This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Two weeks ago, 63 companies took the stage at FinovateFall 2025 to demonstrate their newest offerings live in front of our audience. Whether or not you were in attendance, you can now watch all of the seven-minute demo videos for free online. That’s more than seven and a half hours of fintech content, available for free.

Don’t know where to start? We’ve highlighted the six Best of Show-winning demos below to get you started.

If you don’t want to miss out on the live action next time around, be sure to register for FinovateEurope, taking place February 10 through 11 at the O2 Intercontinental in London.

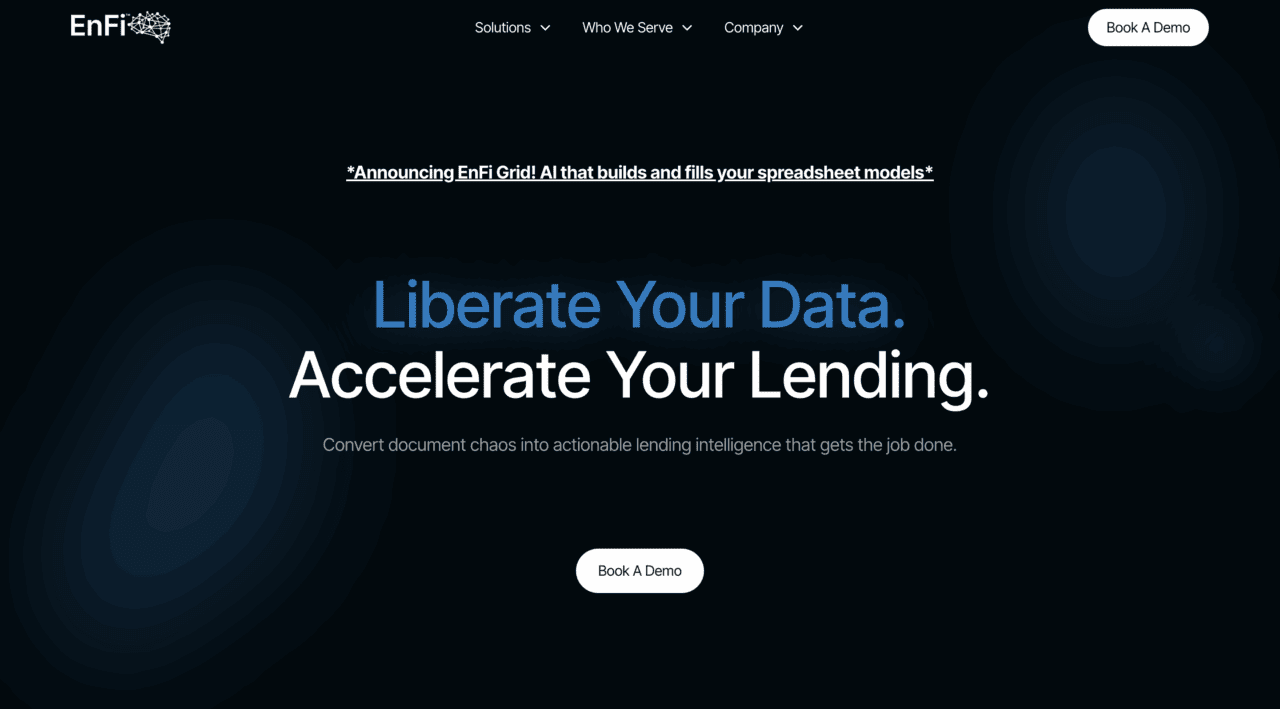

Lending platform EnFi has introduced EnFi Grid, its new AI-powered spreadsheet intelligence for lending solution.

The new offering brings full, AI-powered, spreadsheet functionality directly into the EnFi platform.

Headquartered in Boston, Massachusetts, and founded in 2024, EnFi made its Finovate debut at FinovateFall 2025.

AI-native lending platform EnFihas launched its new AI-powered spreadsheet intelligence for lending solution, EnFi Grid. The company, which offers technology that automates commercial credit workflows for financial institutions and private lenders, reports that the new offering brings full spreadsheet functionality directly into the EnFi platform, assisted with AI.

“This is a major launch for Team EnFi,” the company noted on its LinkedIn page. “EnFi Grid lets commercial lenders work in the familiar spreadsheet interface and models they know and love while taking advantage of the power of EnFi’s purpose-built commercial lending AI to add a layer of intelligence and scale to their efforts.”

EnFi Grid enables users to upload existing spreadsheets or start from scratch from within the platform. Users can build custom financial models, stress tests, and projects, as well as collaborate with AI to complete scoring models and trackers. EnFi Grid has a complete range of spreadsheet features including formulas, charts, pivot tables, editing, and more. Lenders can use the technology, for example, to complete a credit scorecard with a borrower’s most recent financial data, or to build a cash flow projection for a given construction project.

“At times like this—quarter end—where the crush of production goals collides with reporting requirements in a sea of cells, imagine being able to deploy an army of EnFi Grid Agents to ingest, analyze, and update your spreadsheets in minutes,” the company wrote.

Founded in 2024, EnFi made its Finovate debut at FinovateFall 2025 in New York. At the conference, the Boston, Massachusetts-based fintech introduced its suite of agentic AI agents for data ingestion/extraction, automated spreading, and relationship management. The company also demoed orchestrations that combined agents into bigger automated workflows for deal screening, underwriting, and portfolio monitoring. Finally, EnFi showed how the platform can be tuned to provide customer-specific workflows for a variety of commercial credit types including CRE, C&I, SBA, and venture.

Named a “Startup to Watch in 2025” by the Boston Business Journal, EnFi began this year adding to its C-suite. The company hired its first chief revenue officer, Chris Aronis, a fintech executive with more than 20 years of experience, in January. Aronis has held leadership roles at Fiserv, Quovo, and Bottomline, and was chief revenue officer of business banking and lending for Numerated.

EnFi was co-founded by Joshua Summers (CEO), Scott Weller (CTO), and Michelle Hipwood (CFO). According to Crunchbase, the company has raised $7.5 million in funding courtesy of a June 2024 seed round led by Unusual Ventures.

Paytech ACI Worldwide announced that Berlin-based embedded finance platform Solaris SE will consolidate all SEPA payments onto ACI Worldwide’s ACI Connetic payment hub.

Unveiled earlier this year, ACI Connetic is a unified solution that integrates account-to-account (A2A) payments, card processing, and fraud prevention within a single, cloud-native architecture.

Founded in 1975, ACI Worldwide has been a Finovate alum since 2011.

Just months after launching its centralized payment hub, ACI Connetic, ACI Worldwide has announced that European embedded finance platform, Solaris SE, will consolidate all SEPA payments onto ACI’s cloud-native payments solution.

“ACI Connetic represents a significant step-change in our commitment to supporting financial institutions as they navigate the complexities of the global payments landscape,” ACI Worldwide CEO and President Tom Warsop said. “In an environment of increasing payments complexity and regulatory demands, ACI Connetic delivers the agility, resilience, and innovation required to drive digital transformations, sustainable growth, and long-term success.”

ACI Connetic is a unified solution that integrates account-to-account (A2A) payments, card processing, and AI-powered fraud prevention within a single, modular, cloud-native architecture. ACI Connetic helps financial institutions simplify their operations, innovate faster, and meet emerging regulatory and compliance requirements with greater agility and less cost.

Solaris SE joins a number of financial services companies around the world—including leading clearing and settlement systems—that are integrating their payment capabilities into ACI Connetic. These early adopters include the Bank of England, Swift, the US Federal Reserve, and The Clearing House. The company’s partnership announcement with ACI Worldwide comes at a time when the benefits of centralized payment processing are becoming more apparent to both financial services analysts and financial institutions.

“Migrating our instant payments capabilities to ACI Connetic marks a key milestone in Solaris’ digital transformation and growth journey,” Solaris SE CEO Carsten Höltkemeyer said. “It future-proofs our payments infrastructure, accelerates service innovation, and enhances the value we deliver to partners and their customers across Europe.”

Based in Berlin, Germany, Solaris SE was originally established as a part of incubator and accelerator, Finleap. As Solarisbank, the company secured its German banking license in 2016. The company rebranded to Solaris in 2022, a move which coincided with the firm changing its legal status from a German AG (Aktiengesellschaft) to an SE (Societas Europea or European company). Today, Solaris SE offers a Banking-as-a-Service (BaaS) platform that enables businesses—from SMEs to multinational corporations—to embed a wide range of financial solutions from digital banking and payments to cards and lending.

A Finovate alum since 2011 and an alum of our developers conference FinDEVr Silicon Valley, ACI Worldwide offers solutions that power intelligent, real-time, payments orchestration to enable banks, billers, and merchants to deploy modern payment technologies seamlessly and securely. The company serves the top 10 banks worldwide; enables more than 80,000 merchants directly and via PSPs; and provides thousands of businesses and organizations with billpay solutions. Founded in 1975, ACI Worldwide now processes 25 billion cloud transactions and more than 225 billion consumer transactions annually. The company is headquartered in Elkhorn, Nebraska.

Swift is launching a blockchain-based shared ledger with Consensys to enable instant, always-on cross-border transactions.

Swift is leveraging its 50 years of experience providing global financial messaging to offer the same standardization and trust for tokenized assets as it has for payment instructions.

The ledger will emphasize trust and compliance while being interoperable by working with both public and private networks.

Swiftannounced this week that it is launching its own blockchain in partnership with blockchain software company Consensys.

Swift’s new blockchain-based shared ledger will facilitate instant, always-on cross-border transactions. Today’s announcement comes after Swift prototyped the blockchain with more than 30 financial institutions across the globe. The experience with those firms is helping Swift design and build the ledger, which is starting with a prototype powered by Consensys.

This move builds directly on Swift’s five-decade history as the backbone of cross-border financial messaging. Since it was founded in 1973, Swift has grown from a consortium of 239 banks in 15 countries into what it is today: a global standard for secure interbank communication that connects more than 11,000 institutions worldwide.

Just as Swift’s original network created a common language for banks to exchange payment instructions, its new ledger is designed to provide standardization and trust for tokenized assets. Swift anticipates that its new ledger will expand its focus on infrastructure. The member-owned cooperative plans to work with banks on leveraging the ledger infrastructure.

The launch also reflects rising demand for always-on settlement, interoperability between blockchains and fiat rails, and the need for a trusted global standard in digital finance. “We provide powerful and effective rails today and are moving at a rapid pace with our community to create the infrastructure stack of the future,” said Swift CEO Javier Pérez-Tasso. “Through this initial ledger concept we are paving the way for financial institutions to take the payments experience to the next level with Swift’s proven and trusted platform at the centre of the industry’s digital transformation.”

The new ledger will work with existing and emerging networks to record a secure, real-time log of transactions that take place among financial institutions. Swift will place a great emphasis on trust and compliance, leveraging its long-standing reputation. It will also ensure interoperability between distributed ledger transfers and existing fiat rails, by orchestrating between different systems and supporting both private and public networks.

“As digital assets continue to develop and mature at pace, Swift’s blockchain-based ledger provides the foundational infrastructure needed for trusted, real-time cross-border payments alongside existing ways of moving money,” said NatWest Head of Group Payment and Digital Asset Strategy Lee McNabb. “By partnering in this initiative, we are shaping solutions that allow our clients benefit from greater speed, transparency and crucially, flexibility in the digital age—without wavering on robust compliance and risk management.”

Swift’s ledger is not just an evolution of the company. It is also an example of how the wider industry is changing along with technology. In this case, the same rails that have carried payment messages for 50 years may soon carry records for tokenized funds, as well.

The rebound in fintech funding that we’ve been looking for over the past few weeks earned further confirmation today after our review of the funding totals for companies that have demoed on the Finovate stage.

Nine alums have raised more than $566 million in the third quarter of 2025. This figure is the highest funding total for alums in a Q3 since 2022. In fact, given that the amounts of the investments in two instances this quarter (the fundraisings by AKUVO and Argyle) were not disclosed, it is likely that this year’s Q3 total is more than double the amount raised in the third quarter of 2023.

Previous quarterly comparisons

Q3 2024: More than $16 million raised by six alums

Q3 2023: More than $293 million raised by eight alums

Q3 2022: More than $1 billion raised by eight alums

Q3 2021: More than $1.1 billion raised by 14 alums

While this quarter’s tally falls short of the billion-plus we’ve seen in many third quarters in the past (2022-2019, 2017, and 2015 for example), the sizable figure is still a hopeful sign heading into the final quarter of the year that fintech funding is on the way back.

Top equity investments

The top equity investment for Finovate alums in Q3 2025 was far and away the $300 million announced by Quavo Fraud & Disputes in July. In fact, Quavo’s fundraising total represents more than half of the total quarterly funding for alums in Q3 2025.

Quavo’s growth equity investment came from Spectrum Equity and empowered the company, in the words of Co-Founder and CEO Joseph McLean, to “accelerate our AI-led product development initiatives and expand our go-to-market and client success teams to meet growing market demand.” The investment took the company’s total capital raised to $311 million, according to Crunchbase.

Founded in 2016 and headquartered in Wilmington, Delaware, Quavo provides fraud and dispute management solutions to companies ranging from global issuers and fintechs to regional banks and credit unions. The company most recently demoed its technology at FinovateFall 2025.

Here is our detailed alum funding report for Q3 2025.

If you are a Finovate alum that raised money in the third quarter of 2025, and do not see your company listed, please drop us a note at [email protected]. We would love to share the good news! Funding received prior to becoming an alum not included.

Tomorrow is the final day of the third quarter of 2025, which means that Wednesday marks our entrance into October. Historically, fall has been the busiest season for fintech announcements, so we’re ready to keep up with all of the new developments. Here is some of the biggest news from this week so far. We’ll continue adding news to this post throughout the week, so stay tuned!

BaaS and embedded finance

Worldpaylaunches embedded lending, banking and card issuing for platforms partners.

Payments

Citi and Dandelion collaborate to transform cross-border payments and enable near-instant payments into digital wallets across the globe.

Swift to add blockchain-based ledger to its infrastructure stack.

Bolt launched its all-in-one SuperApp, combining digital banking, crypto trading, ecommerce, and peer-to-peer transfers in a single platform.

The company has partnered with Midland States Bank and Zero Hash for FDIC-insured banking services and crypto infrastructure under one roof.

The app has added agentic AI and dual-rail transactions give users seamless fiat and crypto payments, personalized shopping, and integrated rewards.

Identity and ecommerce fintech Boltlaunched its all-in-one app to bridge the gap between traditional finance (TradFi) and decentralized finance (DeFi). The new app offers users a singular way to shop, spend, save, earn, and invest.

Bolt is calling the app its SuperApp because it provides crypto trading, peer-to-peer transfers, digital banking capabilities, and ecommerce, with Midland States Bank providing FDIC-insured banking services and Zero Hash powering crypto custody and trading infrastructure.

“The future of money and commerce isn’t siloed—it’s seamless,” said Bolt Founder and CEO Ryan Breslow. “Today’s consumer shouldn’t have to juggle multiple apps for fiat, crypto, rewards, or shopping. Our SuperApp brings it all together in one secure, intuitive platform. By building rewards, banking and commerce directly into a single app, we’re creating not just another wallet, but a financial operating system for the modern consumer. Bolt is delivering the infrastructure to make this future real, scalable, and accessible to everyone.”

The app, which is launching out of beta today, offers a virtual and physical debit card with the ability to lock and unlock the card using the app. Users automatically earn rewards, including personalized rewards boosts that let users optimize earnings across everyday spending categories like restaurants, travel, groceries, transit, and fuel.

Crucially, in addition to debit and credit functionality, the app offers dual-rail transaction support for both fiat and crypto, including Bitcoin, Ethereum, Polygon, Solana, USDC, and more. Additionally, Bolt’s crypto trading is available on more than 40 major cryptocurrencies.

Bolt is leveraging agentic AI by introducing an AI agent that helps users search, compare, and products products based on personalized preferences, intent, and constraints. The new app offers integrated shopping and spending that brings commerce, payments, and tracking in a single experience.

Bolt was founded in 2014 and is headquartered in San Francisco, California. The company offers both retail and commercial payment tools, such as conversion and loyalty solutions for retailers and one-click checkout for more than 80 million shoppers.

The challenge of modernization remains a daunting one for many community banks and credit unions. Faced with the expense and risk of a “rip and replace” strategy on the one hand and a seemingly endless series of quick fixes, workarounds, and complex third-party relationships on the other, some financial institutions remain in a limbo of inaction.

To this end, the latest innovations from banking technology platform company Nymbus are a welcome development. In our interview with Nymbus CEO Jeffery Kendall, shared here, we talk about the current state of core banking systems, the innovative “sidecar” approach to core modernization that Nymbus offers, and the transition toward vertical banking which helps community financial institutions deliver differentiated solutions to a wider range of customers and members.

“We are a United States-focused banking technology platform. We work with community banks and credit unions (that) tend to be in the one to ten billion asset size; those are the customers we are able to help the most. We provide a full banking stack that allows them to run their core processing, their digital banking experiences, onboarding experiences … from one unified platform.”

Chairman and CEO of Nymbus since 2020, Jeffery Kendall has more than 20 years of experience in technology and financial services. He succeeded Scott Killoh, who founded the company in 2015. With Kendall as CEO, Nymbus has secured more than $123 million in funding courtesy of Series C and D rounds in 2021 and 2023, respectively. The company launched a Credit Union Service Organization (CUSO) in 2021, and has forged partnerships with financial institutions like PeoplesBank, VyStar Credit Union, and MSU Federal Credit Union.

A leading provider of banking technology solutions for financial institutions, Nymbus offers a full-stack banking platform for US banks and credit unions that helps them accelerate their growth and enhance their market positioning. The company modernizes legacy core systems for both brick-and-mortar and digital-first institutions. Nymbus also supports vertical banking strategies and the launch of subsidiary brands with a sidecar core alternative. The company is headquartered in Jacksonville, Florida.

Klarna’s debit card hit one million US sign-ups in just 11 weeks, reflecting strong consumer demand for flexible, seamless payment experiences.

The card’s growth highlights the success of Klarna’s integrated model that combines commerce, payments, and banking features.

Banks and fintechs should take note of Klarna’s playbook to meet customer expectations of unified ecosystems, modernized infrastructure, and agility.

BNPL leader Klarnarevealed today that its debit card reached one million US sign-ups in just 11 weeks. The news from Klarna is certainly a testament to the company itself, which has freshly gone public. The growth also sends deeper signals about evolving consumer behavior, fintech product strategy, and what banks should do to stay relevant.

As a recap, Klarna launched its debit card in the US on July 4 of this year. The fintech is seeing 13,000 new US users sign up for debit cards each day, reaching a peak of 50,000 sign-ups on September 23. The card, which is aimed at consumers seeking a wider variety of payment options and timing, is different from other fintech debit cards on the market, as it adds BNPL flexibility to help shoppers pay on their own terms, wherever they shop.

“The amazing response to our card in the US shows just how strong the demand is for a fairer, more transparent way to pay,” said Klarna CMO David Sandström. “With the Klarna Card, consumers get the best of both worlds: the simplicity of a debit card with the flexibility of credit.”

What Klarna is doing right

There’s no denying that these numbers are staggering. They also highlight key aspects about Klarna.

First, the numbers reflect an increase in demand for seamless payments experiences. With its single card able to offer a variety of payment options, Klarna’s debit card provides a single wallet experience with integrated financial tools rather than multiple, disjointed products. The rapid increase in cardholders suggests users prefer an integrated payment experience that offers multiple payment options.

The data is also an indication of how Klarna has achieved an optimal trifecta in the fintech world. The company already combines commerce, payments, and banking features, and its debit card extends the reach of each of these elements even further.

Crucially, reaching one million debit cardholders in 11 weeks requires KYC, underwriting, fraud prevention, compliance, and scaling techniques that all work in unison. Klarna has been able to balance each of these elements, proving that its critical infrastructure is able to stand up under stress.

What banks can learn

Given each of these elements contributing to Klarna’s success, it’s worth taking a deeper look at what banks and fintechs can learn from this growth.

First, they should take a look at their own ecosystem to ensure their cards, deposits, credit, and payments products work together in an integrated manner, and do not exist in isolated silos. They should also seek to modernize their underwriting, fraud, and decisioning engines to support their onboarding flows. Banks should also work to prioritize agility, product iteration, and scaling infrastructure. For firms seeking to grow, infrastructure upgrades are no longer optional.

Risks and caveats

While we can look to Klarna as an example of growth, it’s important to keep in mind that there are a few hidden factors to consider. The fintech’s rapid growth does not necessarily guarantee that its operations are profitable. Orchestrating interchange revenue, default risk, and customer acquisition costs is tricky, and the debit card issuance numbers don’t offer a full picture of profit. Additionally, as issuance numbers like these increase, so will regulatory scrutiny. Because of this, compliance overhead for consumer protection and disclosures may worsen as scale increases.

When it comes down to it, Klarna’s milestone shows that consumers want flexible, unified payments. It is a warning signal to banks that hesitate moving forward to modernize and integrate their product stack. Slow-moving players risk being reduced to back-end utilities.

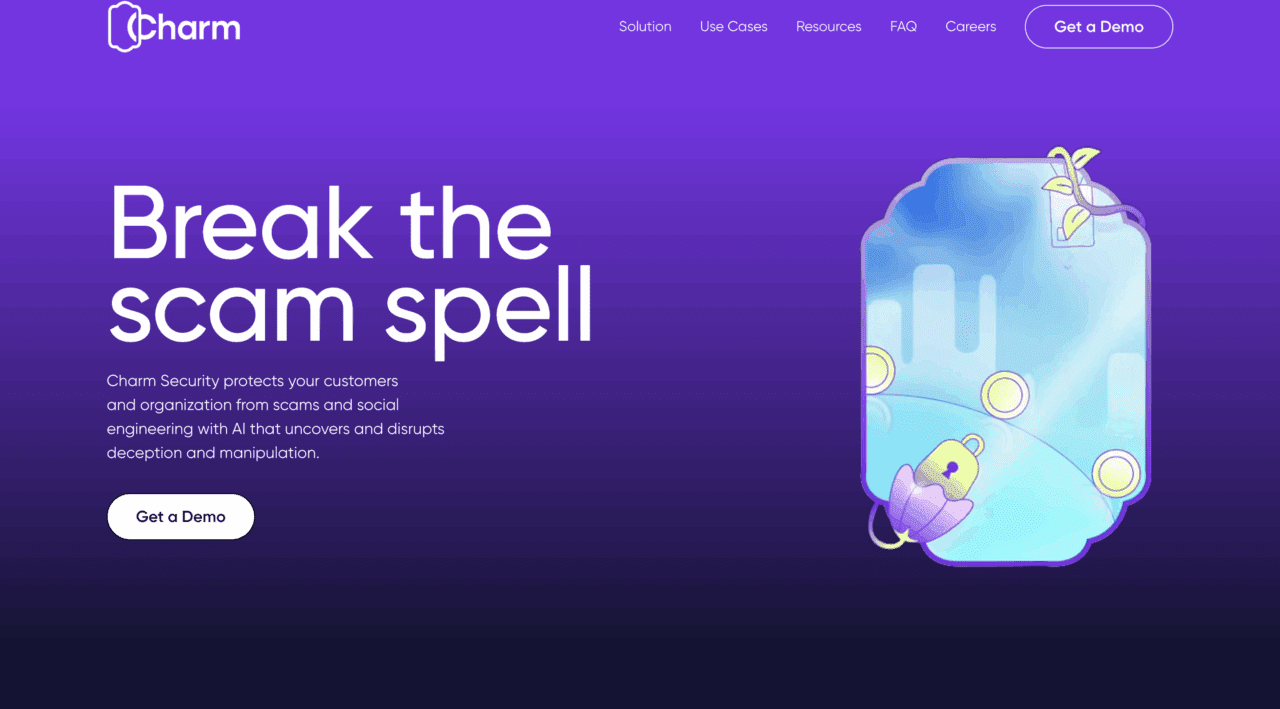

AI-powered scam defense platform Charm Security has forged a strategic partnership with no-cost mental health service provider Give an Hour.

Charm Security will embed the experiences of scam victims as well as those of mental health professionals directly into its AI model training to help “break the scam spell” before losses—financial and emotional—accumulate.

Headquartered in New York and founded in 2024, Charm Security made its Finovate debut at FinovateFall 2025.

Charm Security, an AI-powered scam defense platform for financial institutions, recently announced a strategic partnership with Give an Hour, a nationwide non-profit that provides access to no-cost mental health services. Courtesy of the partnership, Charm Security will embed the experiences of scam victims and their families, as well as clinicians and psychologists, directly into its AI model training. This integration will fortify Charm Security’s Human Vulnerabilities, Exposures, and Exploits model (HVE) and power real-time interventions that, in Charm Security’s parlance, “break the scam spell” before financial or emotional losses escalate.

In their statement, the companies cited a survey from Lloyds Banking Group that indicated that 69% of fraud victims reported experiencing significant mental impacts such as anxiety, as well as less trust in online platforms. The UK Home Office has documented fraud and scam victims experiencing depression and, in some cases, even suicidal thoughts or attempts.

“Scams exploit human vulnerabilities, not just financial systems,” Charm Security Co-Founder and CEO Roy Zur said. “By embedding victim and clinician experiences and voices into our AI, we can anticipate manipulative tactics, disrupt them in real time, and ensure prevention and healing go hand in hand.”

The integration will feature feedback loops to deliver insights back to Give an Hour’s national mental health network to provide victims with both prevention and compassionate care. The partnership will enable Give an Hour to deliver training to financial institution teams to help them better recognize and respond to the concerns of their customers when they are victims of scams and fraud. This training complements Charm Security’s AI scam prevention agents and copilots, which support frontline workers with real-time tools to assist in detecting and disrupting scams as they are happening.

“For nearly two decades, Give an Hour has provided free mental health care to those in need,” Give an Hour CEO Dr. Trina Clayeux said. “By partnering with Charm, we can ensure scam victims receive both better protection from cutting-edge AI-based technology and the compassionate support they deserve from their financial institutions.”

Founded in 2005, Give an Hour leverages the skills, experience, and compassion of mental health professionals, peer support facilitators, and others to provide no-cost mental health services to those in need. To date, Give an Hour has provided more than 400,000 hours of free mental health care to military servicemen and women, veterans, families, and communities.

Headquartered in New York and founded in 2024, Charm Security made its Finovate debut earlier this month at FinovateFall 2025. At the conference, the startup demonstrated how its AI agents help users and frontline employees proactively avoid scams, actively engage with users during transactions to “break the scam spell,” and provide immediate, personalized post-scam support, including incident reporting, evidence collection, and recovery processes.

Stablecoins may have saturated headlines earlier this year, but September has marked a turning point to the industry. This month has brought four large announcements in agentic payments, demonstrating that the technology has moved from fringe to forefront.

And while the announcements speak volumes about how quickly technology developments move in fintech, it also sends seven major signals to banks and fintechs.

A preferred protocol layer emerges

Earlier this week, agentic commerce platform Circuit & Chisel landed $19.2 million to launch ATXP, a web-wide protocol. The protocol will not only position Circuit & Chisel as an orchestrator of agentic commerce, but it will also help streamline workflows and enable businesses to operate faster and more efficiently by leveraging revenue-generating autonomous agents.

The launch and growth of ATXP show the industry’s movement toward a web-wide standard for agentic payments. It also highlights how payments are shifting from app-specific functions into a common infrastructure layer.

Big Tech wants to lead

Google and PayPal made headlines last week when they announced their partnership on agentic shopping, embedded payments, payments processing, and more. The two are positioning themselves at the forefront of agentic payments and commerce and are providing developers with tools to engage in the new era of digital commerce.

The partnership between Google and PayPal shows that Big Tech wants to be at the forefront in shaping how commerce and payments flow online in the future. This early movement is a warning to players that sit back on the sidelines and wait for others to move first. Slow-moving banks and fintechs risk being relegated to backend providers unless they strategically find their own niche in the space.

Crypto and Web3 join forces with platforms

Also last week, Google announced that it is leveraging the x402 protocol within its Agent Payments Protocol (AP2) to allow AI agents to pay each other using stablecoins on Coinbase. With the ability to handle payments on behalf of their end users, agents will now be able to complete certain tasks that previously required manual oversight, such as paying for data crawls, services, or microtasks.

The launch merges crypto protocols and mainstream platforms, and is a great example of how agentic payments won’t be limited to decentralized finance environments. Instead, we’ll see agentic payments within web browsers, search, and commerce platforms.

Credit has an agentic future

After landing strategic backing from Citi Ventures earlier this month, agentic AI-powered credit data and payments platform Spinwheel plans to fuel growth, expand its agentic AI platform, build out its data sets and add new products. Additionally, Citi Ventures will advise the company on banking-specific product use cases.

This funding shows backing for the idea that consumer credit and agentic payments will be integrated in the future. It shows the breadth of potential for agents to manage payments, debt repayment, refinancing, and credit optimization.

The shift to autonomous decisioning

All four of these announcements demonstrate how payments will move from static, user-initiated tasks to autonomous, rule-driven events. To stay current, banks and fintechs will need to embed decisioning logic, risk scoring, and compliance into their payment flows.

Regulators will take notice

While regulators don’t have a lot of time (or expertise), agentic payments are sure to get their attention. These announcements around autonomous money movement have raised concerns around AML, KYC, and consumer protection issues. Firms that build compliance into agentic systems will be one step ahead in winning not only consumer trust but also regulators’ approval.

The race for standards is on

Much like open finance, the world of agentic payments will desperately need to abide by an agreed upon set of standards. Because competing protocols and ecosystems could fragment adoption, the disorganization could not only disrupt the user experience, but it could also wreak havoc on creating a clean, regulated environment. Whichever parties are involved in driving standards for payment rail interoperability will take the role that SWIFT did in shaping payments rails in the 1970s.

The ultimate question is, who will lead and who will follow?

FIS has acquired Chicago-based Amount, adding the fintech’s digital banking and lending SaaS platform to its portfolio; terms of the deal were not disclosed.

The acquisition strengthens FIS’s digital banking strategy, enabling banks, lenders, and credit unions to streamline account origination, lending, deposits, cards, and fraud prevention.

Amount brings 158 employees and a fintech growth story marked by unicorn status, layoffs, and $313 million raised.

Fintech giant FIS has finalized the acquisition of digital banking and lending SaaS platform Amount. The financial terms of the deal were undisclosed.

“After years of successful partnership, we are thrilled to welcome Amount’s talented team and innovative capabilities to FIS,” said FIS CEO and President Stephanie Ferris.

Founded in 2019 and spun out of online lending company Avant a year later, Chicago-based Amount helps banks offer unified digital banking origination and decisioning experiences across lending, cards and deposits. The company’s solution offers embedded AI functionality to simplify the online account opening experience for banks, lenders and credit unions.

FIS anticipates that adding Amount will help it strategically expand its solutions portfolio. Specifically, the Florida-based company will leverage Amount to empower financial institutions to boost efficiency, streamline lending, improve customer service, simplify account opening while reducing fraud, and optimize credit card issuance and payments. The deal will offer FIS’ bank clients the ability to provide a more unified and seamless digital account opening process for the retail and commercial clients.

“Our strategy and investments have positioned FIS to lead the next generation of banking solutions, enabling financial institutions to thrive in today’s digital-first world with confidence, innovation and reliability. The Amount platform, integrated into FIS digital, core banking and card systems, will help FIS clients grow deposits, loans and card portfolios efficiently and securely,” added Ferris.

Established in 1968 and based in Florida, FIS serves 15,000 clients across the globe. The company’s product suite includes payment solutions, risk management services, and customer communication tools. Its technology supports the processing of $50 trillion in transactions annually and oversees assets totaling $16 trillion.

“Joining forces with FIS marks an exciting new chapter for Amount,” said Amount CEO Adam Hughes. “FIS provides global scale, robust infrastructure, and regulatory expertise that will allow us to strengthen our market offering and deliver seamless, innovative customer experiences and accelerate digital transformation. Becoming part of the FIS organization will create a unique asset and the industry’s most comprehensive digital banking platform.”

Logistically, all of Amount’s 158 employees have joined FIS and the fintech will maintain its headquarters in Chicago.

Today’s agreement comes after a roller coaster ride for Amount. After it began operating independently in 2020, the fintech went on to raise $81 million with a $1 billion valuation and later acquired small business lending platform Linear for $175 million. In June 2022, however, as fintech began to slump, Amount had to cut 18% of its workforce and later that year had to lay off another quarter of its workforce. The company picked things up again last year when it raised another $30 million, bringing its total raised to $313 million. The company’s updated valuation is unknown.

FIS’s move to acquire Amount is yet another example of how established fintechs are leveraging incumbents to meet demand for secure and seamless digital experiences. As competition heats up in the US and beyond, the acquisition will ultimately help FIS strengthen its leadership in end-to-end digital banking.