This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateEurope on March 22 and 23, 2022 in London. Register today and save your spot.

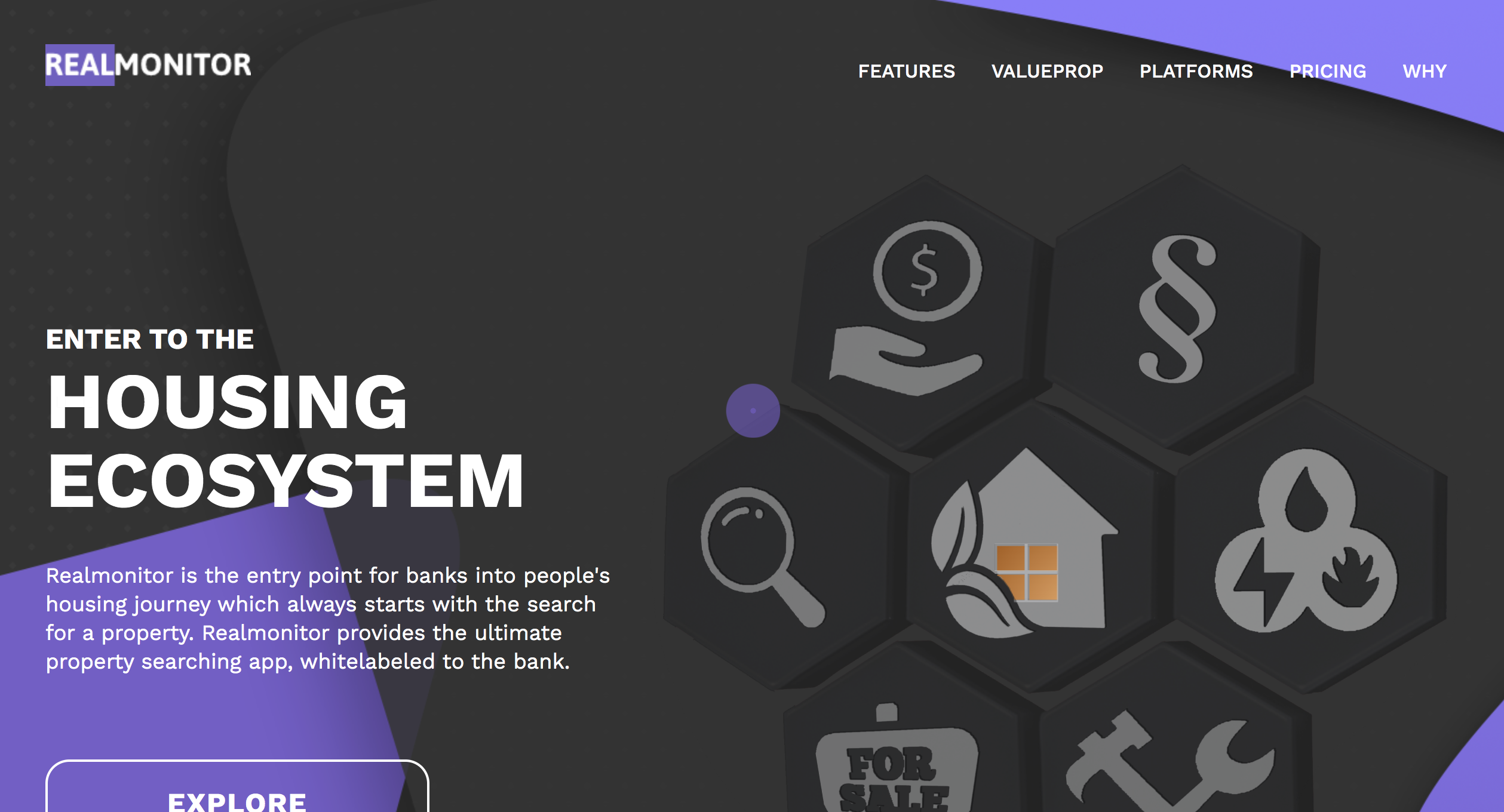

Realmonitor reduces customer acquisition cost for mortgages and significantly lowers the bank’s exposure to the agent network by providing super early customer engagement.

Features

Significantly reduce customer acquisition cost

Provide early customer engagement and super sharp customer profiling

Reduce bank’s exposure to agent networks

Presenter

Peter Farago, CEO and Co-founder Farago has spent the last 15+ years in the bank and real estate industry covering several stages of the housing ecosystem. LinkedIn

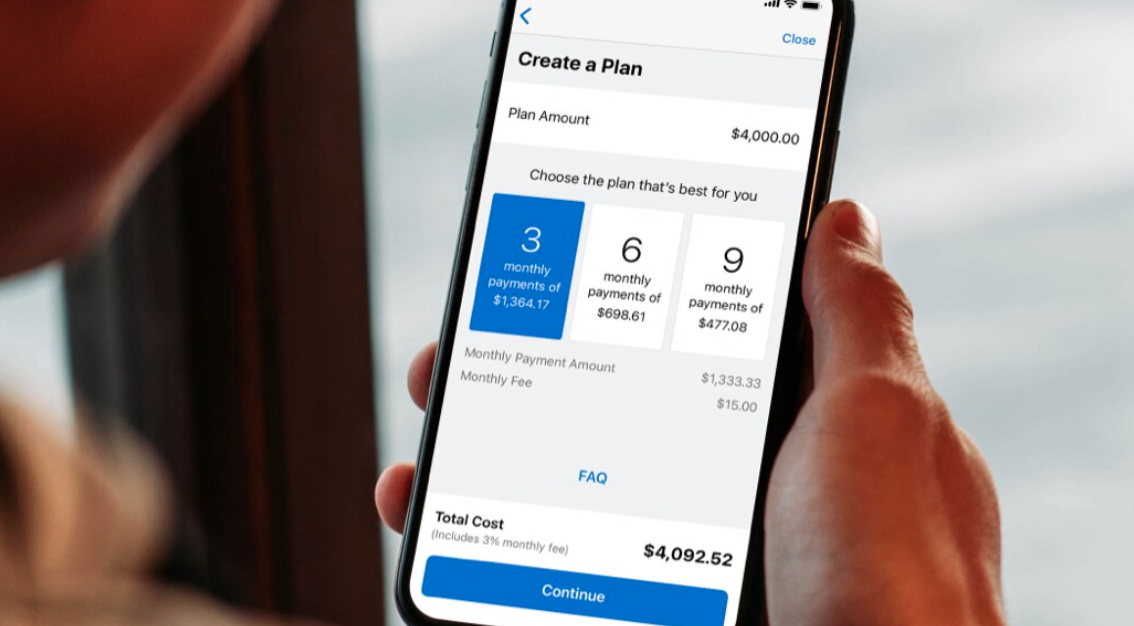

American Express partnered with Delta Air Lines to offer American Express’ buy now, pay later tool, Plan It, as a payment option at checkout.

Plan It allows users to select from one to three repayment options and charges a fixed monthly fee.

Plan It will be added as a checkout option on Delta’s mobile app this spring.

American Express and Delta Air Linespartnered this week to offer their shared customers a buy now, pay later (BNPL) option when booking flights on Delta.com’s web interface.

The partnership, which leverages American Express’ Plan It tool, enables American Express U.S. consumer card members to split up purchases of over $100 into equal monthly installments with a fixed fee.

Launched in 2017, Plan It allows customers to select from one to three repayment options, depending on factors such as the purchase amount, the cardholder’s account history, and their creditworthiness. Plan It charges a fixed monthly fee that is disclosed before the transaction.

As an added advantage over other BNPL plans, Plan It is built into the American Express card and does not require users to enroll, plus cardholders earn rewards as they usually do with their card payment. Further, cardholders do not need to keep track of additional payments, since they are included in their monthly statement.

As Anthony Cirri, Executive Vice President for Global Consumer Lending and Cobrand at American Express highlighted, the timing of the partnership is ideal. “It’s the perfect time to bring these together as people are booking long-awaited trips, and our card members can book with confidence knowing they are backed by the strong partnership between Delta and American Express.”

Plan It has benefited from the rising popularity of BNPL and alternative payment options. The volume of new plans originated in the fourth quarter of 2021 was more than double the volume in the fourth quarter of 2020. And 65% of plans originated in the last year were from new users.

Travelers will see Plan It as a checkout option on Delta’s mobile app this spring.

The partnership marks the first time that an Israel-based fintech company has teamed up with a financial institution from the UAE. The collaboration was made possible by the historic Abraham Accords, signed in the fall of 2020, which normalized relations between Israel and the UAE, Bahrain, Sudan, and Morocco.

“Mashreq Bank is our first customer in the UAE,” ThetaRay CEO Mark Gazit said. “We look forward to accelerating collaboration with additional financial institutions in the UAE and the entire Middle East, as part of the continued expansion of ThetaRay’s global reach.”

Making its Finovate debut in 2015, ThetaRay offers banks and financial payment providers the ability to detect anomalies in multiple data sets, regardless of size or source. This makes the company’s cloud-based, SaaS AI analytics platform is especially effective in monitoring cross-border payments, an area that has become increasingly vulnerable to financial crime – including money laundering – in recent years. ThetaRay estimates that the cross-border payments market will grow from $37.15 trillion in 2020 to nearly $40 trillion by 2026, potentially attracting an even greater number of fraudsters and thieves.

“ThetaRay’s technology, underpinned by advanced machine-learning based models complementing rules, sets the foundation for next-generation transaction monitoring,” Mashreq Bank’s Group Head of Compliance and Bank MLRO Scott Ramsay said. “By combining speed and agility with efficiency, it allows banks to effectively thwart financial crime risks in the increasingly complex space of cross-border payments.”

“Mashreq’s advanced digital transformation program has continued to deliver outstanding service to customers throughout the nine months ending 30th September 2021,” Group CEO Ahmed Abdelaal said. He highlighted the role of digital platforms in supporting the bank’s growth, and embraced the “development of a diverse, inclusive, and enabling working environment” courtesy of Mashreq’s adoption of a “work from anywhere culture.”

FinovateEurope 2022 is just one month away. If you are an innovative fintech company with new technology to show, then there’s no better time than now and no better forum than FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22 and 23, visit our FinovateEurope hub today!

Here is our look at fintech innovation around the world.

Thailand’s central bank will let banks increase the amount they are allowed to invest in fintech – but investing digital assets was excluded from the new higher funding limits.

Backbase has forged a new partnership with New England-area financial institution, Eastern Bank.

Eastern Bank will leverage Backbase-as-a-Service and Backbase Digital Sales technology to streamline its new account opening process, as well as create and release new financial products and services.

With $24 billion in assets and more than 120 locations, Eastern Bank serves customers in eastern Massachusetts, southern and coastal New Hampshire, and Rhode Island.

A new partnership between engagement banking innovator Backbase and Eastern Bank will bring a fully digital account opening experience to the Boston-based financial institution’s customers. Eastern Bank ($24 billion in assets) will deploy both Backbase-as-a-Service and Backbase’s Digital Sales solutions, which will give Eastern the technical infrastructure it needs to create and deliver new products and services faster.

The deployment of Backbase’s Digital Sales solution will enable Eastern Bank to combine Backbase’s out-of-the-box accelerators and integrations with solutions from third-party fintechs to offer their customers personalized digital banking services – as well as remove much of the complexity customers encounter when opening new accounts. Eastern Bank expects to offer Backbase’s Digital Sales capabilities in the first half of this year to new retail customers. The bank’s new commercial and business banking customers can expect a similar offering later in 2022.

“We are thrilled Eastern Bank chose to collaborate with us around this commitment to technology and innovation,” SVP of Americas at Backbase Vincent Bezemer said. “Like us, they are passionate about delivering the best digital experience possible for customers.” Bezemer complimented Eastern Bank’s team as “agile and digitally-focused” as well as having a “human-centered approach” to collecting and incorporating customer feedback to ensure high-quality customer experiences.

Founded in 1818, Eastern Bank offers banking, investment, and insurance products and services for retail consumers and businesses in parts of Massachusetts, New Hampshire, and Rhode Island. The bank earned the 2021 Impact Innovation Award for Artificial Intelligence and Advanced Analytics by Aite-Novarica Group and was a finalist in the Best Small Business Banking Solution category at the 2021 Finovate Awards.

A multiple-time Finovate Best of Show winner, Backbase is one of Finovate’s oldest alums, having made its debut on the Finovate stage in 2009. More recently, the company participated in Finovate’s return to live events last September as part of FinovateFall in New York. At the conference, Backbase demonstrated its complete customer onboarding technology that consolidates customer finances via direct deposit, billpay auto linking, and debit card account opening.

Founded in 2003 and headquartered in Atlanta, Georgia, Backbase was named “Best in Class” among digital banking platform vendors in Javelin’s 2021 Digital Banking Platform Scorecard. In addition to its partnership with Eastern Bank, Backbase has collaborated in recent months with Wyoming-based Blue Federal Credit Union and St. Louis, Missouri-based, family-owned First Bank.

Clients that use U.S. Bank’s prepaid Focus Card for payroll can offer their employees access to their wages as they earn them, thanks to a new partnership between U.S. Bank and Payactiv.

Employees will not only benefit from early access to their wages, but will also have access to Payactiv’s other financial wellness tools.

“We’re proud to be on the leading edge, developing a solution that helps our business clients provide additional convenient options for their employee payroll,” said U.S. Bank Payment Services Vice Chair Shailesh Kotwal.

U.S. Bank is partnering with financial wellness company Payactiv this week. Under the agreement, U.S. Bank will leverage Payactiv’s earned wage access (EWA) tools.

U.S. Bank’s commercial clients that use U.S. Bank’s prepaid Focus Card for payroll can enable their employees to access a portion of the wages they’ve already earned. Employees can access their funds on their U.S. Bank Focus Card, via an instant deposit into their checking account, or other payment options.

In addition to benefitting from early payouts, employees will have access to other financial wellness services such as savings and bill management tools, financial education, and a discounts marketplace.

“The future of payments is one where companies may soon say goodbye to the traditional, biweekly payroll,” said U.S. Bank Payment Services Vice Chair Shailesh Kotwal. “Employers recognize that providing employees on-demand access to earned wages improves employee satisfaction and recruiting efforts. We’re proud to be on the leading edge, developing a solution that helps our business clients provide additional convenient options for their employee payroll.”

Payactiv was founded in 2011 to help companies send their employees their wages as they earn them, as opposed to bi-weekly. “We provide timely access to liquidity – so a single mother can pay for daycare between paychecks and a healthcare worker can cover an unexpected car expense,” explained company CEO Safwan Shah.

California-based Payactiv has raised $134 million in funding and earned a Best of Show award for its 2016 demo. In 2020, the Consumer Financial Protection Bureau (CFPB) approved Payactiv’s EWA program as exempt from the federal Truth in Lending Act and Regulation Z rules governing creditors. “Employers can take comfort in knowing that PayActiv continues to be the leader in responsible EWA for employees,” Shah said at the time.

A week before FinovateEurope’s in-person event begins on March 22nd, our annual Europe-based fintech conference will feature a special Digital Kick Off. This afternoon session on March 15 is accessible from anywhere and 100% virtual. The day will feature a mastermind keynote, a fireside chat, a set of digital demos from fintech innovators, and a power panel on the future of fintech.

Here, we will introduce two of our Digital Kick Off speakers – Zennon Kapron, founder and director, Kapronasia; and Malin Lignell, VP of Digitalization & Innovation, Handelsbanken. For more information on FinovateEurope, including both the Digital Kick Off on March 15 and the in-person event on March 22 and 23, visit our FinovateEurope hub.

Zennon Kapron

Founder and Director of Kapronasia, Zennon Kapron will lead a Mastermind Keynote on our Digital Kick Off day titled The Trends & Opportunities Shaping Fintech in Asia. Kapronasia provides research and consulting services with a focus on financial and blockchain technology.

Previous to Kapronasia, Kapron was Intel’s Global Banking Industry Manager and, before that, CIO for Citigroup Portugal. He has extensive experience with fintech and Asia, currently serving as an instructor in fintech at the Singapore Management University, an ambassador with the Emerging Payments Association of Asia, and founder and director of China Fintech, which works with startups, financial institutions, and investors to build an ecosystem that develops innovative solutions for China’s financial industry.

Kapron is also the author of Chomping at the Bitcoin: The History and Future of Bitcoin in China. He earned a B.S. in Computer Science from Syracuse and an MBA from INSEAD.

Malin Lignell

Vice President of Digitalization & Innovation with Sweden’s Handelsbanken, Lignell will provide a Fireside Chat as part of our Digital Kick Off event on March 15th. A 20+ year veteran of the Swedish bank – the oldest company on the Swedish stock exchange – Lignell has served in leadership roles, including as Deputy Branch Manager, for more than half of her tenure at Handelsbanken. She joined the Digitalization and Innovation team at the bank in the fall of 2019, where she works at both the strategic and operational level to help drive the institution toward greater innovation as it pursues its digitization objectives.

With a special focus on the way that emerging technologies shape and change customer behavior and business models, Lignell has spoken frequently on the challenges that financial institutions face as they undertake digitization. She has noted that while behavioral changes are often the most difficult component of technological transformation, often the forces that help propel change (for example, the global pandemic) nevertheless serve as a powerful and effective incentives to solve new problems in new and creative ways.

Lignell is an alum of the London School of Economics and Political Science (LSE) where she received a diploma in Accounting and Finance. She also earned a Master of Science in International Business Studies and Economics from Ekonomihögskolan i Växjö, and a degree in Business Administration and Economics from The University of Graz.

When your day job keeps you busy for 40+ hours per week, it’s hard to take on new tasks or pay attention to new initiatives. But one thing 2020 taught us is that the digital initiative doesn’t take vacation days. So when enabling technologies and platforms like the metaverse come around, banks and fintechs need to pay attention.

First, let’s look at what the metaverse is and what it is not. You can think of the metaverse as immersive, collaborative internet. In some respects, the metaverse is already here. Users are already collaborating with each other on multiple platforms, and alternate realities– whether in 2D or 3D– have been around for decades. However, though the metaverse will be accessible via virtual reality, it is not the same as virtual reality.

The metaverse is at an early stage and is still not well defined. Despite this, banks and fintechs still need to be paying attention. Here’s why.

It’s not the first time fintech has tried to embrace a different reality

In 2014, many fintechs and even some established financial services companies launched mixed reality experiences in the form of Google Glass, which was released to the public in May of 2014. Top Image Systems (now Kofax), Fiserv, eBankIT, and Wallaby Financial (now Bankrate) all released tools for Google Glass in 2014.

Most are familiar with the fate of Google’s mixed reality glasses– they were discontinued in 2015. The failure of Google Glass is not the point, however. What matters is the speed at which this group developed around the new technology. We can expect the same for the metaverse.

You’re already behind

It’s easy to sleep on trends that seem like they are nothing but hype. Despite that, if you’ve been sleeping on this trend, you’re already behind. JP Morgan announced yesterday that it has joined the metaverse by opening a virtual lounge. Located in Decentraland, JP Morgan’s Onyx Lounge shows a timeline of the bank’s blockchain innovations, has three videos to watch, and has a tiger walking around.

The bank also released a white paper on opportunities in the metaverse. “There is a lot of client interest to learn more about the metaverse,” JPMorgan’s Head of Crypto and the Metaverse Christine Moy told Coindesk. “We put together our white paper to help clients cut through the noise and highlight what the current reality is, and what needs to be built next in technology, commercial infrastructure, privacy/identity and workforce, in order to maximize the full potential of our lives in the metaverse.”

In five years, you’ll wish you had paid attention

If there’s nothing to the metaverse right now, why bother paying attention? Because five years from now you’ll wish you had been paying attention.

While it’s easy to say that about any risk-laden investment such as real estate or tech stocks, you can consider the example of cryptocurrency. What if your organization had been investing in crypto research five years ago? You may have already been leveraging the benefits of stablecoins or smart contracts. The metaverse is just one more way to invest in the future of your organization.

Metaconomy

One very attractive aspect of the metaverse is that it is intertwined with the blockchain. In the metaverse, digital assets will be exchanged for digital currencies in a new economy. There is even speculation that work will take place in the metaverse. According to JP Morgan, $54 billion is spent on virtual goods each year and NFTs have a current market capitalization of $41 billion. Banks won’t want to be left out of this new metaconomy.

It’s where you’ll find your next clients

Generation Z* and Generation Alpha** are not only digital natives, many of them are mixed reality natives. They’ve grown up with virtual reality headsets and spend hours a day in parallel universes such as Fortnite. To capture the attention of this group, there is no doubt that financial services companies will need to meet these young clients where they are.

If JP Morgan’s bet on Decentraland is any indication, banks and fintechs should start planning their first move in the metaverse. However, as Cornerstone Advisors’ Alex Johnson recently pointed out, they may want to hold off on building their first bank branch in the metaverse.

Leading market data API company Xignite launched its cryptocurrency API, XigniteCrypto API, this week.

The new offering helps wealth managers and brokers serve clients interested in trading or investing in digital assets.

The XigniteCrypto API provides real-time and historical data on more than 900 different cryptocurrencies.

Market data API provider Xignite has launched a new solution to help its broker and wealth management customers take advantage of the cryptocurrency revolution. This week, the San Mateo, California-based fintech introduced the XigniteCrypto API, the first API of its kind to combine the large and growing universe of cryptocurrency information with the stock, exchange-traded fund (ETF), and options data that brokers and wealth managers rely upon to serve their clients.

Xignite CEO and founder Stephane Dubois highlighted the challenge of working with cryptocurrencies for the average broker or wealth manager. “Cryptocurrencies tend to operate in their own world,” he explained. “This means that if you want to offer integrated equity, option, and crypto trading or analytics for your clients, you are going to have to cobble up a lot of heterogeneous data from many disparate sources, and that’s a pain.”

The new cryptocurrency API provides real-time and historical quotes for more than 900 different cryptocurrencies, including coins and tokens. The solution features unique API endpoints to help brokers and wealth managers engage digital traders and investors, and provides data and tools such as price alerts, historical charting, currency conversion, and news to help customers make sound trading and investing decisions using cryptocurrencies.

“With our new crypto API, you get the depth of coverage, the quality, and the reliability across all asset classes you need to grow your business – all in one integrated solution,” Dubois said.

A market data innovator for nearly two decades, Xignite launched the first commercial REST API and has since grown into one of the leading providers of market data API solutions to brokers, wealth managers, and fintechs. Today, the company’s APIs are used by 700+ companies more than 500 billion times a month to serve their digital investing clients. A Finovate alum since 2014, Xignite has raised more than $37 million in funding from investors including StarVest Partners and Japan-based QUICK.

Revolut has acquired India-based Arvog Forex. Terms of the deal were not disclosed.

The purchase will help Revolut launch services in India in the latter half of this year.

Arvog Forex has more than 20 branches across India and served more than 15,000 customers last year.

Global financial services innovator Revolut recently acquired Arvog Forex to deepen its roots into India, a region with a population of 1.3 billion and ripe for fintech disruption.

Arvog Forex, an international money transfer and currency exchange company, is headquartered in Mumbai. With more than 20 branches across India, the company served over 15,000 people with its remittances and other forex services last year.

Revolut, which plans to invest $25 million into the Indian market in the coming years, expects the purchase will strengthen its foundation in India. The company initiated its India expansion plans last April after hiring Paroma Chatterjee, a former Flipkart executive, to lead its India operations. Under Chatterjee’s leadership, Revolut plans to launch bespoke financial products that serve the unique needs of Indian consumers.

The company is aiming to launch services in India in the latter half of this year. The Arvog Forex acquisition should streamline this, helping Revolut offer remittances and multi-currency accounts to Indian customers.

Chatterjee calls the buy a “first step” towards the company’s aspiration to usher in a “digital financial revolution” in India. “Our significant investment plans, this acquisition, and the quality of the team we are putting together reflect our intention to rapidly roll out these innovative products and services. India is a key region in our global expansion plan and this acquisition is testament to the rapid strides we want to make here. It is an incredible time to be a fintech company in India and we plan to make the best of this opportunity,” she said.

U.K.-based Revolut was founded in 2015 and has already expanded into other Asia-based countries, including Japan and Singapore, but has yet to enter into China, a market that will prove to be highly competitive. On the other side of the globe in North America, Revolut has applied for a bank charter in the U.S., but withdrew its operations in Canada last March. The fintech plans to reenter the region later this year.

As part of our commemoration of African American History Month, our Alumni Profile feature for this week showcases two African Americans who represented their companies at Finovate events in 2021.

Nathan Gibbons

Nathan Gibbons is Chief Operating Officer of Innovation Finance USA, the company behind QuickFi, a fully digital mobile, self-service business equipment financing platform. QuickFi made its Finovate debut at FinovateAsia during the summer of 2021 and returned to the Finovate stage later that year for FinovateFall.

“Businesses acquire new equipment as they grow, and most equipment is financed by banks or manufacturer finance companies through leases and loans, similar to the way that automobiles are financed by consumers,” Gibbons explained at the beginning of QuickFi’s demo last year. “In fact, roughly a trillion dollars of business equipment is financed each year in the U.S.”

“Unfortunately, the equipment financing process is lengthy, opaque, and takes days or weeks to complete. And this is a real problem. Because there are literally millions of businesses whose growth and success is stifled by a slow, antiquated, equipment financing process.”

Previous to joining Innovation Finance, Gibbons was an executive with First American Equipment Finance, serving as Vice President for five years and as Project Manager for six. Educated at the University of Rochester, where he earned a B.A. in Spanish, Gibbons received his MBA from the University’s Simon Business School. He is both a Certified Lease and Finance Professional (CLFP) and a Certified DISC Behavioral Analyst. He is also a member of the Board of Directors for the Equipment Leasing and Finance Association and the CLFP Foundation.

Headquartered in Fairport, New York, and founded in 2018, QuickFi has partnered with companies like Johnson Controls, SANY America, and Juniper Networks. The company was recognized last November by the 2021 Asset Finance Connect UK Conference and Awards by Asset Finance International. The following month, QuickFi was named a 2021 Pan Finance Award winner in the Innovative Commercial Financial Platform, USA category.

Anthony Heckman

Anthony Heckman is Head of Business Development and Growth for and founding member of unitQ, a product quality monitoring platform that enables fintechs and other companies to pursue a data-driven approach to product quality and enhancement. The company made its Finovate debut at FinovateFall in New York last September.

“We’ve built a world-class, machine learning platform. And today, I’m going to show you how we help some of the best companies in the world – companies like Chime, BRD, Truebill, and Pinterest — fix the right quality issues faster,” Heckman said last year at FinovateFall. “And by doing so, (we help them) improve product quality, (and) important metrics like retention and app store ratings. We’re cutting ‘time to fix’ for some of the best engineering organizations in the world so they can win in hyper-competitive markets like fintech.”

A graduate of the University of Southern California, where he received his Bachelors degree, Heckman earned his JD from the University of Pennsylvania Carey Law School. He is mentor with Defy of Northern California, an organization that helps current and formerly incarcerated men, women, and youth develop the skills they need to pursue legal business opportunities and careers. Heckman is also a board member of Safe & Sound, an organization that works to prevent child abuse.

Based in Burlingame, California and founded in 2017, unitQ raised $30 million in Series B funding last fall in a round led by Accel. With partners including Chime, HelloFresh, NerdWallet and, most recently, PagerDuty, unitQ gives product managers a single, platform with which to observe and benchmark user feedback and product quality signals. Earlier this month, the company unveiled its February 2022 unitQ Scorecard of the highest-ranking apps with the best product quality across a range of different industries.

Madison Dearborn Partners has agreed to acquire MoneyGram in a $1.8 billion deal.

The deal will offer shareholders $11 per share and will make MoneyGram a privately-held company.

MoneyGram anticipates the acquisition will help it advance digital growth and compete against smaller fintechs.

MoneyGram, an 82-year-old fintech, announced today it has agreed to be acquired by private equity investment firm Madison Dearborn Partners (MDP) in a $1.8 billion deal. The transaction is expected to close in the fourth quarter of this year.

When the deal closes, MoneyGram shareholders will receive $11 per share. In addition, MoneyGram, which is currently listed publicly on the NASDAQ under the ticker MGI, will no longer be listed on a public exchange. Logistically, MoneyGram will continue to operate under its own brand. Company CEO Alex Holmes and the existing leadership team will continue to lead MoneyGram from the company’s headquarters in Dallas, Texas to continue to serve its 150 million customers.

Holmes anticipates the deal will not only deliver value to shareholders, but will also help MoneyGram as it seeks to advance its digital growth. “MoneyGram has undergone a rapid transformation over the last several years to expand our digital capabilities and adapt to the evolving needs of our customers. By partnering with MDP and becoming a private company, we will have greater opportunities to innovate and transform MoneyGram to lead the industry in cross-border payment technology and deliver a more expansive set of digital offerings, while leveraging our global platform for new customers and use cases.”

The move will place MoneyGram in a better position to compete with the onslaught of fintechs in the cross-border payments arena. And in today’s increasingly decentralized economy, this competition goes beyond cross-border payments companies of the last decade such as Azimo, Wise, Visa’sCurrencyCloud, and Payoneer. Looking ahead, MoneyGram will need to deepen its crypto roots.

The Dallas-based company dipped its toe in the crypto waters in 2018 when it initiated a partnership with Ripple to leverage xRapid for remittance payments. And last fall, MoneyGram began collaborating with Stellar to enable consumers using Circle’s USDC stablecoin to receive cash funding and payout in local currency.

“We are looking forward to applying our substantial experience growing digital businesses and deep payments knowledge to help MoneyGram further strengthen its market-leading cross-border capabilities and enhance its digital platform,” said MDP’s Managing Director Vahe Dombalagian.

Marqeta and Plaid have teamed up to simplify and streamline the ACH transfer process to enable faster funding of financial accounts.

The collaboration is designed to provide both seamless account funding as well as additional security during data transfer.

Both Marqeta and Plaid made their Finovate debuts as part of Finovate’s developer conference series, FinDEVr.

A partnership between a pair of Finovate alums – card-issuing platform Marqeta and financial data network Plaid – will simplify ACH transfers to make it easier for customers to authenticate and fund their accounts.

Per the agreement, Marqeta customer cardholders will be able to transfer money seamlessly between customers and external accounts, as well as verify and link to external accounts faster. The company’s customers also will be able to keep cardholders informed on the status of fund transfers via real-time notifications, and better manage issues ranging from initiations to cancellations to return. Enhanced security is another benefit of the partnership. Marqeta customers no longer will need to store sensitive information from cardholders’ external bank accounts – relying instead on tokens while Plaid and Marqeta exchange necessary bank account information in the background.

“We’re making it as simple as possible for consumers to access their bank information from one application, and reduce the time it takes to fund and begin using their account,” Marqeta Chief Operating Officer Vidya Peters explained. “Through our Plaid integration, developers building on Marqeta can authenticate users’ bank accounts without the complexity and extra time associated with traditional ACH processing, creating an overall more seamless experience.”

Founded in 2010 and headquartered in Oakland, California, Marqeta is an alum of our developers conference FinDEVr Silicon Valley. The company’s card issuing platform provides businesses with the infrastructure, technology, and tools to build and manage their own payment programs. Last month, Marqeta announced that it has secured certification to operate in three countries in Southeast Asia – Singapore, Thailand, and the Philippines – which means the company’s platform is now enabled in 39 countries around the world. Marqeta announced that, with its further expansion into the Asia Pacific (the company is also active in Australia and New Zealand), it will establish an Asia Pacific regional hub in Singapore later this year.

Also a veteran of our developers conference, Plaid began 2022 with the launch of its data privacy solution, Plaid Portal. The new privacy tool is designed for customers who have used Plaid to connect their financial accounts to apps and services in the U.S. Plaid Portal allows account holders to see which apps have accessed their financial data and to control where the data is shared. The company calls the new offering “one of many tools” under development to give customers both greater visibility into and control over how their data is shared. Ideally, this additional transparency will help allay data privacy concerns and provide users with greater confidence when it comes to taking advantage of increasingly open nature of the modern digital financial ecosystem.