your spot at the show today.

Image Designed by Freepik

Music producer, broker, coder, and a leading influencer within fintech, Natasha Kyprianides is not short of experiences and skills. Group Head of Digital Banking & Innovation at Hellenic Bank, she gives us a window into her fascinating path into fintech and some expert advice for other women in fintech paving their ways.

Music producer, broker, coder, and a leading influencer within fintech, Natasha Kyprianides is not short of experiences and skills. Group Head of Digital Banking & Innovation at Hellenic Bank, she gives us a window into her fascinating path into fintech and some expert advice for other women in fintech paving their ways.

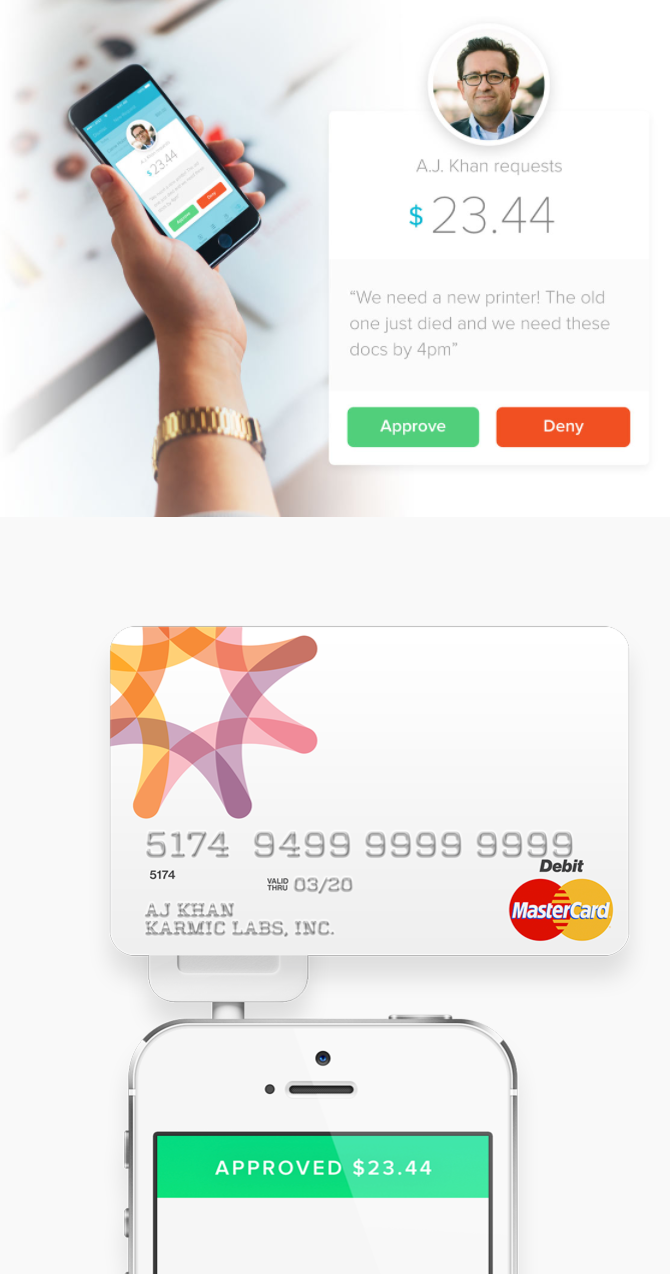

Karmic Labs

Karmic Labs