This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

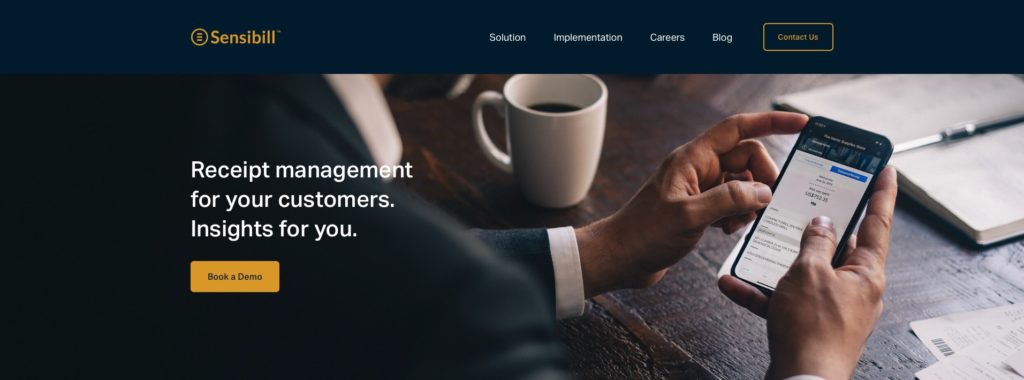

Digital receipt management specialist – and FinovateFall Best of Show winner – Sensibill has forged a new partnership that will put its receipt capture and management solution in the hands of more banking customers.

JPMorgan has agreed to integrate Sensibill’s technology into its Chase Mobile Banking app, making it easier for the firm’s customers to manage expenses, provide proof of purchase for insurance claims, and monitor spending “at a granular level.”

The offering will be made available to the 38 million active users of Chase’s mobile app as part of a progressive rollout later this year. As the U.S. consumer and commercial banking business of JPMorgan Chase & Co., Chase has 4,900+ branches in 38 states and the District of Columbia, as well as a network of 16,000 ATMs.

“Chase has created a digital banking experience that makes it easier for consumers and businesses to manage their finances,” co-founder and Sensibill CEO Corey Gross said. “Through our partners with Chase, millions of customers will have access to a best-in-class product that solves the hassle of expense and receipt management.”

Sensibill’s smart receipt management enables users to capture any physical receipt or invoice by taking a photo or forwarding an email. The solution leverages optical character recognition (OCR) and AI to turn receipt images into categorizable data that can be downloaded into expense reports, spreadsheets, or other digital documents. Sensibill makes it easier to organize and add context to expenses, and includes functionality to link receipts to card transactions for SKU-level visibility into spending.

The technology also helps financial institutions enhance their customer engagement by leveraging digital receipt data to offer more personalized solutions. Sensibill’s 75 financial institution partners in North America and the U.K. have used the technology to spot small businesses that may be ready to migrate from a personal to a business account, identify non-card spending patterns to better guide their own product offerings, and build brand loyalty.

Founded in 2013, Sensibill has raised $55.4 million in funding according to Crunchbase. The company, based in Toronto, Ontario, Canada, includes Radical Ventures, First Ascent Ventures, Information Venture Partners, Impression Ventures, and Mistral Venture Partners among its investors.

I feel the need to start this piece with a disclaimer: Racial bias and gender bias are two completely different issues. Both women and people of color, however, face stereotypes and suffer from wage discrimination. And though the battles are different, some of the tools used in the fight are the same.

While both women in fintech and ethnic diversity in fintech efforts have been around for half a decade, the women in fintech crusade has managed to gain a fair amount of momentum. There are now hundreds of passionate activists that promote women in fintech.

Even though the tech industry as a whole has a long way to go to achieve gender equality, the truth is that we have even further to go until we reach parity for black and brown workers. The following graph from Information is Beautiful shows the employee breakdown by ethnicity and gender at top tech companies in 2017.

The message is that the technology community has a lot of work to do. Each of us– not only as companies, but also as individuals– has a responsibility to take concrete action to help elevate ethnic diversity within our industry.

The movement to promote women has already begun to successfully create change and growth in the fintech industry. Here are a few things that are working for gender diversity that we can use to further promote ethnic diversity.

Mentorship

Networking events

Organized member associations

School programs

Competitions

While it can be difficult to know where to start, perhaps begin with a simple action such as following more black and brown voices on social media to hear perspectives you might not otherwise hear. You can also become a member of an existing organization, such as Blacks in Technology, or simply donate to the cause. Small actions will add up and change begins with individuals.

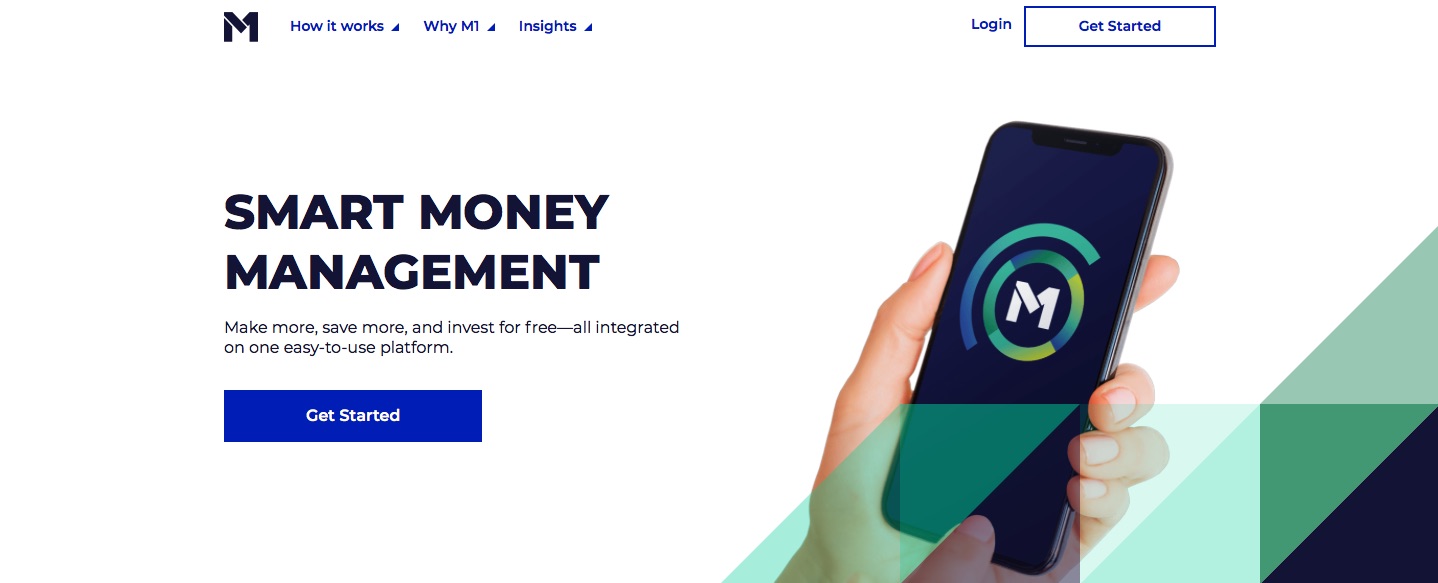

In a round led by New York-based growth equity firm Left Lane Capital, money management platform M1 Finance has raised $33 million in new capital. The Series B, which also featured the participation of Jump Capital, Clocktower Technology Ventures, as well as existing M1 investors, takes the company’s total funding to $53.2 million, according to Crunchbase.

The investment comes at the halfway mark of a year in which the company reached $1 billion in customer assets managed and added more than $650 million in customer deposits to its platform. The company noted that it achieved the $1 billion AUM milestone faster and with less funding than many of its competitors.

“We’ve built the premier personal finance platform that combines the best of digital investing, borrowing, and banking, and have done so on relatively little funding,” company CEO and founder Brian Barnes said. “That is a testament to the team and culture we have here. We’re just getting started and look forward to accelerating our growth with this new funding and strong new partners.”

The M1 personal finance platform consists of three main, integrated solutions to help users build wealth over the long-term, respond to intermediate-term financial challenges and needs, and manage near-term spending and saving. M1 Invest is the platform’s free investment solution that enables investors to build customized portfolios of stocks and exchange-traded funds (ETFs). The module features both fractional share functionality and advanced automation. M1 Borrow is the platform’s line-of-credit product, which offers rates between 2.0% and 3.5%. M1 Spend gives platform users an FDIC-insured digital checking account and debit card. This offering features a 1.00% APY and 1% cash-back on qualified purchases (with a subscription to the company’s M1 Plus upgrade).

“With M1, you can build an entire wealth strategy in only a few clicks, down to individual stocks and ETFs,” Barnes said. “We take it from there, handling all the day-to-day optimization, rebalancing, and re-investing according to your instructions so you can spend more time building strategies and less time executing them.”

Founded in 2015 and headquartered in Chicago, Illinois, M1 Finance demonstrated its platform at FinovateFall 2016.

Facebook-owned messaging giant WhatsApp announced today that users in Brazil can now send payments within its app.

The digital payments capabilities, powered by Facebook Pay, will allow users to send P2P payments to friends for no fee. The app also facilitates payments between WhatsApp users and businesses, but charges the business a 3.99% transaction fee.

With 120 million monthly active WhatsApp users, Brazil seems to have cut in line in front of India, which counts 400 million monthly active WhatsApp users, for the payments service. However, according to TechCrunch, WhatsApp has had difficulty sorting through regulations in India.

In the way of security, WhatsApp requires a 6-digit PIN or fingerprint to authenticate transactions. WhatsApp is working with Banco do Brasil, Nubank, and Sicredi to accept Visa and Mastercard debit or credit cards. Latin America’s largest payment systems company, Cielo, was chosen to be the payments processor.

There is no word on further international expansion for WhatsApp’s in-app payment capabilities.

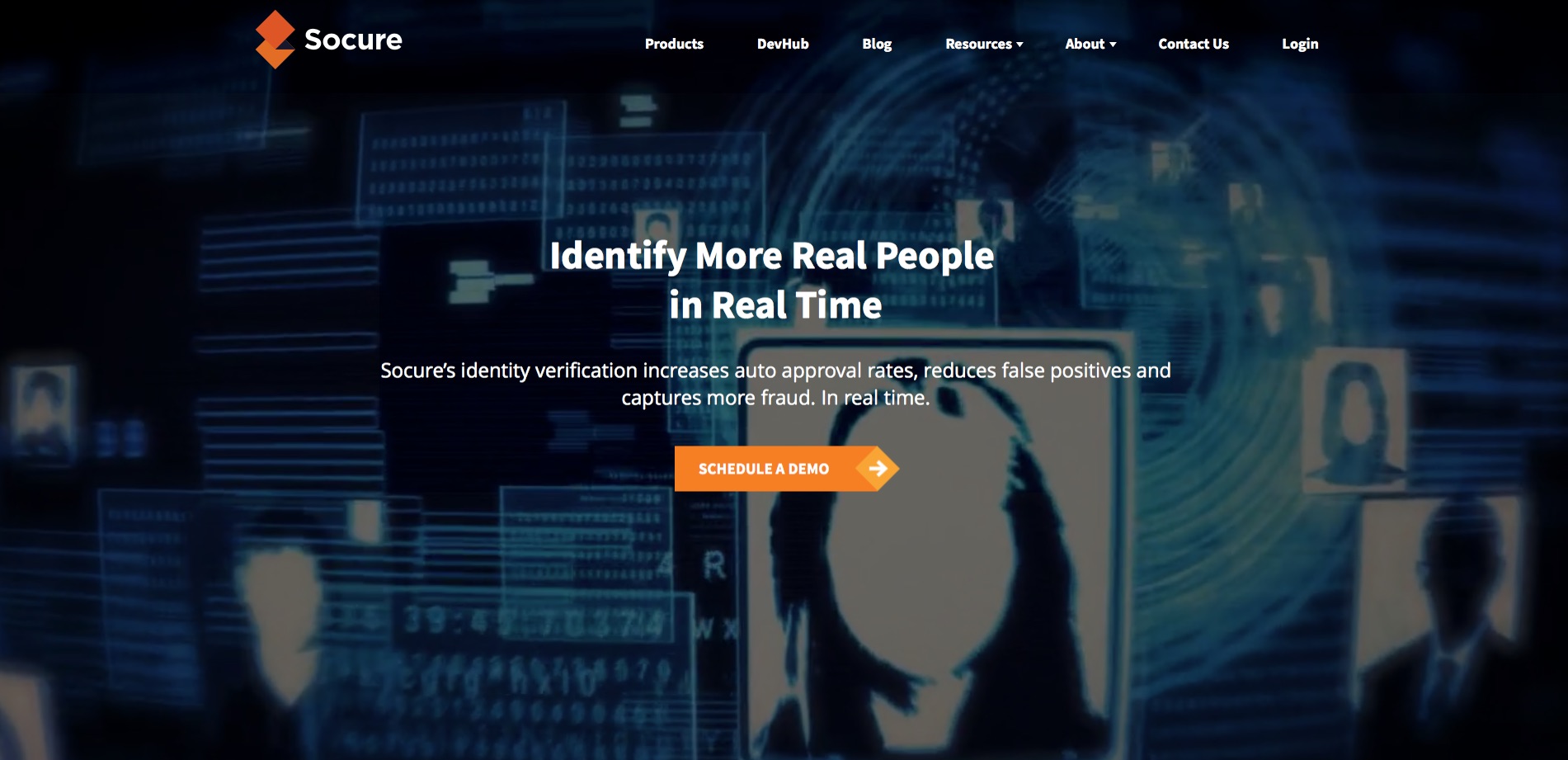

Digital identity verification specialist Socure has introduced a new solution to help accelerate and scale customer acquisition. Intelligent KYC, launched last week, leverages advanced graph analytics, unsupervised machine learning, and a sizable volume of data sources to give businesses higher auto-approval rates compared to legacy identity verification systems, as well as fewer manual reviews.

“In the digital-first world, compliance teams need hyper-accuracy in their use of KYC tools without introducing more friction for customers or costly reviews for their operations teams,” Socure CEO Tom Thimot explained. “Intelligent KYC is the industry’s most sophisticated KYC solution and will push our clients far beyond check-box compliance.”

Available as both an individual solution as well as part of an end-to-end integrated, identity fraud engine, Intelligent KYC is especially suited for institutions serving underserved populations – from millennials with thin credit files to newly-arrived immigrants with no domestic credit record. Intelligent KYC leverages machine learning to access more than 310 million entities and three billion records from a wide variety of authoritative sources including credit header and inquiry, utility and telecommunications companies, and more.

Writing about the concept of Intelligent KYC on the Socure blog, privacy, data security, and fintech attorney and company advisor Annie C. Bai noted the emphasis that Socure’s solution places on precision accuracy in the initial phases of the KYC process. This accuracy, Bai explained, “is not only valuable for initial results but has downstream benefits as the cornerstone of understanding the customer.” Bai highlighted diversity in data, automated analytics, and user empowerment as three key differentiators between traditional legacy KYC and Socure’s latest offering.

“Socure’s market-leading identity fraud scores, (enable) an automated 90% customer acceptance rate, a 95% fraud capture rate, a 10% reduction in false positives, and over 50% reduction in manual reviews,” Bai wrote.

Founded in 2012 by Sunil Madhu, Socure most recently demonstrated its digital identity verification and fraud protection solution, Socure ID+, at FinovateFall in 2017. Recognized in March as one of America’s Best Startup Employers by Forbes, and named to Inc. Magazine’s Best Workplaces 2020 roster in May, Socure was also recently featured as a Gartner Cool Vendor in Artificial Intelligence for Banking and Investment Services.

Headquartered in New York City, Socure has raised nearly $62 million in funding from investors including ff Venture Capital, Scale Venture Partners, Commerce Ventures, and Flint Capital.

Crises, such as the current coronavirus pandemic, often bring out the best in us. But troubled times can also provide opportunities for unscrupulous and malevolent actors to take advantage of people’s anxieties and fears.

The hoarding of personal protective equipment that occurred early in the coronavirus crisis and the spread of crazy conspiracy theories about the origins of the virus have helped create a climate of fear and suspicion. This can make dealing reasonably and confidently with the crisis that much more challenging for all of us.

Unscrupulous and malevolent actors are also taking advantage of people’s financial anxieties and fears during this time. Our Fraudtech Digital Day – part of Finovate Fintech Halftime Review – will take a close look at how the cybersecurity threats before the crisis struck have intensified in many ways in the weeks and months since.

How big is the current cybersecurity problem for financial services firms and their customers? What technologies are being deployed to help financial firms and other businesses stay one step ahead of the fraudsters? How can businesses defend themselves against fraud while still providing the kind of seamless, digital experience consumers demand? These are some of the topics we’ll discuss as part of our FraudTech Digital Day.

To whet your cybersecurity whistle, we’re sharing excerpts from our conversation earlier this month with BioCatch co-founder and Chief Cyber Officer Uri Rivner. We spoke with Mr. Rivner about the new threats to cybersecurity that have arisen with the global public health crisis of COVID-19.

“Fraud isn’t going away and, in fact, we anticipate a surge in account takeover activity as criminals scale up their cash-out operations,” Rivner said. “They already have the data they need to steal more money, but they need to scale their infrastructure.”

BioCatch specializes in providing behavior-based authentication and threat detection solutions. Headquartered in New York and Israel, and founded in 2011, the company demonstrated its Passive Biometrics/Invisible Challenge technology at FinovateFall. BioCatch’s platform analyzes 2,000 behavioral parameters based on user-device interaction, and leverages this data to build real-time risk scores that provide continuous authentication and a superior defense against account fraud, social engineering scams, and more.

“We’ve taken a scientific field in cognitive studies, something that was working in the lab, and made it extremely practical for use in solving the biggest issues in online fraud,” Rivner explained. “(A)cross dozens of banks, credit card issuers and companies outside the financial sector, (we are) protecting over 100 million online and mobile users. We’ve tackled issues that were initially deemed impossible to solve.”

Here are some key takeaways from our conversation.

On the threat of increased fraud and cybercrime during the pandemic

If I had to pick one community that is definitely going to thrive during a global virus outbreak, it’s online fraudsters. They have a golden opportunity to scale their operations while entire companies move their fraud operations and analytics teams to a work from home model, which is not an easy process for, say, a major bank.

On the danger of identity theft and why behavioral-based authentication is key to fighting it

The most scalable fraud operation is opening credit card or personal loan accounts. All you need is to buy a bigger list of stolen identity records, and have a team of people opening accounts in other people’s names. Identity theft is reported to sky-rocket, and it can be quite dangerous, especially if it’s a new digital service that is launching these days. If a new digital service is targeted by a massive campaign, there will be more fraud applications than real applications – that’s disastrous.

Traditional defenses such as checking KYC (know your customer) data and device recognition no longer hold, and new technologies such as behavioral biometrics are used to stop such fraud campaigns and reduce false rejections due to high security bars.

On the role of enabling technologies and “the right kind of AI” to help fight fraud

Machine Learning can instantly look at thousands of features, resulting in an extremely accurate model that predicts fraud and can adapt itself when cyber criminals change their strategy. At BioCatch we have over 2,000 such features.

An important consideration though is that some machine learning models are a black box and don’t really provide insights into why a certain action is risky. BioCatch, for example, uses Explainable AI models to make sure customers can get the reasons why a score was high, as well as many negative and positive behavioral factors observed during a session.

CNBC reported today that Quicken Loans is planning to go public this year. Morgan Stanley, Goldman Sachs, Credit Suisse and JPMorgan are helping manage the deal.

Founded in 1985 by Dan Gilbert, Quicken Loans has risen to the ranks of the largest mortgage lender in the U.S. It’s unclear what the company will be priced. However, as CNN explained, “The targeted valuation is still being decided, but it is likely in the tens of billions of dollars… That would imply a multi-billion-dollar IPO, one of the largest – if not the largest – this year.”

The spike in mortgage refinances has been beneficial to the Michigan-based company. In April, Quicken Loans experienced the biggest month in its history, closing $21 billion in mortgages.

There is no official word on when (or if) the IPO will take place, but CNBC reports the offering could take place as early as next month.

In some parts of the globe, cities are slowly relaxing their social distancing guidelines. Businesses are beginning to open up and residents are once again venturing out to offices and into storefronts.

Some tech companies have made the move to become remote-first, keeping employees out of physical offices for the foreseeable future. Banks, however, face regulatory scrutiny over communication and documentation, and can’t allow their employees to work from home as easily.

So as many begin to let their guard down, where do a bank’s responsibilities lie in regard to maintaining a safe, virus-free work environment and branch location?

As with everything, the buck stops with the banks’ leadership. They are responsible for not only heeding guidelines from their local and federal governments, but also for understanding concerns of their customers and employees. To answer the question in the title, no, banks don’t necessarily need a chief medical officer. They do, however, need to appoint a person or a group responsible for creating safety measures around their branch and workplace.

The first step in doing this (aside from abiding by governmental guidelines) is to listen to the concerns of customers and of employees. While some may be ready to show up to the office or branch with minimum precaution, others may request increased social distancing in the office and curbside services at the branch.

Listening to these concerns will offer a clearer picture of next steps and a timeline. Options include offering individual cubicles separated by plexiglass, monitoring employee temperatures, increasing cleaning frequency to once-a-day, limiting the number of employees in the office and rotating work-from-home schedules, limiting customer numbers in the branch, requiring face masks, increasing sick leave for employees, etc.

If a requirement such as taking temperatures at the door arises that no one on the team feels comfortable with, hire an outside medical specialist. And if all of the new protocols seem completely overwhelming, banks should consider bringing on a consultant to help with things like deep cleaning protocols, updated health and safety plans, and emergency response plans.

Would it hurt to hire a Chief Medical Officer? Certainly not. But by listening to employees and clients and applying some creativity, banks can come up with a workable solution that helps both employees and customers feel safe.

In the wake of the tragic killing of George Floyd at the hands of a Minneapolis police officer, people around the world are showing remarkable support for the cause of African American equality. From every corner of the globe, and in cities and towns across America, people from all walks of life are increasingly committed to making sure that the slogan “Black Lives Matter” evolves from being a mere rallying cry to a new reality for millions of black Americans.

With this in mind, we want to share again our thoughts on ethnic diversity in our industry, fintech, where we are in terms of inclusivity, and where we need to go.

When the discussion of diversity in the tech world comes up, the conversation is typically oriented around gender diversity. But the call for greater inclusion in the tech world is not limited to gender; diversity along ethnic lines is also a goal that technology companies have increasingly begun to strive toward.

Perhaps the international nature of many technology enterprises, with tech entrepreneurs and tech talent truly arriving in Silicon Valley from all corners of the globe, serves to mask the relatively small number of tech firms in general, and fintech firms, in specific, that are run by Americans who are ethnic minorities. Indeed, an online search for “African Americans in fintech,” for example, is almost as likely to produce entrepreneurs from Nairobi, Kenya as from Newark, New Jersey.

Importantly, there are tech firms that have won admiration for the diversity of their teams. Slack, for example, was widely praised for its diversity report which, released in 2017, showed that the company had achieved better gender diversity than its Silicon Valley peers. The report also revealed that Slack’s workforce had as much as 3x the number of underrepresented minorities (African American, Latino/Hispanic, and Native American) as its peers. An Atlantic article from 2018 pointed out that where Slack had minorities in 13% of all technical positions and 6% in leadership positions, companies like Google and Facebook had less than 4% of their technical positions filled by underrepresented minorities.

Clinc CEO and co-founder Jason Mars during his company’s Best of Show winning demonstration at FinovateFall 2016.

How has fintech fared when it comes to ethnic diversity in its technical and leadership ranks? Finovate has hosted a handful of fintech companies with African American leadership over the years – Clinc and its CEO and co-founder Jason Mars, DarcMatter and its COO and co-founder Natasha Bansgopaul, are two that come to mind. And the industry writ large may have more founders of color than many think: Forbes celebrated the release of its Forbes Fintech 50 roster last year by featuring Ryan Williams, the young, African American CEO of mortgagetech firm Cadre on the magazine’s cover. And venture capital firms like Backstage Capital have made investment in startups with founders of color – as well as women and members of the LGBT community – a priority.

Nevertheless, even as the number of African American and Latino/Hispanic tech founders and leaders has grown, it remains true that there are fewer African American and Latino/Hispanic founders and CEOs in fintech relative to other areas of technology, including education and health-related tech fields.

One of the biggest problems that companies lacking in diversity can face is that it can make them less capable of responding to the needs of diverse markets. Fintech analyst Mary Wisniewski wondered in a 2018 American Banker article “Are black millennials a blind spot for fintech firms?” and noted that while millennials in general have developed a healthy skepticism toward banks, this wariness is all the more pronounced in young people from communities of color. Among the solutions offered are more minority-owned financial institutions, and an increased emphasis on financial literacy and wellness as an engagement strategy for younger minorities.

In this regard, fintechs like GRIND may become more well-known and popular. Launched last year and based in South Central Los Angeles where it caters to the local African American community, GRIND offers FDIC-insured debit accounts, a mobile banking app, and the ability to get paid two days earlier if they set up direct deposit with GRIND. Another example of this kind of company is Finhabits, a bilingual (Spanish/English) mobile investment platform launched by Carlos Garcia in 2015. Garcia, an MIT graduate with experience with Merrill Lynch and Galileo Investment Management, explained that the issue for Latino and Hispanic communities was not their ability to save, but their lack of familiarity with investing. “Our day-to-day money management is good, but planning for 15 years ahead is not” he said in a 2017 profile.

As fintech continues to diversify itself as an industry, one good note is that it appears that fintech may be helping alleviate some of the issues in financial services caused, in part, by a lack of diversity. A recent report from the FDIC on consumer-lending discrimination in the fintech era, for example, suggested that technology may be playing a positive role in reducing the discrimination in credit faced by Latino/Hispanic and African-American consumers in particular. The report specifically pointed to “new entry of fintech platforms” as well as digital improvements by incumbents for increasing competition and declining rate discrimination.

Symbiotic relationships, like the way bees help flowers pollinate while harvesting nectar to feed their colonies, can be found all over nature. They are also quite common in fintech.

The latest example of fintech symbiosis is today’s partnership between Amazon and Goldman Sachs. CNN reported this morning that Amazon revealed a lending program for U.S.-based small businesses that sell on its platform.

Goldman’s Marcus will offer revolving credit lines of up to $1 million. The loans will carry an annual interest rate of 6.99% to 20.99%. Minimum payments are due on a two-week cycle and if borrowers don’t use at least 30% of the funds, they are charged a maintenance fee.

Interestingly, the new offering will compete with Amazon’s existing small business lending product, which it launched with Bank of America in early 2018. According to CNN, last year Amazon loaned more than $1 billion to 14,000 sellers.

Goldman, which will service the lines of credit, will underwrite the loans using merchant data collected by Amazon (if the seller agrees to share their data). As CNN pointed out, this is a rare move by Amazon, which, “has kept a tight rein on its small business lending program, using algorithms and closely guarded sales data to determine who could use a loan.”

The data sharing doesn’t extend past lending opportunities, however. Goldman will only use seller data for lines of credit and will not use it to cross-sell other products or services. Additionally, Amazon won’t be able to access the data that Goldman collects from prospective borrowers.

The move makes Amazon the latest third party on Goldman’s list of partners for its Marcus brand, which caters to a younger and generally less wealthy client base. Furthermore, the partnership accelerates the bank’s mission to make Marcus a banking-as-a-service provider for third parties. Marcus’ existing partners include Apple, JetBlue, Intuit, and AARP.

The following is a guest post by Jake Rheude, Vice President of Marketing for order fulfillment companyRed Stag Fulfillment.

Fintech has dramatically shifted the way people and enterprises use and move money, and that’s increasingly impacting the world of ecommerce. While logistics is typically thought of a sloth when it comes to adopting innovative technologies, fintech may be a unique case because of the savings it generates, protection it offers, and where demands for adoption come from now.

The landscape is changing, and ecommerce is shifting in significant ways that are important to learn. If you’re in fintech, here are some major opportunities for your next solution.

Validation and KYC compliance

There’s a growing call for ecommerce brands and marketplaces to start focusing on better know your customer (KYC) compliance and services. Online payment fraud continues to rise and the European Payments Council notes that threats are demonstrating a greater degree of professionalism of cybercriminals.

Ecommerce companies are tantalizing targets as they grow larger or when it’s discovered that they lack significant security measures. KYC validation provides a very early deterrent by help collect and verify specific user information — from face IDs and credit card numbers to requirements to use only a verified current address.

It’s a security measure that ecommerce companies are happy to adopt. The lane for fintechs to work here is facilitating KYC programs (and even related AML regulatory checks) within their offering. In a growing number of cases, KYC is baked into fintech solutions, easing the burden on ecommerce and providing greater protection while also making it more of an industry standard.

Stores are looking beyond borders

Ecommerce makes more goods available to more people, regardless of where the company or the customer are. Early fintech helped establish the pathway that ecommerce-focused solutions are taking now.

SWIFT gpi (global payments initiative) made it easier for banks to manage and trace these payments. In early 2019, SWIFT announced a specific gpi link for ecommerce that included plans to use R3’s blockchain technology.

While much of the focus is on support bank payments and activities, this shift provides a unique opportunity for large ecommerce brands as well as those near country borders. When this or similar platforms become available, a company may not need a presence in another country to expand its reach there. Fast, affordable payment management could make it easier for ecommerce companies to work with a variety of payment providers for both their interactions with customers as well as supply chain partners.

When fintech simplifies cross-border payment management, it becomes easier for ecommerce to expand beyond greater boundaries or choose where to have fulfillment locations.

Ubanked shoppers are blending commerce

One of the more exciting fintech innovations for ecommerce companies is coming to stores near you. A well-known example comes from the Oxxo convenience stores in Mexico. More than half of Mexico’s shopping population lack bank accounts, but they still want to shop online. So, they make a purchase from select online merchants and then go to their nearby Oxxo store and pay for the products they selected. Someone who only has physical cash and no bank account is able to buy goods only sold online.

It’s a “low-tech” solution that takes innovative fintechs to pursue. It’s also an extremely rich opportunity. According to 2017 data, there are about 1.7 billion unbanked adults in the world. There’s a good chance, however, that this group overlaps with the ever-growing number of Internet users (about 4.54 billion as of January 2020).

We know about two-thirds own a phone, so as these consumers shift to smartphones and gain access, there’s a big place for fintechs to support ecommerce growth.

Better behind-the-scenes payments

Ecommerce relies heavily on the logistics sector and these both interest with fintech at multiple locations for every sale. The problem with all the financial movement of payments, insurance, product handoffs, etc., is that there’s a lot of opportunity for receipts and bills to go missing. Sometimes it is accidental, other times fraud.

Fintech services that aim to automate payment processing during handoffs can protect everyone. This potential is growing with the adoption of more supply chain DLT offers. Ecommerce companies are part of this when their fulfillment partners, suppliers, and manufacturers join such blockchains.

This cost-reduction and risk mitigation is often felt most by the carrier. The move into ecommerce is likely going to be driven by these carriers and logistics partners.

APIs will shape the future

In many emerging fintechs, as well as regtech (regulatory technology), the API dominates the way information is collected, used, shared, and reported. They simplify the way banks and fintechs interact with each other as well as how ecommerce companies manage payments and budgets.

Today, API use is somewhat limited, and most ecommerce merchants won’t think much about it beyond if a payment API integrates with their platform or not. However, this is likely the area of most impact for our future, even if we can’t see what that will be. It’s likely to be beyond simply moving to the cloud.

One possibility will be their ability to connect fintech and ecommerce companies in a way that customers don’t see a difference. Right now, if you shop on Amazon, you might get an offer like saving 10% by opening up an Amazon-branded credit card. API innovations could allow any ecommerce company, of any size, to offer the same based on user data.

Imagine instant (digital) point-of-sale consumer loans and financing, loyalty programs that work across merchant categories, mobile wallet integration, and more.

What might be the biggest fintech revolution, and one we hope to see, is easing ecommerce company requirements. Adopting a platform API might be all a company needs to do now to get continual access to the latest security updates and payment options when the fintechs that build these innovations join the API community.

APIs already run significant warehouse and fulfillment operations, meaning there’s a goldmine of data to be leveraged for everyone at the table, if fintechs make it easy for ecommerce companies.

Budgeting and financial comparison platform Status recently made a tweak to its business model. Company Founder and CEO Majd Maksad recently sent an email to users saying that the company launched a premium membership option.

The app will still offer free access but the premium membership unlocks advanced features and the ability to earn cash rewards for simply using the app. Interestingly, the premium membership will be income-based. Maksad explained, “The app remains free for everyone– but depending on your income, you may be asked to make a contribution to access the Premium features and rewards. You can choose your own contribution amount based on what you think is fair.”

Users can choose contribution levels ranging from $1 per month to $20 per month. However, if the user opts to contribute $1 or $2 per month, they receive a message saying, “A little goes a long way. Please consider contributing $3 or more.”

The premium option unlocks most of the features users were previously enjoying for free. In the screenshot below, the yellow locks in the sidebar show the features behind the paywall.

Status noted that it didn’t take lightly the decision to add a fee. However, the company said that the additional revenue is “crucial” for it to develop new features. “Any contribution you choose to make will also help us continue serving lower income members for free,” Maksad added.

Status’ main business model relies on referral partnerships with companies including Airbnb, AllState, Liberty Mutual, Betterment, VSP, and Haven Life. However, with the VC funding forecast looking bleak, the company probably realized it needed an alternative way to generate capital in order to stay afloat and invest more into the product.