This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Australia-based financial comparison website Mozo has agreed to be acquired by British Media company Future PLC.

Future anticipates the purchase will fuel its global growth by creating a new revenue stream, adding a new financial services content arm in Australia, and growing Mozo’s market share.

Founded in 2008, Mozo is a B2C site that helps consumers compare offers on home loans, credit cards, and personal loans, as well as compare banking and insurance products. In total, the company compares more than 1,800 products from over 200 banking, insurance, and energy providers.

Monzo is also known for its personal finance resources. The company offers financial calculators and creates content to help guide readers through financial decisions and build their awareness of the finance world.

“We’re delighted to be adding Mozo to the Future family,” said Future CEO Zillah Byng-Thorne. “We are seeing the increasing convergence of content and price comparison and this acquisition supports our global growth ambition in this area.”

Mozo has raised $1.4 million (£1 million) via one round of funding. The company’s team of 45 employees works out of Sydney, Australia.

Cryptocurrencies have dominated the fintech headlines this week- from Mastercardagreeing to allow merchants to accept payments in cryptocurrencies to BNY Mellon’s announcement that it will begin custody of cryptocurrencies.

Today, after bitcoin reached an all-time high of over $48,000, marketing services company Kasasaunveiled plans to help its bank and credit union clients provide bitcoin wallets to their consumers.

The new capabilities will be powered by a partnership with New York Digital Investment Group (NYDIG), a technology and financial services firm dedicated to Bitcoin. The collaboration will help Kasasa’s bank clients stay ahead of the rapidly growing bitcoin adoption.

“Clearly, Bitcoin is here to stay, and consumers are demanding that Bitcoin offerings be made through their trusted financial institutions,” said Kasasa CIO John Waupsh. “With this new partnership, we’re looking across the product and services that Kasasa currently offers, as well as future product and service ideas. With NYDIG we can evaluate new offerings such as a buy-sell-hold wallet while also incorporating Bitcoin into our core rewards business.”

This partnership will be a major selling point for Kasasa, especially as consumer interest in cryptocurrencies rise. According to NYDIG, more than 22% of U.S. adults over the age of 18 own Bitcoin today.

This interest, combined with the creation of formal regulation like the OCC’s recent ruling that banks may use stablecoins for payment facilitation, is bringing cyrptocurrencies into the forefront of banks’ agendas. With today’s partnership, Kasasa is better positioned to help small financial institutions compete with larger players when it comes to cryptocurrencies.

If you have the WiFi, we’ll bring the content. This month, we’re hosting two FinovateFocus events– Connect and Roundtable. Both events are free to attend and will take place on February 25 from 9 a.m. to 11:45 a.m. Central Standard Time.

Register for these all-digital micro events and you’ll not only have access to great content, but you’ll also have the opportunity to check out the unique format and full roster of discussions and networking.

This month’s discussions will focus on the digital user experience. Now more than ever, your digital user experience is what your customers see; it shapes how they view your organization. Our dive into digital will help inform how you can leverage your UX to increase sales, create happy customers, and increase operational efficiency.

Here’s what to expect at each event:

FinovateFocus Connect

This event maximizes your time by bringing you nine presentations and nine meetings, all within the span of an hour. The platform will alternate between three-minute presentations and three-minute meetings, which are pre-assigned based on common interests.

FinovateFocus Roundtable

This discussion-based event includes your choice of two moderated, 30-minute roundtables with 15 minutes of networking before and after each roundtable conversation. To encourage engagement, each roundtable is limited to eight participants each.

Roundtable discussions for this month’s event include:

Earning customer trust in the digital age

Future of payments –are we turning into a cashless society?

Effective customer acquisition, engagement, and retention – the Experience Age

Boosting CX in banking with AI – conversation banking: exploring back-end technologies

Authentication, biometrics, and digital identity in digitized society

Chatbots, AI, automation as a platform for revolutionizing the CX

Personalization and customization with data in the banking and payments industry

Insights into how to support financial futures for customers in a post-COVID-19 world

Customer Service NOW

Video banking as a preferred means of customer communication

What do customers want – Meeting customer needs

APIs and Open Banking – Putting the customer in the driver’s seat

FinovateFocus starts on February 25. The Connect portion will run from 9 am to 10 am Central time while the Roundtable portion will run from 10:15 am to 10:45 am Central time. Both events are free to attend, so sign up early.

While you’re signing up, check out the deals for FinovateFocus sessions in March, April, May, and June available on the registration page. Sign up for a single event or purchase a bundle package to save.

Here are the topics we have planned for the months ahead:

Data analytics firm Moody’s announced plans to acquire data insights company Cortera this week. Terms of the deal, which is expected to close in the first quarter of this year, are undisclosed.

Moody’s anticipates the purchase will enhance its risk assessment capabilities. The move will also significantly extend Moody’s coverage in the SME market– the segment that serves as Cortera’s focus.

“Cortera plays an important role in helping businesses understand each other,” said President of Moody’s Analytics Stephen Tulenko. “Our customers will be able to leverage Cortera’s extensive information on small businesses with Moody’s proprietary analytic tools to make better decisions.”

Cortera was founded in 1993 and provides credit data and workflow solutions on North America-based public and private organizations. The Florida-based company maintains a database of credit information on more than 36 million businesses across the continent.

Cortera sources this data from thousands of resources and scrubs it using AI. As a result, the company is able to provide analytics, reports, and monitoring services to help inform businesses’ decisions.

Specifically, the acquisition will augment Moody’s Orbis database of private company information and enhance its KYC, commercial lending, and supply chain solutions.

Moody’s was founded in 1900 and provides data, analytical solutions, and insights to help businesses identify opportunities and manage risk. The company employs more than 11,000 people across 40+ countries. Headquartered in New York City, Moody’s is publicly traded on the NYSE under the ticker MCO. The company has a market capitalization of $52 billion.

Klarna is taking its Buy Now, Pay Later (BNPL) platform to a logical next step. The Sweden-based company announced today it will launch a bank account offering in Germany.

This move makes Klarna the first BNPL firm to make such a move. The company will now compete with the growing roster of digital banks in Germany, including N26 and Tomorrow.

Users will receive a Visa debit card, which is available in two colors, and will have tools on the app to track, manage, budget, and analyze their spending habits. Klarna will also reimburse users for two global ATM transactions per month.

“Our focus is to provide a superior shopping experience to our consumers at the intersection of retail and banking,” said Klarna CEO Sebastian Siemiatkowski. “And we know that there’s still massive room for improvement to the way many people bank and save their money today. Users are demanding more seamless, intuitive and transparent services to meet their daily needs, but many banks still do not cater for this.”

As Siemiatkowski points out, Klarna banking will be useful for “bundling shopping and banking in one app.” However, it is difficult to see the extra value a Klarna bank account will bring to users who aren’t big on shopping. N26 touts an integration with Transferwise for easy and inexpensive foreign money transfers and Tomorrow differentiates itself with a positive approach to sustainability and social causes. Klarna, in contrast, makes shopping a more embedded experience. This isn’t necessarily a positive attribute for one’s finances.

To counteract this “spend, spend, spend” mentality, Klarna said it has plans to add savings goals to the banking app, a feature that is already available in Sweden.

A pilot of Klarna’s bank account will initially be available to the company’s “most loyal” users and will roll out to all Germany-based users “in the coming months.”

The adoption of financial technology continues to rise in general. This progression over time means that not only are there more platforms and use cases for fintech, but companies are also becoming more acclimatised to integrating them into their business plans.

Historically, insurance as a sector has been slower to adopt the latest in technology, and the case of financial technology is no expectation. Often pictured as huge swarms of suited figures in high rise buildings, in fact, the insurance industry is populated with businesses of varying sizes and diverse specialities.

As such, we can see a discrepancy in the adoption of the latest fintech solutions within insurance. The largest corporations offering simpler policies benefit from enhanced budgets and capacity, leaving them in good standing to adopt the solutions internally. The wealth of data available to these businesses also makes the benefits to them greater. Conversely, smaller providers and brokerages offering more bespoke policies have less faith in the ability of fintech to actually make their lives easier, and often with a lower ceiling of reward.

The current adoption of fintech in insurance

Adopting the advancement of technology at policyholder level is a clear example of how larger insurance companies are utilising fintech at the moment. The Internet of Things allows more devices than ever to report data. In the case of car insurance, policyholders are offered the use of an application with the incentive to potentially reduce premiums. This allows increased telemetrics data which can then feed into a better understanding of risk and necessary premium and coverage levels.

This adoption of policy level technology is also seen by some insurers within the health and life insurance sector. Increasingly, a consumer may be offered a device, such as a smartwatch, which not only incentivises the person to take out the policy but also gives opportunities to better understand the data behind claimants for insurance providers.

While consumer insurance is most commonly synonymous with fintech, there is an emerging case for use in the commercial sector. The utilisation of smart sensor technology for flood risks coverage is becoming more common when providing insurance for businesses. The lower cost of such setups is certainly a mitigating factor, and also allows for simpler types of coverage that reduce claim payment periods.

The key differentiator could be considered the gathering of data for companies of differing sizes in the insurance sector. At present, large providers can gain a better understanding of their clientele, allowing them to adjust policy requirements to minimise risks over time.

However, the use of existing customer data has been adopted more recently by insurance companies of all sizes. Once a policyholder has taken out a policy, the benefits of automated touchpoints have become valuable to even the smaller companies. With the use of data such as policy renewal dates, sequences can easily be created to keep in touch with customers and introduce the idea of relevant cross-sell opportunities at an early stage as they come up to renewal. Software itself is usually fairly intuitive. Platforms such as Brief Your Market remove the intense training previously required to run campaigns effectively internally.

What is slowing the adoption of fintech?

While fintech will surely become even more intrinsic to the insurance sector in the future, there can be no doubt that adoption rates will continue to be slow for most. That adoption is not from a lack of knowledge; 74% of respondents to a 2014 survey saw fintech innovations as a challenge for the insurance sector.

Interestingly that same survey found the insurance industry placed a higher than average value to fintech, compared to other financial sectors. This shows the constraints on insurance companies aren’t as clear cut as they may seem. Fears of reducing margins down even further and of moving from a focus on short term strategies to longer-term ones are likely constraints.

Furthermore, the adoption within the more specialist arms of the insurance industry will be understandably slower to adopt fintech at all levels. The nature of specialist insurance brokers hinges on their speciality of providing a human service for those that require a particular level of coverage or have constraints preventing traditional policies. Utilising fintech could prevent brokers from providing this high level of service.

Within such sectors, it’s likely that the primary use of fintech will continue to be more for leveraging current customer data and refining internal operations to save time.

What’s in the future for fintech & insurance?

Naturally, the unstable financial situation brought on by COVID-19 will likely lead to slightly lower adoption rates in 2021. Whilst the application of AI and increasing understanding of policy risks may continue to be alluring to providers, it’s highly unlikely that this will accelerate given the impact of the pandemic on the industry.

Moving beyond the ripple effect of COVID-19 there is no doubt that fintech will continue to grow, and increasingly so within the smaller providers and brokers. Likely, platforms will develop that will be more focussed on partnerships with these companies, rather than the internal adoption seen by the largest companies with the highest budgets.

Paul Monaco is Client Director at Focus Oxford Risk Management and specializes in the advice and arrangement of specialist business insurance and risk management to the Life Science, Medical Device, Scientific Research and Technology Sectors from new business start-ups through to PLCs.

AI marketing expert Micronotes recently launched a refinancing tool that will help consumers reorganize their debt, while enabling banks to lower their borrowing costs and boost customer retention.

The new tool builds on Micronotes’ ReFi solution it launched last June. The credit marketing automation suite enables banks to leverage AI to help their clients automatically identify refinancing opportunities for a range of consumer debt, including auto loans, personal loans, student loans, credit card debt, and mortgages.

With today’s advancement of ReFi, Micronotes is teaming up with Experian to leverage the firm’s database of consumer credit profiles. Experian will compare the bank’s current lending criteria to the consumer’s credit profile, and then synthetically refinance the customer’s existing debt held elsewhere while identifying other refinancing opportunities.

“We’re thrilled to partner with Experian to leverage artificial intelligence and data to help consumers lower their borrowing costs,” said Devon Kinkead, founder and CEO of Micronotes. “With an estimated $2 trillion in mispriced debt, during an era of persistently low interest rates, we help digital banking customers see where they’re overpaying interest that can be refinanced with a lender they know and trust — their primary financial institution.”

Micronotes’ personalization expertise comes in via the customer communication piece. The company will send the customer a message in the digital banking channel that informs them of the potential savings. Using Micronotes’ technology, the customer can respond to the message using preset, customizable quick-response buttons that range from “remind me later” to “chat with a banker.”

This quick-response messaging system is Micronotes’ bread and butter. The company was founded in 2008 to help financial institutions start conversations with their customers in a non-invasive way. At the company’s most recent Finovate appearance, FinovateSpring 2013, Micronotes showed off its cross-sell feature that uses predictive analytics to bring the branch sales process into the digital channel.

Headquartered in Boston, Massachusetts, Micronotes has raised $12.2 million.

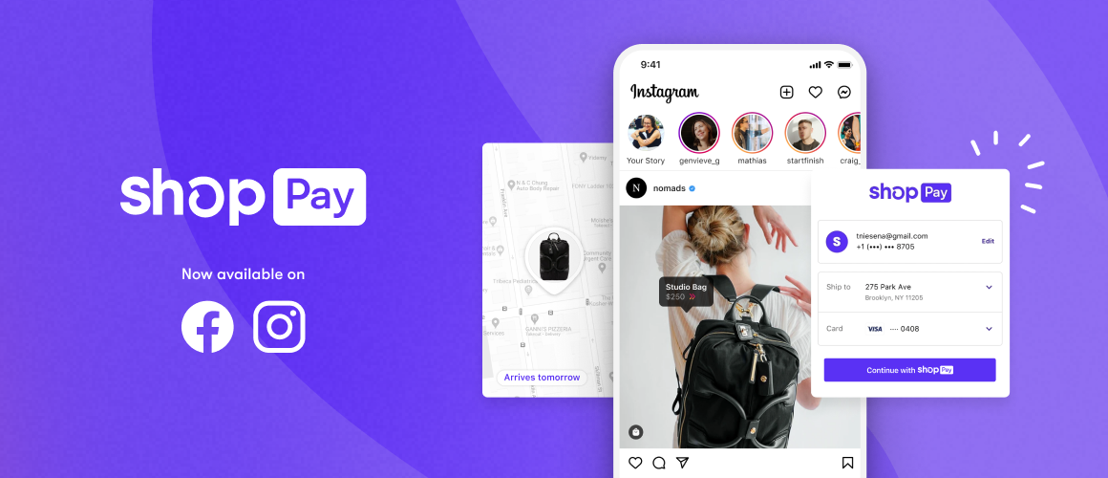

As social commerce rises, e-commerce platform Shopify is getting in on where the action is happening. The company announced today it is bringing its Shop Pay checkout and payment processing system to Instagram users and Facebook Shops.

This builds on the existing payment methods available to these Facebook-owned social platforms. Previously, shoppers had the option to either pay with PayPal or manually enter their payment card credentials.

Shop Pay, on the other hand, stores users’ payment card and shipping information to make the embedded payment experience as seamless as possible for the end customer. Prior to today, Shop Pay was only available to Shopify’s e-commerce store clients, including brands such as Allbirds, Kith, Beyond Yoga, and Jonathan Adler.

Shop Pay has 60 million users and last year helped buyers complete more than 137 million orders. This is small compared to PayPal’s 377 million active users. Shopify, however, is aiming to gain an edge by targeting the millennial customer base by offering carbon offset options that allow merchants and customers to offset the carbon emissions of their deliveries.

“People are embracing social platforms not only for connection, but for commerce,” said Carl Rivera, General Manager of Shop. “Making Shop Pay available outside of Shopify for the first time means even more shoppers can use the fastest and best checkout on the Internet.”

As for what’s next in the Shopify-Facebook tie-up, Rivera said to expect more collaboration in the future. He added, “…we’ll continue to work with Facebook to bring a number of Shopify services and products to these platforms to make social selling so much better”

The ecommerce tools are available for Instagram users today and will be available for U.S. Facebook Shops in the coming weeks.

The decentralized finance (DeFi) conversation started to pick up about a year ago. Today, we’re starting to see this once-fringe topic emerge as a mainstream conversation in fintech.

In fact, now that DeFi has become a reality, it’s not something that’s going away any time soon. The advent of cryptocurrencies enabled consumers to transfer money between parties without relying on a traditional bank. DeFi takes this power the next level.

These added capabilities are what have the potential to take cryptocurrencies from a speculative device to a useful tool. But while this is a reality for some, it is still a concept on paper for most. So why am I paying attention to DeFi now, while it’s still in its infancy?

It’s more than an idea

As mentioned above, DeFi has moved from the concept of “an interesting idea” into a concrete, value-added financial tool. Leveraging the power of smart contracts, DeFi allows users to lend, earn interest, and claim insurance. It can also be used to prove identity, assist with underwriting, AML and KYC compliance, and more.

Because of these capabilities, the use of DeFi is becoming more popular. The following graphic from DeFi Pulse shows the total U.S. dollar value locked in DeFi. The graph shows DeFi starting to take off in July of last year and rise exponentially. Today, the total locked value is more than $35.9 billion.

With this growth, we can expect to see more projects and use cases launch as DeFi emerges from an idea to a new reality.

DeFi will change banking as we know it

Today’s traditional banking system relies on centralized control. But one of the key aspects of DeFi is that it operates without an intermediary. That is, users can complete banking activities without a central governmental authority, a bank, or even a company setting rules, governing, and regulating activity.

Instead of this central control, DeFi leverages smart contracts that use “oracles,” or services that inform smart contracts of external data so that it can execute its purpose based on that data. As an example, a smart contract for flood insurance might rely on rain gauges to determine whether or not to pay out insurance claims to homeowners living in a certain area.

This key difference will change how consumers shop for financial services. Instead of hinging on trusting an institution, the consumer’s decision will rely on how smart they think the smart contract is, and whether or not they trust the oracles the smart contract uses.

It will transform the industry for the better

While DeFi is a little bit intimidating, it has the ability to change the financial world for the better. It is scalable and programmable, and is therefore well-suited for growth. In addition, it is immutable. That is, it is tamper-proof and cannot be changed or hacked. And transaction details are transparent; DeFi protocols are built with open source code and can be viewed by anyone.

The final, and perhaps most notable, aspect of DeFi is that it is permissionless. This means that anyone with a crypto wallet and an internet connection can participate in the DeFi economy. There is no minimum balance requirement and, because it doesn’t revolve around a central government, there are no geographic limitations.

Two weeks after announcing its purchase of Cardtronics, fintech hardware giant NCR is acquiringTerafina, a company known for its digital account opening and onboarding tools.

Financial terms of the agreement were not disclosed.

NCR will tap Terafina’s expertise to expand NCR’s sales and marketing capabilities in its Digital First Banking Platform. The offering, which can be tailored to fit institutions ranging in size from large banks to community banks and credit unions, provides an API-led approach to digital banking that can be hosted or deployed on-premise to help banks lower costs and speed up their innovation cycle.

Last year increased the urgency for financial services companies of all kinds to improve their digital customer experiences. Founded in 2014, Terafina suits this need. The company offers a software-as-a-service solution that offers digital onboarding tools and helps banks and credit unions synchronize their branch, call center, and digital operations to provide a consistent user experience across channels.

At FinovateSpring 2019, Terafina Founder and CEO Meheriar Hasan showcased the company’s digital sales platform that helps banks address the needs of their small business clients.

“Digital Banking is a key aspect of the NCR-as-a-Service strategy we laid out at Investor Day in December,” said NCR CEO Michael D. Hayford. “Terafina has been a partner of ours and is already up and running, integrated with our Digital Banking platform. We know this adds value for our clients by making digital account sales, marketing and onboarding easier, so they can provide a superior experience for customers.”

Today’s deal marks NCR’s 29th acquisition since it was founded in 1884. NCR’s purchase of Terafina fits with the company’s strategy to purchase early stage companies to boost its product capabilities and enhance its leadership.

NCR is headquartered in Atlanta, Georgia, and counts 36,000 employees across the globe. The company is listed on the New York Stock Exchange under the ticker NCR and has a market capitalization of $4.81 billion.

Digital corporate banking solutions company CoCoNet Softwareannounced a new CEO today. Mark Lohweber is now heading up the company, taking the reins from former CEO Björn Hassing, who will transition to serve as the company’s CTO.

Lohweber will head up CoCoNet’s board of directors, which also consists of Hassing and company CFO and COO Axel B. Wiethoff.

“In corporate banking, many banks have great potential for process and portfolio optimisation through digitalisation”, said Lohweber. “CoCoNet already offers outstanding solutions in this area. That is why I am very happy, together with Axel, Björn and the entire CoCoNet team, to be a strong partner in digitalisation for the banking sector.

Lohweber comes to CoCoNet after leading the banking business unit at IT service management company adesso for 13 years.

Founded in 1984, CoCoNet provides digital banking solutions to banks, with a customer lineup including Citi, GarantiBank, HSBC, ING, JPMorgan, KBC, and UniCredit.

At FinovateWest 2020, the company demonstrated its digital onboarding solution. The solution is tailored to corporate customers and is designed to suit the complex needs of this segment.

Investment platform Stashannounced a new round of financing today. The $125 million Series G round boosts the company’s total funding to over $427 million.

Eldridge led the round, which received additional funding from new and existing investors, including Owl Ventures, funds advised by T. Rowe Price Associates, Goodwater Capital, Entree Capital, and others.

The funding comes after a year of record growth for Stash, which was founded in 2015. Last year, the New York-based company saw a 100% increase in account openings. It now has five million customers and $2.5 billion in assets under management. Fueling this increase was the boost in automated deposits; Stash reported a 50% increase in the number of customers automating their investments last year.

Stash’s investment platform democratizes long-term investing by making the process easier and more affordable. “We believe in tried and tested principles of regular, long-term, and balanced investing as the key to building wealth. We therefore built Stash to make diversified investing easy, affordable and accessible, backed by personalized advice and accessible education—in order to avoid the pitfalls of short-term speculation and day-trading,” said Stash Co-Founder and CEO Brandon Krieg. “This new round of funding enables us to take this mission to millions more Americans.”

Stash’s newest upcoming product, Smart Portfolios, helps customers build long-term, diversified portfolios that are fully managed by Stash. The new offering is made for users who want to invest, but don’t know where to start. To keep things simple, Stash uses a subscription model instead of charging fees based on portfolio size. The Smart Portfolios product is included in Stash’s Growth and Plus subscription plans, which cost $3 per month and $9 per month, respectively.