This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Currencycloud teamed up with Future FinTech Labs (FTFT Labs) to help the New York City-based fintech launch its Tempo app.

Tempo is designed to make it easier, more secure and more effective for U.S. immigrants to send money overseas.

Acquired by Visa in 2021, Currencycloud has processed more than $100 billion in cross-border money transfers since inception in 2012.

Global payments solutions and infrastructure company Currencycloud has partnered with Future FinTech Labs (FTFT Labs) to help the NYC-based fintech launch a new remittance solution for U.S.-based immigrants. The new offering, an app called Tempo, will help immigrants living in the U.S. send money securely to North America, Italy, Spain, France, Germany, the United Kingdom, India, and the Philippines.

Tempo will gives FTFT Labs customers access to a multi-currency wallet that makes sending money internationally easier and more cost-effective compared to other high-fee remittance services. Tempo app users will be able to leverage both FTFT Labs’ Conversion Tool to buy and trade currencies and use FTFT Labs’ Funds feature to top off their digital wallet.

“Tempo represents an easy, fast, and secure way to transfer money cross-border,” FTFT Labs CEO Sean Liu said. “Working with Currencycloud and using the breadth of services it allows us to offer our customers a seamless process from start to finish. We are confident we will be able to continue to make remittance a seamless process for our end users.”

Tempo users pay a fee of $2.99 pre-transaction – although the company is currently offering customers fee-free transactions when they sign up. Transfers via Tempo take place instantly rather than over the three business days typical of other money transfer apps, and users can send as little as $20 or as much as $1,500. Tempo sees its transfer amount limit as an advantage compared to other money transfer apps that do not have a limit, seeing the limit as a way to help ensure “a high level of security, by design, for users.” The Tempo app is available for both Android and iOs devices.

Making its Finovate debut in 2012, Currencycloud most recently demonstrated its technology at FinovateSpring 2018. The London-based company serves banks, fintechs, and foreign exchange brokerages, helping them and their customers make seamless and secure cross-border transactions in multiple currencies. Since inception, Currencycloud has processed more than $100 billion transferred between more than 180 countries. Acquired by Visa in 2021, the company includes fellow Finovate alums Dwolla and Mambu among its partners. Currencycloud maintains offices in New York, Amsterdam, Cardiff, and Singapore.

“Migrants in the U.S. should be able to send money cross-border without friction and without prohibitive costs,” Currencycloud VP of Sales Lewis Nurcombe said. “A fintech like Future FinTech Labs understands the needs of working people wanting to send money to family and friends, and as such is successfully reimagining how money flows for this huge market.”

Future FinTech Labs is a subsidiary and research and development center for FTFT Group. FTFT Labs is dedicated to designing, developing, and providing operational support for FTFT’s digital banking and payment services offerings.

Active in 15 countries in Latin America, payments infrastructure provider Geopagos has secured an investment of $35 million. The equity funding round was led by Riverwood Capital and featured participation from Endeavor Catalyst. The sum represents the company’s first institutional financing and will be used to fuel the development of new embedded payments solutions and help the firm expand throughout Latin America.

Geopagos provides financial institutions, fintechs, retailers, software companies and other organizations with end-to-end digital solutions to help them launch or grow their payment acceptance businesses in the area. These solutions include terminals that enable mobile phones to operate as point of sale devices as well as technology that turns websites into e-commerce platforms.

With clients including Santander, BBVA, Banco Estado de Chile, and Finovate alum Fiserv, Geopagos processes more than 150 million transactions and more than $5 billion in volume a year. The Buenos Aires-based company was founded in 2013 by Sebastián Núñez Castro, Julián Lisenberg, Fernando Tauscher, Raúl Oyarzun and Damián Harburguer.

“Latin America is a market with very low card penetration and Geopagos is well positioned as a software enabler and infrastructure provider to boost card acceptance and digital payments across the region,” Riverwood Capital co-founder and managing partner Francisco Álvarez-Demalde said.

Speaking of payments in Latin America, blockchain-enabled accounts receivable and B2B payments company PayStand has acquired Yaydoo, an accounts payable, cash flow management, and liquidity solution provider based in Mexico. Yaydoo is one of the fastest-growing startups in Mexico, with more than 150 employees working in more than six different countries. Founded in 2017 and operating throughout Latin America Yaydoo raised $20.4 million in Series A funding last year and this year was named a “Súper Empresa 2022” and a “Súper Empresas para Mujeres 2022” by Expansión Top Companies México.

“Together, PayStand and Yaydoo will redefine the boundaries of B2B fintech across the continent,” PayStand CEO Jeremy Almond said. “The combined company will be one of the first global B2B blockchain platforms at a significant scale. The resulting company will have processed over $5 billion in payments, added 300 additional employees, and built a network of over 500,000 connected businesses, the largest of any commercial B2B blockchain in the world.”

Founded in 2013, PayStand made its Finovate debut at our developers conference, FinDEVr Silicon Valley, one year later in 2014. The company leverages blockchain and cloud technology to digitize receivables, automate processing, lower time-to-cash, remove transaction fees, and drive new revenue. A member of the 2021 CB Insights Fintech 250 and named to the Inc. 5000 for a second year in a row in 2021, PayStand has secured $86 million in funding, most recently raising $50 million in a Series C investment led by NewView Capital and featuring participation from SoftBank’s SB Opportunity Fund and King River Capital.

Here is our look at fintech innovation around the world.

This week, we take a look at more of the fintech entrepreneurs, analysts, and experts who will share their knowledge and insights into the fintech industry at FinovateFall next month.

Day One will feature Joe Lichtenberg, Global Head of Product and Industry Marketing for Intersystems, with his Mastermind Keynote address: How Next Generation Architectures Empower Financial Services Firms with Trusted Business Insights. Lichtenberg’s morning presentation will introduce a new architectural approach that is providing business decision makers with a consolidated, accurate, and real-time view of their business.

Personetics President of the Americas Jody Bhagat will deliver a Mastermind Keynote: How Mid-Market Banks Can Find Their Sweet Spot with Digital Plus Human Interactions in the afternoon of Day One. Bhagat will discuss how mid-market banks can evolve their relationship models to do more of what they do best: supporting customers with advanced money management capabilities and Digital Plus Human interactions.

VantageScore EVP and Chief Product Officer Rikard Bandebo will deliver a Mastermind Keynote in the afternoon of Day Two of FinovateFall. In a presentation titled Leveraging Data Analytics to Drive Financial Inclusion, Bandebo will talk about new tools and analytic strategies to discover not just newly scoreable consumers, but newly lendable consumers, as well.

Day Three of FinovateFall will feature a Mastermind Keynote during the Payments Stream. Tom Ward, Partner with Sidley Austin LLP and recent CFPB Enforcement Director, will deliver an address titled The CFPB in the Biden Administration – Enforcement and Regulatory Priorities for Fintechs in 2022 and Beyond. Ward’s presentation will explain the CFPB’s enforcement priorities as they relate to fintech and the organization’s current focus within the industry.

Co-founder and Chief Impact Officer for Symend Tiffany Kaminsky will deliver a Mastermind Keynote during the Customer Experience Stream on Day Three. Kaminsky’s presentation – Upping the Ante: Using the Science of Decision-Making for Effective Customer Engagement – will help businesses leverage behavioral science to better engage with customers and hyper-personalize customer outreach efforts.

Our Artificial Intelligence Stream on Day Three will feature a Mastermind Keynote from Kore.ai SVP of Marketing Michael Kropidlowski. In his address – Creating Extraordinary Customer and Employee Experiences for the Banking World – Kropidlowski will show how conversational AI is revolutionizing the customer experience in banking.

Visit our FinovateFall 2022 hub today and reserve your seat. Register by September 2nd and take advantage of early-bird savings!

Alliant Credit Union announced a partnership with lending-as-a-service fintech Upstart.

The agreement will make Alliant part of the Upstart Referral Network.

Upstart SVP of Lending Partnerships Michael Lock said the move will help Alliant “grow its membership while providing greater access to affordable credit.”

Alliant Credit Union first partnered with Upstart in May 2022. With today’s announcement, Alliant becomes part of the Upstart Referral Network. Under this agreement, Upstart offers qualified loan applicants tailored loan offers in around five minutes. When the applicant decides to pursue the loan opportunity, Upstart transitions the client from its own user interface to an Alliant-branded experience, where they finish the online member application and close the loan.

“As part of the Upstart Referral Network, Alliant will be able to grow its membership while providing greater access to affordable credit,” said Upstart SVP of Lending Partnerships Michael Lock.

With more than 650,000 members and over $15 billion in assets, Alliant Credit Union is among the top 10 U.S. credit unions. Alliant SVP, Chief Capital Markets Officer, and Head of Commercial Lending Charles Krawitz said that the company is “very particular” when it comes to selecting partners. “Our partners must embrace doing things the right way, with legal and risk compliance maturity,” said Krawitz. “We believe Upstart has invested in robust systems that ensure borrowers are well-vetted, and that they will make a strong partner for delivering value and options to our members.”

Founded in 2012, Upstart differentiates itself in the alternative lending space by partnering with banks and credit unions seeking to increase their approval rates and lower their loss rates. The company’s AI-first lending tool enables financial institutions to reach a wider variety of end customers, including those with less favorable credit files.

Upstart went public in December 2020 and was in the news headlines recently due to concerns about a drop in funding as well as a decline in earnings. Company CEO Dave Girouard said that the decline was “disappointing” and “unacceptable,” adding, “It may be natural for you to question whether Upstart’s AI-powered risk models aren’t working as designed, but we’re confident this isn’t the case, that, in fact, our models continue to improve with respect to accuracy and risk separation.”

Teslar Software announced a partnership with Missouri-based community bank, The Seymour Bank.

Courtesy of the deal, The Seymour Bank will use Teslar’s lending process automation platform to modernize and streamline its commercial lending business.

Teslar Software made its Finovate debut at FinovateSpring 2015 in San Francisco.

The Seymour Bank, a Missouri-based financial institution with more than $137 million in assets, has selected Teslar Software to enhance its commercial lending strategy. The bank will use Teslar’s lending process automation platform to reduce reliance on manual processes and boost efficiencies..

“With Teslar, we will become more accessible to our customers, delivering a portal that allows them to easily and quickly monitor the status of their loans and securely communicate with us,” The Seymour Bank vice president Heather Johns said. “Plus, Teslar’s automated workflows will save time for our employees, resulting in a better, more efficient experience.”

In addition to the digital customer portal, designed to improve convenience, The Seymour Bank will also leverage Teslar’s technology to improve its ability to track documentation and monitor exceptions. The institution, founded in 1939 and headquartered in Seymour, MIssouri, outside of Springfield, prides itself in its commitment to local involvement and customer service. But, in the words of Johns, the bank “also want(s) to be recognized for modern technology and seamless experiences.” The partnership with Teslar will bring the benefits of modern, automated technology to both the bank’s customer-facing and back office operations.

“The Seymour Bank is a locally owned bank that has prioritized serving its customers and community for more than 80 years,” Teslar Software founder and CEO Joe Ehrhardt said. “We look forward to supporting the bank as (it provides) more digitized, seamless interactions to enhance both the customer and employee experience.”

Teslar’s partnership with The Seymour Bank comes just weeks after the firm announced that it had teamed up with National Bank & Trust to streamline the Texas-based financial institution’s lending process with a new suite of automated workflow and portfolio management tools. Chartered in 1888 as The First National and headquartered in La Grange, Texas, National Bank & Trust is a full-service bank dedicated to providing customized service, “lightning fast lending”, and future-focused technology.

Winner of the 2020 Finovate Award for Best Fintech Partnership for its PPP.bank initiative – a free website developed in collaboration with Citizens Bank of Edmonds and Mark Cuban – Teslar Software was founded in 2008 and made its Finovate debut at FinovateSpring in 2015. Since then, the company has grown into a robust, portfolio management system provider and strategic partner to help community and regional banks compete in an increasingly tough and crowded environment for lending services.

The customer journey is vital in today’s financial services landscape and cloud-enabled business innovation is the vital ingredient.

A good user experience is a critical factor in helping consumers differentiate between firms and helping brands build lasting relationships with customers.

According to the Harvard Business Review, firms with leading customer satisfaction rankings can grow their revenues two and a half times faster than their competitors. Moreover, research by Forrester demonstrates that customers are over twice as likely to stick with a brand when their problems are solved quickly.

Yet, great digital experiences rely on intuitive GUIs and an agile, cloud native strategy, both of which are not easy to achieve. In this article, we’ll demystify how to get started with cloud computing in software engineering for banking and help you develop a leading customer UX.

What Are the Challenges of Cloud Business Innovation in Banking?

Approximately US$1.3 trillion was spent in 2020 on digital transformation, yet Deloitte data shows 70% of projects fail. That equates to over US$900 billion wasted — so what’s going wrong?

Just as an HD TV relies on good HD content, great apps need high interactivity with data, an always-on presence, security, and scalability to perform under high demand.

Eric Newcomer, WSO2 CTO, argues that cloud business innovation goes wrong when there’s a messy middle. In other words, when there’s a lack of clarity about how strategy, outcome, and skill coordinate the microservices within a platform, cloud business innovation becomes dysfunctional.

Within banking specifically, the stakes of digital transformation are extremely high. Today’s financial services firms must deal with an onslaught of cyberattacks and regulatory constraints, not to mention increased competition from new fintech entrants better-equipped to deliver excellent customer experiences. So how can financial institutions ensure they foster an innovative and successful cloud-first environment?

How to Overcome These Challenges

Great cloud computing in software engineering needs equally great cloud native practices and technology, focusing specifically on integration and APIs. Without this focus, customers lose the always-on, always integrated feel that today’s users demand.

Therefore, financial services firms require an all-in-one platform delivering accelerated and enhanced engineering processes to speed up innovation in their cloud environment. Unfortunately, building robust and agile platforms from scratch can be timely and costly.

Instead, partnering with existing solutions providers allows financial service firms to focus on developing cloud banking innovations and better deliver security, compliance, and ideal customer experiences. You can read more about overcoming challenges for banks to generate fintech innovation here.

The Role of Digital Platform-as-a-Service Within Financial Services

An “opinionated” digital platform-as-a-service (digital PaaS) accelerates cloud banking innovation by tackling some of the core complexities of developing digital applications. As a result, you can build, deploy, and iterate new versions more easily.

Digital PaaS platforms enable diagrammatic and low-code functionality, providing a great developer experience. In turn, your teams can increase their productivity and attention to quality assurance for end-users.

Moreover, digital PaaS integrates with automated deployment tools using Docker and Kubernetes. As a result, you can test, develop, and deploy new user features for maximum customer satisfaction faster than ever before, using just a few clicks.

Digital PaaS solutions deliver seamless platform functionality and integration with your existing data warehouses, allowing you to leverage efficient and scalable consumer solutions.

How Low-Code Digital PaaS Enables Cloud Computing in Software Engineering

There isn’t a one-size-fits-all solution to cloud computing in software engineering, so what makes a digital PaaS-based method the most appropriate for financial services?

A digital PaaS approach provides a highly stable environment to create and manage APIs since it establishes core conventions and assumptions within your workflows. These assumptions include the programming language and dev environment, all the way to the publishing process on software marketplaces. As a result, you can remove barriers to collaboration and shorten project lead times. Similarly, as a cloud-enabled solution, you provide collaborative space for your teams to work.

Moreover, you can easily build platform microservices and provide teams with autonomy over their software output. Software teams can publish updates to critical platform elements accordingly without jeopardizing the rest of your platform or relying on slower project teams, keeping your user experience competitive.

However, the benefits don’t stop when you hit publish. Digital PaaS solutions allow you to run professional DevOps systems and make improvements in step with live user trends. Consequently, you can remain competitive and establish a close relationship with customers.

Finally, once your APIs are built, you can share them through marketplace and import or export data with other SaaS platforms. As a result, you can leverage other data sources for enhanced features. For example, you can capitalize on open banking ecosystems, enhance your security through additional identity checks, and more.

And so, with complex development and deployment tasks that are both easy to learn and use, you can deliver fresh digital services faster — and more accurately — than ever.

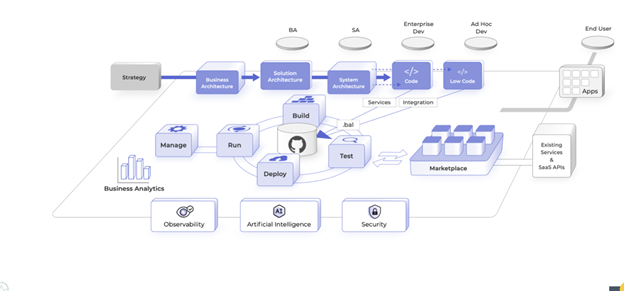

Introducing Choreo by WSO2

With around only three in ten digital transformations being successful and the heightened competition within banking today, financial services companies need to innovate at speed and scale.

Choreo is a digital PaaS that helps companies manage and develop APIs, services, and integrations quickly. Choreo enables developers and operations teams to go from ideation to production in hours or days versus weeks and months via a seamless environment that eliminates the complexity of cloud native computing.

Choreo provides a diagrammatic and pro-code environment side by side, allowing you to create an outline and make detailed tweaks in minutes. It includes a developer marketplace with over 400 pre-built connectors that makes it easy to discover, reuse, publish, and share.

With security and transparency at its foundation, you can easily trace code changes and root issues across your entire development history. You can also benefit from AI-assisted coding and enhanced governance features.

Find out more about Choreo and create an API with just a few clicks.

A look at the companies demoing at FinovateFall in New York on September 12 and 13. Register today and save your spot.

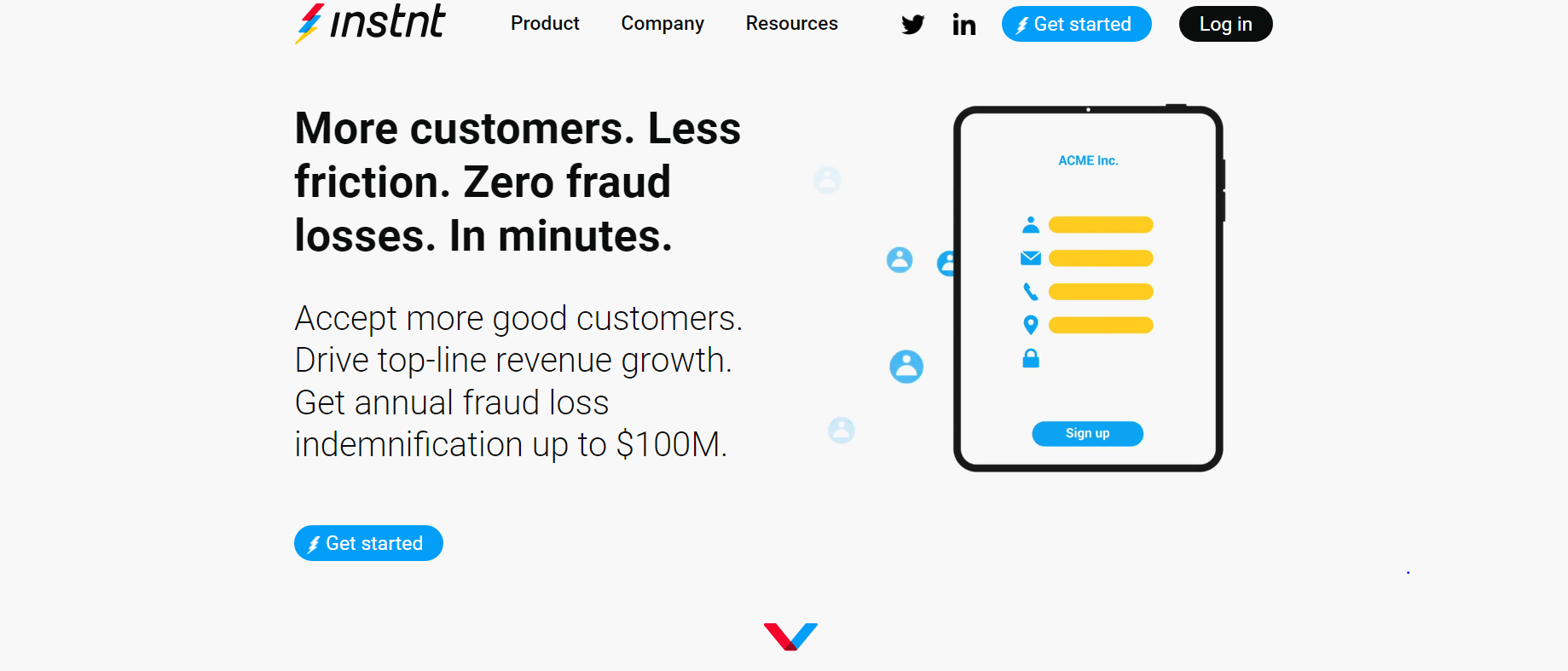

Instnt’s fully-managed Customer Acceptance Platform helps businesses sign up and accept 50% more good customers with zero fraud loss for good, with continuous, portable identity assurance.

Features

One-click frictionless customer acceptance

Day 0 to Day N continuous identity assurance

Decentralized, reusable KYC verification

Why it’s great

Instnt provides frictionless customer acceptance experiences without compromising on security, risk and compliance.

Presenters

Sunil Madhu, CEO Madhu is a serial entrepreneur operating in Security, Risk & Compliance for over 30 years. Recently, he founded and was the CEO of Socure. LinkedIn

Justin Kamerman, CPO Kamerman has over 20 years of experience designing and building high performance distributed systems in the telecommunications, IPTV, identity verification, social media analytics, and IIoT industries. LinkedIn

Frictionless account access without pins/passcodes/passphrases

24/7 customer service with a user friendly, conversational IVR

Better security with biometric voice authentication

Why it’s great

The Illuma Shield Voice Authentication + Posh Conversational IVR integration improves operational efficiency, security, and customer experience for community banks and credit unions.

Presenters

Milind Borkar, CEO & Founder, Illuma Labs Borkar brings a background in R&D and more than 50 successful product launches to his role at Illuma Labs. LinkedIn

Karan Kashyap, CEO & Co-Founder, Posh Posh is a conversational AI fintech working with FIs. Kashyap is an alumni of MIT’s Artificial Intelligence Lab. LinkedIn

Chad Rogers, EVP & COO, Connexus Credit Union At Connexus Credit union ($4.9B in assets), Rogers leads a talented senior leadership team delivering exceptional experiences to ~420K members nationwide. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 12 and 13. Register today and save your spot.

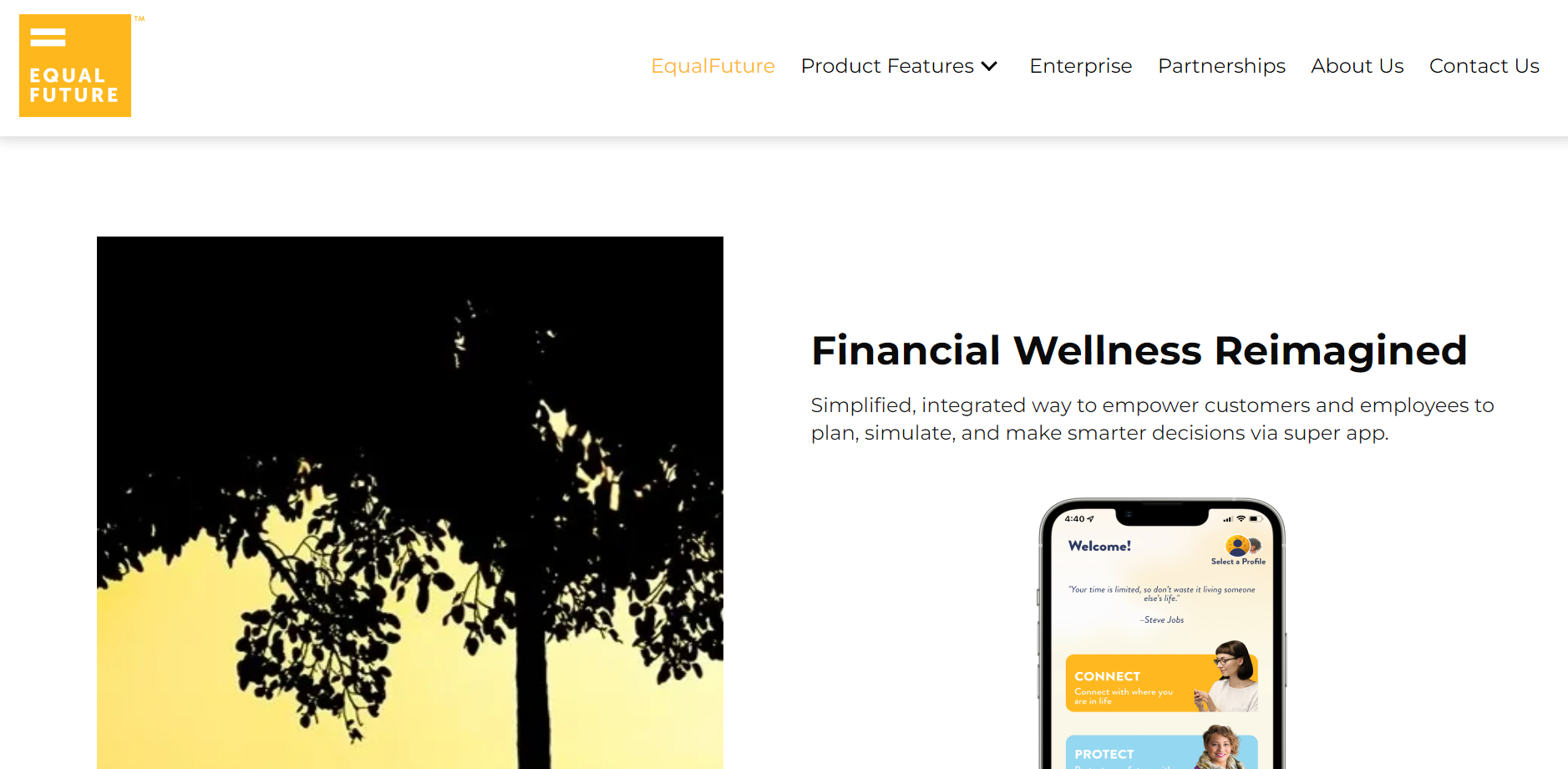

EqualFuture’s Super App reimagines financial wellness through a simplified, integrated way to empower people to plan, simulate, and make smarter decisions.

Features

Includes “Someone Like Me” features that help users create their profiles

Supports goal/scenario-based financial decisions through interactive, gamified tools

Uses cashflow modeling to stay on track

Presenter

Joyce Phillips, CEO & Founder Joyce Phillips is an awarded leader, innovator, and marketer. Phillips brings significant global financial expertise, previously holding executive leadership roles with iconic corporate brands. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 12 and 13. Register today and save your spot.

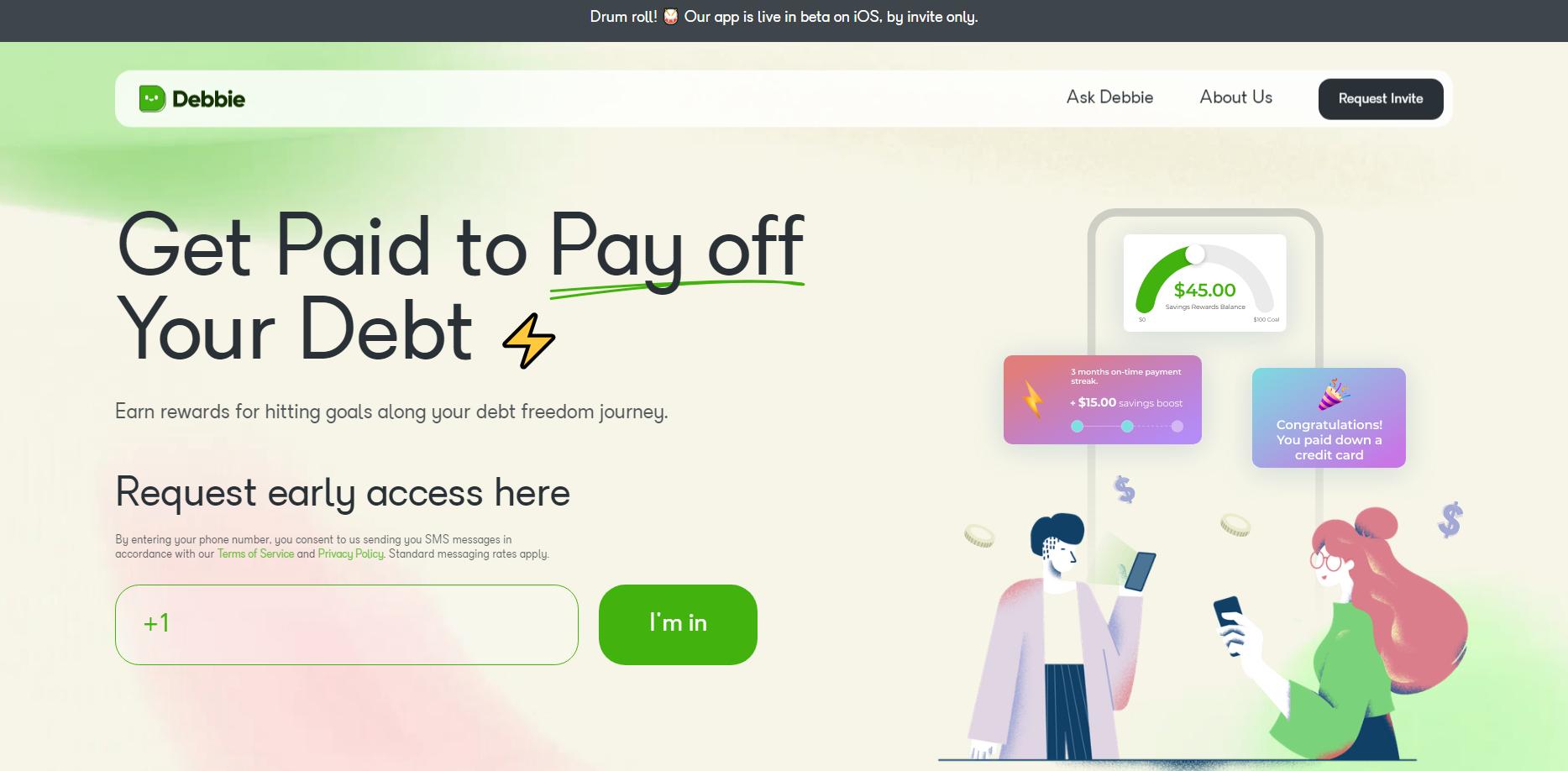

Debbie is the Noom for debt loss, utilizing behavioral psychology and rewards to motivate and incentivize people to crush their debt, for good.

Features

Utilizes behavioral psychology through a guided debt loss program to help users unwind habits

Provides time trended credit data to pre-qualify users for refi

Offers users micro-rewards for improved behavior

Why it’s great

Debbie users pay down on average $450/month of debt, while setting aside savings of $100/month consistently. For folks in $5k-$10k of debt who are making $50k/year, this is significant.

Presenters

Frida Leibowitz, CEO Ex-Credit Risk at Marcus by Goldman. Immigrant, first-gen student from a single parent home. Passionate about financial security because she’s experienced crushing debt while attending NYU. LinkedIn

Rachel Lauren, COO Former VC at BDMI and software equity research analyst at Credit Suisse. Passionate about financial behavior after seeing her family struggle with money management and financial shame. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 12 and 13. Register today and save your spot.

SESAMm specializes in big data and AI. At FinovateFall, the company is demoing its ESG Monitoring and Alerting product that detects controversies and positive impact events on web data.

Features

ESG controversies and SDGs positive impact topics identification on 5+ million companies

Event monitoring on private and public companies

Delivery methods: Daily emails, cloud and CRM integration, among others

Why it’s great

SESAMm’s ESG and SDG Alerts leverage AI to give firms the ability to monitor millions of public and private companies worldwide, providing more objective indicators.

Presenter

Sylvain Forté, CEO Sylvain Forté, CEO and Co-Founder of SESAMm, created the company in 2014 based on his passion for artificial intelligence and finance after receiving a double degree in engineering. LinkedIn

What is venture capital doing to help promote fintech innovators who come from underrepresented groups and communities?

We caught up with Elizabeth McCluskey, Director of The Discovery Fund at CMFG Ventures, to talk about her work in supporting underrepresented entrepreneurs that are building solutions to drive financial inclusion.

We discussed her own extensive experience in financial services, working in both investment banking and wealth management before moving to venture capital. We also learned why she believes it is important to invest in female founders and founders from communities that are underserved by traditional financial institutions.

Why did you decide to transition from investment banking and wealth management to venture capital? What do you enjoy about working at a venture capital firm?

ElizabethMcCluskey: Investment banking is transactional. I enjoyed being part of transformational deals for companies but missed being there for the long-term impact. When I pivoted to wealth management, I was able to develop more longevity in client relationships, but the investments were focused on public equities with which I had minimal connection. These experiences led me to find the ideal balance in venture capital. Now I can build more intimate relationships with portfolio companies and invest in people and ideas that are meaningful and important to me. It brings joy and satisfaction to support their long-term growth and success.

Tell me more about your current role at CMFG Ventures and the Discovery Fund.

McCluskey:CMFG Ventures is the venture capital arm of CUNA Mutual Group. CMFG Ventures invests in fintechs to help financial institutions grow and provide a brighter financial future for all. The firm adds value to fintechs by leveraging its well-established network of over 6,000 financial institutions and suite of complimentary technology solutions. Since 2016, CMFG Ventures has invested in nearly 50 fintech companies and its Discovery Fund has invested in 14 additional early-stage companies led by BIPOC, LGBTQ+, and women founders.

I am the director of the Discovery Fund. The Discovery Fund was created to support underrepresented entrepreneurs who are building solutions for financial inclusion. We plan to invest $15 million over the next three years in early-stage fintech companies. Through my role, I’m able to see the full scope of venture capital investing, including but not limited to:

Sourcing deals and meeting entrepreneurs

Conducting due diligence

Negotiating the terms of the deal

Providing long-term support for entrepreneurs’ journeys by helping them scale, network, and find the resources they need to continue to succeed.

Why is it important to invest in diverse founders, especially women-led businesses? And what qualities you look for when investing in these companies?

McCluskey: Women entrepreneurs receive less than 3% of venture capital funding. This staggering number demands that we take a step back and focus on supporting diverse founders, especially women-led businesses, to improve equity in the venture capital space. This is not just the right thing to do – it’s good business. A 2018 BCG study concluded that women-founded businesses yielded two times as much revenue per dollar invested as those founded by men.

Women and diverse founders who have been historically underserved by traditional financial services are working hard to create the financial inclusion they wish they had. We are investing in entrepreneurs like them who are deeply connected to the problems they’re solving. Empowering underrepresented leaders is already creating new opportunities for liquidity management, wealth management, credit access, asset protection, and more.

Can you share more about the women-led businesses that CMFG Ventures invests in and supports? How are they helping make the financial services industry more inclusive?

McCluskey: CMFG Ventures has made investments in multiple women-led companies, such as The Beans, Climb, Caribou, and Frich to help the financial services industry become more inclusive.

The Beans simplifies the path to financial balance through evidence-based design and cutting-edge technology, so consumers stress less about money and focus on what they love.

Climb is a student lending and payments platform intended to make career education more affordable and accessible.

Caribou enables financial advisers to engage their clients in healthcare planning to support life transitions and build stronger financial futures.

Frich makes money social. It helps Gen Z develop better financial habits leveraging the power of community and benchmarking.

These female-driven fintechs are transforming the financial services space and improving the financial lives of everyday Americans.

What advice do you typically share with women founders? What about those looking to break into the VC space?

McCluskey: I would give the same advice to women founders as I do with men: always ask for feedback, especially to better understand why someone is telling them “no”. Founders who send updates over time allow me to track their progress, including growth and consistency of their business plans. In several cases, I’ve ended up investing in companies that I passed on in earlier rounds. And even if someone says “no” to doing business together, they can still be a valuable ally. Attempt to stay in touch and leverage their networks. People are often willing to share their connections and provide valuable guidance.

As for those looking to break into the VC space, I believe it is slowly becoming more inclusive and representative, yet it is still a very network-based profession. Similar to my advice for entrepreneurs, start with one person you know (or cold outreach via alumni networks, common interest groups, etc.). From there, ask every person you talk to for an introduction to at least one other person. Focus on growing your network with the goal of building genuine relationships, not necessarily getting a job right away. This is a long-term investment in your career.

We’re more than halfway through the 2022, what do you predict for the rest of the year?

McCluskey: After record levels of investments in 2021, we all knew things had to cool off. However, I believe the pace at which this has happened surprised VCs and entrepreneurs alike.

In fact, startup funding has fallen by 23% over the last 3 months, bringing us back to 2019 levels. For many, it probably feels like the sky is falling, but there is still a significant amount of money in circulation. Venture capitalists today, and by extension founders, are more focused on “real” metrics versus vanity metrics when deciding which companies to fund. The companies that will do well in the second half of the year will have measurable revenues, not just wait lists, and will be managing costs and runway to drive profitability, not endless cash burn.