This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

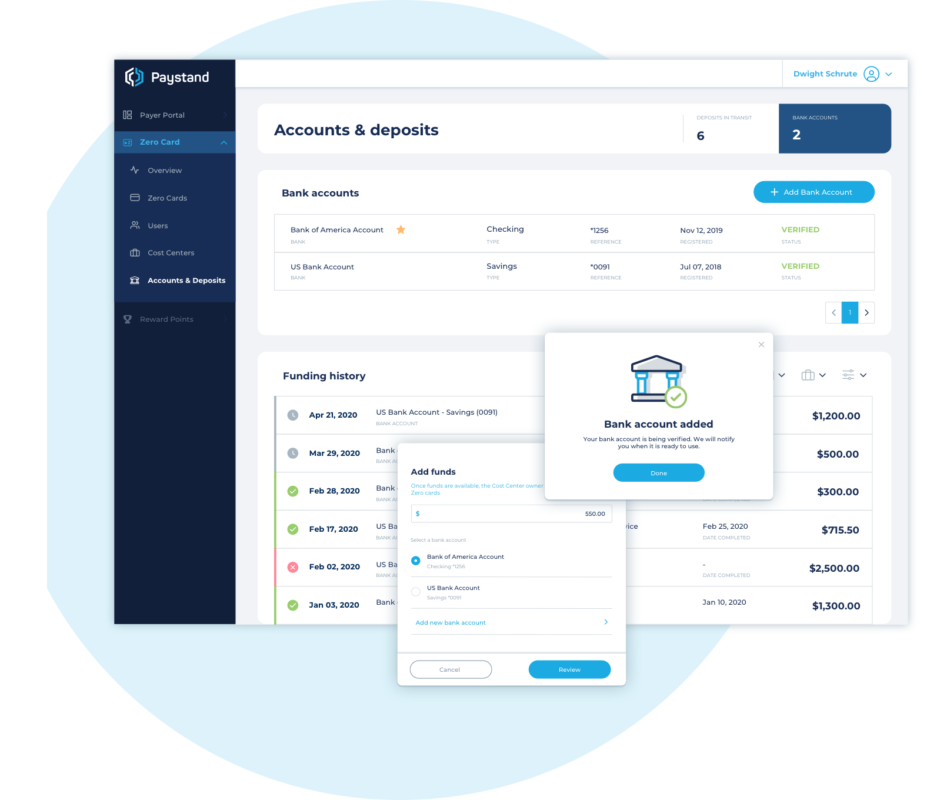

Paystand’sZero Card, launched today, offers businesses a touchless, prepaid corporate expense ePayable solution that leverages Paystand’s zero-fee payment network to eliminate the cost of transaction fees.

Geared to help mid-market businesses in particular, which often require a high degree of flexibility and control over their budgets, the Zero Card streamlines expense management operations such as invoice processing, expense reporting, and payment execution. The prepaid virtual expense card also enables businesses to manage, track, and control spending in real-time. The offering includes fraud prevention controls and the ability to capture and add critical remittance data to transactions to make expense reporting and reconciliation easier.

“The Paystand Zero Card combines the consumer-like experience of peer-to-peer payments with the speed and security of Paystand’s no-fee payment network,” Paystand CEO Jeremy Almond said. “We completely re-engineered the corporate card so businesses can move away from reactive spend management tactics to a place where they have visibility of spend before it happens.”

One of the aspects of the Zero Card the company is touting is the way it brings a common payment infrastructure to accounts payable and accounts receivable operations. In its statement, the company referred to this disconnect as “one of the biggest challenges in B2B payments today,” which pits payers and receivers against one another as “technology and process improvements for one group often lead to inefficiency and friction for the other.”

In contrast, the Zero Card is designed for both accounts payable and accounts receivable, natively connecting both AP and AR to keep costs low, ensure swift and secure payments, and effectively bridge what the company calls “the payables gap for B2B payments”

Challenges like the payables gap, according to Paystand VP of Marketing Mark Fisher, are why he believes B2B payments have “a long way to go before it achieves the ease and speed of consumer payments.” Fisher credited the Zero Card for helping B2B payments catch up. “When money moves over our network,” he said, “it’s instant, automated, and comes at no cost. That’s good for businesses and that’s good for the economy overall.”

Founded in 2013 and headquartered in San Francisco, California, Paystand secured $20 million in funding in February in a round led by DNX Ventures. Mitch Kitamura, Managing Director at the firm put the company’s latest offering in the broader context of the “cashless transformation” led by fintech innovators like Paystand. In a statement, he referred to the Zero Card as “a critical step … in driving more seamless interaction between businesses to help realize the true economic value of digital infrastructure.”

If there are any lingering doubts about the power (and popularity) of the Buy Now Pay Later (BNPL) movement, installment payments platform Splitit has 71.5 million reasons to cast those doubts aside.

The New York-based company, which made its Finovate debut as PayItSimple in 2014, announced that it has raised $71.5 million in a private placement and share purchase plan (SPP). With institutional investors such as Woodson Capital Management, the company plans to use the capital to “accelerate sales and marketing, plus (make) further investments in product and technology” according to a statement. Splitit boasts more than 1,000 ecommerce merchants using its technology, and 300,000+ shoppers with an average order value of $893.

Splitit’s fundraising comes as the company reports record Q2 growth, including processing more than $65 million in merchant sales volume, and growth of 1.76x quarter over quarter and 2.6x year over year. In discussing the company’s success, CEO Brad Paterson credited a new willingness on the part of consumers to “maximize their existing credit to preserve cash flow” while at the same time not incurring additional new debt.

Paterson also noted that while the COVID-19 crisis has helped move digital transformation in ecommerce toward the top of the agenda, it was important for those involved in payments to make it easier for merchants to accommodate their customer’s cash management requirements.

As such, it’s hard not wonder if, once again, crisis is responsible for accelerating innovation. After all, one of the initial innovations in retail, the layaway program, emerged during the Great Depression as a way to maintain at least a minimal level of consumption of non-essential goods during a severe economic retraction. By enabling customers to pay for items in small increments over time and then receive those items once they had been fully paid for, the growing retail economy was able to survive an extended period of historically low demand.

The buy now pay later phenomenon is layaway in reverse, allowing customers to gain the benefits of the purchase immediately and moderating the impact of the cost by paying for that purchase over time. But the goal – to accelerate consumer activity and expand the ability of people to spend – remains the same. The only difference is that layaway tended to disappear once credit cards became ubiquitous, while buy now pay later appears to be rising at a time when we are realizing that affordable consumer financing might not be as ubiquitous as we thought.

For Finovate fans, Klarna has been the pioneer in the Buy Now Pay Later space, with fellow alums like Sezzle also earning recognition for its interest-free buy now pay later option. Founded in 2005 and 2016, respectively, both companies are reminders of how fintechs have been providing consumers with alternative financing options well before the coronavirus hit.

That said, it is clear that COVID-19 has stimulated interest in Buy Now Pay Later options. The Business of Finance reported earlier this week that BNPL had become “fashion’s go-to during the pandemic.” Also this week, American Express announced that it would extend its buy now pay later service to more of its cards. The Wall Street Journal featured Australian Buy Now Pay Later specialist Afterpay at the beginning of this month in the wake of the firm’s announcement that it had signed up more than 1.6 million U.S. users since the onset of the coronavirus in March. And Shopify announced this month that merchants on its platform would have access to BNPL financing from installment payment company Affirm. Affirm looks like it is ready to maximize the Buy Now Pay Later moment with an initial public offering, according to reporting in the Wall Street Journal.

Even the big banks are getting into the Buy Now Pay Later game. Goldman Sachs has introduced a new, installment payment feature called MarcusPay – in partnership with JetBlue Airways – as part of a bigger “build-out” of its Marcus by Goldman Sachs digital banking platform. This week, Citi partnered with Amazon to launch its own BNPL offering Citi Flex Plan.

Place another notch in the belt of the challenger banking crowd. This week banking alternative Bnextextended its Series A round by $13.08 million (€11 million), adding to the $26.7 million (€22.5 million) the bank brought in last October.

Bnext’s Series A round now stands at $39.2 million (€33 million) and its total funding is now in excess of $47 million (€40 million). Existing investors DN Capital, Redalpine, Speedinvest, Founders Future, Enern, Digital Horizons, Kreos Capital, and Cometa contributed to this week’s follow-on round.

Bnext will use the funds to further its growth in its home territory of Spain, as well as build its presence in Latin America by focusing on its expansion into Mexico. The bank initially launched in Mexico at the beginning of this year and now has 60,000 users in the region.

“At Bnext we have always had a clear objective: to be a banking alternative that allows our users to end the bad experiences of traditional banks,” said Bnext CEO Guillermo Vicandi. “Since its launch, our growth has been constant both in services and products and in users, and we are proud to have the support of the best investors to design and execute a strategy that allows us to achieve our objective. Our position to change the banking sector in the Spanish-speaking world is unbeatable and we have a duty to take advantage of it.”

The challenger bank has amassed 400,000 clients since it launched in 2018 and currently processes $119 million (€100 million) per month in transactions. Last month Bnext launched its Premium account and added to its Rewards program.

The latest offering from Envestnet | Yodlee enables financial service providers to combine actionable insights, peer benchmarking, and personalized views to build digital financial experiences that better serve and engage their customers across channels. Insight Solutions, unveiled today, provides a set of new APIs that will help companies leverage data to improve the quality of their virtual financial assistance offerings.

“Hyper-personalization is the new baseline for success, and financial institutions and FinTechs who have a more advanced understanding of consumers and tailor their offerings accordingly will have a strategic and competitive advantage,” Envestnet | Yodlee SVP of Product Brandon Rembe said. “Through our Insights Solutions, financial service providers will have access to meaningful consumer insights faster and more affordably than by growing their own data science team.”

Users will be able to take advantage of features like predictive cash flow; spending, credit limit, and refund monitoring and alerts. The new tool will also provide transparency into subscription-based and other recurring expenses. The solution puts the power of machine learning and algorithms to work to provide users with a comprehensive overview of their personal finances, enhancing their ability to save for retirement, build an emergency fund, as well as manage their everyday spending.

With more than 26 million users worldwide, more than 1,300 partners (including 16 of the top 20 U.S. banks), and 50+ patents, Envestnet | Yodlee offers data aggregation and analytics technology solutions that support financial wellness and sound wealth management. Envestnet acquired Yodlee, one of Finovate’s oldest alums and a multiple-time Best of Show winner, in 2015 in a deal valued at $660 million.

Envestnet | Yodlee began this year with the acquisition of financial data aggregation and analytics platform, FinBit.io. This month, the company issued a report looking at income and spending trends during the COVID-19 crisis. In the form of an eBook, the report looks at how retailers in different industries – from restaurants and transportation to barbershops and gaming – were impacted by consumer behavior shifts due to the economic effects of quarantines, lockdowns, and other efforts to fight the pandemic.

Barrons featured Envestnet co-founder and current CEO Bill Crager in an interview last month. Crager took the helm at the company after the tragic death of previous Envestnet CEO Jud Bergman in a 2019 automobile accident. Crager discussed the personal and professional challenges of the succession, as well as plans for 2019 acquisition MoneyGuide, and the company’s strategy for serving its clients during the global pandemic.

Envestnet | Yodlee is a publicly traded company – ENV on the New York Stock Exchange – and has a market capitalization of $4.4 billion.

Point of sale financing is all the rage in fintech right now. Consumers are looking to continue buying habits despite lower income and merchants are vying for ways to boost consumer spending.

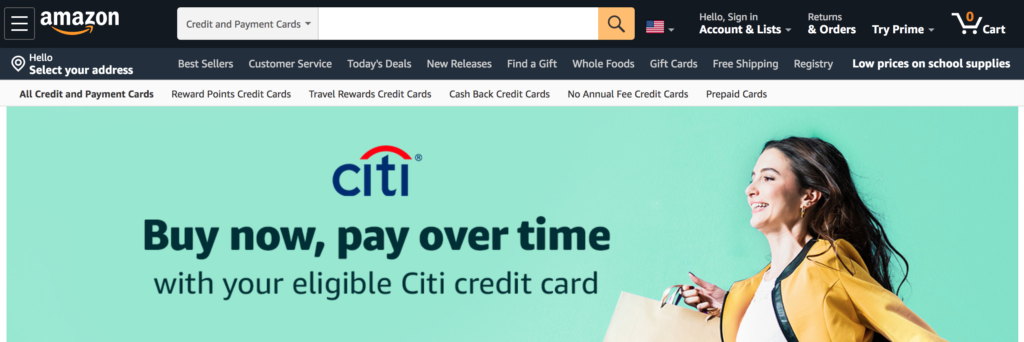

So when it comes to one of the biggest online merchants launching a buy-now-pay-later offering, its a big deal. It is, anyway for Citi, which struck up a partnership with Amazon this week to provide a buy-now-pay-later option for Citi credit cardholders.

The tool is called the Citi Flex Plan and offers Citi credit cardholders a way to pay for larger purchases over time. Loan terms range from three to 48 months with terms ranging from 6.74% APR to 8.74% APR depending on the amount financed. Borrowers face no credit inquiries, no incremental fees, and are not required to fill out a formal application.

“Amazon is one of the most popular destinations for our customers to shop and redeem ThankYou Points,” said CEO of Citi U.S. Consumer Bank Anand Selva. “We want to meet them where they are with another instant, convenient and easy payment option.”

Essentially, Citi cardholders have two forms of credit in one when they shop on Amazon. How do the logistics work? When they place their order, the total purchase amount will be deducted from their available credit. The monthly payment– the amount that varies based on the purchase price– is due to Citi at each billing cycle.

After Citi initiated a partnership with Google in 2019 and yesterday’s news of six more traditional banks following suit, today’s announcement comes as no surprise. Challenger banks are on the rise, and consumers are opening new accounts with these alternative banking providers at a faster rate than before.

By providing its customers with the new buy-now-pay-later option, a traditional financial services provider such as Citi is appealing to the lower income group that is most attracted to challenger banks. The bank is also helping to position its card at the top of consumers’ virtual wallets when they shop at Amazon. This is key since more than one-third of active Citi cardmembers made at least one purchase on Amazon in the past year.

Additionally, partnering with a big tech company helps Citi align more with the tech side of banking. And indeed, the bank has been closer to the forefront of fintech than many of its rivals. At our developers conference Citi showcased its developer hub and sandbox.

Super app Grab is becoming a lot more super. That’s because the Southeast Asia-based company that specializes in transportation, food delivery, and payment solutions is expanding into direct-to-consumer services.

Three new consumer-focused services are launching under Grab’s Thrive with Grab strategy. The new initiative builds off of the company’s merchant services strategy, Grow with Grab, that launched last year. In contrast, Thrive with Grab “aims to empower individuals to grow their personal wealth, manage their finances and protect what they value.”

At launch, Grab’s three consumer-focused services include a loan marketplace that aggregates loan offers from third party providers, a buy-now-pay-later payment offering with partner merchants, and AutoInvest, a micro-investment solution that allows users to invest small sums of money while spending in Grab’s ecosystem.

“As a leading fintech company in Southeast Asia, our ‘Thrive with Grab’ strategy will enable users to build their wealth, manage their finances, and protect what they value during this uncertain period,” said Grab Senior Managing Director Reuben Lai. “By offering innovative micro-transaction-based financial services, convenient financial management tools, and access to products from leading global financial institutions, we hope to unlock the tremendous potential in financial services in the region in ways that serve all Southeast Asians.”

The launch of the three new services is Grab’s second foray into the direct-to-consumer space. The company launched an insurance offering in April of last year and has since issued more than 13 million insurance policies.

Reuben said that the goal of the new launch is to “empower individuals and small businesses across the region to meet their diverse needs through financial services by delivering products and solutions that are accessible, transparent, and convenient.”

Grab raised $856 million in February and yesterday announced a $200 million round, bringing its total raised to over $10 billion and boosting its valuation to over $14 billion. Anthony Tan co-founded the company in 2012 with Tan Hooi Ling and now serves as CEO.

Much of the technology world is puzzling over Microsoft’s moves toward a purchase of popular and controversial social media app TikTok. But more discerning observers may spend more time considering the ramifications of Apple’s $100 million acquisition of Mobeewave.

Based in Montreal, Quebec, Canada, Mobeewave enables contactless payment acceptance simply by tapping enabled smartphones (or credit cards) to another enabled device. Mobeewave’s app leverages NFC (near field communications) technology, a feature that has been on the iPhone since 2014, and could allow the devices to be more effectively used by merchants to process in-person payments. This spring, the company introduced its latest contactless payment solution, Mobeewave Limitless, that provides the varied authentication, regulatory controls, and Cardholder Verification Method (CVM) standards required by regulators in North America, Europe, and APAC when it comes to supporting high value contactless transactions.

As such, the acquisition puts Apple in competition with Square, which has been a leading innovator in providing merchants with a hardware/software combination to enable smartphone and tablet payment processing. The option of a hardware-free alternative – sans dongles and readers – could make Apple an instant player in the small business payments space.

Typically tight-lipped about its acquisitions, Apple said in a statement that it “buys smaller technology companies from time to time and we generally do not discuss our purpose or plans.” We do know that Mobeewave’s team will be retained and will continue to operate out of its Montreal headquarters.

One thing that’s especially interesting about the acquisition is that Mobeewave had agreed last fall to integrate its contactless payments technology into Samsung mobile devices, and had expected to deploy the solution worldwide this year. Samsung is also an investor in Mobeewave, having played a leading role in the Canadian company’s Series B round in January. Mobeewave has raised a total of $26.6 million in funding.

This is a guest post written by Shannon Flynn, managing editor at ReHack.com.

People in the fintech industry have inevitably heard about smart contracts. Here’s how they’re shaping the sector and why some parties may ultimately decide not to adopt them yet.

How do smart contracts tie into the rise of decentralized finance?

Anyone who asks a search engine “What is a smart contract?” will quickly discover it’s a computer code on the decentralized digital ledger system called the blockchain.

Entities ranging from utility to health insurance companies are investigating how smart contracts could help them do business while keeping information safe. Their increasing popularity helped spark the creation of the decentralized finance sector — DeFi for short.

A person located anywhere in the world could access a DeFi account with an internet connection. They can then carry out transactions typically associated with banks without going through those entities or intermediary influences.

Estimates say there are about a billion dollars connected to the DeFi industry now. That’s a relatively small amount compared to centralized finance, but DeFi is worth people’s attention. It offers new opportunities to invest, borrow, and lend, appealing to parties unhappy with traditional investment options. Some DeFi companies using smart contracts let individuals earn cryptocurrency tokens redeemable for platform governance rights.

What’s happening with smart contracts so far?

You can think of smart contracts as business rules translated into software since they work on an if-then basis. One required action triggers a related event. The parties involved set the parameters, and the smart contract automatically upholds them.

In one trial, Spanish banks investigated using smart contracts to administer instant credit transfers. The company that assisted with the rollout clarified the system could work for sending money for any reason.

Similarly, in Singapore, financial authorities recently completed the fifth phase of an initiative called Project Ubin by examining blockchain-based options across a multicurrency payments network. Real-world tests validated smart contracts for various arrangements, including conditional payments and escrow for trade.

IBM announced an upgrade to its smart contracts offering, too. It allows multiple parties to propose and amend alterations to existing smart contracts instead of only accepting or denying others’ proposals.

How do smart contracts work when used with property purchases or loans?

People in the fintech industry often encounter individuals who need business loans or want to take out mortgages for their dream homes. Research indicates about 83% of people are slightly or not at all familiar with cryptocurrencies. Education could show them that smart contracts and related technologies ease the stress of milestone transactions.

Increased speed is one smart contract benefit. However, advantages span beyond the initial signing of paperwork. Once a person’s loan gets approved, they could use an encrypted key to sign the offer, and their signature becomes a unique blockchain entry. Funding and property title transfers also become entries on the ledger. Mortgage approvals and loan term agreements take days, not months.

Smart contracts and the blockchain can help mortgage servicers track borrowers’ payments, too. Plus, if a homeowner wants to refinance a mortgage or sell their property, the blockchain records for the duration of the smart contract to confirm ownership.

What other benefits exist?

Ironing out financial agreements with smart contracts could also make good cost sense. One company offering smart contract-based mortgages in California and New York plans to offer lower rates than banks, and customers may get loans packaged together and sold as securities.

Some analysts think smart contracts could help the economy stave off a recession, preventing prolonged challenges in the housing market. Each intermediary that finalizes a home-buying process adds 1% to 2% of the total property value to the transaction costs, statistics show. Smart contract automation can reduce third-party involvement, cutting costs and delays.

Efforts to use smart contracts could close the gap between investors and investment managers as well. An investment manager might initiate a smart contract that carries out a client’s wishes and avoids missed opportunities.

Several companies are investigating smart contracts to facilitate vacation rentals at lower-than-average rates. They believe the smart contracts would settle disputes faster and facilitate speedier cross-border payments.

What are the downsides of smart contracts?

Smart contracts aren’t without potential faults. One investigation showed that 25% of smart contracts studied contained critical bugs, with 60% having at least one security flaw.

Moreover, these contracts are only as “smart” as the programmers creating them. The code cannot recognize and bypass mistakes. Although errors could be less frequent than traditional contracts — especially with experienced, meticulous developers — the possibility remains.

A World Bank examination of smart contracts concluded they’re not always the best choice for every scenario. One example was that they could lower the cost of providing insurance and perhaps automate payouts. However, if used with short-term unsecured loans, smart contracts would not significantly improve a borrower’s creditworthiness.

Not all analysts agree that the benefits of smart contracts surpass those associated with conventional ones. They see them as an interesting idea that works best in the experimental realm instead of the real world. Smart contracts are still relatively rare, too. People in fintech and other industries may balk at using them since they’re newer and could introduce unforeseen issues. That could change if overall adoption rates rise, however.

Food for thought in fintech

This overview introduces how smart contracts work and proposes appealing ways to use them in the financial sector. Given the associated limitations, you may still have some unanswered questions, and that’s okay. The ideal approach is to view smart contracts as options that could positively change the industry but are not problem-free.

ShannonFlynn is a technology and culture writer with two plus years of experience writing about consumer trends and tech news.

Step aside, challenger banks. Google and a band of eight traditional FIs are coming for you.

News broke this morning that six financial institutions have joined Citi and Stanford Federal Credit Union in offering checking and savings accounts through Google Pay. The new banks include BankMobile, BBVA USA, BMO Harris, The Coastal Community Bank, First Independence Bank, and SEFCU.

These new accounts will leverage Google Pay’s existing infrastructure, which will serve as the front end of a fully digital banking experience.

BBVA announced today that its accounts will launch in 2021 as co-branded, FDIC-insured accounts. The bank will provide the account, while Google will provide the front-end, user experience, and financial insights. The collaboration will be facilitated by the BBVA Open Platform, the bank’s open banking initiative.

“BBVA has focused for decades on how it could use digital to advance the financial industry and, in so doing, create more and better opportunities for customers to manage their financial health,” BBVA USA President and CEO Javier Rodríguez Soler said. “Collaborations with companies like Google represent the future of banking. Consumers end up the true winners when finance and big tech work together for their benefit.”

Aside from the list of bank partners, there are not many details available about the new, hybrid accounts. Tech rumor site 9 to 5 Google speculates, however, that Google with leverage the partnerships to issue its own branded debit card.

ZenBusiness, an Austin, Texas-based company that specializes in serving micro-businesses, announced late last week that it has closed its first acquisition. The company has purchased fintech platform Joust in a move that will bring Joust’s business banking features to the ZenBusiness platform, and enable the firm to re-launch as ZenBusiness Money later this year.

The terms of the acquisition were not disclosed.

CEO and co-founder of ZenBusiness Ross Buhrdorf called the acquisition an opportunity to extend its “mission to provide the nation’s 57 million micro-businesses with exceptional and friendly tools that simplify the process of forming and running their business.” Founded in 2015, ZenBusiness helps entrepreneurs complete the necessary filing and paperwork to ensure compliant formation of their business, and provides a variety of additional services – from identity theft protection and business management tools – to help micro-businesses grow and expand.

Also based in Austin, Texas, Joust offers merchant services and business banking for entrepreneurs, freelancers, and the self-employed. The company, which merged with LoanDolphin earlier this year to scale mortgage reverse auctions, was a finalist at the 2020 SXSW Innovation Awards, and raised $11 million in funding prior to its acquisition by ZenBusiness. Joust was launched in 2017.

“We believe all entrepreneurs should have access to the same banking services reserved for large companies,” former CEO and Joust co-founder Lamine Zarrad said. “By bringing our financial tools to the ZenBusiness platform, we will quickly scale up and empower even the smallest businesses by simplifying and strengthening their daily operations while protecting their interests.”

ZenBusiness has raised $19.5 million in funding from 11 investors including Greycroft and Lerer Hippeau. The company was featured last December by The Jeruslem Post in its look at the top seven business formation services in the U.S.

Village Capital has unveiled the names of the 12 companies that will participate in its Finance Forward Latin America 2020 accelerator program. The incoming cohort will get five weeks of training to help them improve their business models and tailor their solutions for the current demands of the marketplace. The top two peer-selected startups will be eligible to receive $50,000 each in grant funding from program partner MetLife Foundation. Startups ranked third to fifth each will receive $16,000 in grant funding.

What do the 12 startups chosen – from an applicant pool of more than 140 – suggest about the state of fintech innovation in Latin America?

First of all, in some ways, the geographic distribution of companies is representative of what we see in terms of fintech’s strength in the region. Mexico has three representatives, Argentina has two, and Brazil and Chile both have one. Perhaps more surprising is the representation from Colombian fintech, with the country bringing five startups to the program.

Village Capital notes that the selected startups also reflect impressive gender diversity, with more than 80% of the participating companies having one or more female founders. The accelerator also credited the more than 40% of these companies that are innovating “outside major fintech hubs.”

The startups are involved in a wide range of fintech focus areas – from debt management and credit services to e-commerce, “buy now pay later” solutions. Many of these firms offer innovations that are particularly geared toward un- and under-banked populations. Among the more interesting startups in this category are Fundefir, a Colombia startup that specializes in bringing credit and insurance to the underbanked, and Quipu Market, also based in Colombia, which offers an e-commerce marketplace that enables informal microbusinesses to buy and sell locally using community tokens rather than cash.

Village Capital’s accelerator program features the support of PayPal and Moody’s, as well as MetLife Foundation. Since its launch in 2009, Village Capital has worked with more than 1,000 early stage entrepreneurs via its accelerator programs.

“The coronavirus pandemic has had devastating financial effects on low-income populations in Latin America,” Regional Manager for Village Capital Daniel Cossio said. “Now more than ever, tech-driven innovation can be at the forefront of helping small businesses stay afloat, families manage their income, and the region embark on what is bound to be a challenging recovery.”

Some of the more recent research on fintech in Latin America includes this February report from CB Insights, which helps provide context for the expectations many analysts had for the region at the end of 2019. For insights since the COVID-19 crisis, the May discussion published by Latin America Reports shows how fintech has played a “stabilizing” role in helping businesses and individuals cope with the economic and social impact of the pandemic.

Here is our weekly look at fintech around the world.

Payment solutions provider Cohort Go teams up with Brazilian bank Itau as it expands into the country.

Konsentus and Open Vector collaborate to bring open banking to financial institutions in Latin America and Canada.

Asia-Pacific

Hong Kong payments network infrastructure startup EMQ raises $20 million in funding to accelerate cross-border payments.

Venio, a mobile app that specializes in providing financing in emerging markets, goes live in the Philippines.

AEE News Today profiles Malaysian fintech Instapay Technologies which recently partnered with Mastercard to launch an e-wallet service for migrant workers.

Sub-Saharan Africa

Alegra, a cloud-based accounting software provider based in Colombia, announces expansion to Kenya, Nigeria, and South Africa.

Airtel Africa teams up with Mukuru to enable cross-border payments.

Mobile money operators are among the biggest players in fintech in sub-Saharan Africa. TechZim reviews the state of mobile money in the southern part of the continent.

Central and Eastern Europe

A biometric facial recognition-based payments system developed by Romanian fintech PayByFace goes live in Bucharest’s Tucano Coffee shops.

Nordigenscores payments license from Latvia’s Financial and Capital Markets Commission (FKTK), enabling it to provide account information services.

Lithuania’s Bankera introduces business loans for SMEs.

Middle East and Northern Africa

Arabian Business takes a look at the rise in popularity of buy now pay later platforms in the UAE.

Dubai International Financial Centre inks Memorandum of Understanding (MoU) with China’s Jiaozi Fintech Dreamworks.

Al Khaleej Today profiles Saudi Arabia-based payments company Tap Payments and its initiatives to help small businesses during the COVID-19 crisis.

Central and Southern Asia

Indian online investment and wealth management platform, Paytm Money, introduces new Chief Executive Officer Varun Sridhar.

Uzbekistan’s first digital bank, TBC Bank, goes live with technology from Capital Banking Solutions.

Niyo, an India-based neobank, acquires mutual fund investment platform Goalwise.

Remember when the mobile payments game was first getting started? The industry was rallying around NFC as the technology of choice for mobile payments. Bluetooth low energy (BLE) was a close second, and QR codes were generally the last choice.

That was in 2012 and now it appears that 2020 is throwing us yet another curve ball– QR Codes are back in style in the U.S. That’s because PayPal has partnered with InComm to launch its PayPal and Venmo QR codes technology at pharmacy chain CVS.

This move will implement low-touch mobile payments at CVS’ 8,200 brick-and-mortar stores across the U.S., offering shoppers a secure payment experience without needing to touch a keypad or sign a receipt.

PayPal users can pay using stored debit or credit cards, bank accounts, their PayPal balance, or PayPal Credit. Venmo users can also pay using their stored debit or credit cards and bank account, but will additionally be able to tap into their Venmo balance or Venmo Rewards.

“In the midst of COVID-19, we have seen an incredible acceleration of digital payments and touch-free payments,” said PayPal EVP and CPO Mark Britto. “Companies of all types and sizes are looking for ways to maintain the safety of their customers and employees, especially through touch-free experiences like curbside pickup and enhanced online shopping. QR codes complement these and provide retailers an additional payment method that furthers this touch-free mission and continues the growth of digital payments for all partners in the ecosystem. The essential nature of pharmacies makes CVS Pharmacy the perfect initial partner for PayPal and Venmo QR Codes – and we’re proud to help their customers stay safe while purchasing what they need.”

This week’s deal also marks a multi-year agreement between PayPal and InComm. The partnership enables InComm to distribute PayPal QR Code technology to its network of retailers, allowing them to integrate the QR code payment technology into their POS terminals.

PayPal has been touting its touch-free payment technology amidst the COVID-19 pandemic (see below). And given the payment giant’s previous traction and existing user base, the company will certainly come out on top as a winner in the post-pandemic economy.

Elsewhere across the globe, QR code payments have already seen success. Ant Group’s Alipay uses QR codes for in-store payments and had over a 50% adoption rate at the end of 2018.