Looking back at 2003, we selected 10 industry

developments that provide the best glimpse at the future of online financial

services delivery.

Innovation of the Year

Premium Online Banking: Money HQ from Online Resources

Money HQ from Online Resources earns 2003’s Innovation

of the Year and number 15 on our all-time list for its innovative

packaging of several advanced features into a fee-based premium service. The

new service, powered by CashEdge, combines account aggregation and

interbank payment services. It’s accessed via a tab (far-right) on Online

Resources Internet banking platform (see screenshot below left).

The premium service offering is optional for client financial

institutions, but with zero out-of-pocket costs, the company expects

widespread adoption. Currently, 40 out of 500 clients are live with the

service, including First Command Bank (Fort Worth, TX) and

Pinnacle Federal Credit Union (Edison, NJ).

Suggested retail price is $5/mo plus transaction fees for certain A2A

transfers. Revenues are shared between the financial institution and Online

Resources.

Two

Phishing undermines trust (for now)

Not coincidently, just when mainstream users were beginning to trust

online financial services, along comes the mass phisher, spamming the world

with hundreds of millions of fraudulent emails purporting to be from the

user’s bank, credit card company, or ISP. Unfortunately, the problem is

going to get worse before it gets better. Anti-phishing.org, a

non-profit bankrolled by Tumbleweed Communications, identified 60

unique phishing attacks in the two weeks before Christmas, which unleashed

an estimated 60 million fraudulent messages. Not until an authentication

protocol is widely adopted (hopefully, by early to mid-2005) will the

onslaught of fraudulent emails slow.

|

A recent phishing attempt aimed at Bank One went out under |

The media is beginning to jump on this story, with phishing mentioned

in 103 major articles during the past 30 days, compared to just 17 during

the entire first half of 2003. The resulting consumer awareness will help

keep users from being caught in the trap, but it will also lead to

significant problems in marketing new services via email, hampering

financial institutions’ efforts to turn a profit online. For a sobering view

on the subject read the Wall Street Journal Online’s Jan. 19, 2004

article, Stink in Your E-mail Box Means Big Trouble for Marketers.

Long-term, as techniques such as digital signatures eliminate most casual

phishing efforts, it will be a non-issue. In fact, these scares tend to be

good for existing financial institutions whose customers are even less

likely to venture to a new provider .

Three

Banks move to boost security perceptions

After a quiet first half of the year, banks were hit with a number of

highly publicized security intrusions. First, the South Africa press had a

field day with a keylogging incident that became public knowledge in May

. Other incident in the UK and New York were also publicized, but at a far

lower level than the South Africa incident. Then beginning with two Wall

Street Journal stories this summer (July 22 and August 19) and

continuing until year-end, the endless phishing attacks garnered a

significant amount of press, nearly 500 articles in the past six months

contained the word phishing.

Banks, understanding what’s at stake, took decisive actions to reassure

online banking users and prospects. For example, within weeks of its

keylogging breach, ABSA Bank installed numerous new authentication tools to

virtually eliminate the threat. Its most visible change: an optional virtual

keypad allowing wary users to “type” in their PIN codes (see inset).

This defeats most keylogging since the hacker would have to map mouse

coordinates to determine which digits were selected. In addition, the bank

instituted a rotating secondary password requirement for users to move money

out of their accounts or change personal information.

Four

Citibank launches interbank transfers (A2A)

Five years ago (Oct. 1998), when the ill-fated CompuBank first

launched its online services, it included an innovative interbank

funds-transfer system (A2A). At the time, we expected it to become common

within a few years. But other than the Internet-only banks such as ING

Direct and E*TradeBank, the service has not caught on in the

United States. In fact, no major U.S. bank offered it until the fall of 2003

when Citibank added interbank transfers to its online banking

program. CashEdge, which also powers Money HQ from Online

Resources operates the transfer system behind the scenes.

Citibank, which for several years has boasted a top-rated online banking

service based on ranking

by Gomez, Forbes www.forbes.com/bow

and others, may earn a new round of kudos by being an industry leader in

A2A. Just this week Forbes bestowed its Best of the Web on Citibank

once again (see Table 15, right), specifically mentioning the A2A

functionality.

Table 15

Forbes Favorites: Personal Finance & Investing

|

Category |

Best of the Web |

| 401k Advice | MPower Cafe |

| Auto Insurance | InsWeb |

| Banking | Citibank.com |

| Brokers | Charles Schwab |

| Calculators | FinanCenter |

| Credit Cards & Loans | Bankrate.com |

| Debt Management | About.com Credit/Debt Mgmt. |

| Estate Planning | Nolo.com |

| Financial Planning | Financial Engines |

| Financial Portal | MSN Money |

| Full Service Broker | JP Morgan Online |

| Fund Families | Vanguard Group |

| Fund Selection | Morningstar |

| Life Insurance | Quotesmith.com |

| Mortgages | Quicken Loans |

| Tax Planning | Internal Revenue Service |

Source: Forbes, 1/04

Five

Press turns positive online banking and other online

financial activities

A year ago, much of the mass media was negative or neutral on the overall

benefits of online banking. Reporters were still looking for examples of

dot-com excesses and often invoked the names of Wingspan,

CompuBank, and Citi f/i as examples of online banking’s failed

promise. Never mind that the service was growing faster than ever in terms

of net new households. During 2003, the negative reporting gradually gave

way to new stories about convenience, ease-of-use, and good value

(especially with the elimination of bill pay fees). In 2004, we expect a

mini-backlash as the press focuses on the phishing threat, but overall we

expect the media to embrace online banking for years to come.

Six

Bank of America hits seven million users

|

On its homepage, BofA is currently promoting free bill |

At year-end, Bank of America had as many online banking customers as

all U.S. banks combined had five years ago (at year-end 1998). The bank’s 7

million active users account for 43% of its checking account base, and 22%

of all households. Year-over-year growth was an impressive 50%, with 2.3

million new active users. Total enrollment, active and inactive, is now 10

million. Bill payment growth was even stronger, spurred in part by its

high-profile campaign touting free bill payment which began in mid-2002 and

continued through 2003 (see inset). More than 1.2 million new bill

pay users came on board in 2003, a 67% increase, ending the year at more

than 3 million, the largest bill payment base in the country.

Table 16

BofA Online Banking & Bill-Pay Users Trend

active users (past 90 days)

|

|

Online Banking |

Bill Payment |

|

|

Date Reported |

Num |

% OB |

|

| Dec. 18, 2003 |

7.0 mil |

3.0 mil |

43% |

| Oct. 21, 2003 |

6.6 mil |

2.8 mil |

42% |

| Sep 22, 2003 |

6.2 mil |

2.6 mil |

42% |

| Aug. 26, 2003 |

6.0 mil |

2.6 mil |

43% |

| July 24, 2003 |

5.7 mil |

2.4 mil |

42% |

| June 19, 2003 |

5.5 mil |

2.3 mil |

42% |

| Mar 25, 2003 |

5.0 mil |

2.0 mil |

40% |

| Jan. 1, 2003 |

4.7 mil |

1.8 mil |

38% |

| Nov. 27, 2002 |

4.4 mil |

1.5 mil |

34% |

| Oct. 30, 2002 |

4.3 mil |

1.5 mil |

35% |

| Aug. 2002 |

4.2 mil |

ina |

— |

| May 9, 2002 |

3.3 mil |

1.1 mil |

33% |

| March 2002 |

3.1 mil |

900,000 |

29% |

| Dec 2001 |

2.9 mil |

ina |

— |

| Dec. 2000 |

1.8 mil |

ina |

— |

| 3-year growth |

5.2 mil |

|

|

Source: Bank of America, 2001-2003

DDA = demand deposit account (checking)

Table 17

BofA Online Banking & Bill-Pay Metrics

November 2003

| Website Traffic | Value | |

|

Unique visitors per month* |

8.9 million | |

|

Number of visits per month* |

71.0 million | |

| Online Banking | ||

|

Total subscribers |

9.9 million | |

|

Active subscribers (past 90 days) |

7.0 million | |

|

Inactive subscribers |

2.9 million | |

|

Active subscribers, % of all HHs |

22.1% | |

|

Active subscribers, % of DDA HHs |

43.0% | |

|

Subscribers added monthly* |

441,000 | |

|

% BofA associates actively using |

81.5% | |

| Online Bill Pay | ||

|

Active bill payers |

3.1 million | |

|

Bills paid per month* |

16.1 million | |

|

$$ processed per month* |

$4.5 billion | |

|

eBills delivered per month |

2,360,000 | |

|

eBillers |

300 | |

| Online bill pay customers have: | ||

| 80% lower attrition rate | ||

| 30% fewer calls to call centers | ||

| 38% higher deposit balances | ||

| 45% higher loan balances | ||

Source: Bank of America, 11/03

*average monthly rate past 3 months

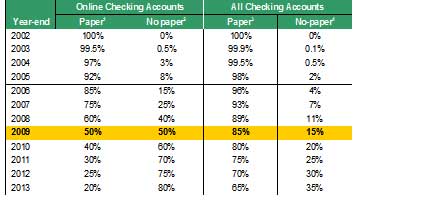

Seven

The decline of paper statements begins

Although it will take the better part of the decade before even 50% of

online banking customers turn off their paper statements, 2003 marked the

beginning of the inevitable decline in paper statements.

Table 18

Market Share: Paper Statements vs. Electronic Statements

U.S. checking/share draft accounts

Source: Online Banking Report estimates, +/- 50%

1Percent of all online-enabled demand deposit

accounts (DDA) receiving monthly paper statements, can also be receiving an

electronic statement

2Percent of all online-enabled DDAs with

no paper statement

3Percent of all DDAs receiving a monthly paper statement, can

also be receiving an electronic statement

4Percent of all DDAs with no paper statement

Eight

Banks redesign websites for Yahoo-like clarity

Each year since the industry got through its Y2K headaches, bank websites

have made dramatic usability improvements. Last year, the most notable

redesign was at Web-banking pioneer Wells Fargo. Every financial

institution should show similar restraint in limiting homepage promotions

and extraneous text. National City and Wachovia also

introduced similar-looking homepage styles.

Nine

Real-time credit for remote deposits

E*TradeBank and Pennsylvania State Employees Credit Union

both earned OBR Best of the Web awards with creative solutions to the

remote banking bugaboo, delays and uncertainties in deposit posting. PSECU

was especially innovative, earning the 23rd spot on our list of all-time

online banking innovations by providing immediate credit for deposits being

mailed to the CU. Not only is it a great online banking benefit, it has

saves the CU more than $100,000 in interchange costs. Pentagon Federal

Credit Union launched a similar service in October, dubbed Trust In

You.

Ten

Identity Theft 911 provides a credible source to fight

ID theft

Identity theft was raised from an obscure crime to dinner conversation in

late summer when the FTC released survey results indicating that everyone in

America has assumed the identity of someone else, or so it seems if you read

all the press accounts. Actually, the FTC reported that 10 million U.S.

adults (5% of the total) fell victim to identity theft (including credit

card theft) during the past five years, far higher than anyone suspected.

Even if you discount the results due to survey methodology, identity theft

claims more than one million victims a year, a huge problem.

Luckily, the private sector stepped up to the table with consumer

protection services. Identity Theft 911 appears to be an early leader,

offering insurance, victim resolution services, credit report monitoring,

and educational material. The company markets directly to consumers, but its

business model revolves around wholesaling services to banks and corporate

employee-assistance centers.