This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Yesterday, Mastercardunveiled two new clients for its Mastercard Track Business Payment Service. The New York-based payments giant announced that BMO and Moneris Solutions Corporation have joined Mastercard Track.

Mastercard launched the new service for Canadian businesses earlier this year. Mastercard Track creates efficiencies for business users by simplifying and automating the exchange of payments data between buyers and suppliers. The service seeks to modernize the $135 trillion B2B payments market.

“Current business payment processes often require manual reconciliation work that can be very labour intensive,” said Sasha Krstic, President of Mastercard in Canada. “The availability of Mastercard Track through our new partnerships with BMO and Moneris will help Canadian businesses gain freedom from an inefficient process by simplifying and automating the exchange of payments to make B2B payments work harder, faster and smarter.”

Using Mastercard Track will help BMO and Moneris modernize the business payments process for their customers. Ultimately, the service will free up working capital for businesses by offering them more control of their payments and helping them to optimize cash flow management.

Derek Vernon, Head of Payments Modernization of BMO’s North American Commercial Deposits and Corporate Card division said that the service “enhances the digital experience by offering a universal solution to simplify and automate B2B payments.” Specifically, Vernon noted that Mastercard Track will help reduce supplier friction and facilitate quicker speed-to-spend.

Mastercard is a public company listed on the New York Stock Exchange under the ticker MA. It has a market capitalization of $364 billion. Michael Miebach took the helm of the company as CEO in January of last year.

Consumer credit reporting agency TransUnion is moving in the direction of Web3. The Illinois-based company announced this week it will bring off-chain consumer credit, identity, and compliance information to public blockchain networks.

The move is made possible via a partnership with Spring Labs, a company that offers decentralized infrastructure for credit and identity data. Spring Labs allows network participants, such as financial institutions, to share information about credit and identity data without needing to share the underlying data itself. Specifically, TransUnion will bring its VantageScore to Spring Labs’ ky0x Digital Passport, a tool that enables blockchain and smart contract applications to access off-chain data sources to create new, permission-controlled decentralized Web3 services and applications.

“We believe in the growth potential of DeFi,” said TransUnion President of U.S. Markets and Consumer Interactive Steve Chaouki. “Providing credit and identity data on-chain is a huge step towards improving the financial products available in the space. Working with Spring’s ky0x, we now have a solution for users to control and share their data on blockchain in a privacy-preserving way, enabling them to safely interact with a broader set of financial products.”

Transporting consumer credit data to the blockchain allows users to offer up information about themselves while maintaining privacy and anonymity of their identity. This secure data sharing allows users to access smart contract applications and helps DeFi and Web3 apps to scale.

Ultimately, the move should benefit both end users and lenders. By having their credit score available on-chain, users can receive better interest rates from DeFi lenders. Simultaneously, DeFi lenders can reduce their risk.

“Enabling access to an industry-standard, trusted credit risk score like VantageScore on-chain and in a consumer permissioned, anonymous way opens the door to greater growth and financial inclusion in the DeFi space,” said TransUnion SVP Consumer Lending Business Leader Liz Pagel. “Paired with ky0x’s AML and KYC capabilities, DeFi lenders can transact with confidence at lower rates, potentially paving the way for lending without the over-collateralization that is standard today.”

To be honest, there is a potential downside to this partnership. Traditional credit scores are prone to racial bias and have negative consequences for borrowers who have no established credit. By porting this imperfect risk underwriting model to the decentralized world, we may be doing ourselves a disservice.

Apple’s iPhone celebrated its 15th birthday this week (if that doesn’t make you feel old, I don’t know what will). Since its launch, the iPhone has been through 33 different models and Apple’s market capitalization has risen from $174 billion to $3 trillion.

In addition to making Apple shareholders much better off, the iPhone is also responsible for reinventing an entire industry– fintech. While fintech did indeed exist before smartphones and app stores, it was quite basic. As an example, check out Jim Bruene’s 2006 post titled, SMS Banking: Will it Work in the United States?.

Without the invention of the iPhone, smartphones would likely be around today– Blackberry and Palm Pilot would have gotten us here eventually. However, they probably wouldn’t have advanced as quickly as Apple did, and therefore wouldn’t have upended so many industries so quickly. So in celebration of the iPhone’s 15th birthday, here’s a look at how the big idea behind the small, rectangular device reinvented fintech to become what we know today.

Always on

Most people carry their phone on their person (or at least within arm’s reach) at all times. According to a 2021 study of smartphone usage statistics, 79% of users have their phone with them at least 22 hours each day, 22% of users check their phone every few minutes, and 51% of users look at it a few times per hour. These devices (and the information that they carry) have essentially become an extension of ourselves.

When your customers have their device nearby for all but two hours of each day, it not only gives them access to interact with your company and brand, it also offers you access to interact with them. Compare this to pre-iPhone era. Customers were only interacting with you when they were physically in a branch location, opening a piece of direct mail, or using their PC. Today, when a nagging thought comes up about their budget or investment information, they no longer have to jot it down to remember to look it up later. Instead, they can simply open an app on their phone to get their answer.

Push notifications

According to the study referenced above, the average smartphone user has 63 interactions with their phone each day. Some of those interactions are thanks to the user receiving alerts or push notifications, which Apple launched in 2009.

When used properly, push notifications can be a powerful tool to prompt users to take important action. Others are useful for simply promoting brand awareness. With the advent of the iPhone and push notifications, reminding customers that you still exist became much easier.

From SMS to GUI

Simply put, the iPhone helped take banks’ and fintechs’ digital customer interactions outside of strictly texting and email. The graphical user interface behind phone’s screen brought a new world to the user’s fingertips. Users were no longer limited to checking their balance or making simple transfers. Mobile apps opened up capabilities to do anything they could do online and (in many cases) in person in a bank branch.

Independent developers increasing competition

When you think of the expertise and capital required to start a bank vs. the requirements to launch a fintech, there are gaping differences. Thanks to an increasingly large talent pool of developers, anyone with a viable fintech product or service has the ability to compete with traditional banks by launching their own app in the app store.

Increased competition from fintechs has been overall healthy for the financial services industry and has made end consumers better off. When customers are unable to find a product they like or even when they have been rejected by a traditional bank, fintechs have consistently proven to meet their needs.

Authentication

Apple launched Touch ID in 2013 and in 2014 it was made available for third party apps to authenticate users. More recently, the company launched Face ID in 2017 to facilitate authentication. While fingerprint and facial recognition technology pre-dates the iPhone, it didn’t come on a pocket-sized device that consumers carry around with them.

Having biometric authentication technology available to verify the identity of users each of the 63 times they open their phone each day has made every day tasks safer for banks, fintechs, and users.

Founded in 2015, Tandem Bank used to be among the ranks of U.K. challenger banks Monzo and Starling. But Tandem Bank has remained relatively quiet for the past year-and-a-half– seemingly sidelined from the digital banking race taking place across the globe.

That’s changing today, however. Tandem Bank announced it has acquired lending platform Oplo. Financial details about the deal were undisclosed.

“I think this is a really exciting business combination,” said Tandem Bank Group CEO Susie Aliker. “We have a shared and common purpose to create a greener and fairer banking proposition. We want to build on our digital and technology capabilities to really create a really exciting but also profitable challenger bank.”

Oplo was founded in 2004 and has since lent over $1.2 billion (£900 million) to mainstream customers. The U.K.-based fintech offers car finance, personal loans, and secured loan products as alternatives to traditional bank loans. When it combines with Tandem, the digital bank will have $1.64 billion (£1.2 billion) in assets.

Tandem is very focused on the ESG initiative that has been sweeping the fintech industry; this includes digital banking players in particular. Tandem Bank currently holds $315 million (£230 million) in its Green Loans, a product that helps accountholders “save the planet whilst saving money.” Last year, the digital bank provided customers with loans for home improvements that contributed to over 12,000 tonnes of CO2 reductions.

The Green Loans product comes courtesy of Tandem Bank’s 2020 acquisition of Allium Money, an alternative lender that offers consumers financing to improve the energy efficiency of their homes.

“By joining forces, we will be able to offer a wider range of products and higher quality of service to more people than ever before,” Oplo said in a blog post announcing the change. “And together, as Tandem, we will build a fairer and greener bank for all.”

In a video, Aliker described the company’s recent shift to double-down on its ESG focus. “Our target market going forward will be what we call The New Mainstream.” We want to give them the choices so that they can also help contribute towards a fairer and greener future.”

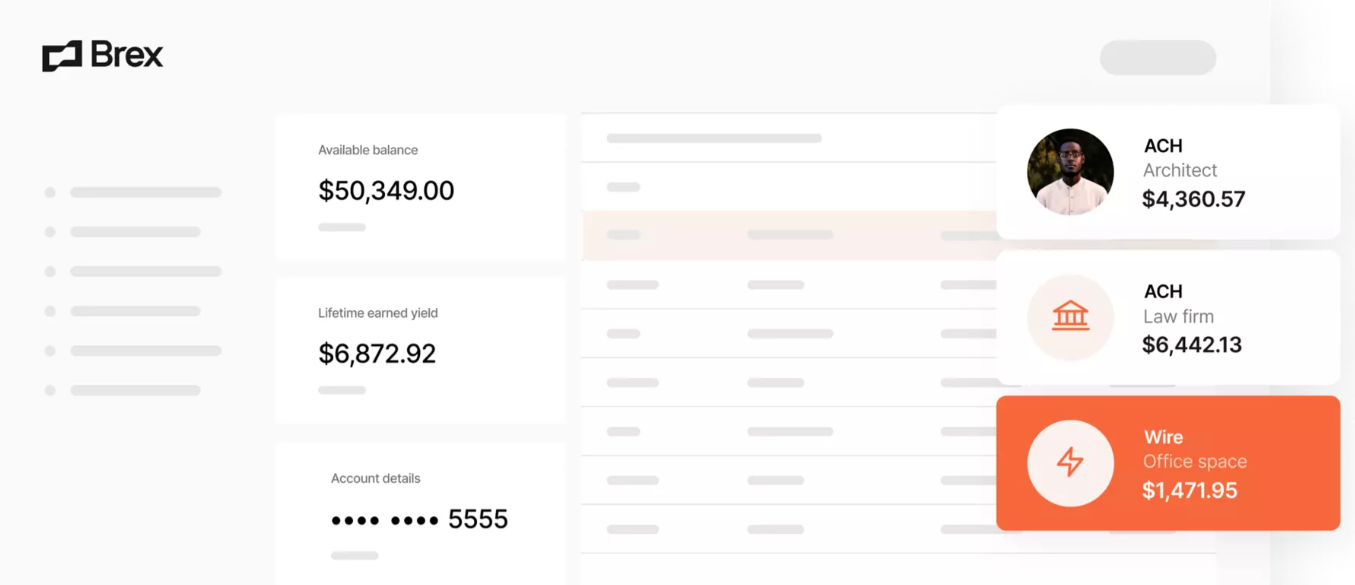

Credit card and cash management solutions company Brexclosed a $300 million D-2 round today. The round, which values the company at $12.3 billion, was led by Greenoaks Capital and Technology Crossover Ventures (TCV).

Brex will use the fresh capital to expand its product portfolio to serve more of companies’ financial needs. The California-based fintech’s funding now totals $1.2 billion.

“Brex is a market disruptor and the opportunity to create economic opportunity for millions of people and businesses globally through innovation in financial products is incredibly exciting,” said Brex Chief Product Officer Karandeep Anand. “The opportunity ahead for Brex is expansive, and I’m grateful for the opportunity to create products that will help our customers grow their businesses.”

Brex was founded in 2017 to create a digital-first business banking solution. The company offers business bank accounts with credit cards that have built-in rewards, spend controls, and expense tracking. The accounts give businesses early access to their online revenue, billpay tools, and integration with popular accounting tools– all with zero fees. The company serves “tens of thousands of businesses” ranging from small private companies to large public brands, including Airbnb and Classpass.

“Brex has always moved fast. But as the company has scaled, they’ve managed to get even faster, accelerating their growth since our last investment,” said Greenoaks Founder and Managing Partner Neil Mehta. “Brex is building a full financial operating system that keeps getting more comprehensive, all of which will delight existing customers and attract new ones.”

In addition to the funding announcement, Brex is also highlighting a noteworthy personnel change. The company appointed Karandeep Anand as Chief Product Officer. Anand comes to Brex from Meta, where he led the business products group, which served more than 200 million businesses globally. Before his start at Meta, Anand spent 15 years at Microsoft leading the product management strategy for Microsoft’s Azure cloud and developer platform.

As we survey the damage from the pandemic and its multiple variants, technology services and consulting firm Accenture has some advice, “It is critical that every bank becomes a challenger.”

In a recent report, the firm uncovered that banking has moved from vulnerable to volatile on its Disruptability Index. Underlining this point, Accenture found that bank revenues declined in 2020, then rebounded last year. “Although COVID hasn’t been a solvency event for the banking industry, we have seen material profit compression that has reordered banks’ priorities,” the report states. “Leading institutions have witnessed double-digit net income declines of 7 percent in Asia-Pacific, 37 percent in North America, and 51 percent in Europe in 2020.”

This profit compression, along with an increased cost of risk and accelerated digital transformation, has resulted in what Accenture is calling a “neo-normal.” The more level playing field has resulted in a more crowded industry. Fortunately, Accenture leaves readers with four “imperatives for success” in this new, post-COVID arena.

Understand your market

While it has always been imperative for banks to understand their customer base, customers’ needs and wants have changed since the pandemic. For example, Global Banking Consumer Study found that when dealing with a bank, customers rank value as the number one priority. That’s up four slots from just two years ago when customers ranked it number five.

Also as a part of this, Accenture noted that banks must balance managing costs with customer acquisition. “Banks can no longer spend multiple years on complex integrations—they need to build a technical stack that can quickly onboard and migrate acquired portfolios and customers so the economic value of the acquisition can be realized swiftly,” the report said.

Future-proof your business

If this was important before the pandemic, it is even more so now. That’s because what we once thought was “the future” is here today. One of the best ways to do this may be cloud partnerships, Accenture explained, because the partnerships can accelerate digital transformation via partnerships.

Banks can’t take a blanket approach, however. There is no one-size-fits-all business model, especially for larger financial institutions. Instead, banks must adopt tailored models for each business sector in which they operate.

Focus on becoming digital

Accenture suggested that a mobile app is just a ticket to the game. Banks can’t rely on the app alone as their digital strategy. Instead of relying on their mobile app as their entire digital strategy, banks should shift their thinking outside of their budget. That is, digital tools shouldn’t be put in place just to decrease cost. Banks should also leverage digital to enhance differentiation, increase revenue, and boost customer acquisition.

Adopt technology

Simply put, “there is a high correlation between technology adoption and revenue growth.” That’s what Accenture found in two separate studies recently. Similar to the point above, banks shouldn’t just look to technology to decrease costs and increase efficiencies. Instead, in order to get ahead, banks need to consider how technology can enable growth, boost differentiation, and facilitate productive partnerships.

This is, of course, easier said than done, so Accenture suggests two jumping off points for banks. First, banks should improve their boards’ knowledge about technology. Second, banks need to align their IT strategy and their growth strategy.

These four tips are just highlights. There is a lot more to the full report, including graphs and many more stats. Check out Accenture’s brief and download the report.

PayPal has confirmed recent rumors regarding plans to launch its own stablecoin. According to Bloomberg, which broke the news last week, a developer found evidence of PayPal’s future stablecoin in the form of the below logo inside the fintech’s iPhone app.

Photo credit: Bloomberg

SVP of Crypto and Digital Currencies at PayPal Jose Fernandez da Ponte later confirmed the suspicion. “We are exploring a stablecoin; if and when we seek to move forward, we will of course, work closely with relevant regulators,” Fernandez da Ponte told Bloomberg.

Developer Steve Moser made the discovery by looking at hidden code inside the PayPal app. The code unveils work on PayPal Coin, a PayPal-specific stablecoin that would be backed by the U.S. dollar. After PayPal was made aware of the discovery, the company confirmed that the code was part of a recent internal hackathon and that details surrounding the project will likely change.

If the project comes to fruition, the stablecoin would be just one initiative among a host of other cryptocurrency efforts. In October of 2020 the company partnered with cryptocurrency company Paxos to allow PayPal users in the U.S. to buy, hold, and sell cryptocurrencies. And last March, PayPal launchedCheckout with Crypto, a tool that enables users with cryptocurrency holdings to transact using crypto at the online point of sale.

When it comes to working on a stablecoin launch, PayPal is in good company. Meta (formerly Facebook) was developing its own stablecoin, Diem, until it experienced regulatory hurdles and pivoted to work with the Pax dollar instead. On top of that, Visa is looking to leverage a stablecoin to settle transactions.

In addition to its stablecoin ambitions, PayPal is also hoping to gain a reputation as the first super app in the U.S. The company revamped its mobile app last September and now offers a range of features including direct deposit, billpay management, rewards, and more. Founded in 1998, PayPal is now listed on the NASDAQ under the ticker PYPL. The company’s market capitalization currently sits at $213 billion.

If you forecasted banking-as-a-service as one of the top trends in 2022, you can go ahead and put a check mark next to your prediction. That’s because U.K.-based digital bank Starling Bankannounced today it is launching a software-as-a-service product, Starling as a Service.

Starling as a Service will help banks launch their own digital banks in months. “With SaaS (or Starling as a Service, as we like to call it) we will offer our partners the benefit of Starling’s advanced technology to use as their own,” Starling CEO Anne Boden announced in a blog post. “It will be their license, our technology.”

The move is part of a new phase for the digital bank, one that also includes an expansion of Starling’s lending offering. Going forward, Starling will now offer “a mix of strategic forward flow arrangements, organic lending across various asset classes, and a targeted M&A strategy.”

Today’s announcement also showcased some of the bank’s growth metrics. Starling has opened over 2.7 million accounts since its 2014 launch, 475,000 of which are SME accounts. The company now has $11.4 billion (£8.4 billion) in customer deposits, a figure that has risen almost $5 billion from $6.5 billion (£4.8 billion) at this same time last year. Additionally, the company has grown its lending from $2.6 billion (£1.9 billion) to $4.2 billion (£3.1 billion).

Along with the boost in these metrics, Starling also grew as a company in 2021. The bank acquired buy-to-let lender Fleet Mortgages last July, launched a new app for kids called Kite, committed to offset its own carbon emissions, (excluding lending and investments), and raised $437 million (£322 million) in March. Starling is now valued in excess of $1.5 billion (£1.1 billion).

Pre-digital P2P payments and remittance player MoneyGram made a strategic investment in cryptocurrency cash exchange company Coinme this week.

The amount of MoneyGram’s strategic investment in Coinme was undisclosed, but it gives the firm a 4% stake in the Seattle-based company. As a result, MoneyGram now holds direct ownership in Coinme.

“At MoneyGram, we continue to be bullish on the vast opportunities that exist in the ever-growing world of cryptocurrency and our ability to operate as a compliant bridge to connect digital assets to local fiat currency. Our investment in Coinme further strengthens our partnership and compliments our shared vision to expand access to digital assets and cryptocurrencies,” said MoneyGram CEO Alex Holmes.

The two companies originally teamed up last year to offer a crypto-to-cash product that combined MoneyGram’s mobile payments platform and Coinme’s cryptocurrency exchange and custody technology. The new product allows customers to purchase bitcoin with cash and withdraw bitcoin holdings in cash at thousands of physical point-of-sale locations.

“Our unique cash-to-bitcoin offering with Coinme, announced in May of 2021, opened our business to an entirely new customer segment, and we couldn’t be more pleased with our progress. As we accelerate our innovation efforts, partnerships with startups like Coinme will further our position as the industry leader in the utilization of blockchain and similar technologies,” Holmes added.

And while last year’s partnership between the two was limited to U.S.-based point of sale locations, Coinme CEO Neil Bergquist unveiled plans for a global launch. “We see this as an incredible opportunity to continue our strong growth and build on our leading presence in the world of crypto,” said Bergquist. “With MoneyGram’s global network and infrastructure, both [MoneyGram’s] continued partnership and strategic investment will help us accelerate our growth and international expansion.”

Coinme offers two cash-to-crypto products that enable users to purchase cryptocurrencies using cash at MoneyGram and Coinstar locations in 48 U.S. states. Since the company was founded in 2014, it has raised $19 million.

Last October, MoneyGram partnered with the Stellar Development Foundation and Circle to enable consumers using Circle’s USDC stablecoin to receive cash funding and payout in local currency. MoneyGram was founded in 1940 and is currently listed on the NASDAQ under the ticker MGI with a market capitalization of $692 million.

Last November, I chatted with Siri Børsum, Global VP of Finance Vertical Eco-Development and Partnerships at Huawei, as part of our Women in Fintech series.

At Huawei, Børsum is responsible for building a team that ensures Huawei has all of the financial apps for their mobile ecosystem. Børsum, who recently entered into the fintech industry, gained an interest in the tech arena while working at Google in the early days. The thrill of the new industry and betting on something big excited her about the field.

During our interview, we discussed the evolution of digital transformation and what to expect going forward. Below is a brief summary of our conversation. You can check out the full interview on the Finovate YouTube channel.

How has the digital transformation narrative changed?

Siri Børsum: I think companies are focusing even more on it and, for the first time, we as consumers have actually followed. It’s been one of those chicken-and-egg type of scenarios because we’ve all seen it’s been possible but the users haven’t joined in as much as we in the industry would have hoped for.

I now think that both companies and consumers see the extreme benefit of having better technological tools to do their banking. Consumers have now experienced good customer experience within not just the finance industry but within the tech industry– they’ve seen how apps can help them in their daily lives. This makes them more demanding than ever before and when customers are demanding, we need to step up.

What are your recommendations to help fintechs and banks keep up with changing consumer expectations?

Børsum: Start to focus on it. Have it top of mind. Not just something you say you want to do, but actually something you are measured on and that everyone in any management group or the C-suite talks about all the time. They know what KPIs there are. They know the development. It’s not something that’s left to the developers on the second floor.

Make sure it’s your highest priority. Make sure it’s measured and also don’t think you can do it on your own…. Also, you don’t drive innovation without the right culture. You need to look after your people, you need to make sure they feel safe, that they dare to try new things, and that they come to you with all the ideas. They also need information. They need to know what’s possible and they need to know what’s going on in the company in order to contribute.

What’s next for digital transformation?

Børsum: I’ve tried to bet on the future and I haven’t succeeded many times– I don’t think most people do. For me, I look more at what we see now. What are the current trends and what do I wish for as a customer?

I think embedded finance is obviously the next step and we need to see that work, truly. For me, personally, I would love to see payments disappear, totally. We’ve already seen these things and were moving towards it. It won’t happen straight away, but it’s definitely the direction we’re going.

Siri Børsum will deliver a keynote address titled, “Capturing Your Customers’ Goals & Finding New Revenue StreamsBy Putting Yourself At The Heart Of Their Lives” at FinovateEurope which is taking place March 22 through 23 both in-person in London and digitally.

AI-powered decision making firm Fractal Analyticslanded a $360 million investment from alternative asset firm TPG Capital this week. The round brings the 21-year-old company’s total funding to $685 million.

While there is no official word on Fractal’s valuation, Fractal CEO and Co-founder Srikanth Velamakanni told Bloomberg earlier this year that the company is “assessing interest from investors valuing the company at significantly more than $1 billion.”

The funds are coming from TPG’s Asia-focused private equity firm, TPG Capital Asia. The deal, which is expected to close in the first quarter of this year, is comprised of a combination of a primary investment and secondary share purchases from funds advised by private equity advisory firm Apax. Both TPG and Apax will be minority shareholders in Fractal.

As part of today’s deal, TPG’s Puneet Bhatia and Vivek Mohan will sit on Fractal’s board of directors.

“Fractal is building a great workplace and an innovative culture that’s driving significant client outcomes through our ‘user focused, decision-backwards’ approach to solving problems,” said Velamakanni. “TPG’s capabilities across all our markets and their proven success in building and supporting top AI providers is the perfect complement to the partnership we’ve enjoyed with Apax, whose insight and expertise have been instrumental in accelerating our growth.”

Headquartered in New York City, Fractal helps businesses leverage AI to power and inform human decisions. The company serves a range of industries, offering products including Senseforth.ai, a conversational AI platform; Samya.ai, a revenue growth AI; Crux Intelligence, an AI-powered analytics platform; Eugenie.ai, a tool for AI-driven operational efficiency.

Fractal employs 3,500 employees in 16 offices across the globe, including the U.S., the U.K., Ukraine, India, Singapore, and Australia. Last month, the company appointed Manish Tiwari as Chief Information Officer. Last summer, Fractal announced it is exploring an IPO. The funding route would help fuel the company’s growth now that companies have made a post-pandemic push to move their operations to the cloud. “The floodgates have opened,” said Velamakanni. “We have the scale to be a public company.”

Sky News announced this week that Lloyds Banking Group plans to invest in loyalty app Bink. According to the source, Lloyds will invest “millions of pounds” in exchange for a minority stake in the U.K.-based fintech startup.

Founded in 2015, Bink enables consumers to forgo traditional plastic loyalty cards by registering their debit or credit cards and linking them to various loyalty schemes. The company’s technology helps retailers identify and reward customers each time they shop, offers banks a way to keep their cards top-of-wallet, and provides a simplified way for shoppers to earn rewards.

In 2019, Bink formed a strategic partnership with Barclays, which made a $13.5 million (£10 million) investment. This deal made Bink accessible to Barclays’ seven million U.K. customers.

Barclays customers can find Bink within their existing mobile banking app, where they can join, accrue, and redeem rewards. Other users can download the Bink app and establish their Bink wallet to begin building rewards.

Lloyds’ partnership with Bink is expected to go live in the next six months, but it is still unknown the amount, or at what valuation, Lloyds plans to invest in Bink.

Bink’s card-linked offers tool is very reminiscent of the many loyalty and rewards schemes that rose out of the mobile wallet craze in 2015. When NFC and Bluetooth Low Energy became promising enabling technologies, many startups (and even some established companies) tried to replace consumers’ everyday mobile wallets. Though mobile wallets failed to take off seven years ago, they are making a comeback today thanks to increased digital adoption.

Given that consumers are finally ready to adopt these new technologies, perhaps Barclays and Lloyds are on to something. Is this the start of a card-linked offers and merchant-funded rewards resurgence?