This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

Virtual Banking Assistant from Fiserv enables you to deliver intelligent, AI-driven conversational experiences to grow, retain, and engage your consumers while reducing your call center costs.

Features

Out-of-the-box AI — leverages conversational AI

Contextual, natural language understanding — supports complex conversational flows

Dynamic financial information — provides actionable, proactive insights

Why it’s great Virtual Banking Assistant understands messy, unknown language and promotes financial health while gaining actionable insights. This platform provides real-time banking assistance across all channels.

Presenter

Deniz Kaya, Director of Product Management Kaya is Director of Product Management and is responsible for setting the vision and strategy for the Fiserv integrated AI and data products. LinkedIn

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

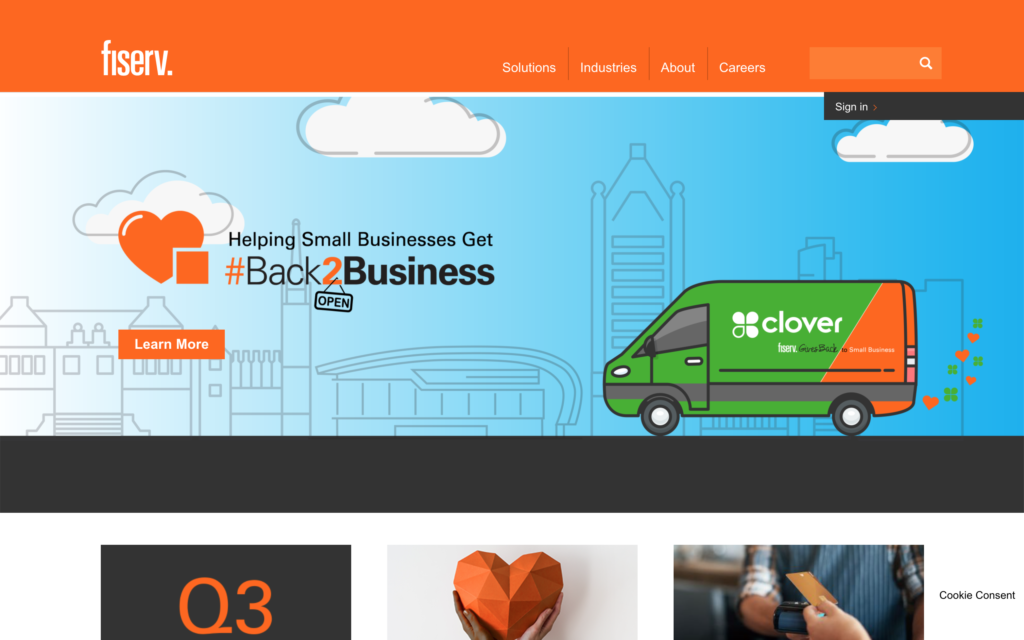

Interface is a leading intelligent virtual assistant provider. At FinovateWest, see its AI-powered call center that automates 60% of calls in 60 days while ensuring the best customer experience.

Features

Automate 60% of calls in just 60 days

Instant responses to pre and post-authentication questions

Save over $2.5M annually with approximately $1B in assets

Why it’s great Automate 60% of calls in 60 days with Interface’s AI-powered call center. ROI: ~$1B Assets – $2.5M savings annually ~$5B Assets – $10M savings annually ~$10B Assets – $20M savings annually

Presenter

Srinivas Njay, CEO Njay has decades of AI-research and experience leading digital strategies to scale. Banks inspired Njay to embark on a mission to enable financial wellness through AI, with Interface. LinkedIn

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

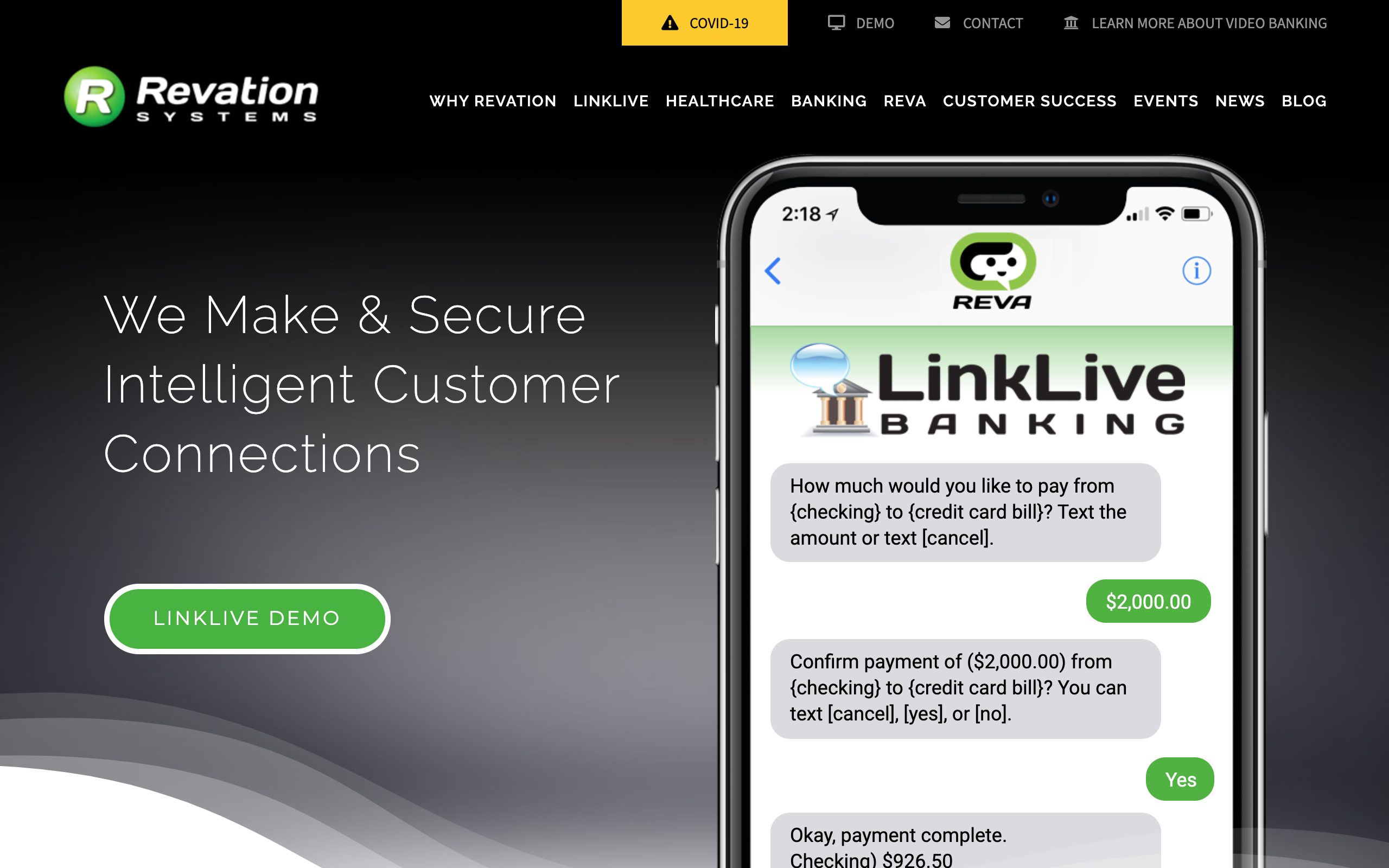

Revation‘s LinkLive brings the virtual lobby to the customer and simplifies digital appointment scheduling and conferencing – all in one solution.

Features

Digital appointment scheduling built on top of secure messaging

Dynamically routed calendar requests for real-time servicing

Permanently eliminating the need to schedule a web conference

Why it’s great Layered on top of LinkLive’s secure messaging foundation, online appointment scheduling and conferencing help banks digitize and virtualize all silos of their business.

Presenters

Patrick Reetz, SVP of Products & Markets Reetz is an innovator who has helped banks define and deliver on their digital destinations. Reetz supports Revation’s mission of elevating digital customer service. LinkedIn

Perry Price, CEO Price is a lifelong entrepreneur and a veteran in the telecommunications industry. Price set out to create the most secure platform in the marketplace. LinkedIn

A look at the companies demoing at FinovateSpring Digital on May 10 through 13, 2021. Register today and save your spot.

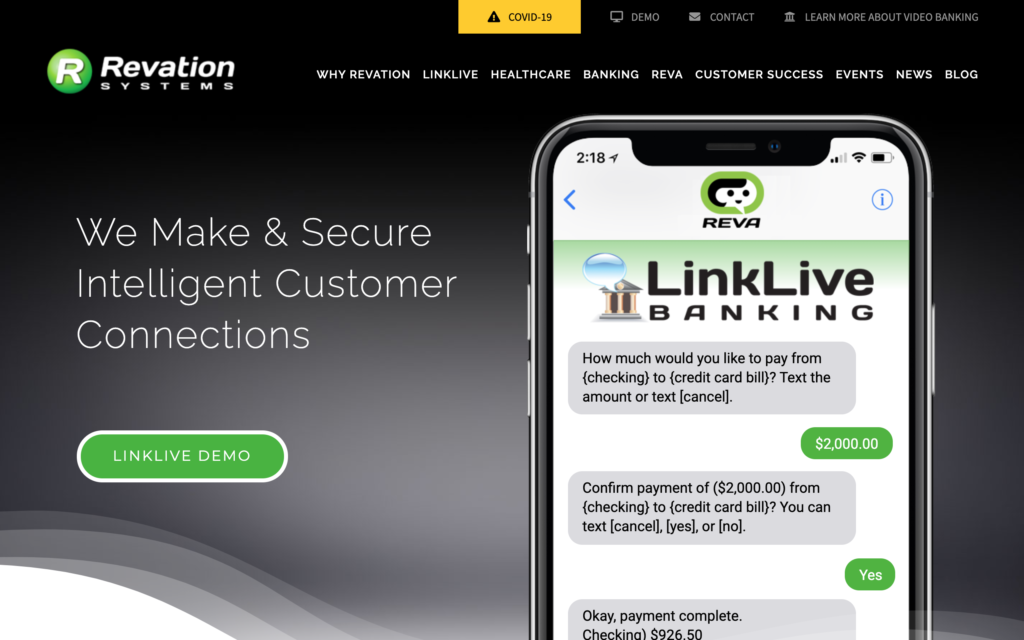

Linqto’s investment platform democratizes the private space for accredited investors in the same way Schwab and Fidelity made public trading available to the average investor.

Features

Accessibility – mobile-first digital platform

Affordability – minimum investment sizes as low as $5,000

Liquidity – transferrable interests without the right of first refusal

Why it’s great Private investing made simple. Linqto is democratizing the investment in pre-IPO companies.

Presenter

Bill Sarris, CEO & Co-Founder Sarris is a recognized expert in the field of banking and investment technology. He is Co-Founder of Linqto and the inventor of Linqto technology. LinkedIn

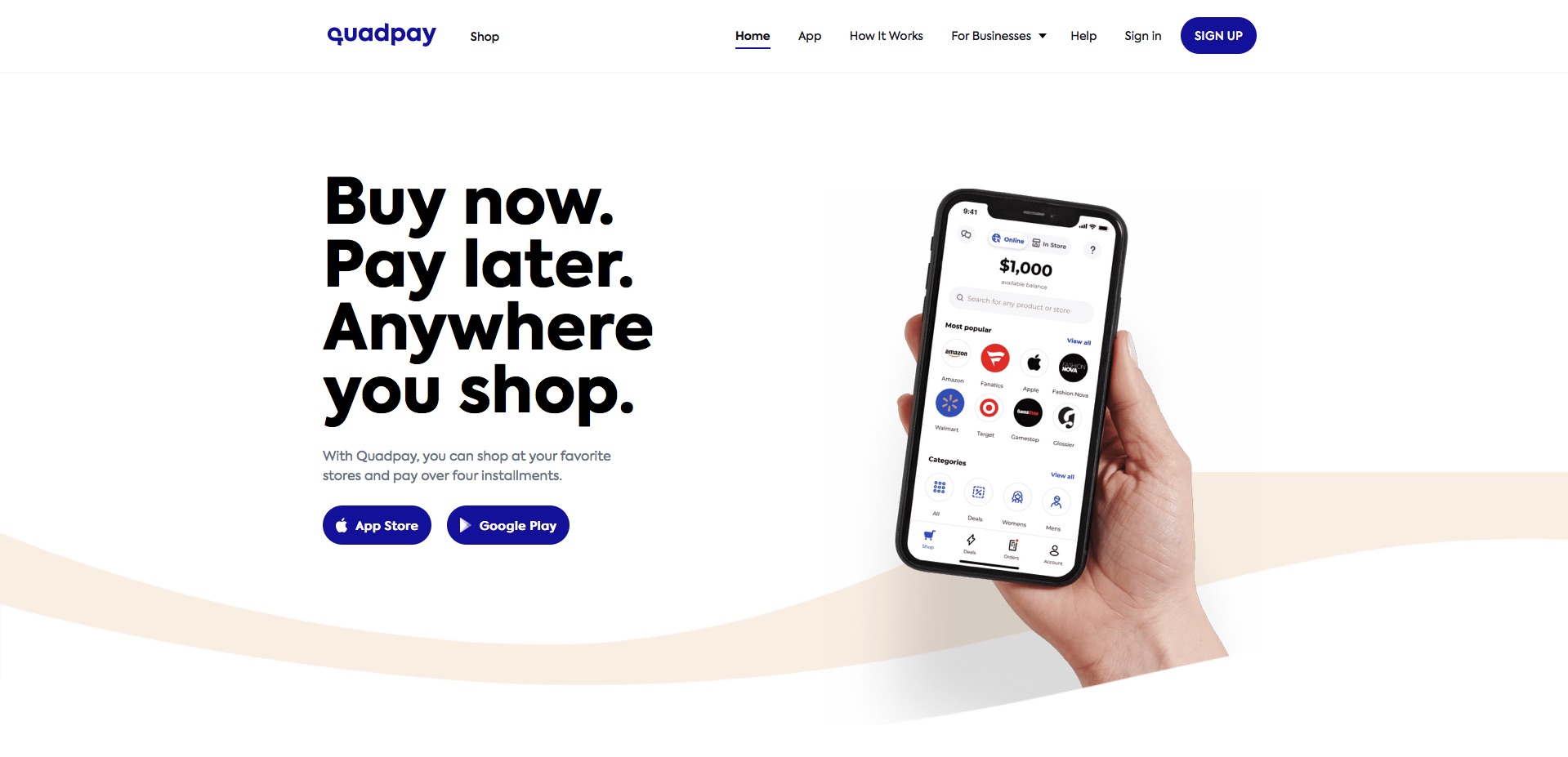

There were many themes that fintech analysts expected to dominate this year. But there were few among them who had “Buy Now Pay Later” (BNPL) on their 2020 bingo cards.

From big recent M&A in the BNPL space to the rash of installment payment offerings recently launched by both fintechs and incumbent financial services companies alike, it is clear that Buy Now Pay Later is one of the hottest trends in fintech and e-commerce right now.

We thought this would be a good time to catch up with one of the leaders in the BNPL movement. QuadPay co-CEO and co-founder Brad Lindenberg shared with us his insights into what’s driving interest and excitement in the Buy Now Pay Later space, and what we can expect to see in the months and years to come.

Finovate: The Buy Now Pay Later phenomenon is one of the more unexpected developments in e-commerce this year. From the perspective of a company that’s been active in this space for years, what made the difference in 2020?

Brad Lindenberg: There are a number of factors in play that have led to the rapid ascent of buy now, pay later (BNPL) globally in 2020. First, consumers – particularly millennials – are wary of high interest credit cards and accruing additional debt. This concern was prevalent before 2020, as many millennials are saddled with student loan debt, but now has been heightened by the economic impact from COVID-19. The BNPL industry has been a major disruptor to credit cards and companies like QuadPay represent the new world of interest-free, transparent digital payment products.

Secondly, BNPL empowers retailers to provide their customers with flexibility to pay over time, which ultimately fosters customer loyalty, increases conversions, and a better customer experience. In the case of QuadPay, merchants that have implemented our BNPL product for e-commerce have seen a 20 percent increase in conversions and 60 percent increased average checkout value.

I would also point out that for QuadPay the BNPL phenomenon is not solely within e-commerce. With QuadPay, consumers can use BNPL to shop everywhere for everything – whether it’s online or in the-physical retail locations of the thousands of merchants on the QuadPay app. QuadPay has direct partnerships with 7,200 world-class retailers that are promoted within the QuadPay app to our four million and growing customer base in the U.S.

Finovate: We can’t talk about 2020 without talking about COVID. How has the pandemic affected both your company, and your company’s relationship with its customers?

Lindenberg: In many ways, QuadPay is the right company at the right time. Almost overnight the industry witnessed a drastic shift in consumer spending to focus almost exclusively online with retailers responding in kind to support that demand and QuadPay was able to facilitate those needs on both sides. We have built a digitally-forward payment product that fits the mobile-first lifestyle of today’s budget conscious consumers that can also be quickly and efficiently implemented by merchants across industries and of all sizes trying to adapt. We have experienced an uptick in interest in BNPL overall, but particularly from small and medium businesses – this has by far been our fastest growing vertical since the pandemic.

Finovate: In this increasingly competitive space, what does QuadPay offer that its competitors don’t?

Lindenberg: Competition is inevitable in a fast-growing and successful category like BNPL and serves as validation that the credit card industry is badly broken. The entry of new players has not changed our strategy or lessened our opportunity. We remain laser-focused on providing our users the best possible products fueled by our drive to innovate. Our recent merger with Aussie payments pioneer Zip Co. (ASX: Z1P) forged a $1 billion global fintech alliance and has us solidly positioned to continue our leadership position in this category.

QuadPay’s true differentiator remains innovation – we are the only installment platform that gives consumers the power to shop anywhere – at any retail location, on any website and with QuadPay’s integrated merchants on the app – and that’s a substantial advantage. We believe our recent partnerships with Fiserv, MasterCard Vyze and GameStop are key indicators of our continued mission to forge the future of BNPL.

Finovate: How easy is it for consumers to qualify for BNPL compared to traditional consumer financing options? Who is left “holding the bag” if the consumer does not hold up their end of the bargain?

Lindenberg: The BNPL qualification process is drastically modern compared to that of traditional consumer financing options. We leverage proprietary technology and algorithms to assess the eligibility of each applicant across a variety of variables and approval can happen within minutes. There is no hard inquiry to the consumer’s credit history. It is in our own interest to approve consumers for an amount commensurate with eligibility. Our platform caters to purchases between $35 – $1,000 so the risk is relatively small. Less than 2 percent of our customers are late to make repayments in any given month – far below the national average for delinquent credit card payment. And in the event they are unable to pay, they can no longer make purchases on the QuadPay platform.

Finovate: Some critics of BNPL say that, unlike old-fashioned layaway programs, Buy Now Pay Later encourages consumption at the expense of saving. How do you think we should understand BNPL in the overall context of individual financial wellness?

Lindenberg: Financial responsibility is built into our model. Our mission is to provide consumers a transparent, financially responsible way to expand their spending power without the debt-spiral of credit cards. Installment payments are set to be charged automatically on the due date, so customers can just sit back and relax without worrying about missing a payment. QuadPay sends SMS and email reminders before installments are due so customers can make sure they have enough funds available to cover an upcoming installment.

In the event a customer can’t make a payment, we can adjust their payment schedule at their request. And if they stop making payments all together, they can no longer use the platform for purchases until the balance is paid. It’s really that simple and easy. There’s no impact on the consumer’s credit score and no interest accrues which is the real driver of most debt. We are here to help, not hurt, consumers. In fact, we have seen many consumers leverage QuadPay to expand their spending power for things like groceries, personal care, and other essentials particularly during COVID-19.

We very much see QuadPay as a critical first step for many consumers to learn and implement overall healthier budgeting habits which could ultimately improve savings.

Finovate: You recently announced a partnership with Gamestop. What is the significance of this relationship?

Lindenberg: The GameStop partnership was rolled out just ahead of the highly-anticipated release and pre-order availability of the new Sony PlayStation 5. It serves as a great example of how retailers can really leverage flexible payment solutions like BNPL to get the latest and greatest products into the hands of an enthusiastic customer-base ahead of the 2020 holiday shopping season.

We are thrilled to be partnered with GameStop, the world’s largest video game retailer, as they look to provide their customers with a simple and flexible way to pay over time both online and at the point of sale inside their more than 3,300 U.S. retail locations.

Finovate: QuadPay has also received significant backing from Goldman Sachs and Oaktree recently. What does this relationship do for QuadPay going forward?

Lindenberg: QuadPay has secured a committed revolving line of credit of up to $200 million from Goldman Sachs, with mezzanine financing provided by Oaktree Capital. The support of two strong institutions like Goldman Sachs and Oaktree is a testament to QuadPay’s leadership position within the BNPL industry.

Finovate: What is the future of Buy Now Pay Later? As a consumer financing option, what innovations have yet to be brought to this space that we might see in the next few years?

Lindenberg: The future for BNPL is very bright. We are only in the nascent stages of adoption in the U.S. market and expect installment payments to become as ubiquitous as “Visa accepted here” logos at checkout or at the register in-store. Consumers will begin to expect merchants to offer interest-free, installment payments as an alternative to high interest credit cards. We also believe that as contactless payments become more widely accepted, BNPL will continue to flourish.

On our part, we will continue to introduce new features and capabilities that make it easier to search and find particular types of items across retailers so shoppers can find the best deals on the items they want. We recently acquired Urge, a retail search engine providing shoppers access to all the world’s leading brands, stores and online retailers in one place which will change the game for BNPL globally.

It’s hard to plan ahead right now. We don’t know when we’ll be gathering in large numbers again, what work will look like next year, or when everything will reopen. But we do know that work still must be done: relationships maintained, customers satisfied, and new business brought in the door.

FinovateEurope is here to help. We’ve structured our digital offering to provide meaningful networking opportunities; insightful, thought-provoking content; and exposure to new, innovative technology. All with the goal of helping you navigate these changing circumstances strategically and intelligently.

Here’s how to get involved:

Demo: We’ve retooled the demo experience for digital events. Greg Palmer, VP of Finovate, joins each digital demo to create engaging interactions. Moderated Q&A sessions follow the demos to help companies build relationships. And demoers walk away with 200+ leads on average. Learn more.

Sponsor: We have a whole host of new and exciting sponsorship opportunities on our virtual event platform. Lead capture, gamification, virtual networking, branded booths, and chatrooms, and more. Download the prospectus.

Startup Booster: These special tickets for startups cost just £199 for all three event days. Plus, we’re pulling together special content geared towards these early-stage companies. See if you qualify now.

Attend: Tickets are at their lowest price, £399. And there are deals for governments, fintech leaders, and 3+ attendees. Check it out.

Find your path forward at FinovateEurope Digital 2021 with any of these options and plan ahead with confidence.

How have the major secular trends in fintech been impacted by the COVID-19 crisis?

In his afternoon presentation at FinovateWest Digital, November 23 through 25, Jacob Jegher, President of Javelin Strategy and Research, will take a close look at which innovations in fintech are moving the needle in terms of boosting customer engagement, creating efficiencies, and helping financial institutions and financial service providers grow revenues.

Formerly Vice President of Global Solution Marketing and Head of Analyst Relations at FIS and, before that, serving for more than a decade as Research Director for Celent, Jegher brings a wealth of knowledge and experience in the banking technology industry. In addition to being widely cited in both mainstream and financial media – including The Wall Street Journal, The Globe and Mail, Bloomberg, and The New York Times – Jegher is a judge and coach at the Innotribe Startup Challenge.

“There are so many different pieces that (fintechs and financial institutions) have to watch out for in changing times,” Jegher told Finovate VP Greg Palmer during the Finovate Podcast earlier this year. “Pitfalls today include: how do you manage your budget and your cash flow associated with investment? What are you going to decide to keep pushing the envelope on and what’s going to get cut back? It’s just a realistic point of view given what’s taking place with company budgets – whether they are fintechs or financial institutions.”

To catch Jegher’s presentation at FinovateWest Digital – as well as the rest of our three-day, all-digital fintech event – visit our FinovateWest Digital hub and save your spot today. Take advantage of Early Bird discounts when you buy your ticket by November 13.

Small business banking solution provider BlueVine announced late last week that its BlueVine Business Banking offering is now generally available for small businesses looking for an integrated banking, payments, and lending solution. BlueVine Business Banking gives SMEs online services and tools to help them manage their finances, deposit checks, transfer funds, and make bill and vendor payments. The solution includes BlueVine’s Business Checking product, which the company said had seen “rapid adoption” by its customers during the recently-concluded beta testing period.

“Now more than ever, small businesses need simple, easy-to-use financial solutions, services, and guidance that support – not nickel-and-dime – them on their path to recovery amid the pandemic,” BlueVine CEO and co-founder Eyal Lifshitz said. “Over the last year, we have worked tirelessly behind the scenes to innovate and iterate on our BlueVine Business Checking product based on tremendous beta customer reception and feedback. We are thrilled to provide all small business owners with access to sign up for an account today, to help them achieve a better financial tomorrow.”

BlueVine Business Checking offers 1.0% interest on balances of $1,000 or more. Beginning this month, the company will offer 1.0% interest with no minimum balances – up to $100,000. The accounts include two free checkbooks, and no monthly ATM, NSF, or incoming wire fees. SMEs get unlimited transactions with no minimum balance requirements, and business owners can apply for the accounts in as little as 60 seconds.

BlueVine notes that more than 20,000 small businesses have signed up for the company’s Business Banking Accounts, which will also now feature BlueVine Payments. This enhanced billpay functionality enables businesses to pay vendors and bills from a directory of more than 40,000 common billers and registered payees – as well as setup their own payee. Businesses can pay by bank account or debit card, and the company’s payment is then sent to vendors by ACH, wire, or check. BlueVine added that payment by credit card is currently in beta testing.

The new product launch was also an occasion to announce a new partnership. BlueVine said that it has teamed up with fellow Finovate alum – and Visa acquisition target – Plaid to enable its small business banking customers to access external accounts when making payments or other transactions via the BlueVine dashboard. The partnership will also add BlueVine as a supported bank account on the Plaid Exchange Network.

Founded in 2013 and making its Finovate debut one year later at FinovateFall, BlueVine has raised more than $767 million in equity funding, most recently announcing a $102.5 million investment in November 2019. The company picked up a debt financing with Atalaya Capital Management that enabled them to secure a $75 million revolving credit facility in September. In August, BlueVine teamed up with DoorDash to help restaurant owners apply for Paycheck Protection Program (PPP) loans.

BlueVine’s participation in the PPP this year has been notable. The company said that it processed more than 155,000 emergency government loans for SMEs, valued at more than $4.5 billion, as part of the relief effort.

Just a few months after buying U.K.-based financial service price comparison site Know Your Money, NerdWallet is back at the register with another big purchase. The company announced late last week that it had agreed to acquire online, small business lending marketplace Fundera. Terms of the transaction were not disclosed.

The acquisition enables NerdWallet to expand its offerings for small business owners, and adds to the financial wellness platform’s content and marketplaces for products including student loans, insurance, mortgages, and investments. Founded in 2013 by Jared Hecht, Andres Moran, and Rohan Deshpande, Fundera will become a NerdWallet subsidiary as a result of the transaction, with all of Fundera’s employees joining NerdWallet.

In a statement, NerdWallet co-founder and CEO Tim Chen pointed to the small business market as an area of “tremendous opportunity” that the acquisition will enable his company to pursue.

“Although we offer free tools and content, we’ve never been able to fully support small business owners — that changes today,” Chen said. “Fundera has been one of our partners for several years and their deep understanding of the SMB market, the long-standing, trusted relationships they’ve built with both lenders and business owners, and their commitment to putting the needs of small business owners first is really unique and impressive.”

Founded in 2009 and headquartered in San Francisco, California, NerdWallet offers personalized, objective, actionable financial guidance to help consumers make intelligent financial decisions. Via its website and app, NerdWallet provides consumers with free access to its expert content and comparison shopping marketplaces to enable them to save time whether they are looking for insights into the best credit card for their needs or assistance in buying a first home.

NerdWallet has raised $105 million in funding. The company includes Camelot Financial Capital Management and Institutional Venture Partners (IVP) among its investors.

The biggest news in international fintech was the $34.5 billion pricing of Ant Group’s upcoming initial public offering. We covered the news earlier this week. The company will be making a dual IPO, offering half of its shares on Hong Kong’s Hang Seng, and the other half on Shanghai’s Star Market. The date for the Hong Kong IPO has been set for next week, November 5th. No date has been determined for Ant Group’s IPO on the Shanghai-based exchange.

The $34.5 billion target would represent a new record, topping the $29.4 billion raised by Saudi Aramco earlier this year in its IPO. Ant Group anticipates earning a valuation of more than $313 billion. This amount would rival that of most of the biggest banks in the U.S., with the only exception being JP Morgan Chase with its market cap of $434 billion.

On the European fintech front, a handful of Finovate alums have made headlines this week. Account takeover prevention specialist SpyCloudannounced a partnership with Southern European-based information security solutions value-added distributor, DotForce. U.K.-based Icon Solutions, a payments technology provider, picked up a strategic investment from JPMorgan. In the Americas, FISteamed up with Brazilian financial services firm Afinz to help the company enhance its private-label credit card processing capabilities. Meanwhile to the north, Toronto, Ontario, Canada’s Finn AIinked a deal with Michigan-based United Federal Credit Union to bring conversational chat to the firm’s 200,000 members.

Here is our look at fintech around the world.

Central and Eastern Europe

German business banking platform Penta partners with savings marketplace Raisin.

Lithuanian government authorizes new Centre of Excellence in Anti-Money Laundering.

German sharia-compliant banking app, insha, raises €2.5 million en route to planned U.K. launch.

Middle East and Northern Africa

Bahrain-based open banking platform Tarabut Gateway launches in the UAE.

Oman Banks Association urges lenders in the country to embrace fintech and open banking.

Turkish fintech Payguru introduces new pay by text message service.

Central and Southern Asia

Indian fintech GetVantage raises $5 million in seed funding.

Smart Engines partners with Alfa Bank Kazakhstan to power digital onboarding and online payments.

PhonePe, an online payments company based in India, announces availability as a payment option at more than two million locations in Maharashtra.

Latin America and the Caribbean

Risk analytics software company Provenir partners with Mexico’s Estudia Mas to automate and digitize risk decisioning for education loans.

Visa to acquire YellowPepper, a company that supports Latin American and Caribbean financial institutions and startups.

Real-time financial data aggregator Afterbanks begins operations in Mexico.

Asia-Pacific

Rapyd launches its “all-in-one” payment capabilities in South Korea courtesy of a partnership with local PSPs.

Hong Kong-based virtual bank Mox onboards 35,000 customers in its first month of operation.

TechinAsia looks at the “brutal” competition in the Vietnamese e-wallet market.

Sub-Saharan Africa

Evolve Credit, a Nigerian loan and financial product marketplace, raises $25,000 in funding from Nigerian VC firm Microtraction.

Fintech infrastructure platform Nium announces expansion into Africa.

Two South African fintechs, B2B digital lender Lulalend and biometric digital identity company Paycode, earn recognition by the 2020 Inclusive Fintech Awards.

Reviewing critical challenges and opportunities in the fintech industry across 2020. With a specialized focus on the latest in lendingtech, bankingtech and customer experience.

Join Finovate for a week of webinars, thought-leadership and video interviews, all accessed online for free.

Here’s a snapshot of what’s to come…

All Finovate Fintech Fulltime Review registrants also get access to the Fulltime Review eMagazine at the end of the week, featuring key session recordings from FinovateFall Digital and FinovateWest Digital, plus an exclusive discount to Finovate events in 2021.

Log in from the comfort of your desk anytime and choose the content that suits you. Get involved now >>

Embedded banking-as-a-service platform Wisesecured $12 million in funding this week. The investment is its second one this year – Wise announced a $5.7 million seed round in April – and was led by e.ventures with participation from Grishin Robotics. The company, which made its Finovate debut last year at FinovateFall, said in a statement that the capital will be used to help fuel growth and accelerate partnership-building in a number of verticals. Wise now has raised a total of $18 million in equity financing.

“We built banking so our partners don’t have to,” Wise CEO and co-founder Arjun Thyagarajan said. “By embedding banking, Wise unlocks deep product offerings and better customer experiences for our partners. e.ventures built a thesis on exactly this, and we agree 100%.”

Wise offers an embedded banking experience that gives small businesses a seamless way to bank, as well as make and accept payments. Companies partner with Wise and leverage its all-in-one business banking solution to offer accounts to their own clients such as e-commerce platforms and marketplaces. In addition to providing a fully-hosted and fully-serviced banking experience, Wise helps companies bridge the gap between what they have traditionally received from banking services and what e.ventures partner Brendan Wales called “an Apple-like experience” brought to the world of business banking.

“Business banking has been broken for far too long. Poor user interfaces, payments delays, unnecessary fees, a lack of integrations, the list goes on and on,” Wales said. Now, cloud-based B2B companies can offer banking services in a matter of days with no coding involved and have the entire operation managed and maintained by Wise.

Wise demonstrated its small business-banking-in-a-box solution at FinovateFall 2019. A Techstars NYC company based in San Mateo, California, Wise was founded in 2018. Check out our profile of the company from earlier this year.