This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Tax compliance firm Avalara has agreed to be acquired by Vista Equity Partners for $8.4 billion.

Avalara has more than 30,000 customers in 95 countries.

The transaction will take Avalara private, removing it from the New York Stock Exchange.

Avalara is starting the week with a big move. The tax compliance firm has agreed to be acquired by global investment firm Vista Equity Partners for $8.4 billion. Vista Equity Partners is acquiring Avalara at $93.50 per share, which represents a 27% premium of Avalara’s closing share price on July 6, 2022.

Founded in 2004, Avalara helps its more than 30,000 customers in 95 countries comply with tax regulations. The Washington-based company offers compliance solutions for various transaction taxes, including sales and use, VAT, GST, excise, communications, lodging, and other indirect tax types. In addition to tax compliance, Avalara also helps companies secure business licenses and provides sales tax data analysis that offer business insights. Among the company’s clients are Zillow, Pinterest, and Roku.

“Avalara is a mission-critical platform serving customers in a variety of end-markets, including retail, manufacturing, hospitality, and software,” said Vista Equity Partners Managing Director Adrian Alonso. “Avalara’s solutions, its commitment to product innovation, and its network of extensive partner integrations, resellers, and accountants make it a true leader in the space.”

Once complete, the transaction will take Avalara private, removing it from the New York Stock Exchange. Prior to going public in 2018, Avalara had raised $341 million. Scott McFarlane is co-founder and CEO.

Santander Bank has selected Rocket Mortgage to provide its clients an online mortgage lending tool.

Rocket Mortgage will offer Santander clients exclusive discounts and resources to help them in their home buying journey.

Rocket Mortgage was among the first to offer a fully digital mortgage lending experience when it did so in 2015.

A partnership between Santander Bank and Rocket Mortgage is taking off today. Santander has selected online mortgage lending company Rocket Mortgage to serve as the as the exclusive preferred mortgage provider for its customers.

Santander will leverage Rocket Mortgage to offer its two million clients exclusive discounts and resources to help them in their home buying journey. The collaboration enables users to interact independently online or speak to a home loan expert via a phone call, email, or online chat.

“At Santander, we place the customer at the center of our business, and I’m pleased to be working with Rocket to deliver a convenient and simplified digital mortgage experience for our customers,” said Santander Bank Head of Consumer and Business Banking Patrick Smith. “Our relationship with Rocket Mortgage is another example of how Santander Bank is evolving our business and continuing to pursue opportunities for our customers to save, invest and manage their money at Santander.”

Santander is able to use its scale to secure discounts on loan costs and closing costs for its clients. Santander Private Clients and employees who close loans with the new platform can benefit from enhanced discounts.

Formerly known as Quicken Loans, Rocket Mortgage was a pioneer in digital mortgage lending. The company was among the first to offer a fully digital mortgage lending experience when it did so in 2015. The company closed $351 billion of mortgage volume across every U.S. state in 2021.

BlackRock has selected Coinbase to help its clients buy and sell bitcoin.

Under the partnership, clients of BlackRock Aladdin will benefit from Coinbase Prime.

Partnering with Coinbase will help BlackRock add digital currencies as an asset class for the first time.

Coinbase is partnering with BlackRock to help some of the asset manager’s institutional clients connect to Coinbase Prime, making it possible for them to buy and sell bitcoin.

Under the agreement, common clients of Coinbase and BlackRock’s end-to-end investment management platform Aladdin, will benefit from Coinbase Prime, a full-service platform to access crypto markets at scale. At the outset, Aladdin clients will be limited to using Coinbase Prime to buy and sell bitcoin.

With $10 trillion in assets under management, BlackRock offers clients a range of investment strategies, including alternative assets, sustainable investing, factor-based investing, systematic investing, and now digital assets. The company has 8,000 employees across the U.S. and works with more than 190,000 financial advisors to help build client portfolios.

The move adds cryptocurrency as an asset class for BlackRock clients for the first time. “Our institutional clients are increasingly interested in gaining exposure to digital asset markets and are focused on how to efficiently manage the operational lifecycle of these assets,” said BlackRock Global Head of Strategic Ecosystem Partnerships Joseph Chalom. “This connectivity with Aladdin will allow clients to manage their bitcoin exposures directly in their existing portfolio management and trading workflows for a whole portfolio view of risk across asset classes.”

BlackRock and Coinbase will roll out functionality in phases to interested clients.

Coinbase was founded 2012 and went public late last year. The company trades on the NASDAQ under the ticker COIN. The news of a new client for Coinbase Prime has given Coinbase a boost this week after the recent crypto winter took its toll on the company, which announced a hiring freeze and layoffs earlier this summer. Coinbase’s market capitalization currently sits at $19.74 billion.

Thoma Bravo is acquiring Ping Identity in an all-cash deal for $2.8 billion.

The acquisition will take publicly held Ping Identity into the private markets.

Thoma Bravo’s other recent fintech acquisitions include Bottomline Technologies, Digital Insight, and Ellie Mae.

Cloud-based identity software provider Ping Identity has agreed to be acquired by private equity firm Thoma Bravo. The all-cash deal is expected to close in the fourth quarter of this year for $2.8 billion.

“We are pleased to partner with Thoma Bravo, which has a strong track record of investing in high-growth cloud software security businesses and supporting companies with initiatives to turbocharge innovation and open new markets,” said Ping Identity CEO Andre Durand.

Ping Identity was founded in 2002 and has since made seven acquisitions of its own, including passwordless identity verification company Singular Key, bot prevention and fraud intelligence firm SecuredTouch, intelligent authorization company Symphonic, blockchain-based identity startup ShoCard, AI-powered security company Elastic Beam, customer identity solution UnboundID, and Accells Technologies.

Ping Identity has leveraged this acquired expertise, in addition to its own in-house knowledge, to help enterprises remove passwords, prevent fraud, support Zero Trust. The company offers a no-code, drag-and-drop user interface to make its seemingly intimidating offerings more approachable for non-technical staff.

After the deal closes, Ping Identity, which is listed on the New York Stock Exchange with a market capitalization of $2.38 billion, will transition to a privately held organization. Before the company’s debut onto the public markets, Ping Identity was majority-owned by Vista Equity, which now owns 9.7% of shares in the Denver, Colorado-based company.

“Ping Identity is a leader in intelligent identity solutions for the enterprise and is well-positioned to capitalize on the significant opportunities in the $50 billion Enterprise Identity security solutions area,” said Thoma Bravo Partner Chip Virnig. “Our shared commitment to growth and innovation, combined with Thoma Bravo’s significant security software investing and operational expertise, will enable Ping Identity to accelerate its cloud transformation and delivery of industry leading identity security experiences for the customers, employees and partners of large enterprises worldwide.”

Today’s purchase marks Thoma Bravo’s 91st acquisition. The firm takes a buy-and-build approach in which it acquires similar companies and consolidates them to create synergies and develop companies with greater scale, scope, and broader service offerings. Among the Illinois-based company’s most recent fintech purchases are Bottomline Technologies, Digital Insight, and Ellie Mae.

The third annual Finovate Awards ceremony is taking place next month, which means our panel of 20 judges has carved down the list of nominees in 23 categories down to just 129 finalists. As always, competition this year was steep, so the finalist title is well-earned.

Congratulations to everyone who made it to the finalist round! The winners will be announced at the 2022 Finovate Awards ceremony on September 13 at the Edison Ballroom in New York City. Register now to secure your seat or table at this year’s celebration.

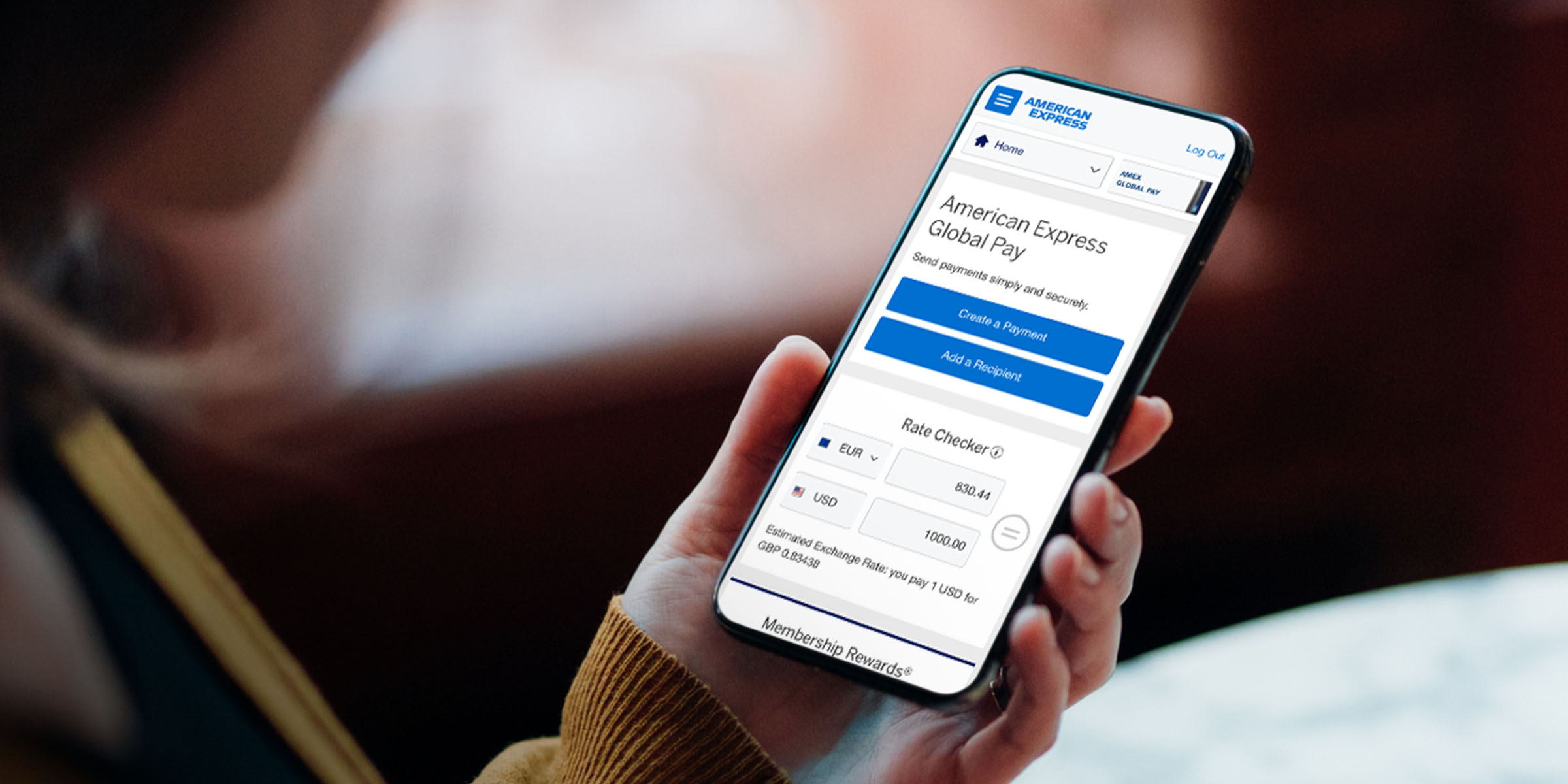

American Express is launching American Express Global Pay, a cross-border payments tool for U.S. small businesses.

Businesses can use American Express Global Pay to pay suppliers in more than 40 countries and in 12 currencies.

American Express did not disclose exact fees, but said that it will display the fees when the business is creating the payment.

American Express is helping small businesses keep up with global competition with its launch of American Express Global Pay, a new cross-border payments tool for small businesses based in the U.S.

American Express Global Pay allows U.S. businesses to make domestic and international B2B payments to suppliers in more than 40 countries and in 12 currencies using the mobile-optimized website. Eligible customers can earn one Membership Rewards point for every $30 in equivalent foreign exchange payments.

“Businesses today start, grow and compete on a global scale,” said American Express Executive Vice President of Global Commercial Services Dean Henry. “Our U.S. Small Business Card Members told us they want an international payment solution focused on simplicity, convenience and the chance to earn rewards – so we built American Express Global Pay to enable these businesses to easily and effectively manage their B2B payments globally on a secure platform, backed by the trusted service and unique benefits of American Express Membership.”

Available to eligible U.S. American Express Small Business Card Members, American Express Global Pay enables users to access the cross-border tool in the same location they manage their American Express Business account and offers same-day delivery of funds in select countries.

While American Express has not disclosed exact fees, the company said that it will display the fees when the business is creating the payment. “In addition to these fees, we also make money from the purchase and sale of foreign currency,” American Express said. “Recipient banks or intermediary banks may charge their own fees, which can reduce the amount delivered to your recipient.”

It’s August, which means that FinovateFall officially kicks off next month. The summer heat may have you in vacation mode, but in a matter of weeks it’ll be time to switch gears and get ready for our three-day event, taking place in New York City, September 12 through 14.

Book your spot at this year’s conference by August 12 to save $600. FinovateFall is celebrating its 15th anniversary this year, so you know it’s going to be big!

Because I know you’re busy submitting your final vacation request for the summer, I’ve distilled the agenda down to a few highlights.

Day 1

Demos It wouldn’t be a Finovate event without the 7-minute demos. We’ll have three demo sessions on the first day of the event. Check out our list of who is demoing so far.

Panel: The Fintech Ecosystem & Strategic Partnerships – From Competition To Collaboration & Co-Creation Moderated by American Banker’s Penny Crossman, this panel features Josh Williams, CBO & Head of Partnerships at Seattle Bank; Maria Gotsch, President and CEO at Partnership Fund for New York City; Mike Vostrizansky, Growth Equity Investor at FTV Capital; and Franklin Garrigues, Vice President, External Ecosystems at TD Bank Group.

Startup booster The Startup Booster offers a chance for fintech founders to network with early stage fintech investors. This new session helps fintech founders gain insights and connections from investors through pre-booked one-to-one meetings. See if you qualify to participate in our Startup Booster program.

Day 2

More demos We’re featuring four demo sessions on the second day of the conference and will announce the Best of Show winners at the end of the second day.

Keynote Address: What Wins Deals in Fintech – What Are The Essential Success Factors for Winning More Deals, Better Deals, Faster Deals? Sam Kilmer, Managing Director at Cornerstone Advisors, will talk us through how to get deals done in fintech.

Power Panel: Why Reinventing Banking & Reimagining Customer Experience Is Vital For Banks To Compete In The New Normal Oak HC/FT Co-Founder & Managing Partner Patricia Kemp will moderate this session, with participation from Beyond the Arc CEO Steven Ramirez and Quavo Fraud & Disputes SVP and Revenue Executive Brittany Usher.

Day 3

Analyst All Stars Hear from Daniel Latimore, Chief Research Officer and Member of the Leadership Team at Celent; Alyson Clarke, Principal Analyst at Forrester; and Philip Benton, Senior Analyst of Financial Services at Omdia, on key opportunities and trends in the financial services space.

Fintech Fight Club Cage Match Edition Watch three industry leaders duke it out over some of the most challenging questions facing financial services. This is not another panel, but a cage match of ideas and opinions. This year’s participants include Jason Henrichs, CEO of Alloy Labs; Mary Wisniewski, Editor of Bankrate; and Lindsay Davis, Head of Markets at Atomic FI.

Fireside Chat: Climate Change & Financial Services – An Existential Threat Or The Biggest Opportunity In A Generation? I get to sit down with OakNorth President and COO Peter Grant to discuss how fintechs and financial services companies can find opportunities amidst a growing climate crisis.

There is, of course, much more to this year’s FinovateFall event. Check out the whole agenda, take a look at the speaker lineup, and be sure to register to be part of the 15th FinovateFall.

Uber is launching a new debit card with tandem checking account.

The Uber Pro debit card is made available via partnerships with Mastercard, Marqeta, and Branch.

Uber Pro cardholders can receive up to 7% cashback on fuel purchases.

Uber’s latest attempt to attract more drivers to its platform comes in the form of a debit card with a tandem checking account. Late last week, the rideshare company announced the Uber Pro debit card.

The new debit card comes courtesy of partnerships with Mastercard, Marqeta, and Branch, a workforce payments platform that caters to gig economy workers and contractors. The card offers Uber drivers up to 7% cash back on gas purchases when they achieve Diamond status as an Uber Pro driver.

The Uber Pro card comes with a checking account powered by Branch, which will automatically deposit cardholders’ earnings into their account after every trip. Branch offers a unique take on earned wage access by enabling workers to access their paycheck as they earn it. The card currently has a wait list and will launch in the coming weeks.

This latest announcement comes three years after Uber originally introducedUber Money, a debit card and mobile app powered by Green Dot, and five years after the company launched its Barclays-powered credit card.

The launch of the Uber Pro card comes alongside a handful of other driver-related announcements from the ridesharing company. The Uber app will now offer drivers a range of nearby trips to choose from, show drivers their exact earnings upfront before they accept a trip, and offer enhanced benefits to Uber Pro drivers.

These driver-focused benefits are in part an effort to smooth out the supply and demand issue that Uber is facing. The nationwide labor shortage, combined with high fuel prices, has historically made it difficult for Uber to attract drivers. In May, Uber CEO Dara Khosrowshahi said, “Our need to increase the number of drivers on the platform is nothing new nor is it a surprise … there’s a lot of work ahead of us, but this is a machine that is rolling.”

Rapyd will facilitate in-app payments for Viber users.

“Through this partnership, Rakuten Viber can confidently step into the world of payments and become a leader in embedded finance, supported by Rapyd’s licensed end-to-end fintech offerings,” said Rapyd CEO Arik Shiltman.

Payments platform Rapyd partnered with consumer-facing messaging app Rakuten Viber today. Under the agreement, Rapyd will facilitate in-app payments for Viber users.

“The future of payments is integrated fintech, and this partnership demonstrates why we founded Rapyd in the first place: to democratize fintech for all,” said Rapyd CEO Arik Shiltman. “We’re proud to provide the infrastructure and licensing for global companies like Rakuten Viber, one of the world’s most trusted and recognized messaging and communications platforms, to develop their own financial services without them having to build the foundation from scratch. Through this partnership, Rakuten Viber can confidently step into the world of payments and become a leader in embedded finance, supported by Rapyd’s licensed end-to-end fintech offerings.”

The move places Rakuten Viber squarely in the center of the global digital payments space. Viber users can use the messaging service to send and receive money instantly, with no fees. Recipients can store money in a mobile wallet with an IBAN, which is available in the Viber app. Rakuten Viber is launching the service in Greece and Germany, where users can transact in Euros. The company will later expand into multiple currencies and will roll out to more countries.

Founded in 2016, Rapyd is a fintech-as-a-service innovator that offers a payments network and platform to facilitate local and international supplier and customer payments. The company has offices in London, Tel Aviv, San Francisco, Denver, Dubai, Miami, Singapore, Iceland, and Hong Kong.

MX has appointed Jim Magats as CEO, replacing Interim CEO Shane Evans.

Magats comes to MX after spending 18 years as a senior executive at PayPal, where he specialized in open finance.

Evans will continue to serve as a senior advisor.

Open finance fintech MXnamed Jim Magats CEO this week.

The news comes after company Founder and former CEO Ryan Caldwell stepped down at the beginning of the year, appointing Shane Evans as Interim CEO. After the transition, Caldwell stepped into a new role as Executive Chair to spend more time with family and focus on his daughter’s health recovery.

“Jim Magats brings a wealth of experience and knowledge about how to deliver high-impact financial solutions and products for consumers, merchants, and financial organizations, along with a vast network of partners and customers at the world’s leading financial institutions and fintechs,” said Caldwell. “We have tremendous confidence in Jim’s ability to lead the organization through the next phase of our growth in establishing our leadership in the open finance economy, helping organizations of all sizes access and act on financial data to improve customer outcomes and grow their businesses.”

Magats comes to MX after spending 18 years as a senior executive at PayPal. Most recently, he served as the company’s Senior Vice President for Omni Payments Solutions where he was charged with overseeing the company’s open banking strategy and partnership network of more than 150 financial institutions and networks.

The appointment is strategic for MX, which has spent the past few years positioning itself as a leader in the open finance space, because of Magats’ experience in open finance. While at PayPal, he worked with regulators in Europe helping to create PSD2 banking standards. He also spent time building PayPal’s open, secure API capabilities to facilitate digital payments.

“Financial data is the lifeblood of a connected economy, and nobody helps organizations access and act on financial data better than MX. Our opportunity to make financial data accessible and actionable is global, extends across verticals, and has the potential to make a positive difference in the lives of billions of people,” said Magats. “After 18 amazing years at PayPal, I’m incredibly excited to join MX, a company on a mission to build the open finance economy and empower the world to be financially strong. We are going to deepen and extend our partnerships with financial institutions and fintechs to fuel the next wave of innovation while fostering greater participation in the global economy through new products, use cases, and services.”

During his seven-month tenure as Interim CEO, Evans saw the company through the tragic passing of company Cofounder Brandon Dewitt. Evans, who joined MX in 2019 as Chief Revenue Officer, will continue to serve as a senior advisor.

European business finance solution company Qonto is seeking to acquire its competitor Penta.

Together, the two will serve more than 300,000 small business customers across Germany, France, Italy, and Spain.

Terms of the deal have not been disclosed.

Two European business finance solution companies have agreed to join forces. In the deal, which is expected to close in the next few weeks, Paris-based Qonto is seeking to purchase Berlin-based Penta. Financial terms have not been disclosed.

“When Steve Anavi and I founded Qonto in 2016, we had the ambitious goal of simplifying everyday banking for SMEs and freelancers across Europe,” said Qonto CEO Alexandre Prot. “Today, we’re already present in four European markets and, while I’m very proud of what we’ve achieved so far, we want to go even further: the natural next step was to join forces with Penta. We are thrilled to welcome the Penta team onboard. Together we’re going to be the finance solution of choice for one million European SMEs and freelancers by 2025!”

Penta launched in 2017 and now serves 50,000 small business customers in Germany. Qonto launched the same year and currently serves more than 250,000 clients across France, Germany, Italy, and Spain. The acquisition will combine Qonto’s brand strength, license, and core banking system with Penta’s local expertise.

Qonto is anticipating that Penta’s existing market presence will strengthen its operations in Germany. The combined entity will make Qonto a strong leader in the European digital business finance sector. After the acquisition is complete, the company will have more than 300,000 customers and 900 employees.

“With the combination of increasing customer numbers and rising revenues, we have gained even more substance in the past 18 months,” said Penta CEO Markus Pertlwieser. “We are very excited that we now have the chance to actively shape digital banking for business customers in Europe as a team with Qonto.”

Open-Finance.ai partnered with FICO to leverage the company’s Blaze Advisor decision rules management system.

Israel-based Open-Finance.ai will integrate Blaze Advisor into its open banking platform to offer real-time credit assessments.

This news comes as “Israel is on the cusp of major banking reform with the introduction of open banking,” said FICO VP of Partner Management in Europe, the Middle East, and Africa Mark Farmer.

Analytic decisioning platform FICO and risk, finance, and compliance software company Open-Finance.ai have teamed up this week.

Under the agreement, Open-Finance.ai will integrate the FICO’s Blaze Advisor decision rules management system into its open banking platform. Using FICO’s technology, Open-Finance.ai will assist its financial services clients to save time on consumer credit assessments by leveraging real-time, analytically driven appraisals.

For Israel-based Open-Finance.ai, this comes just as open banking legislation is gaining traction. “Israel is on the cusp of major banking reform with the introduction of open banking,” said FICO VP of Partner Management in Europe, the Middle East, and Africa Mark Farmer. “Automating decisions allows lenders to increase the efficiency of the lending process without sacrificing risk management regulatory rigour. This will speed up lending, increase customer satisfaction, reduce operational costs and drive economic activity.”

Open-Finance.ai anticipates the move will help remove human bias from lending decisions, improve risk decisions, and expand access to credit to more people.

FICO’s Blaze Advisor gives businesses a solution to make smarter, more transparent business decisions by offering companies multiple methods for rule authoring, testing, deployment, and management. To make this work, Blaze Advisor provides decision trees, scorecards, decision tables, graphic decision flows, and customized templates. The technology also supports business performance monitoring.

“Manual processes, a conservative approach and significant regulation have been a drag on growth of the Israeli market,” said Open-Finance.ai Co-founder Shay Basson. “Now, we have an ability to manage risk instantly, based on multiple data sources to provide an instant, yet risk-aware decision to credit and insurance consumers.”

Founded in 1956 and headquartered in California, FICO offers decisioning tools used by more than 650 clients, including nine of the top 10 U.S. banks and eight of the top 10 EMEA banks. Last year, FICO launched a new loan origination solution called FICO Originations Solution that seeks to automate the entire customer journey.