This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

At a time when concerns about illegal immigration have complicated the mostly positive attitude most Americans have toward immigrants in general, it is heartening to see that innovators and entrepreneurs in the fintech space are finding ways to bring vital services to those fleeing often-horrific conditions to find better lives in another land.

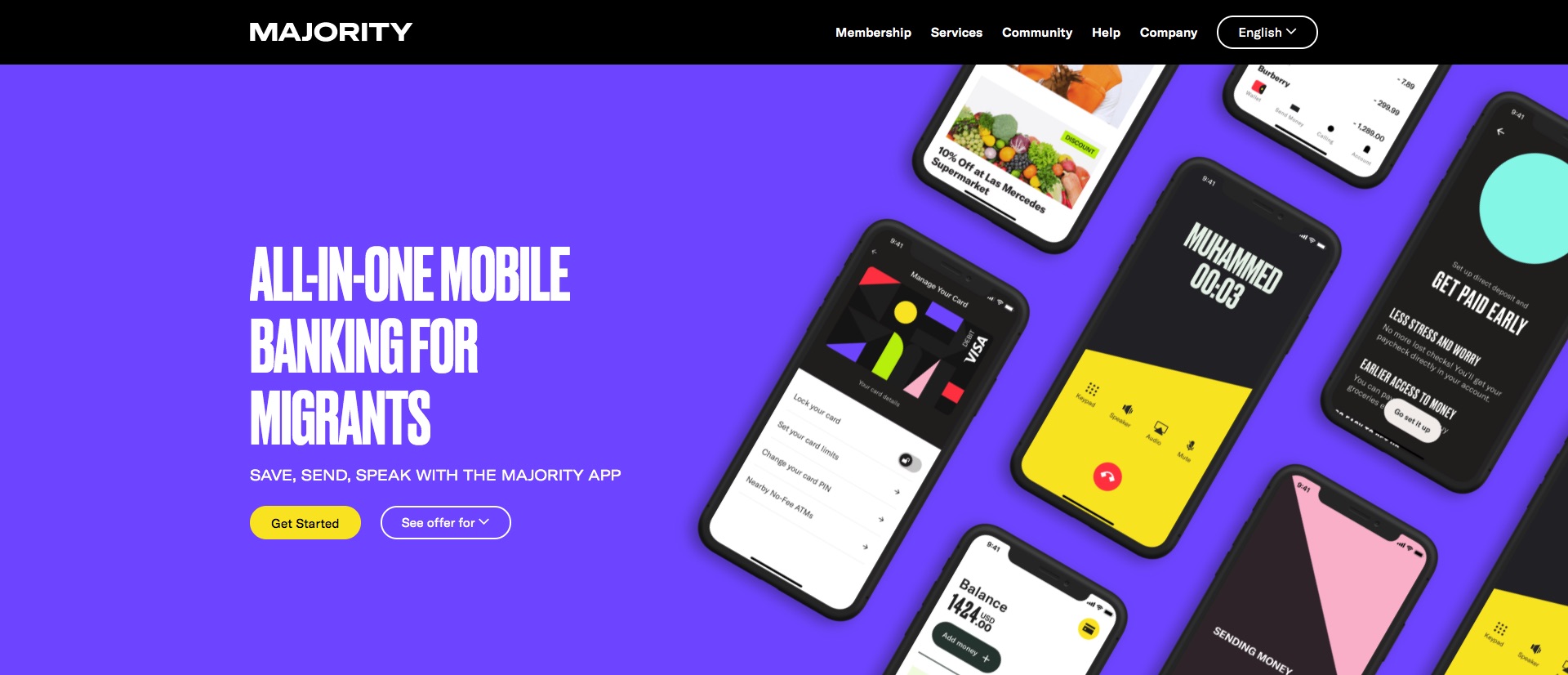

One such company is MAJORITY, a U.S.-based, mobile banking service designed specifically to serve the migrant communities in the States.

Founded in 2019, MAJORITY offers a banking app that provides an no-overdraft-fee, FDIC-insured bank account, a debit card with community discounts from local merchants, no-fee remittances, and “at-cost” international calling. The app is available for $5 a month. Company founder and CEO Magnus Larsson said that MAJORITY already has saved its Cuban members $21 a month on average and its Nigerian members $10 a month on average thanks to its “cost-efficient service offerings.”

MAJORITY also offers members the services of its hundreds of local advisors who help onboard and support new customers in their native languages. And while MAJORITY’s banking services are available in all 50 states, the company’s advisors are currently operating only in Texas and Florida.

Larsson explained the utility of the company’s human advisors in a conversation with TechCrunch. He described how a MAJORITY customer could meet up with an advisor outside of a grocery store and, within minutes, have their bank information, a Visa debit card, and the ability to use that grocery store to send money to another country.

“Migrants, by their very definition, are the most ambitious people in the world, striving for success in a new country – but they are lacking the necessary tools,” Larsson said. “Migrant-relevant financial services come with extensive fees that feel overwhelming for all people, but even more intimidating for those trying to navigate an unfamiliar system. At MAJORITY, we seek to remove the uncertainty that comes with international financial services and do our part to better facilitate a world where people are valued on their positive impact, not their country of origin.”

MAJORITY estimates that there are more than 258 million migrants worldwide, with nearly 50 million migrants in the U.S. – who are under-banked, un-banked, or otherwise experiencing “insurmountable barriers” when it comes to financially integrating into their new country. And courtesy of a $27 million investment MAJORITY announced last week, the company now has new resources to help.

“Our mission, as a migrant-led company, has always been to serve the migrant communities with the unique resources they need—financial and otherwise—and this latest funding will help us continue to perfect our services and support this community that is the backbone of America,” Larsson said.

The Series A round was led by Valar Ventures and featured the participation of Avid Ventures, Heartcore Capital, and a number of Nordic fintech founders. MAJORITY now has $46 million in total funding, which includes $19 million in seed funding the company raised earlier this year.

Accompanying its funding news, MAJORITY also announced that it is introducing a new feature that will enable migrants to sign up for a bank account without requiring a social security number. Instead, applicants will be able to use a government ID from any other country and proof of U.S. residency to access MAJORITY’s banking services.

“A bank account is the starting point to so many other things for someone moving to a new country, and American bureaucratic delays and backup shouldn’t prevent people from being able to establish themselves here,” Larsson said. An immigrant himself from Sweden, Larsson is currently waiting for visa approval in order to move from Stockholm to Miami, Florida, to further build out MAJORITY. He also looks forward to being able to grow the company from its current 65+ employees in Sweden and the U.S.

Supply chain finance company Tradeshift has raised more than $200 million in combined equity and debt funding. The San Francisco, California-based firm, which made its Finovate debut in 2012 at FinovateEurope, now has an estimated valuation of $2 billion according to Reuters. Tradeshift CEO and founder Christian Lanng, who did not confirm the valuation with Reuters, did tell the company that the new funding will help Tradeshift “refinance parts of our balance sheet focusing us on long term continued growth.”

The investment featured participation from Koch Industries, IDC Ventures, LUN Partners, Private Shares, and Fuel Capital. According to Crunchbase, the investment gives Tradeshift more than $1 billion in equity funding.

Founded in 2010, Tradeshift has become a leading B2B e-invoicing and accounts payable automation company. With more than 1.5 million companies connected on its platform, Tradeshift has processed more than $1 trillion in cumulative value since inception, a figure that has doubled in two years. The company’s offerings include its B2B marketplace for e-procurement Tradeshift Buy, its automated accounts payable platformTradeshift Pay, a supplier analytics solution Tradeshift Engage, early payment option Tradeshift Cash, and its virtual credit card offering Tradeshift Go.

By hosting all of these features on a single trade technology platform, Tradeshift enables businesses to transition from being “future proof” to “future flexible,” and to scale their operations virtually without limit. An early adherent of the value of embedded technologies, Tradeshift empowers companies to “continually digitize” their supply chain and take advantage of a dynamic, digital network of connected buyers and sellers.

“Embedding financial services directly into our product unclogs the flow of working capital across supply chains, eliminating a significant pressure point in the buyer-suppliers relationship,” Lanng explained. “As one of the first companies to recognize the potential for embedded finance in SaaS, we have been betting on the convergence of Fintech and SaaS products for awhile. We’ve built the technology and distribution channels to capitalize on what is now one of the defining trends in our industry.”

Named to Fast Company’s list of the World’s Most Innovative Companies for 2020, Tradeshift launched its cross-border e-invoicing solution last month, reducing friction in cross-border transaction flows for companies doing business in China. In October, the company announced that its Tradeshift Go virtual credit card solution was on track to process $2.5 billion in charge volume in 2021, a 6x increase over 2020. Tradeshift has forged partnerships this year with the Danish Export Credit Agency, trade and supply chain financing platform Raindew Trade, and Qatar-based Gulf Warehousing Company (GWC).

Selling nearly 290 million shares priced at $9 in its initial public offering on the New York Stock Exchange this week, Brazilian digital bank Nubank has raised $2.6 billion, reaching a market value of $41 billion. An alumni of Finovate’s developer’s conference FinDEVr in 2016, Nubank is now the most valuable financial institution in Latin America in addition to being the world’s biggest digital bank. CEO David Vélez, who co-founded the company in 2013 with an initial investment of $2 million from Sequoia Capital and Kaszek Ventures, now owns a stake in the company worth $8.9 billion at the IPO price.

“We don’t think the banking branch will survive the way it is,” Vélez said to CNBC this week. “It is too costly to serve the majority of users, especially in emerging markets where you have a very high cost of operations, so a lot of that physical infrastructure will probably disappear.” Vélez predicted that most financial services providers will transition into digital entities in the next five to ten years because of this, leading to an increased focus on customer service as well as lower costs and interest rates.

With more than 48 million customers in Brazil, Mexico, and Colombia, and onboarding more than two million new customers a month on average, Nubank offers financial products for spending, savings, investments, loans, and insurance. The company claims to have provided more than five million people with their first credit card or bank account as of September 30, and to have saved its customers more than $4 billion (R$27 billion) in bank fees and more than 113 million hours of waiting time since inception.

Vélez said that the capital from the IPO will help fuel Nubank’s expansion in Mexico and Colombia, en route to becoming a truly pan-Latin American banking services provider. “There is a lot of opportunity to build the next generation of financial services, so we will continue to invest and grow for a very long time,” Vélez said an interview with the Financial Times.

FinovateEurope 2022 is right around the corner. If you are an innovative fintech company with new technology to show, then there’s no better time than now and no better forum than FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22-23, visit our FinovateEurope hub today!

Here is our look at fintech innovation around the world.

CinetPay, a digital finance platform serving merchants in French-speaking Africa secured $2.4 million in seed funding from 4DX Ventures and Flutterwave.

Online fraud prevention company SEON inked an agreement with a pair of African neobanks, Carbon and FairMoney.

South African device identity and authentication solutions provider Entersektannounced a “significant investment” from U.S. private equity firm Accel-KKR.

German biometrics and digital identity verification company Passbase secured $10 million in Series A funding, as well as another $3.5 million in seed-2 investment.

Earlier this week we shared our conversation with IDology CEO Christina Luttrell on the challenges and opportunities in the digital identity verification space. This fall, IDology was honored at the 2021 Finovate Awards, winning recognition as “Best Identity Management Solution.”

A few weeks later, IDology released its 4th Annual Consumer Digital Identity Study. Surveying nearly 1,500 U.S. consumers over the summer of 2021, the study sought insight into what it called “the insecure, COVID-weary consumer.” How have preferences shifted in the balance between security and privacy on the one hand, and the willingness to share their personal information in order to access services that in many instances became especially valuable during the pandemic on the other? How have expectations grown as consumers’ reliance on new digitally delivered services has increased? And what steps can companies take in order to gain and keep valuable trust relationships with their customers?

These are just a handful of the questions addressed in IDology’s latest “heat check” on consumers and digital identity.

Finovate:IDology just published its 4th Consumer Study. What is the goal of this report and what can you tell us about your findings?

ChristinaLuttrell: This marks our fourth year publishing the Consumer Digital Identity Study to help businesses understand important shifts in consumer perceptions and preferences about fraud and identity verification. This year’s study showed us that, more and more, consumer trust hinges on the ability of businesses to safeguard identities and keep consumer data private, particularly during online account opening and onboarding.

Needless to say, consumers today have experienced seismic shifts in how they live and work, becoming increasingly reliant on all things digital. When we conducted this survey, the COVID-19 pandemic was entering its 16th month and the Delta variant accounted for the lion’s share of new infections. The results of our survey show a weariness that only a once-in-a-lifetime global pandemic can create and, with the emergence of variants such as Omicron, the potential for more uncertainty.

Customer fatigue has undoubtedly impacted consumer practices and preferences relative to the security of their identities, particularly their willingness to hand over personal information. We also observed a growing need for trust-based online relationships, which was evident in the level of protection consumers expect companies to put in place to safeguard their data and ensure privacy.

This report pays close attention to how consumers view the threat of fraud and the never-ending waves of cyber breaches. We also spotlight consumer expectations regarding privacy, why they do not trust businesses to be good stewards of their data, and what can be done to foster trust, especially during the online account opening and onboarding experiences.

From our vantage point, this survey shows that the intersection of fraud, trust, privacy, compliance, and new customer engagement continues to grow in its significance. Consequently, excelling in today’s environment requires embedding identity verification at the center of every digital interaction.

The safety and security of the mobile channel are of critical importance to consumers and companies alike. Twenty-four percent of consumers report that their mobile devices have been compromised since the pandemic began. Consumer concern about smartphone malware attacks has increased 34% year-over-year, and nearly half believe their mobile device is more vulnerable than their personal computer.

Consumers expect more identity fraud. Ninety-six million Americans expect the number of fraud attempts involving their identity or accounts they own to increase over the next 12 months. Amid the rise in unauthorized account openings, 61% are concerned their personal information will be used by criminals to open a new financial account. At the same time, many Americans appear ill-prepared to protect their data. Only 45% believe they have the wherewithal to defend themselves against cyber-attacks and fraud.

Trust in companies to responsibly use consumer data is on the decline. Seventy percent suspect that companies gather data without their permission, and 59% don’t think companies do enough to safeguard the Personal Identifiable Information (PII) they possess. This raises significant worries for consumers, with 53% very or extremely concerned with the practice, which explains why 90% support legislation similar to the California Consumer Privacy Act (CCPA) in their states or at the federal level.

A well-respected industry thought leader, Christina Luttrell was recognized in 2018 by One World Identity as a top 100 influencer in identity verification. She has been named one of the leading women in security by Security Magazine and in 2019 was selected as one of Atlanta’s “Women Who Mean Business” by the Atlanta Business Chronicle. In 2021 she was recognized by Global InfoSec Awards as a top “Woman in Cybersecurity.” Under Luttrell’s leadership, IDology has experienced dramatic growth.

Modern SaaS banking platform Mambu has secured an investment of $266 million (€235 million) in a Series E round led by EQT Growth. The funding, the largest to date for a banking software platform according to Mambu, gives the Berlin, Germany-based company a valuation of $5.5 billion (€4.9 billion).

“This latest round of funding will allow us to accelerate our plans in expanding our mission-critical banking platform to further enable composable business models which are agile and continuously evolving,” Mambu co-founder and CEO Eugene Danilkis said. Additionally, the company will use the new capital to expand its global footprint to support an international customer base that is currently active in 65 countries.

More than 50 million end users rely on Mambu’s technology every day. In Q3 of 2021, Mambu produced year-on-year growth of more than 1.2x. Also this year, the company has signed 40+ customers, with more than 55% of its new customers headquartered outside of Europe. Among the company’s more recent partnerships are its alliance with Capgemini to offer BaaS in the Asia-Pacific region, and its collaboration with Germany-based Raisin Bank, which launched its own BaaS offering using Mambu’s cloud banking platform. Other major deployments included N26, Raiffeisen Bank, and ABN Amro.

Founded in 2011 – and a Finovate alum since 2013 – Mambu most recently demonstrated its technology on the Finovate stage this September at FinovateFall. At the event, the company provided a birds-eye view of its SaaS cloud banking platform, showing how users can open an account, create and launch new solutions in minutes, and leverage integrations with Salesforce, Stripe, Marqeta, and others to include KYC, fraud and identity verification, CRM, and other services.

“Our vision in creating Mambu was always to create an industry-leading platform that will enable more than a billion people to have brilliant banking experiences,” Danilkis said in a statement accompanying this week’s funding announcement. “We want to be able to empower our customers to create any financial product anywhere in the world and create amazing customer experiences.”

Every week is a good week to be a Finovate alum. But for those alums that focus on forging partnerships to help credit unions and banks transition from legacy systems to modern, cloud-based environments, the first full week of December so far has been especially productive.

Westmark Credit Union, an Idaho-based financial institution with more than $1 billion in assets, announced yesterday that it will swap out its current core banking system for Jack Henry & Associates‘ Symitar. The credit union cited Symitar’s open and flexible architecture, including the ability to both use the core “as-is” as well as to introduce additional functionalities in the future should they choose to. Symitar will provide Westmark CU with built-in workflows to bring automation – and lower error rates – to key processes.

“Symitar’s workflows and connectivity provide the opportunity to realize significant financial and efficiency gains,” Westmark Chief Information Officer Don West said. “And most importantly, it gives us the optionality we need to integrate with the products and service providers of our choice. With Symitar, we can build the best technology plan for our unique business needs, fueling future growth and keeping a highly competitive pace with the accelerated speed of change in today’s market.”

The transition will also take Westmark from an in-house core banking system to one that leverages a private cloud environment instead. This will enable the credit union to focus less on managing the day-to-day tasks of core maintenance and hardware updates and more on improving their member experience.

Speaking to this point, Jack Henry & Associates VP and President of the company’s Symitar division, Shanon McLachlan noted, “Jack Henry has seen a significant movement from on-premise to the private cloud environment with approximately 30 existing customers a year making the move, and this isn’t limited to any asset size. While this shift continues to be a huge trend, so is the need to have a modern core that enables credit unions to provide their members with the options they need to succeed,” McLachlan said.

Jack Henry & Associates made its first Finovate appearance at FinovateFall in 2010. Headquartered in Monett, Missouri, the company announced a major collaboration with fellow Finovate alum Envestnet | Yodlee last week to enable financial institutions to access consumer-permissioned financial data.

Another major fintech/financial institution partnership announced by our Finovate alums in the first half of this week is the collaboration between Trusted Novus Bank, a Gibraltar-based institution, and banking software company Temenos. As part of a “complete, end-to-end digital transformation,” the bank will trade its legacy core banking and front office systems for Temenos Transact and Temenos Infinity on the Temenos Banking Cloud.

“We want to expand our retail, corporate, and private banking and scale fast to increase our customer base,” Trusted Novus Bank CEO Christian Bjørløw explained in a statement. “With the Temenos Banking Cloud, we can deliver personalized, real-time customer experiences on a scalable platform that will foster innovation and keep the bank at the forefront of technology, and at the same time be true to our vision and values.”

The oldest established bank in Gibraltar, Trusted Novus Bank was reorganized in 2020 with goal of growing its business and enhancing the digital experience for its customers, as well. With its new core and front office system and access to the Temenos Banking Cloud, the bank will be able to build and offer personalized, real-time customer experiences that are customized for its different lines of business. Trusted Novus Bank will also be able to take advantage of straight-through-processing (STP) and automation, enabling its professionals to prioritize value-added, customer-facing services rather than on time-consuming administrative tasks.

“With banking services powered by the Temenos Banking Cloud, Trusted Novus can dramatically reduce costs and turbocharge innovation to deliver outstanding customer experiences,” Temenos President of International Sales Jean-Paul Mergeai said. “Trusted Novus has exciting plans to extend its banking services on our platform, and we will be working closely to ensure rapid time-to-value.”

A Finovate alum since 2013, Temenos operates worldwide and is headquartered in Geneva, Switzerland. The company recently announced that it was moving its North American regional headquarters to new offices in Manhattan, New York.

Even though our annual European conference has moved from February to March, FinovateEurope will always be synonymous with wintertime for many of us. So with the coldest season swiftly approaching, now seems as good a time as any to check in on the latest from some of our most recent FinovateEurope alums.

Paris, France-based Thread recently earned recognition at Catapult: Kickstarter 2021 Fall Edition. As one of the event’s five winners, the company is now eligible for up to $56,360 in subsidies. Thread made its FinovateEurope debut earlier this year, demonstrating its technology that makes complex and critical investment workflows more efficient and collaborative. In doing so, Thread aims to help investors make better investment decisions and reap “consistently higher performance.”

“With the acceleration of digital transformation worldwide, many companies have struggled to personalize their customer journeys online,” Surfly CEO Nicholas Piel said in a statement. “Surfly’s Co-browsing has helped ensure that insurers globally do not lose their personal touch with customers.”

Earlier this month we shared news that Strands had teamed up with carbon tracking company Doconomy. The partnership will enable the Barcelona, Spain-based fintech to offer climate impact and insight-driven engagement tools to their customers. Last month, Strands announced that digital financial solution provider Comviva will use Strands’ smart PFM solution to help its bank and financial services clients offer their customers a better digital banking and payments experience.

FinovateEurope 2021 Best of Show winner Quantum Metric was one of our more recent guests as part of our Finovate Webinar series. In partnership with BMO, the company led a webinar on How BMO is reimagining the Commercial Banking digital client experience using real-time analytics. Available for free on-demand for a limited time, the webinar panelists discuss the importance of quantifying the long-term impact of negative user experiences and how to establish a customer-centric mindset via Continuous Product Design (CPD).

Picking up a variety of fintech awards this year, white-label digital banking solution provider Meniga is another company that is leading the way in helping its customers understand and manage their climate impact – as citizens, consumers, and investors. Meniga, which demonstrated its Carbon Insight solution at FinovateEurope this year, announced that its transaction-based carbon footprint calculator had earned independent assurance from global accounting and professional services company EY.

ITSCREDIT was one of five Portuguese fintechs chosen to participate in a program to help provide Portuguese technology companies with the tools they need in order to “gain a foothold in (their) respective U.S. tech ecosystems” and help drive expansion. The landing pad program, Portugal Tech NYC, is sponsored by AICEP Portugal Global and SOSA, and will also feature the participation of Finovate alums ebankIT and LOQR.

ITSCREDIT demonstrated its Genie Advisor at FinovateEurope this year. The technology predicts customers’ financial conditions and provides insights to banking and finance professionals on how to best support customers that may be facing financial challenges.

To start the week, multiple-time Finovate Best of Show winner iProov announced that its partnership with Eurostar, the high speed passenger rail service that links the U.K. with mainland Europe, was now live. Eurostar has launched a trial of a new contactless fast-track service, SmartCheck, at London Pancras International. The service lets passengers use their mobile devices to secure ticket verification and U.K. exit check before they travel. Ticket holders of Eurostar’s Business Premier and Carte Blanche programs will be able to use their iPhones to complete a biometric face scan, which uses iProov’s Geniune Presence Technology, for identity verification that is linked to the traveler’s e-ticket.

“The days of rooting around in your bag for your passport or hoping that your phone battery doesn’t run out before you show your e-ticket at the gate are over,” iProof founder and CEO Andrew Bud said, “(SmartCheck) is effortless and convenient while also delivering the reassurance and security that travelers expect.”

Speaking of companies that have won more than a few Finovate Best of Show trophies, Digital Customer Service innovator Glia has been on an epic partner-making pace since its FinovateEurope appearance earlier this year. Customer engagement solution provider Engageware, Connecticut-based Liberty Bank ($7 billion in assets), digital banking solution provider Apiture, and Conversational AI specialist Posh Technologies are just a few of the companies Glia has collaborated with this fall. In November, the company earned a top 250 spot in the Deloitte’s Technology Fast 500 for North America.

Stockholm, Sweden-based Dreams, which demoed the savings module of its financial wellbeing platform at FinovateEurope this year, earned recognition at the Banking Tech Awards hosted by Fintech Futures. The company was named “Best Digital Banking Solution Provider.” Learn more about the Best of Show-winning company in our interview with Dreams CCO Lucia Hegenbartova, who sat down with Finovate VP Greg Palmer for an episode of the Finovate podcast over the summer.

CoCoNet Group, a digital banking services provider based in Germany, recently. announced a successful collaboration with Raiffeisen Group. The Swiss banking group leveraged technology from CoCoNet to launch a multibanking solution with integrated cash management and a secure EBICS interface to streamline online banking for corporate customers. CoCoNet made its FinovateEurope debut this March, demonstrating its MULTIVERSA Corporate Customer Onboarding solution.

The company formerly known as Nordic API Gateway has enabled more than 40 financial institutions, and a number of businesses, to integrate financial data and offer A2A (account-to-account payments) via a simple API. Founded in 2017, the company had raised $15 million (€13.5 million) in funding to date.

“For the past decade, we have worked to build Aiia into a leading and quality-driven open banking platform, which has onboarded hundreds of banks and fintechs onto safe and secure open banking rails,” Aiia founder and CEO Rune Mai said. “We have worked closely alongside banks, customers, and local authorities to ensure that our APIs show the true effect of open banking. We’re excited to become a part of Mastercard and progress our journey of empowering people to bring their financial data and accounts into play – safely and transparently.”

FinovateEurope 2022 is right around the corner. If you are an innovative fintech company with new technology to show, then the time is now and the forum is FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22-23, visit our FinovateEurope hub today!

A $60 million investment will enable digital asset compliance and risk management platform TRM Labs to help organizations and institutions better identify cryptocurrency-based financial crime.

“Crypto is moving faster than any sector in our lifetimes,” TRM Labs CEO Estaban Castaño said. “Organizations need a blockchain intelligence partner that can stay ahead of the evolving risk landscape – from ransomware attacks to DeFi exploits. This round enables TRM to continue to offer the most reliable data and most innovative technology solutions in the market to its customers.”

The Series B funding was led by Tiger Global and featured participation from a number of major firms including Visa, Amex Ventures, Citi Ventures, PayPal Ventures, Block (formerly Square), as well as DRW Venture Capital, Jump Capital, and Marshall Wace – among others. Combined with the capital TRM Labs has raised to date, the San Francisco, California-based firm now has total equity funding of nearly $80 million.

TRM offers a cohesive platform to empower businesses to better manage financial crime risk. The company’s technology enables firms to assess the risk profile of Virtual Asset Service Providers – what TRM calls “Know-Your-VASP” – and other cryptocurrency businesses. TRM’s platform provides forensic capabilities that allow organizations to investigate the source and destination of cryptocurrency transactions, and transaction monitoring that helps companies screen cryptocurrency wallets and transactions for AML and sanctions compliance.

TRM supports more than 900,000 digital assets across 23 blockchains, and features cross-chain analytics to enable seamless movement between Bitcoin, Ethereum, other blockchains. This allows organizations to build comprehensive visualizations that enable a more accurate and complete tracking of the flow of funds. Users of TRM’s platform can select from more than 80 different risk categories to establish their own risk scoring criteria.

Founded in 2017 and emerging from the Y Combinator two years later, TRM has since grown revenues by 6x year-over-year and expanded its workforce from four to 60. Cryptocurrency businesses such as Circle and MoonPay currently use TRM’s technology to identify suspicious activity in digital asset transactions and to satisfy AML requirements. Government agencies are using the company’s solutions in order to learn more about advanced cryptocurrency-related financial crime, ranging from hacks to terrorist financing. Last month, cryptocurrency payments company Dash announced an integration with TRM Labs to bolster its ability to monitor transactions on its platform for financial crime.

“By integrating with Dash, we enable organizations, including virtual asset service providers who want to list Dash, the ability to detect cryptocurrency fraud and financial crime and strengthen their compliance with AML/CFT regulations,” Castaño said when the integration was announced in November.

Asked what she was most proud of after a year as CEO of IDology, a GBG company and a leader in identity verification and fraud prevention, Christina Luttrell gave a big tip of the hat to her team.

“Without a doubt, I am most proud of what our team has delivered to IDology customers and the difference they have made,” she said. “For example, our dedicated fraud team recently spotted a new fraud vector utilizing tumbled email addresses and collaborated with IDology’s product innovation team to build, test and deploy a capability that mitigated the risk head-on, within weeks. Their dedication to serving our customers is energizing and I’m humbled by their contributions every day.”

In over 10 years at IDology, Luttrell has significantly advanced the company’s technology, forged close relationships with IDology customers, and driven the development of technology innovations that help organizations stay ahead of constantly shifting fraud tactics without impacting the customer experience.

We caught up the IDology’s Chief Executive in the wake of the company’s victory at the Finovate Awards, where IDology was named “Best Identity Management Solution.”

IDology won Best Identity Management Solution at the Finovate Awards this fall. What is unique about IDology’s approach to fraud fighting and identity verification?

Christina Luttrell: First, thank you for the honor. I am exceptionally proud of my team and thrilled about upcoming innovation we’ll be introducing into the marketplace.

Regarding the IDology difference, it’s based on our philosophy and relentless focus on customer success. From a business value perspective, we facilitate more revenue with less friction and fraud while enabling compliance. What makes IDology unique is how we go about it. We always consider ourselves a product company with a solution offering that utilizes vast and diverse data sources, acquiring deep fraud expertise, and building our consortium network for collaborative cross-industry fraud insights and combining all of these elements into one single integrated flexible platform called ExpectID.

We pioneered multi-layered identity verification by fusing physical and digital identity attributes. When we conceived identity verification orchestration and built the ExpectID platform we wanted to go beyond basic data matching to leverage thousands of diverse, high-quality data sources, correlate multiple identity attributes such as location, device and activity-based data, and use advanced algorithms and rules engines to analyze and evaluate risk factors. We were especially intentional to empower customers to customize a nearly infinite number of identity attribute combinations to gain more control of data and better understand risk.

We are innovating the ExpectID platform to new levels with anti-fraud machine learning layers, adding cross border verification, enriching data intelligence and launching more mobile capabilities so our customers can keep ahead of fraud and stay ahead in their business.

Can you discuss the importance of data diversity in the identity verification process and the challenge of achieving it?

Luttrell: Single sourcing identity data for verification is dangerous. With massive breaches, entire identity data pools have been compromised, packaged and sold on the Dark Web for new account fraud and account takeover schemes. This can be especially problematic when financial institutions use the same data sources for identity verification as they use for credit risk analysis.

Diversifying data from multiple streams and sources, whether public sources or digital attributes, such as email or mobile phone providers, and fusing them together, enables a more complete identity profile and deters schemes, such as synthetic identity fraud. The challenge isn’t so much in accessing identity data feeds, but in designing and orchestrating effective technologies and skill sets to create decision engines with precision and accuracy that can quickly adjust as fraud and consumer behaviors shift. Doing so takes years to develop, deliver, harden, and prove.

What role do configurability, flexibility, and orchestration play in an identity verification regime?

Luttrell: Our research shows that 90 percent of businesses view identity verification as a strategic differentiator. However, that competitive advantage is only realized when businesses are empowered to verify who they want, when they want, and which attributes they want, with economy and precision.

As a result of COVID and its implications on businesses and consumers, the identity attribute data and fraud landscapes are changing at faster rates than ever before, resulting in a growing number of elements that need to be tweaked, tuned, and verified to validate a consumer’s identity.

At the same time, we found that 70 percent of Americans think companies collect personally identifiable information (PII) online about them without their knowledge. Needless to say, consumers want to provide as little PII as possible. They also express intense dislike for encountering unnecessary verification steps and will abandon account creation if they feel the identity collection process isn’t secure or is overly complex. All of these factors point to real challenges for businesses.

The ability to build, customize and evolve their identity verification programs to suit the unique requirements, risks and opportunities of their industries, use cases, customers, and compliance needs – and defend against ever-evolving fraud schemes – is critical for businesses.

The ideal identity verification solution empowers businesses to customize and fully flex transparent validation checks, workflows, and attributes economically, at any time throughout the customer journey. When looking to mitigate fraud, either upfront in the customer journey or upon re-entry, the desired solution will provide a high level of flexibility to validate customer leads without sacrificing risk protection and compliance or generating front- or back-end friction.

A superior solution will enable businesses to pick and choose, mix and match identity attribute proofing and curate workflows, based on their unique needs.

Last but not least, the orchestration of multiple systems and services is key. At IDology, we’ve embedded flexibility for seamless orchestration across services and systems to our solution for over 14 years. Coordinating with many data sources and services, while offering deep “home-grown” analytics based on hundreds of combined years of experience in fraud and identity can enable businesses to onboard legitimate customers without friction while keeping the fraud out. Our orchestration platform is a one stop shop for managing KYC / CIP, validating emails, geo location, phone numbers, identity signals, and access to the largest consortium network in the country, offering dynamic and seamless escalation for methods such as document verification-based smart rules controlled by the business.

One of the more important developments in AI technology is the idea of explainable AI which enables the results of a solution to be understood by human agents. Is explainability a similarly important concept in the world of digital identity verification?

Luttrell: Artificial Intelligence (AI) and Machine Learning (ML) are hot buzzwords that often seem to be used interchangeably. Although widely used, there are major misconceptions about what these words actually mean. True AI means that a machine knows what to do with zero human interaction. When companies talk about using AI today, they’re really talking about using machine learning, which is an application of AI in which the system is “trained” by feeding it huge amounts of data and allowing it to adjust and improve.

As an early adopter of machine learning, we believe it plays an important role in building trust, removing friction and fighting fraud. By applying machine learning to the identity verification process, we have the power to analyze massive amounts of digital transaction data, create efficiencies, and recognize patterns that can improve decision making. At the same time, we recognize that machine learning alone is not enough.

Counter to the many benefits of utilizing machine learning are risks in its propensity for bias, lack of data transparency, and absence of governance. While machines are great at detecting trends that have already been identified as suspicious, a critical blind spot is their inability to detect novel forms of fraud. This is why we believe in a hybrid of machine learning and human intelligence.

Since 2016, we’ve supplemented machine learning with our fraud review team and today, continue using data, technology and expertise to meet the business needs of customers by verifying identities with high locate rates, low friction and less fraud. With the powerful combination of machine learning and human fraud expertise, we can analyze large amounts of data at scale while leveraging the intuition and expertise of our fraud review team to detect novel fraud, govern AI models to eliminate bias and reduce risk, and provide closed-loop data transparency.

Among the more recent challenges to identity verification is synthetic identity fraud. How significant is this problem and what needs to be done to combat it?

Luttrell: Synthetic identity fraud (SIF) continues to trouble businesses, causing financial institutions alone $50-$250MM in financial losses each year. The growth of this type of fraud can be attributed to its effectiveness for criminals and how difficult it is to detect.

Although there are no silver bullets, eradicating SIF requires businesses to monitor diverse data sources and employ multiple layers of integrated identity intelligence supplemented with system-specific SIF attributes, such as location, device and activity factors. This, along with dynamically evaluating a combination of cross-industry fraud data, machine learning, and human intelligence, has the potential to help businesses pinpoint instances of SIF.

You took over the top spot at IDology a year ago. What are you most looking forward to in your second year?

Luttrell: Going into the new year, I am excited about multiple things. For starters, GBG’s acquisition of Acuant opens up all kinds of possibilities to serve our customers with new innovation. I am also excited about global identity verification and making ExpectID the ultimate cross-border verification platform for easy and flexible international compliance and privacy from one single system. From tokenized identities to blockchain and advancements in machine learning, we are going into the next year with momentum and energy from the bottom up.

Speaking of accomplishments, you were recently named Woman of the Year at Golden Bridge Business and Innovation Awards. What does this recognition mean to you? What advice do you have for women who are pursuing leadership opportunities in technology today?

Luttrell: I have a great deal of gratitude and am humbled by the recognition. I see the recognition as a reflection of the excellence and talents of the entire IDology team. It also shows that I’ve been blessed with meaningful mentors along my career journey. At IDology in particular, dedication to our customer’s success is a value that has served me and the company well.

The advice I would offer women, and anyone for that matter, is to place the customer at the center of everything you do. Lead with confidence, but balance it with humility. Set and focus the business goals, persevere and stay positive. At the end of the day, we are all in this together so the kinder, the better.

In a Series A funding round led by FINTOP Capital, automated fraud and dispute resolution solution provider Quavo has raised $6 million in funding. The financing, according to FINTOP partner John Philpott, will help the company “expand their go-to-market strategies, grow their brand, and add further expertise fo the Quavo ecosystem.”

Founded in 2015, Quavo offers a chargeback management solution for fintechs and financial institutions that provides automatic regulatory, card network association, and product enhancement updates. The company’s Disputes-as-a-Service technology is cloud-based, and integrates with core banking platforms, financial service providers, and merchant collaboration software with zero upfront implementation costs. With its AI-enabled fraud management solution, ARIA; its automated dispute management software, QFD, and its human intelligence service, Dispute Resolution Experts; Quavo offers end-to-end dispute management that helps financial services firms reduce losses and provide real-time resolutions while remaining compliant.

“We are incredibly excited about our Series A raise,” Quavo co-founder and Managing Partner Joe McLean said. “FINTOP has a fantastic reputation, depth of knowledge in the financial services space, and its team is comprised of genuine and authentic leadership.”

Speaking of leadership, the investment comes as Quavo announces the formal creation of its board of directors, which will feature FINTOP partners John Philpott and Jared Winegrad as board members. Quavo co-founder and managing partner Dan Penne credited FINTOP for its “specialization in fintech and familiarity scaling companies to the next level.” He added, “Access to the FINTOP network and this infusion of capital will drive advances in Quavo’s products and services for existing and future clients.” Among the fintechs in FINTOP’s portfolio are firms such as FISPAN and Digital Onboarding, both Finovate alums.

Quavo’s recent fundraising is the second major capital infusion in recent years. In June of last year, the company announced a “multi-million dollar funding round” from Decathlon Capital. More recently, Quavo was recognized as a “Rising Star” at the 2021 Pega Partners Innovation Event in May for its work with credit unions and regional banks in particular.

“Our mission from day one was to create a complete Disputes-as-a-Service offering,” Quavo co-founder and Managing Partner Richard Jefferson said upon receiving the Rising Star award from Pegasystems. “The capabilities of the underlying Pega platform allowed us to accomplish this quickly and economically, which has enabled us to capture the imagination of the market. We thank our key vendor Pega for recognizing this accomplishment.”

Quavo’s clients include banks such as KeyBank, TD Bank, and Euro Pacific Bank; credit unions including NASA FCU, Schools First FCU, and Patelco CU; as well as fintechs like ADP, CardWorks, and Green Dot. The company is headquartered in Wilmington, Delaware.

With plans to launch initially in Mexico before expanding to Colombia and Central America, fintech startup Jefa is out to do what even the most innovative challenger banks have so far failed to do: bring better financial opportunities to women in Latin America.

Company CEO and founder Emma Sanchez Andrade Smith highlights the fact that nearly 1.3 million of the world’s 1.4 million underbanked people are women. Add to this the problem that the majority of new, digitally-oriented financial institutions are focused on mature markets in Europe and the United States rather than in emerging markets. Combined, these two facts represent a major challenge for women in developing markets – and a potential opportunity for creative fintech entrepreneurs.

Jefa announced earlier this week that it has secured $2 million in seed funding to bring financial empowerment women in Latin America and the Caribbean. More than a dozen investors participated in the round, including The Venture Collective, partners of DST Global, Foundation Capital, Amador Holdings, The Fund, FINCA Ventures, Rarebreed VC, Siesta Ventures, Springbank Collective, Bridge Partners, Hustle Fund, Foundation Capital, Latitud, J20, and Magma Partners. A number of angel investors such as Daniel Bilbao, JP Duque, Ricardo Schaefer, Jean-Paul Orillac, and Allan Arguello were also involved in the financing.

Founded in 2020, and an alum of TechCrunch’s Startup Battlefield, Jefa has 115,000 women on its waitlist and the backing of Visa, with whom the firm forged a seven-year strategic partnership. The alliance will enable Jefa to launch a Visa card for the Mexican market, where more than half of the country’s women are unbanked.

“Visa believes in empowering women – from entrepreneurs to home-makers,” Visa Latin America and the Caribbean Senior Director of Fintech Partnerships Sonia Michaca said. “Financial and digital inclusion transform economies. Women, who control the lion-share of everyday household spending, should be at the core of this transformation, yet women are vastly underserved by traditional banks.”

Visa sees the partnership also as a way to help respond to growing demand for contactless payment options. A recent study led by the company underscored rising interest for contactless payments from women in Latin America, with 44% of female consumers in Brazil reporting more frequent use of contactless payments and 58% saying they would not shop at a store that did not offer them. With Jefa, women need only a government-issued ID to open a free, “no minimum balance required” account and access built-in savings apps as well as other “women-tailored features.”

“Jefa is a solution for women that empowers them with the tools they need to create a better livelihood,” Smith said. “At Jefa, we take a multifaceted approach that addresses the numerous barriers women face to entering the global economy. This includes using gender-disaggregated data to inform our product, designing distribution channels to reach women in place they trust, and providing services that are tailored to their distinct financial behavior.”

A graduate of Duke University and The London School of Economics and Political Science (LSE), Smith previously co-founded Eversend, Africa’s first neobank, in 2018. She was also the director of Togo-based Microfinance des Jeunes de Farende where she launched and ran the first microcredit organization for youth in West Africa.

FinovateEurope 2022 is right around the corner. If you are an innovative fintech company with new technology to show, then there’s no better time than now and no better forum than FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22-23, visit our FinovateEurope hub today!

Here is our look at fintech innovation around the world.

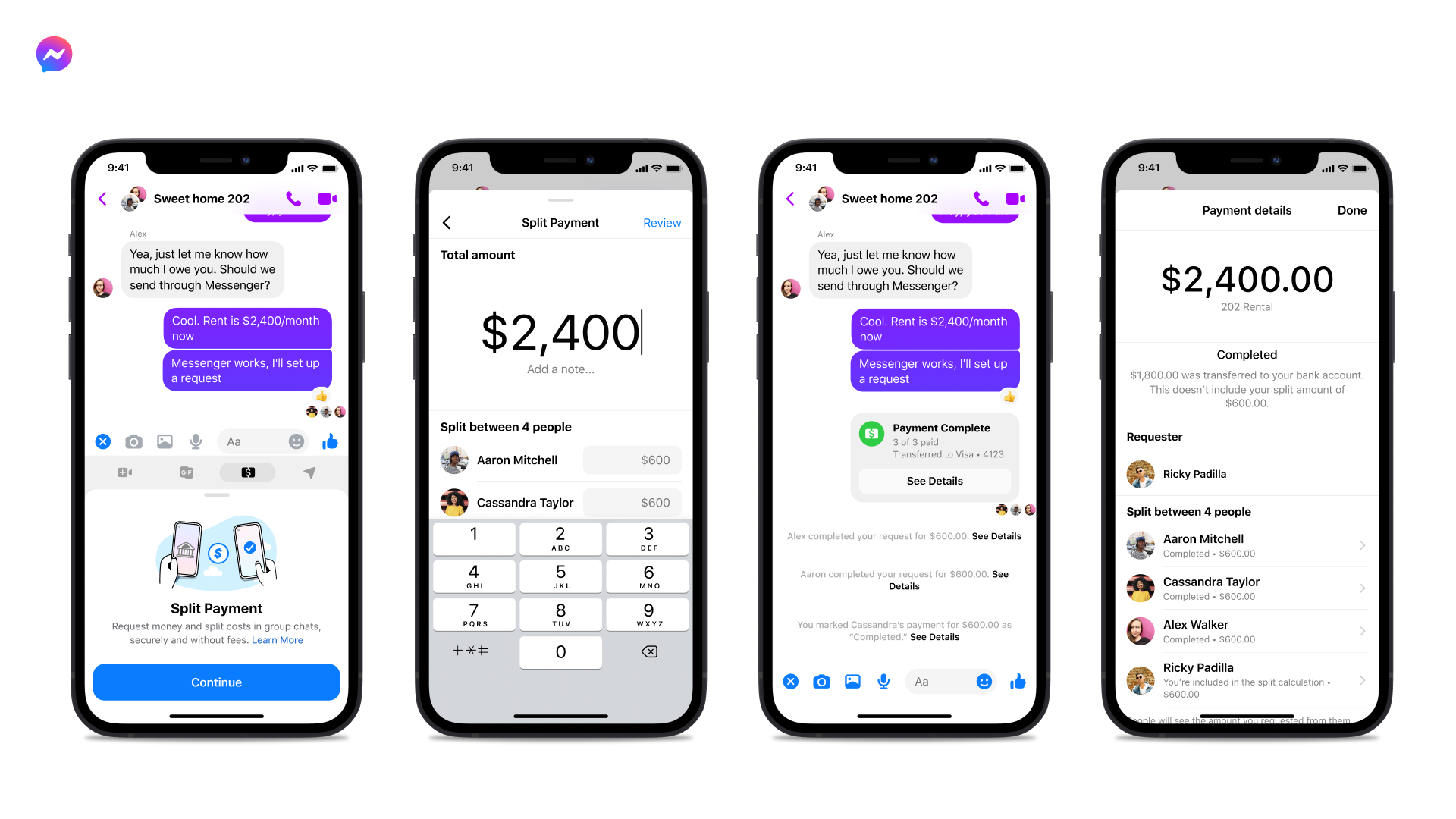

Facebook Messenger unveiled today that it will pilot a feature that will allow users to split payments in the Messenger app. Facebook will begin testing the “free and fast way to share the cost of bills and expenses” next week for users in the U.S.

In a group chat or payments hub within Messenger, users select “get started” and can split a bill evenly or modify each person’s contribution amount. After the amounts are determined, users enter a personalized message, verify their Facebook Pay details, and send their request in a group chat in Messenger.

The launch of Facebook Messenger’s Split Pay feature comes as “Request to Pay” is heating up in the fintech world. Venmo has used QR codes to facilitate person-to-person payments since 2017, and Messenger began using similar functionality in June of this year.

Outside of the P2P realm, Request to Pay is becoming a popular way to replace payment methods such as cards, invoices, and direct debits in B2C and B2B transactions. Essentially, customers can pay for everyday purchases within a messaging framework. Shoppers can, for example, pay for their lunch by opening a push notification on their phone and accepting the payment, thereby finalizing the transaction.