This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

While Finovate is all about demoing the newest fintech, we’re also into discussing it.

At this year’s FinovateSpring conference, which will be held digitally on May 10 through May 13 in Central Standard Time, we’re hosting hours of discussions on the hottest topics in banking and fintech. Thinking of joining us? There’s still time to buy your ticket before the price increases on April 20.

Here’s a highlight of some of the topics you can expect:

Neobanks vs Traditional Banks

A look at who has the advantage and how neobanks will find a path to profitability

Embedded Finance & Banking As A Service: A Game-Changing Opportunity For Incumbents?

A discussion of how banks can leverage open finance

Fintech, ESG & Climate Change: How Financial Services Companies Can Play A Key Role Helping Clients On Their ESG & Climate Change Journeys

A look into how banks should act on the explosive ESG trend as it transcends investing into everyday finances

The ABC Of CBDCs: Why Central Bank Digital Currency Initiatives Are A Gamechanger

CBDC initiatives are moving fast. Here’s what you need to know.

Buy Now Pay Later: A Great Product For Customers Or A Debt Trap?

Experts debate the pros and cons of buy now, pay later schemes.

Seven in Seven

7 Expert Speakers Have Just 7 Minutes to Tackle Critical Issues Facing Financial Institutions & Fintechs.

Analyst All Stars

Alyson Clarke, Principal Analyst at Forrester; Daniel Latimore, Chief Research Officer at Celent; and Jacob Jegher, President of Javelin Strategy & Research discuss the top trends in fintech and banking.

Want to see more? Check out the full agenda on the FinovateSpring event page.

Alternative banking services company SoFi unveiled a new product last month that will enable eligible members to participate in upcoming IPOs.

The tool will sit within SoFi Invest, a suite of investment tools that offers automated investment services, retirement accounts, a cryptocurrency wallet, and more.

Here’s how it works- users with at least $3,000 in their Active Invest accounts can select the IPOs they’d like to participate in by submitting an indication of interest. Once the IPO is live, investors will receive a notification asking to confirm their order and secure their shares.

If you’re a fintech veteran, this concept may sound familiar. There have been a handful of companies that have opened up IPO participation for retail investors, which are generally excluded from IPOs since they don’t generate the same revenues as institutional investors or high net worth individuals.

The first fintech to offer IPO access to retail investors was Loyal3, which was founded in 2008. The company launched a social IPO platform in 2014 that partnered with pre-IPO companies to enable them to include consumers, employees, partners, and fans in their IPO. Investors were required to purchase a minimum of $100 in stock but were not charged a fee. Loyal3, however, may have been ahead of its time. The company closed its doors in 2017.

Linqto, which recently demonstrated its platform at FinovateWest 2020, allows accredited investors to invest in pre-IPO unicorns. The company requires investment minimums ranging from $5,000 to $10,000. Among the companies currently available to investors are Impossible Foods, Ripple, and Nerd Wallet.

Yet another fintech in this arena is MarketX, a cross-border marketplace that allows investors to browse deals and invest in pre-IPO companies across the globe. MarketX currently offers investors access to pre-IPO companies in the U.S., China, Singapore, Indonesia, India, the UAE, and more. While MarketX advertises to accredited retail investors, the company requires a minimum of $50,000, a figure that is much higher than others working in this space.

With higher minimums and accredited investor restrictions, the IPO investment offerings from Loyal3, Linqto, and MarketX aren’t as accessible as SoFi’s proposed IPO investment tool. Stock trading app Robinhood, however, is also rumored to be entering this space with an offering that will compete on the same level as SoFi.

Reuters reported last month that Robinhood plans to democratize IPO investing by enabling its users to buy into IPOs. According to the news source, Robinhood is allowing its users to buy into its own IPO (which is slated for later this year) and will then use the technology it built to create a more general IPO investment tool for its 13 million users.

SoFi showcased at FinDEVr New York 2017 in a presentation about leveraging bank authentication. FinDEVr will be returning to the Finovate lineup with its own stage at this year’s FinovateSpring digital event. Check out the event page to learn more.

Small business financial services platform Hatch unveiled its funding total today. The California-based company has pulled in $20 million in two funding rounds since it was founded in 2018.

The first investment, a Seed round that closed in January 2019, totaled $5 million. The company’s Series A round closed in February of last year, totaling $14 million.

Hatch’s investors include Kleiner Perkins, Foundation Capital, and SVB.

Hatch offers small businesses a line of credit and a business checking account which it launched this January. The checking accounts come with a Mastercard debit card and allow Hatch’s 4,000 business users to send money through ACH, billpay, or via digital checks from the Hatch dashboard. Additional features include overdraft protection and cashback rewards.

Because Hatch uses machine learning to complete KYC, KYB, and OFAC compliance checks, businesses can get approved for a checking account in under five minutes. Accounts cost $10 per month and feature a transparent fee structure.

Founded by Thomson Nguyen, Hatch has a team of 48 people, 40 of which were brought on in the past year during the pandemic.

Mortgagetech innovator Better.com recently landed a $500 million investment from Japan-based Softbank, bringing the company’s total funding to over $900 million.

According to the Wall Street Journal, which broke the news, Softbank is buying shares from existing Better investors, a list which includes Goldman Sachs, Citigroup, and Kleiner Perkins.

With the new round, experts estimate Better’s valuation to be around $6 billion. This is a significant jump from the company’s most recent valuation, which sat at around $4 billion after Better closed a funding round in November of last year.

Better was founded with the goal of reengineering the mortgage process. The company streamlines mortgage originations by taking the entire process online. Better also offers Better Real Estate, which matches buyers with real estate agents; Better Settlement Services, which offers title insurance; and Better Cover, a home insurance marketplace.

The new investment comes at a time of significant growth for Better. Inspired by low interest rates, more consumers have been refinancing their properties. The Wall Street Journal reports that because of this increase in demand, Better lent out $25 billion in loans in 2020 and has extended $14 billion in loans the first quarter of this year.

Better saw $800 million in revenue last year and is expected to go public by the end of 2021. Founded in 2014, the company is headquartered in New York City. Vishal Garg is CEO.

Mobile banking platform MoneyLion announced a move into the crypto realm today. The New York-based company will soon unveil tools that enable members to buy, sell, and earn digital currencies.

The new offering is expected to launch this fall.

Facilitating the new cryptocurrency capabilities is a strategic investment that MoneyLion has made in digital asset settlement provider Zero Hash. Founded in 2015, Zero Hash provides a turnkey solution that allows platforms to integrate a range of digital asset capabilities into their own user experiences.

The new cryptocurrency tools will enable users to buy and sell Bitcoin and Ethereum and earn cryptocurrencies via a rewards program and a spending roundup tool that will round up debit card purchases to the nearest dollar, investing the spare change in cryptocurrencies.

“We’re seeing exploding interest in the utility and investment potential of digital currencies, but one of the top reasons our members say they haven’t yet acquired cryptocurrencies is because they lack knowledge of the asset class,” said MoneyLion co-founder and CEO Dee Choubey. “The MoneyLion crypto offering will provide members an intuitive way to own digital currencies within a seamless and secure environment and, through our strategic investment in Zero Hash, we’re confident that we’re advancing our mission to increase access to previously exclusive financial services.”

This news comes at a time when user interest in cyrptocurrency is at an all-time high. According to a recent survey, 27% of Americans are planning to invest in cryptocurrency this year. Among MoneyLion users, almost 60% are already investing in cryptocurrencies.

Founded in 2013, MoneyLion recently announced its planned public debut after agreeing to merge with special purpose acquisition company Fusion Acquisition Corp. The deal is expected to close in the first half of this year.

What’s behind all of the buzz surrounding the recent buy now, pay later (BNPL) trend? We spoke with Jason Pavona, FIS General Manager for North American E-commerce, to get his thoughts on the matter.

As the General Manager for North America, Pavona leads FIS’s merchant acquiring commercial efforts in the United States and Canada along with driving the payments analytics business he founded and acquired by FIS.

In our interview below, we gleaned insights from FIS’s recent payments report and tapped Pavona’s expertise on BNPL, the uptick in ecommerce, and banks’ responses.

It’s widely understood that ecommerce grew in 2020. Do you anticipate that the growth curve will continue or level off?

Jason Pavona: We are seeing this growth continue for at least the next three years. Our recent Global Payments Report is forecasting that the global ecommerce market will grow by nearly 60 percent by 2024 to a total value of $7.3 trillion. The pandemic did accelerate this growth, as we saw two to three years of typical acceleration condensed into 2020, so some leveling off can be expected. However, this rapid growth was also driven by a push towards digital retail that was underway well before we had ever heard of COVID-19. Consumers are now more comfortable than ever making payments online — their inclination to the speed, ease, and flexibility of online shopping points to continued growth in the ecommerce market. While growth may slow down the line, we are not seeing signs of a plateau in that growth.

The report notes that Asia is leading when it comes to using mobile wallets at the point of sale. What’s holding back U.S. consumers from using mobile wallets at the point of sale?

Pavona: Payment innovation in Asia, and particularly China, has coincided with the rise of smartphones and powerful local super apps, helping the region leap ahead of the rest of the world in the use of mobile wallets. The pandemic helped to accelerate digitalization of the point of sale across the world and increase the usage of digital wallets, but buy-in from Asian governments in the innovation of payments has supported that development.

Mobile and digital wallets are rising in the U.S., with digital wallets accounting for a third of all online payments in 2020, but the U.S. does still have some catching up to do. We expect mobile wallets to become more ubiquitous as Americans become more used to the technology and begin using digital wallets in place of their physical credit cards.

Many Americans, however, are torn over going fully digital in their payments. FIS has found that while 55% of consumers prefer digital payments, 67% feel more comfortable using traditional payments methods.

There’s been a relatively large influx of third-party players in the BNPL space, but some banks have created their own BNPL offerings. Which do you see coming out on top?

Pavona: It is possible that banks are able to take some market share in the BNPL space, however this could be considered to be taking back market share from BNPL providers that have taken over the relationship with bank customers at the point of sale.

Third party BNPL providers are growing rapidly, and in order to compete banks need to forge stronger relationships with merchants at the point of sale – relationships companies like Affirm and Klarna already have. It may also be reasonable to expect banks, in response to third party financing, to adjust their consumer credit card offerings to gain a competitive edge and compete directly within their customer’s wallets, rather than at the point of sale.

Do you think BNPL payments will be a lasting trend or will consumers eventually default back to traditional credit?

Pavona: It is a bit early to say one way or another whether BNPL will be a lasting trend and how the leading providers will expand their product sets and relationships, though given the rapid growth of BNPL solutions across markets it’s not difficult to make a case for BNPL being here to stay. FIS expects BNPL to more than double its market share to 5% of all transactions by 2024, and comprise 4% of the global ecommerce market by 2024. While U.S. consumers may still be building trust in BNPL tools, some European countries have accepted them whole-heartedly. For example, BNPL purchases account for 20% of all online transactions in Sweden and Germany.

While we forecast several more years of strong BNPL growth at least, another question to consider is how BNPL will fare under heavier scrutiny from regulators. The U.K. and other countries have already begun discussing and introducing BNPL regulations and other countries like the U.S. could be soon to follow.

Open banking platform TrueLayer recently landed $70 million in Series D funding.

The investment, which brings the London-based company’s total funding to $142 million, was led by Addition, with contributions from all major existing investors, as well as new investors including Visionaries Club, Surojit Chatterjee, Zack Kanter, Daniel Graf, and David Avgi.

TrueLayer’s mission is to open up finance with its open banking network that connects payments, data, and identity to help people spend, save, and transact more freely online.

The funding comes at a time of major growth in the open banking scene in the U.K. The nation has seen more than three million open banking users and if the growth curve continues, 60% of the U.K.’s population will be using open banking by the end of 2023.

Founded in 2016, TrueLayer now processes more than half of the open banking volume in the U.K., Ireland, and Spain. Much of this growth has come over the course of the past year during which time the company has grown by 600x and expanded across 12 markets.

As for what’s next, TrueLayer will launch new open banking capabilities this year. The company will also expand its network, which will in turn add more account connectivity for consumers.

“We believe that open banking is reaching maturity in several markets and the next phase is about solving bigger, more complex problems for our customers – layering value on top of the raw infrastructure,” said TrueLayer CEO and Co-Founder Francesco Simoneschi. “You’ll see us building more and more in this direction.”

TrueLayer’s clients number in the hundreds and include fintechs such as Revolut, Nutmeg, Trading 212, Stake, and Payoneer.

Online lending platform Avant is building out the breadth of services for its underbanked clients this week. The Illinois-based company acquired Zero Financial and its neobank Level for an undisclosed amount.

Level is built on the premise of helping users attain financial freedom. To differentiate itself from traditional financial services offerings, the digital bank offers cash back rewards on debit card purchases, a competitive APY on deposits, early access to paychecks, and no hidden fees.

As a result of today’s deal, Avant will be able to offer its 1.5 million customers access to Level’s digital banking services to augment its existing personal loan and credit card products. The additional banking products will also offer Avant access to more customer data which, in the end, will help in its underwriting process.

Avant CEO James Paris describes the move as “an important element” of the company’s strategy that involves providing underbanked consumers with financial products. “Expanding our product portfolio allows us to serve even more people, offering every consumer access to innovative and rewards-based products to simplify and improve their financial journey,” he added. “We’re looking forward to building on this acquisition and continuing to bring new products to our growing customer base.”

Current Level customers will still be able to make purchases, earn rewards, receive direct deposits to their account, and earn interest. While new customers cannot sign up for a Level account, they are able to join the wait list for Avant’s newly-branded banking product.

Avant was founded in 2012 and has since connected customers with more than $7.5 billion in loans and 400,000 credit cards. The company has raised more than $600 million in equity from investors including JP Morgan Chase and Hyde Park Venture Partners.

Digital financial solutions provider SoFi is getting into the vehicle loan refinance game. The online lender formed a partnership with MotoRefi to offer users yet another reason to use its services.

Founded in 2016, MotoRefi connects users with lenders and manages the back-end documentation process with each state’s motor vehicle department.

According to SoFi Executive Vice President Jennifer Nuckles, the addition of an auto loan refinancing tool was a logical one since many of the company’s users carry large balances on their auto loans.

Additionally, the nation is an increasingly fertile ground for a car loan refinancing tool. In the past decade, the number of vehicle loans has grown by 41%. Today, auto loans account for 9% of all household debt, with 114 million Americans carrying a total of $1.37 trillion in auto loans.

Through today’s partnership, MotoRefi will have access to SoFi’s two million customers via an integration on SoFi’s website. MotoRefi is banking on this increase in exposure; the company expects to process $1 billion in loans this year after handling $250 million last year.

Overall, the addition of the new service is another step toward making SoFi into a more “bank-like” environment. The California-based company, which originated in student loan refinancing, has since expanded to offer personal loans, home loans, investing tools, a checking account, rewards, budgeting tools, and more.

Launched last month, SoFi’s latest tool offers investors early access to IPOs. Users with at least $3,000 in their account can purchase shares of companies as they go public. This type of access to IPOs, which is generally not available to individual retail investors, will help SoFi reach the new generation of traders that have entered the stock market since the pandemic hit last year.

Fintech connoisseurs may notice the irony in SoFi’s new IPO investment tool. The company itself recently eschewed a formal public listing for a SPAC merger with Social Capital Hedosophia Holdings.

We reported earlier this year that cloud-based digital banking solutions provider Alkami was heading toward an IPO. Today, the Texas-based company has confirmed rumors.

Alkami will to list on the NASDAQ under the ticker symbol ALKT, launching 6,000,000 shares of common stock. Shares will be priced between $22 and $25. The company believes it will to raise up to $250 million via its IPO, which would value Alkami at $3 billion.

“We currently expect to use the net proceeds from this offering, together with our existing cash and cash equivalents, to finance our growth, develop new or enhanced solutions, and fund capital expenditures,” the company said in a statement.

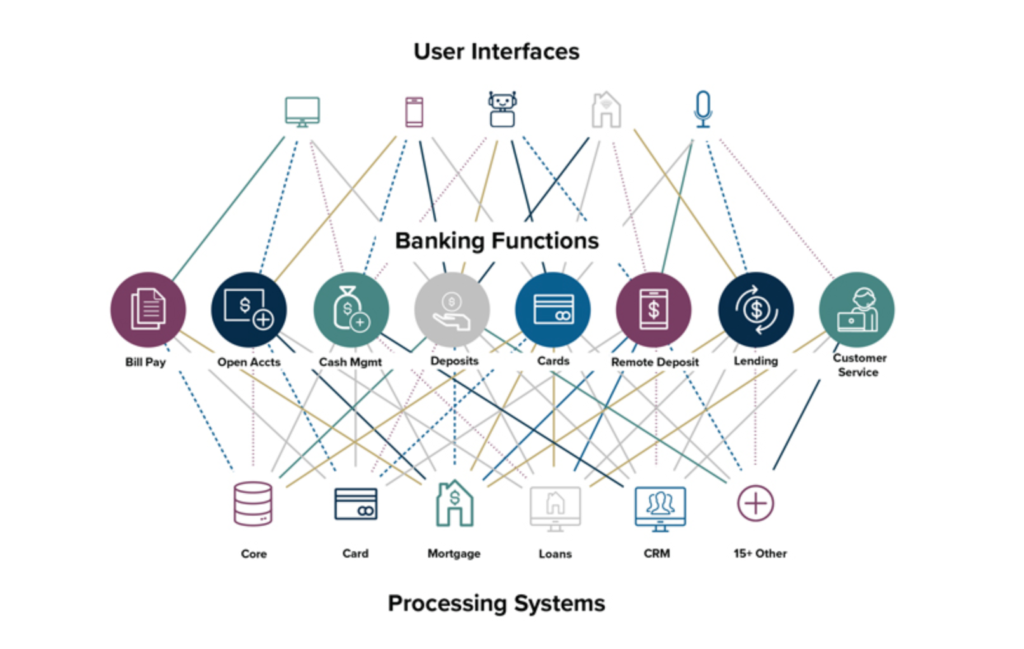

Alkami offers solutions for both retail and business banking. The subscription-based offerings include tools for money transfer capabilities, financial wellness, customer service, security, and more. And because the company is built on an open platform, banks can leverage third party solutions to customize their offerings even further.

According to Alkami’s S-1 document filed with the SEC, the company saw revenues of $112 million last year, representing a 150% increase over 2019 revenues. Alkami has received more than $385 million from nine investors, including Franklin Templeton Investments, Fidelity Management and Research Company, and D1 Capital partners.

Founded in 2009 as iThryv, Alkami counts 151 bank clients representing 9.7 million end users. Mike Hansen is CEO.

Online insurance company for the self-employed Next Insurance just closed a $250 million investment round. The funding marks the company’s second $250 million investment received in the past seven months.

Investors include FinTLV Ventures and Battery Ventures, which led the round, with participation from CapitalG, Group 11, Zeev Ventures, Founders Circle, and G Squared.

With its total funding now at $881 million, Next Insurance’s valuation now sits at $4 billion. This figure is double the $2 billion valuation assigned to the company last September.

The valuation boost is well-deserved. In the past six months, Next Insurance announced two acquisitions, added new strategic partners, and doubled its gross written premium (for those not in the insurance industry, gross written premium is essentially the total amount customers pay for insurance coverage).

Since it was founded in 2014, Next Insurance has boosted its client base to more than 200,000. The company leverages machine learning and a purely digital approach to drive costs down by up to 30% in comparison to traditional policies.

“This latest round of financing is a validation of our vision which is to make it dramatically easier for small business owners to get the insurance coverage they need by removing friction from the customer experience,” said Next Insurance Co-founder and CEO Guy Goldstein. “It starts with developing a comprehensive digital product portfolio under one roof, continues with leveraging technology that improves the customer experience, and ends with a network of integrated partnerships that bring policy purchasing to the customer within the systems they already use.”

Digital banking services company Q2 is getting a boost today. The Texas-based company announced it has acquired Minnesota-based ClickSWITCH.

As part of the agreement, Q2 will integrate ClickSWITCH’s account switching software-as-a-service solution into its product offerings. Terms of the deal were not disclosed.

Founded in 2014, ClickSWITCH offers its 450 financial institution clients an account switching solution for their end customers. The company leverages direct integrations with thousands of employers, payroll providers, and financial institutions to help users switch their direct deposits and automatic payments to new accounts. The client onboarding process, as a result, is simplified significantly.

Q2 anticipates the purchase will help its bank clients attract and retain new primary account holders. “We also believe that with ClickSWITCH we can help our customers provide their account holders with a more streamlined, frictionless experience, by offering an end-to-end digital customer acquisition, onboarding, and account switching solution,” added Q2 CEO Matt Flake.

Q2 will not only benefit from exposure to ClickSWITCH’s client base, but will also offer its existing banking-as-a-service clients more deposits, decreased client acquisition cost, and the potential for growth from an increase in cross-selling.

“As a combined force, we look forward to solving a fundamental issue that banks, credit unions, and fintech companies face – managing the complexity and administrative burden of account switching – by providing the most comprehensive and differentiated digital account switching solution in the market,” said ClickSWITCH Founder and CEO Cale Johnston. “We are delighted to be joining the Q2 team and look forward to delivering best-in-class financial solutions.”