This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Germany-based digital bank N26 announced today it is bringing on Gilles BianRosa as its new Chief Product Officer.

In this new role, Gilles will be responsible for leading product teams in Berlin, Barcelona, Vienna, and New York. He will also define, guide, and implement N26’s product strategy. To support these efforts, Gilles will bring on new team members and build N26’s product innovation.

“Gilles has a track record of delivering consumer-facing innovation that truly engages, excites and entertains customers,” said N26 co-founder and CEO, Valentin Stalf. “Today, N26 has revolutionized how people relate to their banking experience on an everyday basis. With Gilles on board, we will expand our experience further to being banking that easily connects an account with one’s lifestyle in an even more tangible way.”

Gilles brings with him decades of experience as CPO at tech companies including SoundCloud and Samsung Electronics. He also has entrepreneurial roots, having served as the co-founder and CEO of two Silicon Valley startups.

N26 is one of the most well-known players in the ever-growing digital banking realm. Founded in 2013, the startup offers its digital banking services in 25 countries, including the U.S., where it launched in 2019 and has since accumulated 500,000 customers in the area.

Today’s news comes about a month after N26 received a $35 million (€30 million) investment, bringing its total raised to $819 million. And it’s not the first C-level hire that N26 has initiated this year. In January, the company brought on Jan Kemper as Chief Financial Officer. Kemper holds experience in leading companies to go public, which may be an indication of N26’s intentions. In fact, Bloomberg expects the startup to IPO within the next two years.

In the biggest fundraising for an identity verification company to date, Jumio has locked in an investment of $150 million. The funding comes courtesy of Great Hill Partners, a private equity firm that specializes in investments in “high-growth, disruptive companies.” The investment takes Jumio’s total funding to more than $255 million, according to Crunchbase.

“Jumio’s innovations helped establish the identity verification market, and the need to establish someone’s digital identity remotely has never been greater,” Jumio CEO Robert Prigge said. The company plans to use the new capital to automate its identity verification solutions, expand the breadth of its Jumio KYX Platform, and further build out the platform’s suite of AML compliance solutions.

As part of the investment, Great Hill Partners’ Nick Cayer and Matt Vettel will join Jumio’s Board of Directors. Cayer, who has been with Great Hill since 2006, praised the company as “the de factor global leader in online identity verification, fraud detection, and compliance.” He added that given the mandate many institutions have to digitize processes such as onboarding and KYC monitoring, firms like Jumio can play a key role in helping them keep pace with the growing volume of digital and mobile-based transactions.

Making its Finovate debut in 2013 and being acquired by Centana Growth Partners in 2016, Jumio has verified more than 300 million identities issued by 200+ countries and territories since inception in 2010. With customers and partners in a wide range of verticals – from financial services and the sharing economy to retail, travel, and online gaming – Jumio leverages AI, biometrics, machine learning, and certified liveness detection to help ensure that customers are who they claim to be. Jumio’s KYX Platform, launched last fall, provides organizations with an end-to-end identity verification and eKYC solution that enables them to onboard new accounts safely and accurately, keep existing accounts secure, and meet their compliance obligations with regards to KYC, AML, and GDPR.

“Digital transformation is more than a buzzword. It’s today’s business imperative,” Prigge said. “To succeed, organizations must transform quickly and do it in ways that build trust, security, and satisfaction. Businesses can tailor the Jumio KYX Platform to fit their unique needs and risks and tap into services that accelerate digital transformation without sacrificing security and convenience.”

Learn more about how Jumio fights deep fakes and bots in our interview from last summer featuring company VP of Marketing, Dean Nicolls.

Online small business insurance company Huckleberry announced a partnership with Berkshire Hathaway GUARD today.

As part of the partnership, Huckleberry joins Berkshire Hathaway GUARD’s curated network of independent agents and brokers across the U.S. For Huckleberry, it’s the largest partnership with an insurance carrier the company has inked since it was founded in 2017.

Huckleberry offers a range of coverage for U.S. small businesses in need of insurance. Coverage types include general liability, workers’ compensation, business owners’ policies, business interruption, liquor liability, and more. Five of its policies, including including cyber, automotive insurance, and umbrella insurance, were added just last year.

What’s unique about Huckleberry, which offers coverage in 45 U.S. states, is its paper-free application experience that offers an estimate in a matter of minutes. And because the startup doesn’t charge brokerage fees, it not only provides a streamlined approached, but also a more competitive rate. instant coverage

The San Francisco-based company is in the process of moving its headquarters across the country to New York and also has plans to open a second headquarters location in Columbus, Ohio. As part of this growth, Huckleberry aims to boost its workforce to 100 people by the start of next year.

Founded by Bryan O’Connell , Huckleberry has raised $22 million. Its most recent investment was a $22 million Series A round led by Tribe Capital.

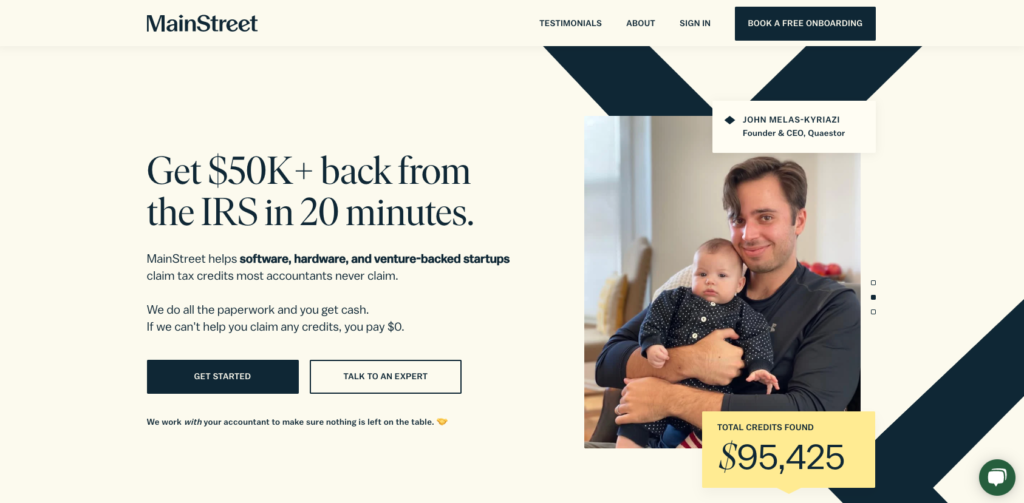

Here in the U.S., it’s tax season. And even though the IRS has extended the filing deadline by a few weeks, it’s still a stressful time for both individuals and businesses. In an era of changing benefits, everyone is on the lookout to minimize their tax burden.

Enter MainStreet, a company founded in 2019 that helps qualify tech startups for tax credits that most accountants don’t check for. The California-based company works with startups’ accountants to check for more than 200 potential unclaimed tax credits.

MainStreet works by integrating the startups’ payroll and scanning the data on a monthly basis for potential federal, state, and local tax credits. If MainStreet finds a tax credit, the company will advance 80% of the credit amount to the startup so that they can use the funds right away instead of waiting on their tax refund. The client is responsible for repaying that amount, with no interest incurred, after they receive their credit from the government.

MainStreet does not charge a fee for this monthly service. Instead, the company keeps the remaining 20% of the startups’ tax credit amount. However, MainStreet only receives payment if it successfully finds a refund for the client.

In the event of an audit, MainStreet offers support through the auditing process. And if MainStreet makes an error with the paperwork or credit claim, the client is insured for up to $1 million.

So far, MainStreet has found more than $80 million for over 1,000 startups. The company’s clients include Rally, Newfront Insurance, LedgerX, Pave, and more.

In the long term, MainStreet plans to expand its operations beyond serving tech startups to include small businesses, as well.

MainStreet has received almost $63 million from investors including Gradient Ventures, Sound Ventures, and Signal Fire.

Anybody else old enough to remember the argument that while blockchain technology probably had value, actual cryptocurrencies were already passé?

In a round led by Coatue, Ribbit, and Stripes, digital asset infrastructure specialist Fireblocks has secured $133 million in new capital to power its mission to make it easier for banks to get into the digital asset space.

“Fintechs and banks require not only a specialized custody and settlement infrastructure to ensure customer funds are safely managed, but (also) a platform that enables new lines of digital offerings,” Fireblocks CEO Michael Shaulov said. He noted that while the company has no plans to become an actual bank itself, “we believe our infrastructure will lend itself perfectly to power an entirely new era of financial services.”

Also participating in the round as strategic investors were The Bank of New York Mellon and SVB. A number of Fireblocks existing investors also contributed to the round, including Paradigm, Galaxy Digital, Swisscom Ventures, Tenaya Capital and Cyberstarts Ventures. The investment brings the fintech’s total capital raised to $179 million.

Founded in 2018, Fireblocks launched as a digital assets infrastructure company helping crypto-based institutions and exchanges move, store, and issue digital assets. As interest in digital assets – especially cryptocurrencies like Bitcoin and Ethereum – has surged, Fireblocks has begun to leverage its talent and technology in digital assets to enable banks and other financial institutions to bring cryptocurrency access to their customers. By linking to its Fireblocks’ platform, banks and fintechs will be able to deploy a wide range of solutions – from custody, tokenization, and asset management to trading, lending, and payments – on both public and private blockchain networks.

The company’s investors highlighted Fireblocks’ capacity to enable banks and other financial institutions to efficiently and securely take advantage of the opportunity of and interest in digital assets. CEO of Asset Servicing and Head of Digital for BNY Mellon Roman Regelman said that bridging the gap between traditional and digital assets is “foundational to the future of custody.” Coatue Managing Partner Kris Fredrickson concurred: “our belief (is) that a new financial ecosystem is emerging and (companies) like Fireblocks are essential.”

Peer-to-peer lending platform and digital bank Zopa landed some extra funds this week, now that its new banking platform is starting to take off.

The U.K.-based company pulled in $28 million (£20 million) from existing investors, bringing its total raised to $465 million.

Investors in today’s round include IAG Silverstripe, which led the round, as well as Augmentum, Alternative Credit Investments, Venture Founders, and others. The company will use the funds to support the growth of its digital bank.

Zopa secured its banking license last June and has since transitioned its platform from a peer-to-peer lending operation to a digital bank with a peer-to-peer lending option. Since that time, Zopa began offering savings accounts, which have reached $346 million (£250 million) in customer deposits, and a credit card product that has made Zopa a top 10 credit card issuer in the U.K. based on new customers.

The new funding comes at a time when competition among digital banks is at an all-time high. Zopa is poised to do well in the battle for new clients and deposits, however. The company has built a well-established client base, resources, and relationships since it was founded in 2004 as a peer-to-peer lending platform.

Zopa CEO Jaidev Janardana echoes this. “Less than a year since launching our bank, we have exceeded our plan for growth, both in terms of customers and balance sheet,” he said. “This capital injection will enable us to continue on this accelerated path. Our strong entry to the U.K. savings and credit card markets shows the organic appeal of our products and we are happy to have investors who share our excitement at the opportunity to serve more customers across more product categories.”

Still looking for evidence that cryptocurrencies have arrived? The $170 million raised this week by Austrian digital asset neobroker Bitpanda is a testament to both the surging interest in cryptocurrencies as well as the vitality of fintech innovation in the CEE countries.

Bitpanda’s Series B round earned the company a valuation of $1.2 billion, giving Austria its first fintech unicorn. The Vienna-based company, founded in 2014 by co-CEOs Eric Demuth and Paul Klanschek, along with CTO Christian Trummer, plans to use the capital to add to the types of investments available on its platform, as well as expand to more markets in Europe.

This latest funding round was led by Valar Ventures and featured participation from partners of DST Global. The round is more than triple the amount raised by Bitpanda in its Series A financing back in September, which was also led by Valar Ventures (SpeedInvest of Vienna was an investor in the round, as well). The capital arrives the same week that Bitpanda announced that it had reached a new milestone of more than two million registered users on its Bitpanda and Bitpanda Pro platforms.

Bitpanda enables cryptocurrency investors and traders to buy, sell, save, and send more than 50 digital assets including Bitcoin and Ethereum. The neobroker also offers the world’s first real crypto index and a Bitpanda Card that enables Bitpanda accountholders to spend their digital assets as easily as they spend their cash.

With FinovateEurope right around the corner, we’ve got more than a little continental fintech on the mind these days. This week we take a quick look at fintech news from France, a country whose fintech industry is often overlooked in the broader conversation on European fintech.

Earlier this week, we learned that Finovate alum Ledger was launching a new business division dedicated to taking advantage of growing institutional interest in cryptocurrencies. Headquartered in Paris and founded in 2013, the company announced that its Ledger Enterprise Solutions unit will support enterprise adoption of the company’s core custody technology, Ledger Vault, as well as advise institutional clients with regards to technology implementation, security, and governance of digital asset portfolios.

On the French fintech funding beat, PayFit, a payroll and HR platform launched in France in 2016, announced that it has secured $107 million (EUR 90 million) in Series D funding. The investment was led by Eurzeo Growth, Large Venture, and BPI France, and featured participation from the company’s existing investors Accel, Frst, and individual investor Xavier Niel.

The company said that the capital will help support its comprehensive HR solution for SMEs and enable the company – which also operates in Spain, Germany, the U.K., and Italy – to “increase headcount from 550 to 800” by the end of 2021.

PayFit serves more than 5,000 small businesses, and includes Revolut, Starling Bank, and Treatwell among its customers. The company experienced growth of 40% in 2020 – a pace PayFit anticipates doubling this year – and credited much of this “hypergrowth” to the digital imperative brought on by the COVID-19 crisis.

“As a result of the pandemic, HR professionals have faced a much higher workload and unfamiliar challenges,” PayFit co-founder and CEO Firmin Zocchetto said. “They have had to deal with various issues, including supporting the company’s management with the implementation of remote work policies and ensuring employee wellbeing through new initiatives.”

Zocchetto said that there are “tens of millions of SMEs” that are ready for digital transformation. “The market is huge, and our ambition remains the same: to become the point of reference for payroll and HR management for all SMEs,” he said.

Striking another note in the funding beat, French fintech Silvr announced a EUR 3 million seed investment this week. The company, launched last year by Nima Karimi and Gregory Tappero, provides financing for digital businesses that cannot access traditional bank financing and want to raise equity capital.

Silvr offers a revenue-based financing model based on the performance of the financed company, an approach that contrasts with both traditional asset-based lending and fundraising models. Karimi has said that Silvr’s strategy offers a new option for SMEs in France, calling it simpler and more transparent.

Here is our look at fintech innovation around the world.

SEON, a Hungarian startup helps companies weed out false accounts and prevent fraudulent transactions, secured $12 million (EUR 10 million) in funding. The round is Hungary’s largest Series A funding to date.

Lithuanian fintech FINCI has gone live with Temenos’ Payments and Transact core banking solutions.

Estonian financial services company LVH invested GBP 4.45 million in U.K.-based B-North, which is building a SME lending bank.

Phone-based fraud prevention company Pindropacquired Next Caller this week. Terms of the deal were undisclosed.

Pindrop anticipates the purchase of NextCaller, a call verification and fraud detection solution for contact centers, will position the company for growth, expand its client base, and position it as an industry leader.

“Our two companies will now be able to service the market in its entirety with the right solution for whatever stage of voice security and authentication they are in,” said Next Caller Co-founder and CEO Ian Roncoroni.

The deal comes at a time when demand for call centers is expanding. In a recent report, Forrester found that 42% of brands surveyed saw an increase in year-over-year call center call volume since the pandemic began. Additionally, 65% of companies reported they struggle to manage the high call volume and 80% of firms reported that fraud is a very serious issue in the call center.

Given this, Pindrop CEO Vijay Balasubramaniyan has a positive outlook for the fraud prevention industry. “We couldn’t be more bullish about the future,” he said, “The need for our combined solutions will only continue to grow as brands across multiple industries not only look to better secure their voice channel, but also improve the customer experience. Understanding who you are speaking to is the most effective way to build a better relationship with customers, resulting in a higher NPS and subsequently more profitable exchanges.”

As for what’s next, Next Caller will operate as a wholly-owned subsidiary under Pindrop.

Founded in 2011, Pindrop debuted an IVR solution as well as the availability of its voice authentication technology for use in OTT streaming devices. Headquartered in Alabama, Pindrop is privately held and has raised a total of $213 million from investors including Andreessen Horowitz and Citi Ventures.

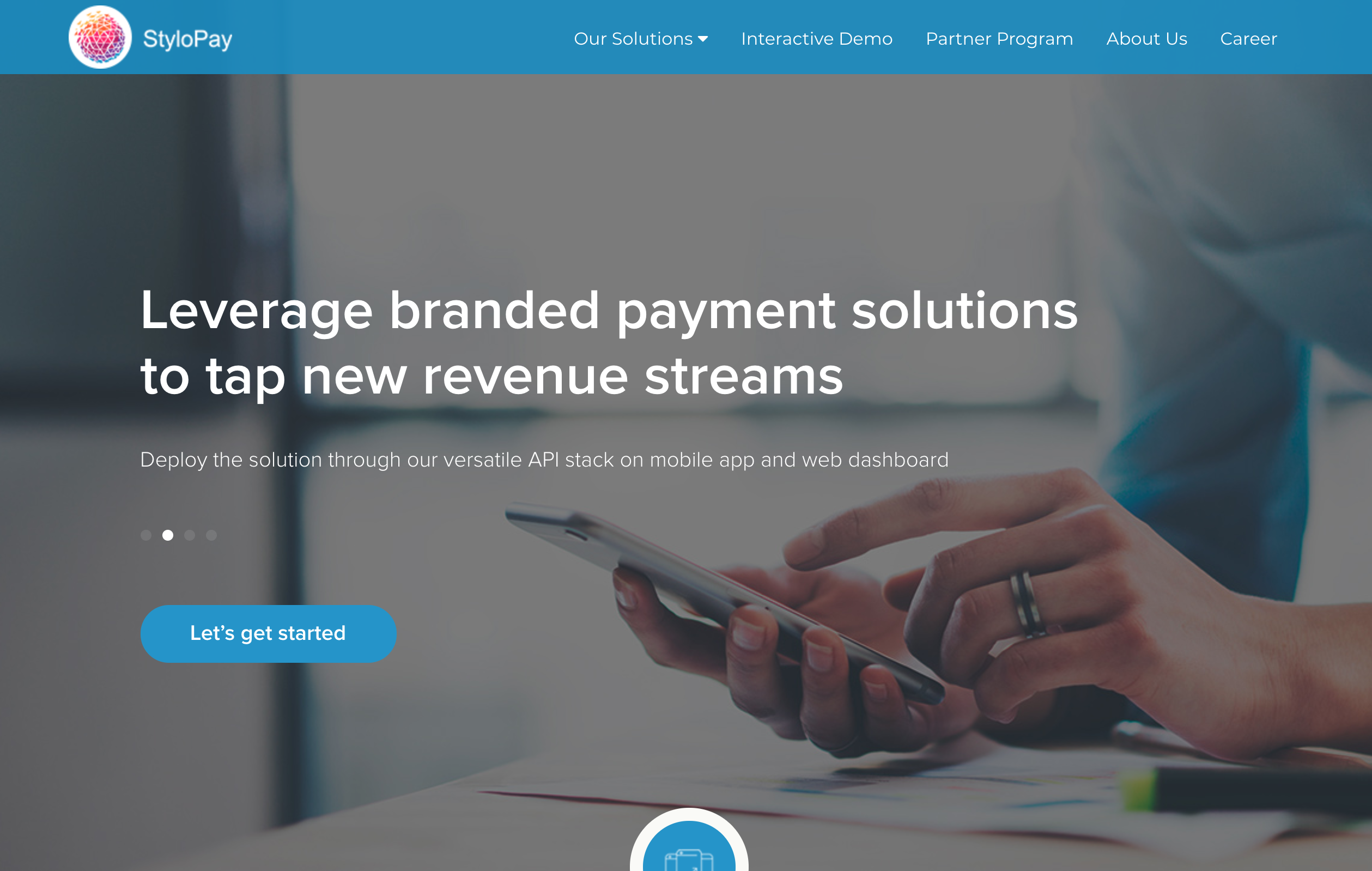

Stylopay‘s Zoqq is a self-service application and management portal for corporate card programs. Apply in 30 minutes and get approved in 7 days. Pay only card cost.

Features

Apply in 30 minutes and get approved in 7 days

Get and manage programs in different countries and different currencies

Start with 100 cards at low costs with complementary admin and user portals

Why it’s great Faster application, multi-currency card program, global reach!

Presenters

Sanjit Ghanti, COO Ghanti is a payments expert. He has a background in hosted BPAAS solutions, business transformation, and operations. He manages IT infrastructure, product launch, and operations. LinkedIn

Avishek Singh, CEO Singh has experience in marketing, finance, and start-ups. He also manages business connections, contributes to marketing strategies, and is passionate about innovation. LinkedIn

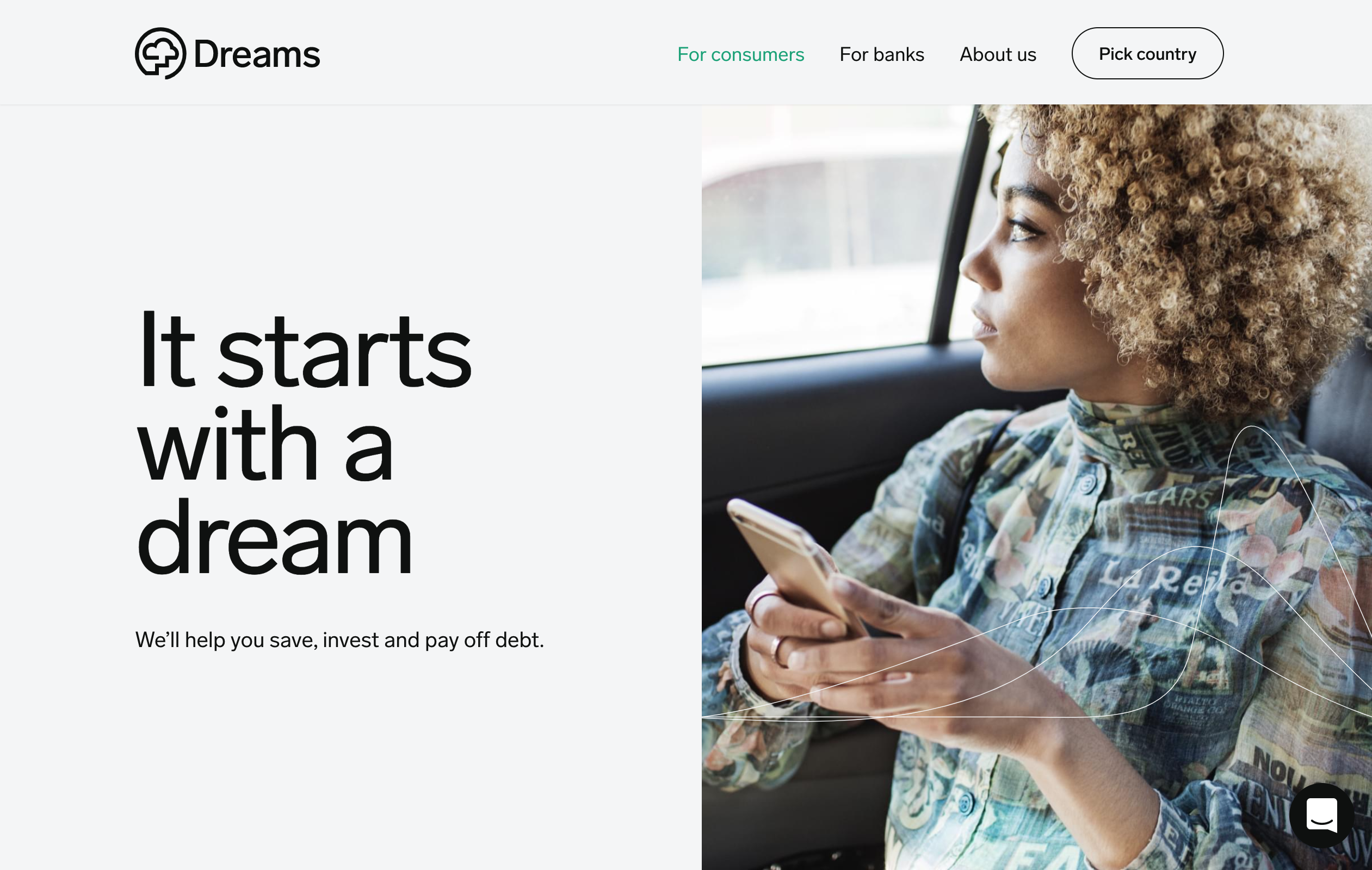

Dreams is a financial wellbeing platform that helps banks attract the new generation and create superior digital engagement by leveraging the latest insights from cognitive and behavioral science.

Features

Increase financial wellbeing: 2/3 of Dreams users feel less stressed about money

Increase retention: 4.3x vs. comparable financial apps

Attract the next generation: 75% millennial audience

Why it’s great Dreams leverages cognitive and behavioral science to effectively influence consumer behavior, help the end user create healthier financial habits, and help banks significantly increase digital engagement.

Presenters

Lucia Hegenbartova, Chief Commercial Officer Hegenbartova is Chief Commercial Officer at Dreams, responsible for building commercial partnerships with banks around the world. LinkedIn

Elin Helander, Chief Scientific Officer Helander is Chief Scientific Officer at Dreams, responsible for injecting the latest insights from cognitive and behavioral science into the Dreams app. LinkedIn

FinovateEurope is right around the corner! Our all-digital, interactive fintech conference begins March 23 at 9am Central European Time and continues through March 25. Visit our registration page today to save your spot!

FinovateEurope will feature our signature format of innovative fintech demonstrations and in-depth, insightful keynotes, panel discussions, and debates on some of our industry’s most important topics and critical themes. To learn more about our demoing companies, check out our Sneak Peek Series. For more on our thought leadership content, here’s a short, day-by-day summary of what to look out for.

March 23: Martes / Dienstag / Wtorek / Tuesday

Kicking off the event on Day One of FinovateEurope are keynote addresses from Katharina Lueth of Raisin UK, Joe Lichtenberg of InterSystems, and a conversation between HSBC’s Steve Suarez and Louise Beaumont of the Open Banking Working Group.

The afternoon will feature a number of panel discussions and roundtables covering topics such as open innovation and strategic partnerships, the future of hybrid digital customer experience, and leveraging agility to thrive at times of crisis. The day will end with a conversation on digital engagement in the post-COVID era.

March 24: Mercredi / Onsdag / Quarta-feira / Wednesday

On Day Two, FinovateEurope begins with a keynote on open innovation and open banking, and continues with a pair of Mastermind Keynotes from Alex James of GoCompare and Alex Thomson of Quantum Metric, as well as from Annerie Vreugdenhil, Chief Innovation Officer with ING. In addition to a keynote on sustainable finance, the afternoon on Day Two will be devoted to panel conversations on the shift to digital payments and preserving “the human touch” in the digital financial world.

March 25: Donderdag / Giovedì / Čtvrtek / Thursday

The final day of FinovateEurope will feature some of our conference’s most popular sessions, such as our Analyst All Stars presentation. This year, our All Stars include Jost Hoppermann of Forrester, Zil Bareisis of Celent, and Vinod Jain of Aite Group. Day Three will also tackle the growth of morgagetech by way of a Mastermind Keynote from Floris van der Kolk of Ohpen and Rik Douwes of Link Asset Services. Rounding out the day will be a venture capital panel discussion on investment trends in the post-COVID era. This conversation will feature Citi Ventures’ Luis Valdich, Silicon Valley Bank’s Claire Palmer, SixThirty Ventures’ Samarth Shekar, and Mouro Capital’s Manuel Silva Martinez.

Upcoming webinar Title: Customer Engagement Tactics to Boost Loyalty and Monetization Date: Thursday, April 15, 2021 Time: 04:00 British Summer Time Duration: 1 hour

Research shows brands that excel in customer engagement often exceed their revenue goals. But how well is the financial services industry really responding to customers, and delivering on promises of “customer-centricity?”

Join this upcoming webinar where our expert panel will explore the top trends in customer engagement in 2021 for financial services companies, growth levers for financial service businesses, and how customer engagement strategies can be used to drive long-term growth. Find out which steps you can implement now, and in the long term, to improve customer engagement. Hear first-hand insights from Wise, including how the company has advanced its customer engagement strategy over time.

Featuring:

Erin Bankaitis, Strategic Business Consultant, Braze