This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Starting this week, NatWest is making it easier for clients to get the help they need to make their banking experience easier. The initiative is called Banking My Way and provides a single place for customers of the U.K.-based bank to input their preferences so that they are addressed across all channels.

The preferences are divided into two sections, About me, which addresses vulnerabilities or disabilities such as being visually or hearing impaired, and Support me, which focuses on how the bank can support the user, such as speaking slowly and clearly or not assuming a gender when addressing them.

“Banking My Way will allow you to tell us more about your current circumstances and the difficulties that you are facing with your banking,” NatWest explained on its website. “This will allow you to also tell us about the support you require, and we will ensure that this information is shared with our teams to support any further interactions that you have with us.”

Clients can input or change preferences online, in a branch, or via phone. In order to ensure information is up-to-date, users will be asked to review their preferences on an annual basis.

This is an amazingly simple idea, but because it is a pull, rather than a push approach, it may be lost on some consumers. That said, NatWest will have the best response rates with this system if it is implemented as part of the onboarding process, instead of being structured as a separate item customers need to register for.

Crypto asset-backed lender BlockFI just landed $50 million in funding, marking the company’s third investment in just 12 months.

The round was led by Morgan Creek Digital with participation from Valar Ventures, CMT Digital, Castle Island Ventures, Winklevoss Capital, SCB 10X, Avon Ventures, Purple Arch Ventures, Kenetic Capital, HashKey, and others.

BlockFI will use the cash to hire more employees and boost its business offerings. Specifically, BlockFI plans to add support for additional assets and currencies and is working on the launch of a bitcoin rewards-based credit card.

Flori Marquez, SVP of Operations and Co-Founder of BlockFi, described the company as “a driving force in bringing cryptocurrencies mainstream.” And that summarizes BlockFI’s goal with this new growth round. Not only does the company hope to improve the customer experience, it also wants to broaden the appeal of crypto-based investment.

Founded in 2017, BlockFI offers some of the same services customers are used to seeing at their traditional bank, only for cryptocurrencies. In addition to providing trading and institutional services, the company allows users to earn compound interest in a range of different cryptocurrencies. BlockFI also helps clients leverage their cryptocurrency as collateral towards a loan, paid in U.S. dollars, and receive their cryptocurrency back after the loan is paid off.

“With the support from our partners, we’re creating a platform for investors where they aren’t investing in just digital assets anymore—they’re investing in the future, greater financial empowerment and accessibility,” said Zac Prince, CEO and Founder of BlockFi.

BlockFi, which currently has $1.5 billion in assets on its platform, has seen impressive growth in recent months. The company ballooned its revenue 10x over the past year, with plans to reach $100 million in revenue over the next 12 months.

A couple weeks back I had a conversation with Andrew Besheer, Head of North America for Appway, about the rise of challenger banks. Our discussion centered around some of the data points in Ron Shevlin’s piece, The Online Banking Insurgency of 2020, published in Forbes last month.

One of the questions that came up was if this surge in new challenger bank accounts is an accident of digital transformation? In other words, are Millennials and Gen Z consumers gravitating towards challenger banks because their websites appear more digitally savvy?

At its core, this is a chicken-and-egg question. Are challenger banks successful because their tech-first approach satisfies consumers? Or are underserved consumers driving challenger banks to create new products and services that banks are unable (or unwilling) to offer?

First, its important to recognize that both challenger banks and incumbents know their target market. That is, the challenger banks are catering to an audience looking for a different bank experience than the one that appeals to their parents.

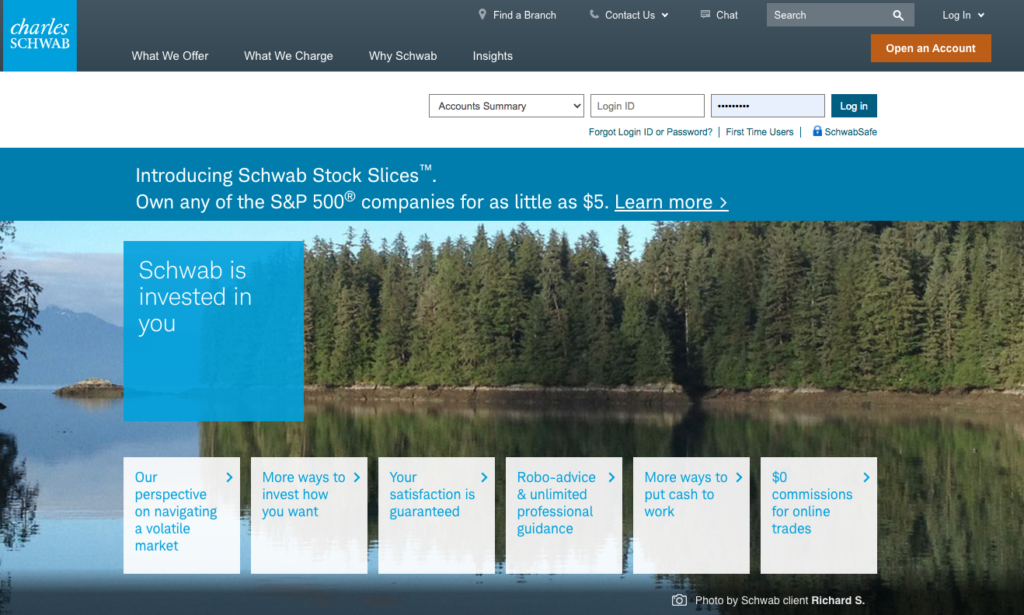

To answer this question, first, take a look at the outward appearance. Traditional banks’ websites are text-heavy, with long-winded fine print, and are intimidating enough to drive away less experienced consumers. Conversely, challenger banks use colloquial language and present websites that look simple and transparent. As an example, take a look at Charles Schwab’s website:

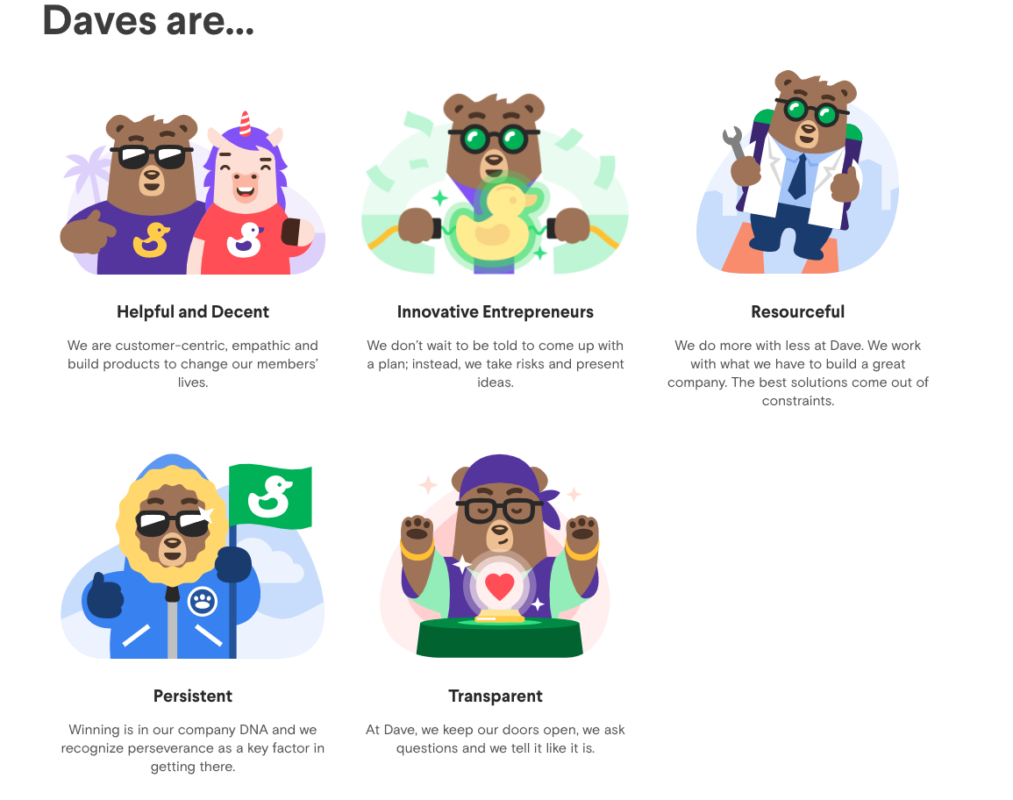

And now look at Dave’s:

Both are relatively technologically and digitally advanced banks, but they are appealing to two entirely different demographics.

Taking a look under the surface, the products and services each bank offers are also different. Schwab’s are heavily geared toward investing and trading, while what Dave offers– paycheck advances and credit building tools– seems to center around keeping its users afloat.

In the end, the two approaches are perfectly suited for users on opposite sides of the generational spectrum. My father and grandfather would never bank somewhere that had a cartoon as a mascot. And younger, Generation Z users don’t trust incumbent banks’ language and apparent lack of transparency.

Now, to answer the question, “are Millennials and Gen Z consumers gravitating towards challenger banks because their websites appear more digitally savvy?” The answer is no. Challenger banks are built from the ground up to entice this generation of users. And while the banks’ advanced digital capabilities help to draw users in, they are not the sole reason younger, tech-savvy users choose them.

You can check out the full interview, where Besheer and I delve further into the challenger banking conversation, on Appway’s website.

You’ve likely heard the phrase, “every company will become a fintech company.” That’s because the banking-as-a-service model has officially taken off and is helping companies across all industries offer their customers a variety of banking options.

Perhaps that’s what Alviere was thinking in creating its new flagship offering, TheHivePlatform, which it distinguishes as a Financial-Services-as-a-Platform (FsaP) tool. Hive allows businesses to choose from a range of seven financial services offerings– including banking and treasury application services; payment processing and cross border transactions; debit, prepaid, and credit issuing services; identity, risk, and fraud management services, business intelligence and analytics, customer communication tools, and mobile technology– and enables them to easily integrate their own branded tools into their existing business via an API.

“We know from our own experience the pain it takes to get a financial service to market, so we launched Alviere and The HIVE to help companies like us to alleviate the pain,” said Yuval Brisker, co-founder and CEO of Alviere. “We’re excited to announce the launch of The HIVE, which is the most advanced and complete Financial Services as a Platform (FsaP) on the market today. It’s much more than Banking-as-a-Service, incorporating many more capabilities than similar offerings.”

The Hive Platform also solves one of the biggest hurdles for companies delivering financial services– regulations. That is because it is already designed to be deployed in any geography with any regulatory framework.

Offering businesses financial services is a good move because it allows companies to focus on their core competency while providing access to valuable financial services. In addition to keeping customers happy, delivering financial services helps businesses by creating a stickiness that will drive customers back to their business, website, or app more frequently.

Founded by Yuval Brisker and Pedro Silva, Alviere is now available to businesses in Canada and the U.S. The company plans to be available in more geographic regions by year-end.

After teasing the launch of its debit card in the U.S. earlier this year, Samsung announced that its digital debit card, the Samsung Pay Card, is now available in the U.K.

To make the launch possible, Samsung has teamed up with Curve, a fintech that consolidates all of a user’s existing Mastercard and Visa payment cards. The London-based company makes all of a user’s cards contactless and compatible with Samsung Pay.

Users will receive access to Curve features such as peer-to-peer money transfers, instant notifications about spending, competitive foreign exchange rates, 1% cash back on purchases made with a select group of three merchants, and 5% cash back on purchases made at Samsung.com. Samsung Pay Card users will also be able to use Curve’s Go Back in Time feature that allows them to switch payments from one card to another for up to 14 days after the purchase was made.

The deal is a win-win for both companies; Samsung will benefit from Curve’s e-money license with the U.K. Financial Conduct Authority, and Curve will gain from an increase in users. Interestingly, however, existing Curve users cannot also apply for a Samsung Pay card. As other sources have pointed out, the reason for this exclusion isn’t entirely clear.

“At Samsung we believe in the power of innovation and, through our partnership with Curve, the Samsung Pay Card brings a series of pioneering features that will change the way that our customers manage their spending, with their Samsung smartphone and smartwatch at the heart of it,” said Conor Pierce, Corporate VP of Samsung U.K. and Ireland. “This is the future of banking and we look forward to continuing this journey with our customers.”

Fintech giant FIS has adopted the subscription model that has proven popular in selling everything from wine to digital media to diapers. The Florida-based company launched a subscription core banking solution today called ClearEdge.

ClearEdge is geared specifically to serve community banks and offers a bundle of technologies to help them modernize their operations and provide a better customer experience. The flat-fee, month-to-month subscription model doesn’t require lengthy terms and it eliminates liquidated damages and exclusivity requirements.

“We are committed to making it as easy as possible for our qualifying community bank clients to access the advanced technology they need to offer modern, differentiated products and services to their customers,” said Head of Global Core and Channels, Americas at FIS Rob Lee. “ClearEdge takes that commitment to the next level with a powerful offering that we believe will be a game-changer for many community banks.”

“The ability to bundle solutions relative to our business needs creates the opportunity for us to be more creative and flexible while better controlling our back-office expense,” said John Dickson, chief operations officer at Coastal Community Bank. “Plus, it just makes sense in today’s volatile market.”

As the bank-fintech partnership ecosystem strengthens and the uncertainty of the COVID-19 economic environment persists, we can expect to see more subscription-type models from tech providers. The increased flexibility, combined with the ability to pick-and-choose solutions that are tailored to each individual organization, is a model that is better suited to modern banking requirements.

The following is a guest post by Borys Pikalov Head of Analytics and Cofounder at Stobox.

One of the greatest challenges in fintech is reaching the unbanked. Accessing poor communities is operationally complicated and their use of financial services is very limited.

Microfinancing institutions are only a partial solution and traditional loans do not work as an investment vehicle because they are risky for both parties: banks don’t want to give, and poor don’t want to take. To solve this puzzle we may use two creative concepts from financial engineering.

Individual investment contract

Instead of taking a loan, people promise part of their future income in exchange for money. This reduces the risk for farmers in case they cannot pay off the debt. This is already being practiced when corporations provide education grants to poor students in exchange for future employment.

Loan securitization

Instead of taking a single loan from banks, real estate developers issue debt securities and sell them to many institutions. Thus, the loan is divided into many small parts that may be traded on a secondary market, which spreads the risk for parties giving the credit. For conventional real estate loans, the maximum debt-to-value ratio is ~60%, while for securitized loans it is ~90%, which means that 50% higher risk is acceptable.

Personal securities

Combining these two concepts we arrive at personal securities – individual investment contracts issued in the form of securities that can be divided into small parts and traded on a secondary market. There is already an example of a personal securities offering in use: a software developer offered a part of his future income in order to move to Silicon Valley.

The use of personal securities can solve the risk puzzle of investing in poor communities. However, there are a number of practical problems to be solved in order for personal securities to be an efficient solution.

First of all, personal securities should be powered by proper technology. Offering many securities to many investors in dozens of different countries requires robust and scalable infrastructure. Blockchain technology is widely considered suitable for these purposes. In the last few years, providers of securities tokenization made serious progress and now enable convenient mass operations with securities. For example, the blockchain was used to reduce the entry threshold in a $22 million venture fund by 2,0000 times– from $1,000,000 to $500.

Another problem is the operational complexity. Using personal securities would require reaching poor communities, doing the legal groundwork of signing investment contracts, choosing investment opportunities, and gathering and distributing income. This requires wide collaboration between existing banking providers, governments, nonprofits, and startups.

A solution may be to organize everything as an investment fund that would issue securities to investors worldwide and use the proceeds to organize the investment process and do the investment itself. Pooling investment into funds can further reduce the risk for investors. It is better to do pilot projects to test the best structures.

The next big investment opportunity

Giving money to poor communities is the next big investment opportunity. It would not only directly benefit investors but also all businesses that can sell to poor communities. It can vastly improve the financial outcomes of developing countries. Most importantly, it can assist in finally ending extreme poverty and providing people with a dignified life.

Borys Pikalov is Cofounder and Head of Business Analytics at Stobox, an award-winning advisory and technology company in the field of securities tokenization. Pikalov has done 2500+ hours of research in the digital securities industry. Co-author of the book “How to Attract Investments with STO: A Practical Guide”. He is currently advising the government of Ukraine about developing an ecosystem for virtual assets.

Earned wage access startup PayActivclosed $100 million today for its technology that helps companies offer their employees their pay on a daily basis rather than wait for their bi-weekly paycheck.

The Series C round was led by Eldridge and includes existing investors Generation Partners and the Ziegler Link•Age Fund II. The investment brings PayActiv’s total funding to $134 million.

The company will use the funds to expand its client base, which currently consists of 1,400+ businesses and organizations representing more than four million employees. Walmart, Wayfair, and Ibex Global are some of the major employers in PayActiv’s portfolio.

“American families are facing more financial stress than they have in generations,” said PayActiv CEO and Co-Founder Safwan Shah. “The timing gap between work and wages is the main reason workers get hit with punitive late fees, overdraft fees and other penalties. Cumulatively, these fees reduce wages by seven percent every month. The PayActiv platform is the only system where everyone wins: employers lift worker morale with little to no cost and huge dividends; employees get wages when they actually need them most; and cash re-enters the economy faster, making communities financially healthier.”

PayActiv was founded in 2011 and has emerged as a major financial wellness tool for employers. In addition to offering flexibility around how frequently employees receive payment, PayActiv also gives employees multiple options of how they receive payment. Workers can opt for direct cash pickup, a PayActiv prepaid card, an instant Visa or Mastercard debit card load, an ACH payment, or use their wages to pay bills, make purchases on Amazon, or purchase rides on Uber.

The company also offers financial wellness and planning tools that help employees to save, budget, and manage their money. Additionally, PayActiv announced today that it will offer employers a retirement benefit in partnership with Security Benefit, a retirement services provider based in Kansas.

Demand for earned wage access tools are on the rise, especially in today’s post-COVID economy. Sending employees their paychecks on a daily basis can help them avoid overdraft fees and high interest financing options such as payday loans and credit card debt.

“The future of pay is not a two-week cycle,” said Eldridge Co-founder, Chairman, and CEO Todd Boehly. “By simply giving people access to their wages as they earn them, PayActiv increases the velocity of money, stimulating the economy and serving employers and employees by driving costs down and efficiencies up.”

Describing the opportunity to use AI to create tools and solutions that make society better off, Pablos Holman (pictured right) said, “we get the chance to work for the humans yet to come.”

I like the way of looking at a controversial technology in such a positive light. Instead of focusing on the potential of AI to displace us at our jobs or make our lives unfair in some ways, maybe it is better to examine how we can use AI to craft products, technologies, and services that make our world better to live in.

To do this we need to ask ourselves and the community we work in, “All of this technology is in our hands, what do we want to accomplish with it?” It’s important to ask questions like these in the fintech sector, so that the industry can control how we use new technologies such as AI. As Holman puts it, “Speculate about the possibilities, focus on the positives.”

Holman is a hacker, inventor, entrepreneur, and technology futurist who is on a quest to solve the world’s problems through the innovation of technology. He will be the keynote speaker kicking off FinovateFall on September 14, offering his thoughts on innovating in the post-COVID landscape.

He is certainly a speaker you won’t want to miss. Holman has helped build spaceships; the world’s smallest PC; artificial intelligence agent systems; and the Hackerbot, a robot that can steal passwords on a Wi-Fi network. He is a world-renowned expert in the fast moving 3D printing space, and is currently working on printing the food of the future among other things.

Holman will discuss some of the invention projects under way at the Intellectual Ventures Lab, and their efforts to create an Invention Capital market. He will also be showing off some of the super powers that hackers possess.

FinovateFall Digital will run September 14 through 18 and will be broadcast live in Eastern Standard time. There’s still time to register (at a discount!) so take advantage and book your ticket today.

Have you ever heard of open-banking-infrastructure-as-a-service? American Express has, and it has tapped U.K.-based Yapily as the provider.

The open banking infrastructure company has signed an agreement with American Express to take the financial service giant’s open banking payment initiation product, Pay with Bank Transfer, to select European markets. Yapily’s API will enable Amex’s end users to complete a payment without being redirected to a different channel or website.

Pay with Bank Transfer is self-explanatory– it leverages open banking to enable users to transact via bank transfer. The payment method uses biometric authentication and instant payment APIs for faster, more simple, and secure payments.

“The partnership is the first real step to bringing open banking payments to everyone across Europe and the U.K.,” said Yapily CEO and founder Stefano Vaccino. “Now, a significant number of international merchants will finally be able to access, and benefit from, an open banking API.”

Yapily was founded in 2017 to help financial service providers leverage the open banking opportunity by connecting them with banks. The company enables its clients to access data in 15 countries across Europe, and at more than 180 financial institutions. Yapily has raised $18.4 million.

Mortgagetech has historically been one of the last sectors of fintech to see innovation. However, with digitization en vogue because of COVID-19, there has been an uptick in interest in companies looking to make closing on a home mortgage easier.

As evidence, U.S.-based Blend is gaining attention today for a fresh round of funding and a new valuation. The company landed $75 million in Series F funding, bringing its total raised to $365 million and increasing its valuation to almost $1.7 billion.

The round was led by Canapi Ventures. Existing investors Temasek, General Atlantic, 8VC, Greylock, and Emergence also participated.

“Financial institutions have traditionally taken time to modernize legacy systems, but digital is now table stakes. Shelter in place and social distancing mandates have forced banks and other lenders to accelerate digital transformation plans from years to months,” said Jeffrey Reitman, a partner at Canapi Ventures. “Blend is at the forefront of this innovation, offering flexible digital solutions to help lenders like Wells Fargo, U.S. Bank, Truist, M&T Bank, and other key regional banking institutions meet their accelerated timelines and their customers’ changing needs.”

Blend, a banking-as-a-service company that aims to create a “less stressful, more accessible lending experience,” will use the funds to expand its products and broaden its strategy. Specifically, Blend will likely bolster the consumer banking and auto loans offerings it launched late last year.

“Our goal is to deliver software that gives lenders the flexibility to meet the evolving needs of consumers,” said Marc Greenberg, head of finance at Blend. “We’re committed to being the digital layer that enables millions of people to gain access to the capital they need, while helping our customers be there as trusted advisors for every milestone in a consumer’s financial journey.”

Among Blend’s new launches this year are a digital closing solution for mortgages and home equity loans, a mobile app for loan officers, and new reporting tools for lenders. Since the start of 2020, Blend has brought on 130+ new employees and helped its bank clients process more than $771 billion in consumer loans– over $3.5 billion each day.

Adding to the big-bank-to-big-tech partnerships announced in recent weeks, Standard Charteredsecured a three-year partnership with Microsoft today.

The bank will leverage Microsoft to take a multicloud approach that will port its significant applications to the cloud. Specifically, Standard Chartered is planning to make its core banking and trading systems and digital ventures such as virtual banking and banking as-a-service cloud-based by 2025.

“Cloud is a cornerstone of Standard Chartered’s strategy to meet the present and future banking needs of our clients,” said Group Chief Information Officer of Standard Chartered, Michael Gorriz. “Using cloud services improves our ability to be agile and innovative, while increasing our operational efficiency and resilience. As disruption in the financial industry continues, we can focus on client benefits by deploying our solutions quicker and allowing for faster integration of new business models and partners.” Gorriz added that today’s partnership is a “major milestone” in Standard Chartered’s journey to become cloud-first.

Standard Chartered will pilot the launch by moving its trade finance systems to Microsoft Azure. The move is expected to facilitate cross-border trade at the bank.

The partnership extends to Microsoft’s workplace tools. Standard Chartered’s 84,000 employees will be working on Office 365 and communicating via Microsoft Teams.

This news comes during a time of widespread digital transformation across the banking sector. Banks and fintechs are seeking to move their operations to the cloud to update their infrastructure and create a better customer experience. There are two factors driving this change: the global health crisis that has moved many in-person interactions to online channels and the rise of competition from challenger banks.

“Cloud computing is an enabler for financial institutions to modernize their infrastructure and systems, to gain the agility they need to respond to competitive pressures, regulatory environments and customer demand,” said Bill Borden, Corporate Vice President of Worldwide Financial Services at Microsoft. “We are committed to helping Standard Chartered Bank in its ongoing digital transformation journey as it strives to address evolving customer needs and build the next generation of banking experiences.”