This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

“With eBay International Shipping, we’re making global connections even more accessible, affordable, and profitable, significantly increasing the volume of items available to shoppers in 200+ countries and making it even easier for our sellers to tap a universe of new business opportunities,” eBay U.S. VP and GM Adam Ireland said.

According to Juniper Research, the value of cross-border ecommerce will top $2.1 trillion this year. But the cross-border ecommerce market is not without its complications. Businesses must navigate through a range of customs duties and import taxes in a process that can be both complex and costly. Using Avalara’s software, eBay International Shipping determines Harmonized System (HS) commodity classification codes, identifies item-level trade restrictions, and generates landed cost pricing for more than 200 items hosted on eBay. The new offering will help the platform’s more than five million merchants sell to more than 70 million buyers worldwide.

“With Avalara’s cross-border solutions embedded within eBay’s International Shipping program, we’re able to simplify cross-border compliance complexity and reduce potential customer experience disruptions by providing more transparent landed cost pricing for global buyers and helping ensure parcels meet local customs requirements,” Avalara EVP and GM of Indirect Tax Jayme Fishman said.

Avalara made its Finovate debut at our developer’s conference, FinDEVr SiliconValley in 2015. In the years since, the company has grown into a leading regtech with more than 30,000 customers across 95 countries. Avalara went public in 2018. The firm was acquired in 2022 by Vista Equity Partners in a deal valued at $8.4 billion. Headquartered in Seattle, Washington, Avalara was founded in 2004. Scott McFarlane is CEO.

Raisin has appointed Cetin Duransoy as CEO of the company’s U.S. division, SaveBetter by Raisin.

Duransoy comes to Raisin from Fundbox, where he served as President and COO.

Today’s announcement follows Raisin’s $64.7 million capital raise in March of this year.

Savings and investment product marketplace Raisin has appointed a new CEO for its U.S. savings division. The Berlin-based company has selected Cetin Duransoy to head SaveBetter by Raisin, its U.S. savings platform originally launched in 2020.

Duransoy

Raisin launched SaveBetter in 2020 to serve as an online marketplace where customers can choose from a variety of savings products, including savings accounts, money market deposit accounts, and certificates of deposit. The savings tool enables users to access more favorable rates than most traditional savings accounts from a single portal.

SaveBetter has seen impressive growth recently, having added $1 billion in assets under management in the past three-to-four months. Additionally, over the same time period, the company has brought 30 financial brands onto its online marketplace.

In the release, Duransoy said this is an “exciting time” to join Raisin as CEO. “Having already established itself in the U.S. market, demonstrating scale to banking partners and tangible benefits in increased returns for everyday Americans, Raisin is poised to lead the way in further disrupting the American cash savings market and providing a valuable tool to help millions of savers secure their financial future,” he added.

Duransoy has more than 20 years of experience in financial services. He most recently served as President and COO Fundbox, and has also held senior positions at companies including Capital One and Visa.

Today’s announcement comes just over a month after Raisin raised $64.7 million (€60 million) in a Series E funding round led by M&G’s Catalyst and Goldman Sachs. The round boosted Raisin’s total funding to almost $305 million since it was founded in 2012.

Raisin counts more than one million customers and $31.7 billion (€38 billion) assets under management across the U.S., U.K., and European Union. The company taps its network of more than 400 banks and financial service providers from 30+ countries to offer its catalogue of savings, investment, and pension products. Tamas Giorgadse is Co-Founder and CEO.

May is Asian-American/Pacific Islander Heritage Month. May is also the month that brings Finovate back to San Francisco for our annual spring fintech conference, FinovateSpring.

To this end – and to officially launch our Asian-American Month Commemoration – we’re highlighting the women and men of Asian-American heritage who will be taking the stage at FinovateSpring May 23 through May 25.

As Financial Literacy Month draws to a close, we reached out to Parker Graham, founder and CEO of Finotta. We wanted to hear his thoughts on what it means to be financially literate at a time of major digital transformation and technological change – both in financial services and in the world writ large.

Finotta enables banks and credit unions to personalize their mobile banking experiences for their customers. Headquartered in Overland Park, Kansas, and founded in 2018, Finotta helps smaller financial organizations generate new revenue streams, boost user engagement, and compete with larger financial institutions.

Finotta made its Finovate debut last year at FinovateFall.

What does it mean to be financially literate in 2023?

Parker Graham: For many people, managing their finances and staying financially literate is not just a challenge – it feels harder than ever.

With decades-high inflation and historic interest rate hikes, consumers are feeling the heat. Most workers reported that any salary gains they’ve received in the last year have been outpaced by inflation. We’re really seeing this hit young people hard. Half of Gen Z and Millennials are living paycheck to paycheck.

Many consumers don’t know what steps to take to get ahead. And with traditional digital banking channels lacking that personalized experience, they aren’t getting the advice they need. Banks and credit unions must prioritize financial education for their customers because they can’t afford to be left behind.

In today’s world, is digital literacy required in order to be financially literate?

Graham: Digital literacy is a huge challenge we’re facing in the banking industry. More than 15 million people are not digitally literate. Consumers should not have to know how to bank online to make good financial choices.

To tackle this, banks should ensure that customer experience is at the forefront of all of their technology decisions. Banking apps need to be easy to read, quick to navigate, and intuitive – even for individuals who are not digital natives. This is exactly why we work directly with users when building our technology at Finotta to make sure it is easily accessible, navigable, and understandable.

Banking tech also must go the extra mile and make it personal by providing Personalized Financial Guidance (PFG) to customers. This guides consumers through their financial journey, no matter where they are, by offering tailored advice on how to meet their financial goals.

How can we make sure technology is an enabler of financial literacy rather than an obstacle to it?

Graham: Banks have to remember that acquiring a new digital banking solution isn’t just about technology for the sake of seeming flashy or modern. A banking app can actually help with financial literacy by taking the guesswork out of what customers should do with their money.

Your banking app needs to deliver the right experience, service, or product to the customer based on their individual data. Then, it should offer users concrete suggestions, like opening a new savings account for college tuition, that help them achieve financially healthy lives. The cherry on top is offering in-app rewards, like badges and milestones, that recognize customers for their positive choices and make financial literacy fun.

How does personalization in digital banking help foster financial literacy? How can fintechs help digital banking customers turn insights into action?

Graham: Consumers are looking for financial guidance beyond typical personal financial management tools, which do nothing more than provide fancy pie charts that show a customer’s spending.

From a consumer’s perspective, getting alerts in their banking app that tell them how much money they spent at Starbucks over the last month (when that money could have gone towards a 401K instead) does nothing more than shame them. It’s essentially saying, “Hey, you’re in a hole.”

Instead, banks can take consumer data one step further by helping them take actionable steps to reach their goals – like setting up monthly direct deposits to save towards retirement. A bank using a personalized approach can say, “Hey, we see you’re in a hole, and here’s how you can get out.”

Finotta made its Finovate debut last year at FinovateFall. What was that experience like?

Graham: Debuting our technology last year at FinovateFall was incredible. It gave us an opportunity to tell the story of how powerful and impactful our platform is in a room of our customers and peers.

What can we look forward to hearing about from Finotta in the coming months?

Graham: The next few months for us are going to be about scaling with more and more customers. It’s been a journey building our software and now we are focused on replicating our successes with as many financial institutions as possible.

We see founders from across all fintech sectors at every Finovate event, and FinovateEurope 2023 was no different. At last month’s event, we gave five fintech founders a microphone to answer five questions.

In the four-minute video below, you’ll hear from Katalin Kauzli, Co-Founder and Business Development Director of Partner Hub; Gonzalo de la Peña, Founder and Chief Business Development Officer at Openfinance; Alexander Lempka, Co-Founder and CEO at Connect Earth; Elizabeth Rossiello, CEO at AZA Finance; and Anandhi Dhukaram, CEO and Founder at Esdha.

Each of these experts talks about their struggles, advice for running a company, what they wish they knew sooner, and who they could not operate without.

Tyfone is also announcing that it has merged with digital banking provider Cubus Solutions. The two companies will move forward under the Tyfone brand. The investment and merger are designed to help accelerate the adoption of Tyfone’s nFinia digital banking platform. The addition of Cubus’ customers, digital solutions, and expertise will help the combined entity better serve financial institutions, helping them boost revenues and efficiency.

“Today success in digital banking – in fact, success in any financial technology – is all about engaged digital experiences and the ability to scale,” Tyfone CEO Dr. Siva Narendra said. “That means scaling up to power digital growth for larger institutions and scaling down to facilitate the smaller ones (to) stay relevant.”

Cubus CEO John-Ashley Paul added: “It is rare to find two companies so culturally well-aligned that also complement each other technologically. Our best-of-breed loan payments, loan skips, e-statements, and rewards solutions will extend the Tyfone digital banking ecosystem, leading to tighter integration and a truly exceptional user experience.”

Tyfone demoed its technology at FinovateSpring in 2008. In the years since, the Portland, Oregon-based company has grown into a provider of market-leading software for credit unions and community banks. This year, Tyfone has announced partnerships with Southwest Financial, a Texas based financial institution with 9,200 members and $81 million in assets; and with Members Advantage Credit Union, a credit union based in Wisconsin Rapids with 11,000 members and $178 million in assets.

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

The Lazu Group’s CULTURL Heritage Calendar offers insights into the history and significance of holidays across many different cultures, helping companies educate and communicate in a multicultural workplace.

Features

Provides a wealth of resources designed to support internal inclusion

Includes 80 holidays, commemorations, and cultural heritage months

Offers 13 toolkits to guide organizations in the creation of diverse content

Why it’s great

The CULTURL Heritage Calendar offers ideas and resources for creating timely content and communication to promote empathy, curiosity and dialogue around the significance of cross-cultural moments.

Presenter

Malia Lazu, Founder & CEO Lazu is an award-winning, tenured strategist in diversity & inclusion who has sparked deep economic development and investment in urban entrepreneurship for more than twenty years. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

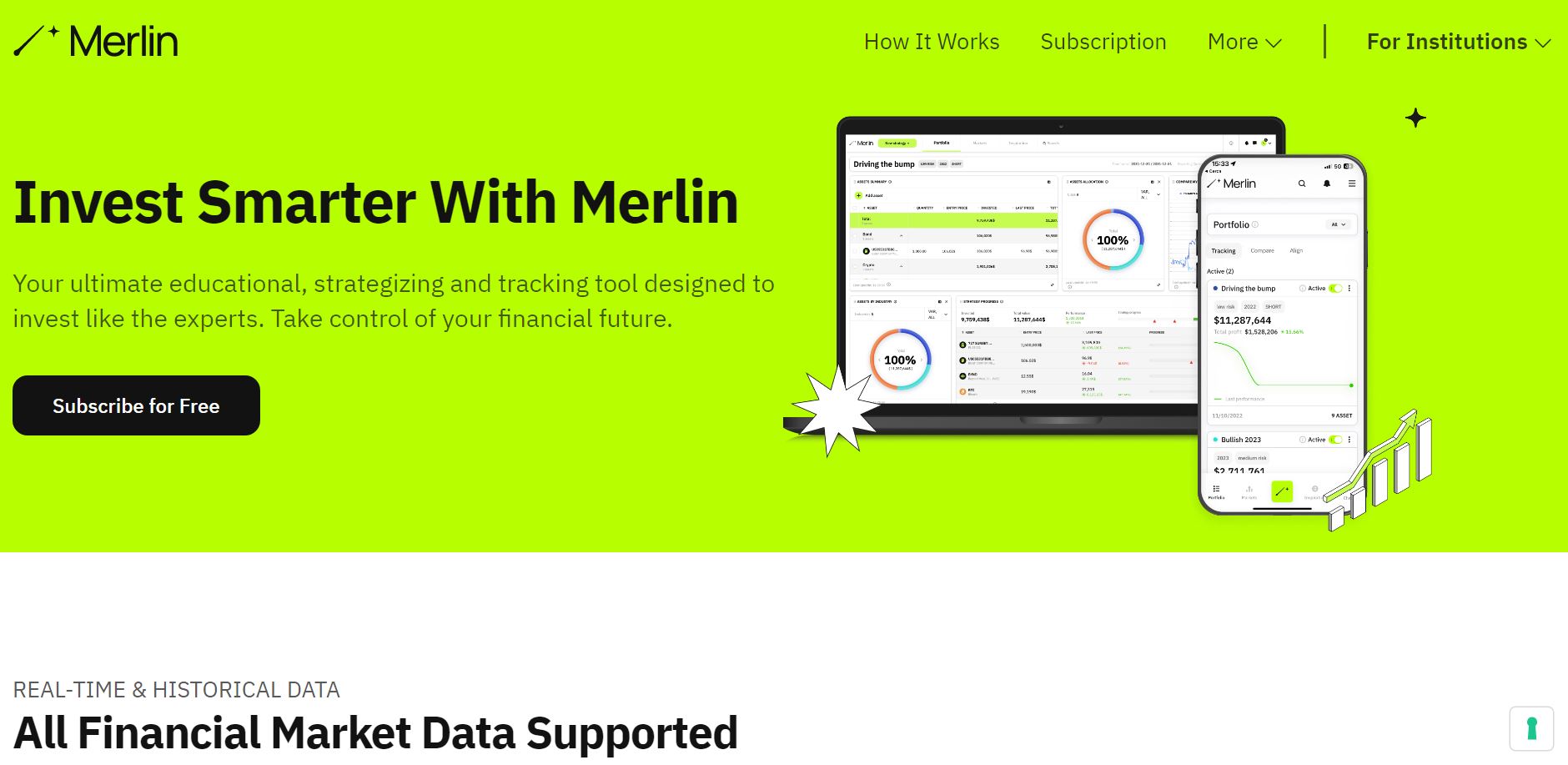

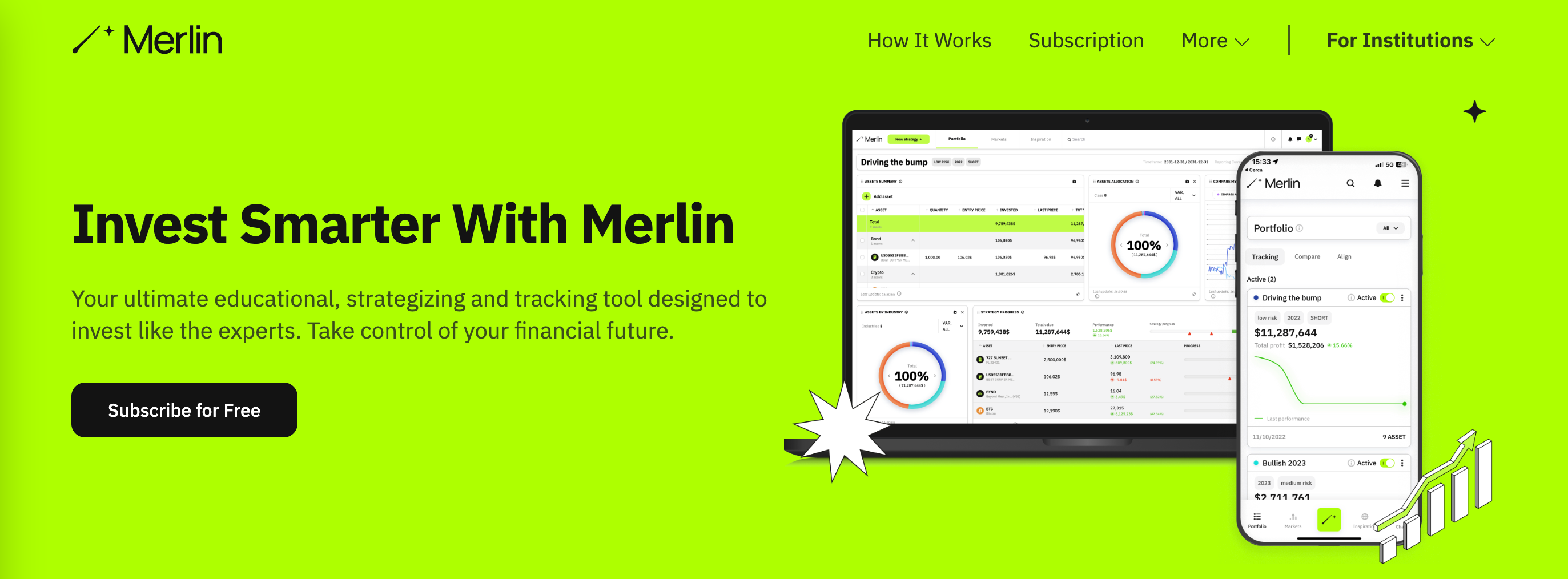

Merlin Investor offers a multi-asset educational, strategizing and tracking tool complementary to any trading platform and designed for any kind of investor.

Features

Access different market data and sentiment all in one place

Create, analyze, compare and backtest an infinite set of investment strategies

Track portfolio performance

Why it’s great

The Merlin platform allows financial institutions to attract and retain customers throughout the entire investment process and not just during the execution of trades.

Presenter

Guido Petrelli, Founder & CEO Before starting Merlin Investor, Petrelli was the CFO and COO of a multinational company operating in the automotive sector for almost 15 years. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

9Spokes unlocks the potential of open data and open banking by collecting consented data from businesses to give financial institutions a powerful set of tools to engage their business customers.

Features

Cashflow – plan, project and manage cash position

Banking – analyze spending habits and trends

Business Apps – provides a streamlined business management experience using key business apps

Why it’s great

The 9Spokes toolset makes the financial institution the center of their business customers’ daily financial lives – driving customer engagement, cross-selling and up-selling opportunities.

Presenter

Tom Baran, Head of Partnerships Baran has been a growth agent and business development leader concentrating within technology and SaaS verticals. He oversees the product-partnership ecosystem for 9Spokes. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

Prelim is a white-labeled platform that helps banks digitize business banking. With core integrations and out-of-the-box AML/BSA solutions, they power automation by connecting with any system via API.

Features

Automate business account onboarding with a few clicks

Connect to external providers, including cores, to satisfy AML/BSA/CIP requirements

Launch products and services without re-keying data

Why it’s great

Prelim offers a core integrated business account onboarding solution that allows users to launch other banking products (i.e., treasury & merchant services, lending, etc.).

Presenters

Heang Chan, Co-Founder & CEO Prior to founding Prelim, Chan was a Product Expert for Blend. LinkedIn

Sam Kim, SVP, Head of Banking Platform Before joining Prelim, Sam Kim worked for Wells Fargo Home Mortgage and Enterprise. LinkedIn

Ever since Elon Musk purchased Twitter last October for $44 million, he has been hinting of spinning the social media giant into what he is calling “X, the everything app.” In fintech, “everything apps” are known as super apps, and they exist primarily in Asia.

One of the latest developments in transitioning Twitter into a super app is Musk’s move to change Twitter’s name to X Corp. But a super app is much more than a name. Here’s a look at what the social media app currently offers, what it’s working on, and what it still needs to become a fully fledged super app.

What it has

Social Social is most certainly Twitter’s strongest attribute. The micro-blogging platform was founded in 2006 and currently has around 450 monthly active users. While this is a considerable user base, however, it pales in comparison to well-known super app WeChat, which counts 1.3 billion monthly active users.

Investment tools Earlier this month, Twitter partnered with eToro to not only offer real-time pricing data for stocks, but also to facilitate trades. The trades, however, do not take place within Twitter’s interface. Instead, users are routed to eToro’s website for stock details and to make trades.

What it’s (publicly) working on

Generative AI Last week, Musk unveiled a new company called X.AI, The move confirmed rumors of his plans to launch a generative AI product after he purchased thousands of graphic processing units. X.AI is expected to compete with OpenAI, which Musk co-founded in 2015 but left in 2018 to avoid a conflict of interest.

While most super apps do not boast their own generative AI tool, adding a powerful chatbot such as OpenAI’s ChatGPT would be a major differentiating factor

Payments Musk is publicly vociferous about his plan to add Venmo-like payments capabilities to Twitter. And it’s not just talk. Twitter filed with the Treasury Department’s Financial Crimes Enforcement Network (FinCEN) and is also in the process of obtaining necessary state licenses, as well.

After Twitter begins facilitating peer-to-peer payments, it may begin offering more digital bank-like tools such as a high-yield savings account or even an X-branded payment card. This leads the conversation into what Twitter still needs to become a super app.

What’s missing

Personal finance Twitter already offers stock trading (through a third party) and it is working on offering peer-to-peer payments. There is more to personal finance, however, than just investing and spending. In order to truly become an “everything app,” Twitter must offer brick-and-mortar payments, as well as an in-app dashboard that helps users track their spending, savings, and investments.

Shopping This may end up being one of the most challenging aspects for Twitter to add in a way that would compete with the current top super app contenders in the U.S.– Walmart and PayPal. Currently, Walmart offers consumers access to goods from an Amazon-like supplier base, as well as to goods in their local Walmart store. PayPal’s shopping experience is less compelling, but offers deals from major service providers and retailers (including Walmart).

For Twitter to start a shopping experience from scratch wouldn’t be unfathomable, but it would take a long time. If it is seeking to compete with Walmart as a super app, it will likely need to find success via a partnership.

Transportation A few of the most well-known super apps– Grab, Gojek, and Ola– began as transportation apps. Adding transportation capabilities has the potential to draw users into the app on a daily basis because they not only facilitate commutes via ride-hailing or public transportation payments, they also facilitate hyper-local delivery, grocery delivery, and restaurant delivery. These aspects play major roles in the lives of consumers.

Health services Amazon, Walmart, and others have tackled the fragmented healthcare industry. Providing affordable health services, such as appointment booking, tele-health calls, records management, and ask-a-nurse services in a single place provides a lot of value for end users.

Health services will not be a primary driver bringing users into Twitter’s super app, but it will certainly help to keep them around and may even help target the app’s older users.

Insurance Similar to adding health services, insurance tools will not serve as a primary draw for users. However, offering tools such as a digital lock box with insurance cards, contact information, coverage options, and payment history is a valuable add-on and can help reach older users not necessarily seeking social or payment capabilities.

Government and public services To become a well-rounded super app, Twitter should add government and public services, such as public transportation payment and tracking, library cards, and tax preparation services. In the U.S. however, with the advent of FedNow and the potential addition of a CBDC, the government may end up beating Twitter to the punch with a super app of its own.