This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

CB Insights shared its State of Fintech Q2 2023 report last month. The top takeaways? Fintech funding continues to take a hit, with the report noting that both funding and deals globally have retreated to “levels not seen since 2017.”

But wait, there’s more. Mega-round funding, deals valued at $100 million or more, fell to a six-year low. And payments – which were memorably referred to by the VCs on our Smart Money Power Panel at FinovateFall last year as “the gift that keeps on giving” – stopped giving. CB Insights reports that funding for payments-related companies fell 75% quarter over quarter. It was the largest decrease for any fintech sector.

What about upsides? The report noted increases in fintech funding in Latin America and the Caribbean, the only region to see significant gains. CB Insights also highlighted the fact that the five exits in the quarter all came from fintechs based outside of the U.S.

Read the whole report. There are a number of interesting observations, some of which give some reason for optimism in the second half of the year. For one, early-stage companies dominated deal volume in Q2 2023. The strength of fintech funding in Latin America, mentioned above, was also a promising sign. Some of this deal-making involved cryptocurrency and DeFi related firms – and geographies like the Cayman Islands that are outside traditional Latin American fintech powerhouses Mexico and Brazil. But much of the investment in Latin America was driven by strong trends like digitization and financial inclusion. Investors have also been encouraged by the success of fintechs like Brazil’s Nubank. The report also saw positives in the market for companies going public in Asia last quarter.

For more on CB Insights’ examination of fintech funding so far in 2023, also check out the firm’s Fintech Midyear Review: The Data Behind the 6 Year Low webinar released last week. Lead Fintech Analyst Anisha Kothapa puts the current fintech landscape into context, and highlights where investors see opportunity around the world – and why.

“I think some of the biggest drivers of capital being invested in (Latin America) is due to, one, financial inclusion,” Kothapa explained. “There are many unbanked and underbanked people in Latin America that need innovative financial solutions. The second is that the region has seen rapid digital adoption, especially with the use of smart phones, and growing internet connectivity. The third thing is around a more favorable regulatory environment.”

By the way, Finovate’s weekly Finovate Global column is a great source of news on fintech developments around the world. With regard to Latin America in particular, recent columns have focused on fintech innovation in Brazil and Colombia.

New York-based digital mortgage lender Better.com is going public.

The company will combine with Auora Acquisition Corporation via SPAC “on or about August 22.”

The transaction between Better and Aurora has been more than two years in the making. The companies first announced the deal in May 2021.

Time to party like its 2021? The week begins with news that digital mortgage lender Better.com’s proposal to combine with Aurora Acquisition Corporation via SPAC has secured shareholder approval. The new Better.com will go public “on or about August 22, 2023.”

When finalized, the transaction will provide the combined entity with a minimum of $550 million and as much as $750 million in new capital. The company will trade on the NASDAQ under the tickers “BETR” and “BETRW.”

Founded in 2014 by CEO Vishal Garg, Better has been trying to close its SPAC deal for years. The transaction had been extended three times since 2021, amid concerns over market conditions, financial losses, and regulatory controversies. Among the bad press Better.com dealt with during this stretch was the infamous Zoom meeting in December 2021 during which Garg announced a layoff of approximately 900 employees. The CEO and founder also allegedly admitted that the company has “probably pissed away $200 million.”

With regard to finances, Better.com reported a net loss of $888.8 million in 2022. In the first quarter of this year, the company acknowledged losses of $89.9 million. Better.com also reported a decline in the number of loans funded year-over-year. The firm funded 18,559 loans in Q1 of 2022. Better.com funded 2,347 loans in the first quarter of this year.

In one response to these challenges, the company has made significant changes to its real estate strategy. Better.com announced in June that it would begin partnering with outside agents as referral partners in its Better Real Estate subsidiary. This pivot away from in-house licensed real estate teams to this new model is designed to help the subsidiary lower costs. The company also indicated that the change will help it deal with the challenge of lower mortgage volumes. Better Real Estate, which receives a significant number of its leads from its parent company’s mortgage operation, provided Better.com with $23.1 million in revenue in 2022.

Better has also introduced new solutions along its main line of business. The company began the year with the launch of One Day Mortgage. The new offering f gives borrowers a mortgage commitment letter within 24 hours of applying for a loan.

The Reserve Bank of India (RBI) announced a number of new fintech initiatives this week. Among the more interesting was a plan to bring AI-powered, conversational payments to the country’s UPI (Unified Payments Interface) system.

The National Payments Corporation of India (NPCI) launched the platform in 2016. Today, UPI has more than 300 million monthly active users in India. There are also 500 million merchants who use the platform to accept payments. With UPI, users can link multiple bank accounts to a single mobile app, and then make real-time, P2P transactions via mobile device or smartphone. Analysts expect daily transaction volume on UPI to reach one billion by 2026-2027.

The proposal would enable users to initiate payments from within both chat and messaging apps. “As Artificial Intelligence (AI) is becoming increasingly integrated into the digital economy, conversational instructions hold immense potential in enhancing ease of use, and consequently reach, of the UPI system,” the RBI press release read. “It is, therefore, proposed to launch an innovative payment mode viz., ‘Conversational Payments’ on UPI, that will enable users to engage in a conversation with an AI-powered system to initiate and complete transactions in a safe and secure environment.”

Conversational Payments will be available initially in Hindi and English, with other Indian languages to be added. The technology will be available via smartphones and feature phone-based UPI channels, which the Reserve Bank of India believes will lead to broader adoption and further financial inclusion. To this end, the RBI has also proposed to bring Near Field Communications (NFC) technology to its UPI-Lite on-device wallet. Launched last fall, UPI-Lite is designed to facilitate small value transactions and now processes more than ten million transactions a month.

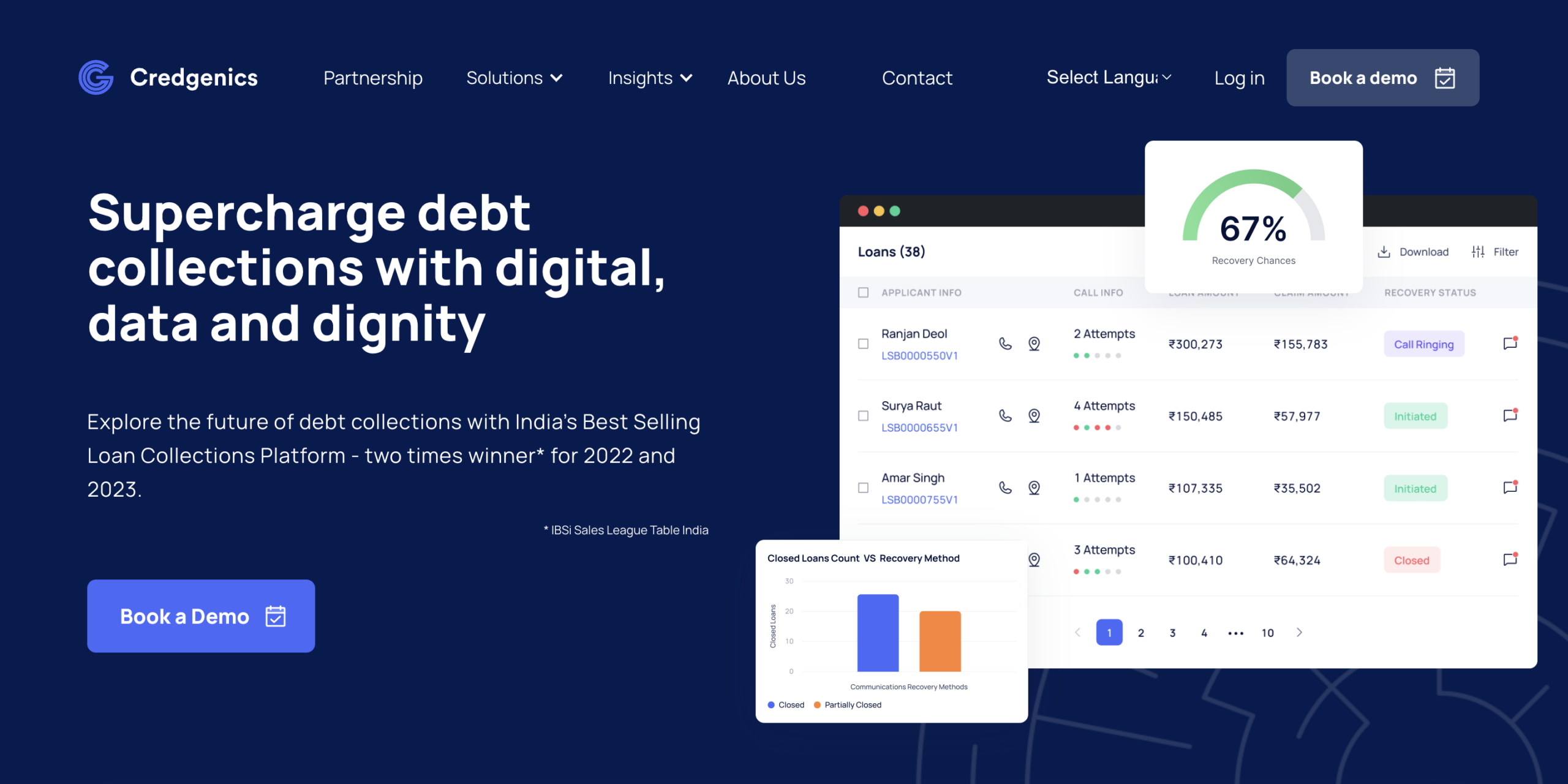

An investment of $50 million has given Indian debt collection software-as-a-service (SaaS) platform Credgenics a valuation of $340 million. Accel, Westbridge Capital, Tanglin Ventures, Beams Fintech Fund, and other strategic investors participated in the Series B round.

Company co-founder and CEO Rishabh Goel said that the capital would do more than just help the firm expand into new markets. “This funding not only accelerates our growth, but also enables us to make a meaningful impact on the economic landscape of countries, unlocking new opportunities for financial well-being,” Goel said.

Founded in 2019, Credgenics currently serves more than 100 private banks, non-bank financial companies, fintechs, and asset reconstruction companies. The company’s debt resolution platform provides a suite of solutions including digital collections, collections analytics, litigation management, agent performance management, and a field collections mobile app. The technology leverages AI-driven intelligent automation and machine learning to bring greater efficiency to the collections process.

Credgenics handles 11 million retail loan accounts and touched an overall loan book worth $60 billion in fiscal year 2023. The company became operationally profitable this spring. This summer, Credegnics announced a partnership with Indonesia-based lender Investree. The company also was recognized as the Best Selling Loan Collections Platform in IBS Intelligence India Sales League Table for the second year in a row.

Minister of State for Corporate Affairs (independent charge) Rao Inderjit Singh provided the report to Parliament as part of the Startup India initiative. Launched by the Department for Promotion of Industry and Internal Trade in 2016, this initiative establishes the criteria that confers recognition by the Department. These factors include data of incorporation, as well as revenue and profit benchmarks.

Singh pointed to the “Fintech Entity Framework” as an example of one of the actions taken by the government – in this case the International Financial Services Centres Authority (IFSCA) – to promote the country’s fintech startup ecosystem. This framework includes a comprehensive scheme of grants for startups, sandboxes, proof-of-concepts (PoC), accelerators, and more.

Singh also credited the government for the success of an initiative which streamlined beneficiary account opening and direct benefit transfers, and improved access to multiple financial services applications. The initiative is called the Pradhan Mantri Jan Dhan Yojana (PMJDY), meaning “The Prime Minister’s Public Finance Scheme,” and it set a new world record for account openings upon its launch in 2014. This spring, the initiative reached a major milestone of more than $28 billion (₹2 lakh crore) in deposits.

Here is our look at fintech innovation around the world.

FinovateFall 2023 is one month away! Our annual autumn fintech showcase returns to New York City, September 11 through September 13, for three days of live fintech demos, insightful mainstage speakers, and hours of high-quality, professional networking. Book your ticket now and take advantage of big, early-bird savings.

To whet your appetite for our upcoming event, here’s a look at the keynote speakers who will address attendees on Day One of FinovateFall this year.

Devendra Kumar Sharma, President & Chief Operating Officer, Kore.ai

Sharma leads go-to-market functions, revenue growth, client success, strategy, and cross-functional collaboration as Kore.ai President and Chief Operating Officer. At FinovateFall, he will lead a Mastermind Keynote titled “How Generative and Conversational AI is Transforming Everyday Banking.”

Tomas Chamorro-Premuzic, Author, I, Human: AI, Automation, and the Quest to Reclaim What Makes Us Unique

Chamorro-Premuzic will lead an Out of the Box Keynote address titled “ChatGPT, Generative AI & the Future for Humanity.” An international authority in people analytics, talent management, leadership development, and the Human-AI interface, he is the Chief Innovation Officer at Manpower Group.

Jody Bhagat, President of Americas, Personetics and Daniel Caplan, Director, Digital Money Management and Wealth Services, BMO Financial Group

Bhagat and Caplan will team up to deliver a Mastermind Keynote titled “Winning the Battle for Deposits.” Bhagat has deep operating experience in financial services, including managing direct channels, launching digital ventures, and leading digital transformation programs. Caplan is an experienced and agile product manager and strategist who builds winning products, experiences and strategies that deliver tangible business results.

David Porter, Managing Director, Genesys Financial Services and Sachin Tandon, Worldwide Banking Industry Strategist, AWS

Porter leads the Genesys Financial Services vertical team, having spent many years in wealth management, payments, and consumer banking at J.P. Morgan Chase. Tandon has more than 20 years of experience in financial services and consulting leadership roles at J.P. Morgan Chase, EY, Fidelity, and Accenture. Together, Porter and Tandon will provide a Mastermind Keynote titled “The Future of Customer and Employee Experience in Financial Services.”

Justin Kamerman, Chief Product Officer, and Sunil Madhu, founder and CEO, of Instnt

Kamerman has more than 20 years experience designing and building high performance distributed systems in the telecom, IPTV, identity verification, social media analytics, and IIOT industries. Founder and previously CEO and CTO of Socure, Madhu has more than 30 years of experience innovating in the identity and access management, security, governance, and risk and compliance markets. Kamerman and Madhu will team up to deliver a Mastermind Keynote titled “Zero Fraud Loss + Zero Marketing Spend = 50% More Growth.”

Greenlight Financial Technology unveiled its Greenlight Family Cash Mastercard this week.

The Greenlight Family Cash Mastercard helps teens build credit before they reach adulthood.

Headquartered in Atlanta, Georgia, Greenlight has raised more than $550 million in funding. The company has a valuation of $2.3 billion.

Greenlight Financial Technologylaunched its Greenlight Family Cash Mastercard this week. The new card fosters financial literacy by helping teens build their credit before they reach adulthood.

Available with all of Greenlight’s subscription plans, the Greenlight Family Cash Card enables families to earn up to 3% cash back on all purchases. Parents can add their teen children as authorized users on the card, and teens can track their credit card balances using the Greenlight app. At the same time parents can establish spending limits and receive real-time purchase alerts to help them monitor card activity. The addition of the Greenlight Family Cash Card means that Greenlight’s in-app financial literacy game, Level Up, now features instruction on the responsible use of credit, as well.

Greenlight subscription plans start at $4.99 a month. Other plans are available that add features such as identity theft, purchase, and phone protection (Greenlight Max for $10 a month), as well as family location sharing and crash detection (Greenlight Infinity for $15 a month). The Greenlight Family Cash Card is issued by First National Bank of Omaha.

In an interview with TechCrunch, Greenlight co-founder and CEO Tim Sheehan highlighted the company’s 3% cashback, Level Up financial literacy game, and parental controls as a trifecta that trumps offerings from other credit cards – including those that cater to families and youth. “Nobody has all three of these features,” Sheehan said.

Headquartered in Atlanta, Georgia, Greenlight was founded in 2014. The company has raised $550 million in funding, which includes a $260 million Series D round in 2021. This investment gave the fintech a valuation of $2.3 billion. The following year, Greenlight unveiled its Greenlight for Classroooms offering, a web-based financial literacy library. The library includes more than 100 animated videos, and a bank of thousands of vocabulary words and test questions. Additional features include quizzes, ideas for individual projects, discussion activities, and a teacher’s guide. Aligned with K-12 national standards, Greenlight for Classroom is available to schools, teachers, and students across the U.S. for free.

Data analytics and insights platform ForwardLane launched a new generative decision intelligence platform this week.

The new offering, EMERGE, will enable financial professionals to create and interact with client insights while keeping private data private.

ForwardLane made its Finovate debut in 2016. Nathan Stevenson is founder and CEO.

Data analytics and insights platform, ForwardLane launched a new generative decision intelligence platform called EMERGE this week. The technology will help financial services professionals deal with issues of data transparency, privacy, and security within the wealth management and insurance space.

EMERGE gives financial professionals the ability to leverage generative AI to find, create, preview, publish, and interact with new and newly-uncovered insights and data in a manner that is private, secure, and accurate. The technology combines ForwardLane’s composite AI, EMERGE-GPT, with its Visual Insight Generator (ViGOR). Visual Insight Generator is a zero-code tool that enables users to create insights from data using natural language – without requiring any technical expertise in LLM. Along with ForwardLane’s Next Best Action platform, EMERGE provides a complete cycle from insight and orchestration to last-mile delivery, usage, and feedback.

ForwardLane founder and CEO Nathan Stevenson noted that his company has been leveraging AI for several years. “EMERGE is an applied Generative AI solution for financial services that brings together the best functionalities of ForwardLane’s ViGOR and privacy-friendly EMERGE-GPT,” he said. “It gives financial services firms the ability to rapidly activate their existing data and data science investments and deliver insights to their frontline advisory and sales professionals.”

EMERGE will enable financial services professionals to:

Identify opportunities and risks across their client base

Review up-to-date client intelligence and analytcs along with recommended Next Best Actions

Receive Next Best Action recommendations that are integrated via API with workflow links

Accelerate daily workflow with 100x increases in document reading ability

Summarize, interact, and extract insights from PDF, DOC, and other files up to 25,000 pages

EMERGE is available on a white label basis. The technology can be deployed on cloud platforms or hosted by ForwardLane. EMERGE is currently in limited beta testing; the company expects to offer wider availability in the second half of 2023.

Founded in 2015, ForwardLane made its Finovate debut a year later at FinovateSpring. The New York-based company has raised more than $8 million in funding from investors including SixThirty and SEI Ventures. ForwardLane began the year teaming up with InterGen Data to offer predictive life-event driven insights.

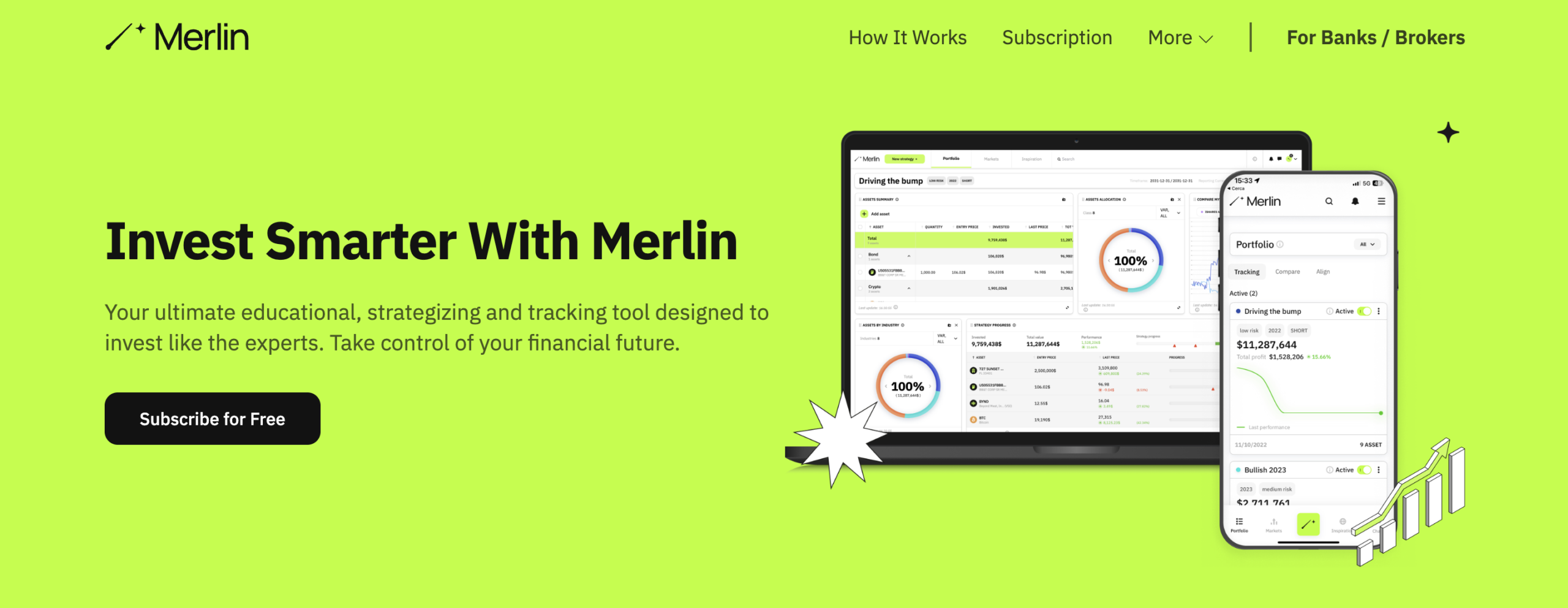

Launched in the fall of 2021, Merlin Investor is on a mission democratize access to investment strategies. The fintech offers a while label, multi-asset, educational, strategizing and tracking tool that helps investors accomplish two critical goals: building long-term positive results and limiting potentially catastrophic losses.

Merlin Investor’s technology is compatible with all trading platforms. The technology is suitable for both retail and professional traders, and is available for both the desktop and mobile. Merlin Investor enables users to retrieve market data and sentiment from multiple sources and apply that data to a massive range of tailor-made investment strategies.

With offices in both West Palm Beach, Florida, and Lugano, Switzerland, Merlin Investor made its Finovate debut at FinovateEurope earlier this year. The company returned to the Finovate stage in May for FinovateSpring. We caught up with Merlin Investor founder and CEO Guido Petrelli (pictured) this summer to learn more about the company, its mission to democratize access to investment strategies, and what to expect from the company in 2023 and beyond.

What problem does Merlin Investor solve and who does it solve it for?

Guido Petrelli: Merlin Investor was born as an intelligent protection and conscious guide for a more farsighted management of investments aimed limiting potential catastrophic losses while building long term positive results. Thanks to the Merlin platform, retail investors can educate themselves, study the markets, and create and track their own investment strategies to easily understand, balance and diversify investment risks.

In other words, we help and empower a new generation to invest with strategy in mind. This is the key to becoming successful and is the only factor distinguishing between gambling and investing. As we are on a mission to democratize financial inclusion and investment planning, our technology was built to allow anyone, regardless the level of knowledge or experience, to become independent and the one and only master of their own financial future.

How does Merlin Investor solve this problem better than other companies?

Petrelli: In the retail investor space, we see many companies focusing on execution, meaning focusing on the act of buying and selling assets. But executing without evaluating multiple sources of information first, combined with the lack of a diversified and balanced investment strategy, can lead to uncontrolled and unlimited potential losses because of the market’s ups and downs. While it may imply the chance for quick gains, it’s actually not the norm as wealth is usually built over time by managing a positive-sum game.

That’s why from the very beginning Merlin was designed as a complementary product to a trading platform and not as a substitute solution. Merlin Investor addresses the strategic essence of investing while the majority of the competition just focuses on enhancing the trading experience – which is already well supported by several financial institutions in a pretty similar way.

Who are Merlin Investor’s primary customers. How do you reach them?

Petrelli: Our primary customers are financial institutions focusing on educating a new generation of retail investors and offering the possibility to trade different asset classes through their digital banking platforms. We attend multiple fintech events in several countries that are attended by financial institution decision-makers responsible for delivering an innovative and digitalized experience to their clients. We also analyze the markets to identify those prospect clients we believe to be a fit in terms of services and client base. Then we look for the people focusing on retail digital products and platforms and reach out to them to introduce our company and technology. Last, we work to be featured in fintech-specialized magazines having financial institutions as target audience.

Can you tell us about a favorite implementation or deployment of your technology?

Petrelli: We offer our technology as a white-label solution that financial institutions can easily embed into their own digital platforms through API keys, while having the possibility to customize product’s appearance and features. As result, our product is delivered to the final users in the bank’s name and as a sub-section of the same app/e-banking they are already familiar with. Through our B2B partner’s portal, we grant to financial institutions the flexibility to choose from the full Merlin product those asset classes, sections, features, and contents they intend to integrate based on their own specific needs. In this way, they can design a tailored solution and experience for their own clients, while sticking to the overall structure and design of the banking platform they already offer.

What in your background gave you the confidence to respond to this challenge?

Petrelli: In a nutshell, it was the combination of my knowledge around investing and the problem I personally experienced as a retail investor that led to Merlin Investor. In fact, I was just a teenager when I first started to trade. Then I quickly realized that executing trades “per-se” – meaning the simple action of buying and selling assets – is the less strategic and relevant part to achieve long term positive results. Instead, studying different market sources, and then designing a diversified and balanced investment strategy, are what make the difference in the end. Still, (available) banking and trading platforms were not enough to educate me about investing, or to (help me) design and analyze my own investment strategies.

As a result, for years I was forced to create time-consuming and unfriendly spreadsheets to the point where I couldn’t accept it anymore – not in a world like today’s where we have an app for everything we do! At the same time with trading platforms booming basically everywhere, it became more and more clear that a new generation wants to invest autonomously and in the right way. As I couldn’t find any product in the market like the one I envisioned, I decided to create it. And that’s how Merlin Investor was born.

Merlin Investor founder and CEO Guido Petrelli demoing the company’s technology at FinovateEurope this year.

You recently demoed at FinovateSpring and will be demoing your technology at FinovateFall in September. What brings you back?

Petrelli: This year I’ve demoed the Merlin platform at FinovateEurope and FinovateSpring, so FinovateFall will be my third appearance. So far the experience has been great. We have been able to show our cutting-edge technology to major financial institutions in Europe and North America, while receiving much interest and establishing meaningful connections with decision-makers within the banking industry. The high visibility and key connections with prospect clients are the two main factors which bring us back to FinovateFall. The well-organized events and the team at Finovate are also a plus.

What are your goals for Merlin Investor?

Petrelli: Our goal is to be recognized by the major global banks as the innovative partner to work with when it comes to educating and empowering a new generation of retail investors. We focus on establishing solid and strategic partnerships with a limited numbers of players in the banking industry to achieve our mission of democratizing financial inclusion and strategic planning globally, while helping young investors to reach financial independence and to become the masters of their own financial futures.

What can we expect from Merlin Investor over the balance of 2023 and into next year?

Petrelli: We’ll continue to prioritize continuous and never-ending improvement of our technology by looking to upgrade the experience we offer either to financial institutions and to the final users to whom our product is deployed. We will also continue to work to boost our market presence to make the Merlin platform known to more financial institutions serving retail clients in several countries. We will eventually concentrate on scaling the team and operations to be able to manage expectations. We will accomplish all of this without forgetting our mission to make conscious and strategic investing accessible to anyone through strategic partnerships with financial institutions.

Embedded finance solution provider upSWOT announced a pilot partnership with NerdWallet Small Business.

The partnership will combine upSWOT’s embedded finance tools with NerdWallet Smart Business’ financial guidance.

upSWOT most recently demoed its technology at FinovateSpring 2023.

White-label embedded finance innovator upSWOT has teamed up with NerdWallet Small Business. The pilot partnership combines upSWOT’s embedded finance tools with NerdWallet Smart Business’ financial guidance to support small businesses.

“As a platform that provides financial guidance to consumers and small and mid-sized businesses, we recognize the unique challenges small business owners face,” NerdWallet Small Business General Manager Brandon McDonough said. “By partnering with upSWOT through this pilot, we will integrate tools and resources that help simplify small business owners’ financial decisions and fuel their growth and success.”

upSWOT leverages data from more than 200 SaaS business applications and banking platforms to provide its clients with personalized business insights. upSWOT’s embedded finance tools work with banking, ecommerce, payroll, marketing, accounting and other subscription-based technologies typically used by small businesses. The insights derived from these sources enable business leaders to see trends and performance across their customer base. This in turn empowers them to make smart decisions to enhance engagement, build loyalty, and reduce churn.

upSWOT CEO Dmitry Norenko praised Nerdwallet Small Business for its commitment to “transform the way financial services are delivered to small businesses” – a commitment shared by upSWOT. “Together, we will provide small business customers with the tools and resources to thrive in today’s competitive business environment,” he said.

Founded in 2019, upSWOT most recently demoed its technology at FinovateSpring earlier this year. The Charlotte, North Carolina-based company announced partnerships with fellow Finovate alums Alkami and Jack Henry in May. This spring, the company announced that it was teaming up with financial data access network Akoya. The partnership with Akoya will link small businesses via secure API to accounts at large U.S. banks. These financial institutions include Bank of America, Wells Fargo, TD Bank, Fidelity Investments, Truist and more.

upSWOT has raised more than $4 million in funding. Common Ocean Ventures and First Southern National Bank are among the company’s investors.

PayPal launched its new stablecoin, PayPal USD (PYUSD) today.

PayPal USD is backed by U.S. dollar deposits, short-term U.S. treasuries, and cash equivalents. The coin is redeemable 1:1 for U.S. dollars.

The new offering is designed for digital payments and Web3 and will be available on Venmo “soon.”

Fully backed by U.S. dollar deposits, short-term U.S. treasuries, and cash equivalents, PayPal’s new stablecoin, PayPal USDis now live. The stablecoin – PYUSD – is designed for digital payments, and is compatible with most digital asset exchanges, wallets, and Web3 apps. Eligible U.S. PayPal customers who buy the coin will be able to transfer it to external wallets, send it via P2P payments, and use it to fund purchases at PayPal-supported checkouts. PYUSD holders will also be able to convert their cryptocurrencies into and from PYUSD, which is redeemable 1:1 for U.S. dollars.

PayPal president and CEO Dan Schulman said that the successful adoption of crypto will need stablecoins like PYUSD. “The shift toward digital currencies requires a stable instrument that is both digitally native and easily connected to fiat currency like the U.S. dollar,” Schulman explained. Moreover, Schulman noted that PayPal – with its “commitment to responsible innovation and compliance” – and powerful brand – is in an ideal position to play this role via its PayPal USD offering. He added that PYUSD will be compatible with Web3 apps from the start and will soon be available on Venmo, as well.

PayPal USD is an ERC-20 token issued on the Ethereum blockchain. The stablecoin is managed by Paxos Trust Company. Paxos has indicated that it will publish a monthly Reserve Report for PYUSD outlining the instruments composing the coin’s reserves. The first such report is expected in September.

PayPal has been a Finovate alum since 2011. In the years since, the fintech has grown into a payments leader with more than 435 million active consumer and merchant accounts, and nearly 30,000 employees. The company has facilitated more than 22 billion payment transactions, representing a total payment volume of $1.36 trillion. Founded in 1998 (as Confinity), eBay acquired the company in 2002 for $1.5 billion. eBay spun off PayPal to its shareholders in 2015, returning the firm to its independent status.

PayPal is a public company, trading under the ticker symbol PYPL on the NASDAQ exchange. The San Jose, California-based fintech has a market cap of $71 billion.

Formerly known as TeamApt, Moniepoint is the largest business payments platform in Nigeria. The company processes $170 billion in annualized total payments volume (TPV), and became QED Investors’ first investment in Africa last year.

Headquartered in London, with offices in Nairobi and Lagos, as well as the U.S., Moniepoint was founded in 2015. The company counts more than 600,000 businesses large and small among its customers. Moniepoint has been recognized by the Central Bank of Nigeria as the most inclusive payment platform in the country, and was named the second-fastest growing company in Africa by the Financial Times.

We caught up with Tosin Eniolorunda (pictured), founder and CEO of Moniepoint, to discuss the state of fintech in Nigeria and what Moniepoint is doing to help provide better financial services to businesses and communities in Africa.

In our extended conversation, we discuss challenges to digital transformation in the region, the evolution of Nigeria’s cashless economy, and what to expect in the wake of Moniepoint’s recent rebranding.

What problem does Moniepoint solve and who does it solve it for?

Tosin Eniolorunda: Moniepoint solves the problem of fragmented, inaccessible, and low-quality financial services for businesses in emerging markets. It is a full-service business banking platform seeking to provide all the digital financial services a typical business needs.

Moniepoint specifically provides businesses in emerging markets with banking, payments, credit, and business management tools to help them grow. Our motivation is to power business dreams and create financial happiness for our customers. We recognize the importance of businesses in driving economic growth. By powering the profitability and operations of these businesses, we hope to enable them to make significant contributions to the economy at large.

To date, we have powered the dreams of over one million businesses who support local communities up and down Africa.

Your company began the year with a rebrand, transitioning from Team Apt to Moniepoint. What was the significance of this decision?

Eniolorunda: The company, TeamApt, started as a service provider, and our name was aptly selected. The team providing these services was the heart of our solution. As the company grew, our flagship product – Moniepoint – became ubiquitous in the market, and it became necessary to bring everything together to push the whole brand forward. We had become the point for people’s money, and it was only right we took up that name.

We know top talent is highly sought after in the global fintech industry, which is why we wanted to show our commitment to embracing the best and brightest by going out into the world in our choice of headquarters. By being more globally oriented, we want to be recognizable as an employer of choice for talents around the world.

What is the financial services industry like in Nigeria? And what is its relationship with the fintech ecosystem?

Eniolorunda: The financial services industry in Nigeria is generally a collaborative one. The Central Bank of Nigeria drives policy change in collaboration with all players in the industry – traditional banks and fintech players – all geared towards a more financially inclusive ecosystem. An example of how this plays out is fintechs working with traditional banks as their settlement partners, and traditional banks providing virtual account solutions to fintechs so they can, in turn, provide digital wallets to their customers.

It’s also recognized that fintechs take a generally technology-first approach to financial solutions, and regulations exist to make this as seamless as possible.

You have said that “low-trust” is an impediment to digital transformation in Africa. Can you elaborate on this challenge and what is necessary to overcome it?

Eniolorunda: Financial education is particularly important to gain trust and support for digital transformation, as people generally are wary of what they do not understand. In societies with a large percentage of uneducated people, it is expected that they will push back on innovation that promises to make their lives better.

For example, if a digital bank wants to provide nimble convenient services, it might decide not to have physical branches or a call centre to manage costs. However, low-trust means that these communities of people want to see a person or hear from them in order to leave their monies in the bank.

We overcame this barrier by approaching these markets using a hybrid distribution method – via collaboration with local people they could identify. When they got introduced to these digital solutions by people they knew and saw in their neighborhoods, it became easier for them to trust these products and try them out.

This spring there were a number of headlines about the “cash crisis” in Nigeria. Can you tell us about this and how the crisis impacted Moniepoint?

Eniolorunda: In March 2023, as part of its effort to aid in adopting cashless means of payments, combat inflation and prevent fraud, the Central Bank of Nigeria started a redesign of the Naira, Nigeria’s currency. People had to turn in their old notes as they were no longer legal tender, and the consequence of this process was a reduced availability of cash and, by extension, increased reliance on digital payments.

Moniepoint began to focus on supporting businesses in April 2022, extending our banking and payment tools to them. Consequently, during this cash crunch, we were well-placed to provide these businesses with the tools they needed to accept digital payments and stay afloat.

As a result, we saw a surge in transactions during this period. We adjusted our platform to make it more reliable, helping us to keep supporting these businesses.

What role will Moniepoint play in an increasingly cashless economy in Nigeria and other parts of Africa?

Eniolorunda: By being a banking partner for businesses, we enable them to receive payments digitally, which is very important in Africa’s journey towards becoming a cashless economy. In 2022, we helped businesses process over $170 billion, and are continuing this positive trend in 2023.

We are determined to stay at the forefront of the digital revolution. Initial efforts across the continent have been focused on providing individuals with access to digital financial services, giving them cards and other means to pay digitally. It’s not enough for customers to be empowered to pay digitally; the businesses have to be equipped with the education and resources to receive these payments.

When businesses are able to receive these digital payments directly, cash becomes less central to every transaction, and we’re collectively closer to a cashless ecosystem.

There has been talk in the fintech press about Moniepoint and potential acquisition opportunities. Is the company actively looking to make significant acquisitions?

Eniolorunda: Yes, the plan is to make significant and strategic acquisitions that align with our overall goal of providing an all-in-one financial platform for businesses in emerging markets. These acquisitions allow us to expand our product suite or enter new markets.

Also recently Moniepoint announced a partnership with Google Cloud. Why did Moniepoint pursue this partnership, and what will the partnership help Moniepoint accomplish?

Eniolorunda: As we grew bigger and faster, it was important that financial transactions on our platform could be performed at light speeds, so adopting a hybrid cloud strategy was key for us.

Some of the tools include Cloud Spanner and Kubernetes, which help us to manage and process high volumes of transactional requests per minute, with no lag time. A partnership with Google Cloud ensures we can use their services with personalized support that the scale of our business needs.

What can we expect from Moniepoint in the second half of 2023 and into next year?

Eniolorunda: We are proud to have already been be recognized this year as not just Africa’s largest fintech, but also its fastest-growing. But this is only the beginning.

We have so much in store for the second half of 2023, including plans for a new product and to enter new markets. Watch this space.

Venture investing platform OurCrowd announced an integration with Airwallex.

The integration will make it easier for investors around the world to use their local currency to invest in startups.

Based in Israel, OurCrowd made its Finovate debut at FinovateSpring 2016.

Payments and financial platform Airwallex and venture investing platform OurCrowdannounced a new partnership this week. The two companies are combining their efforts to make it easier for both institutions and accredited investors to invest in startups wherever they are and in their local currency – all with a single click.

The integration works with OurCrowd allocating a global account for each investor. Investors can choose to convert their funds into a number of different currency options, including their own local currency. OurCrowd converts the funds to the selected currency at a transparent rate that is typically guaranteed for 24 hours. More than a third of OurCrowd’s FX flow has moved via Airwallex since the company embedded its API in February. OurCrowd anticipates increasing its flow to 90% by the end of the year.

“With the globalization of the startup world advanced fintech which is multi-currency is a game changer,” OurCrowd CEO Jon Medved said. “Now you can be sitting in Israel and invest in a Silicon Valley startup, pay in Shekels with a single click and it is totally transparent.”

Traditionally, investors have had to convert their local funds into U.S. dollars and then send those funds by wire in order to invest in startups. In contrast, the partnership between OurCrowd and Airwallex will provide investors from more than 195 countries with a platform that enables them to use their own currency to invest in startups. Integrating Airwallex’s API into its platform also gives accredited investors access to Airwallex solutions such as Global Accounts, Payouts, and LockFX which offer further opportunities for investors to participate in startup deals.

Pranav Sood, EGM, EMEA at Airwallex, described the partnership as another success for embedded finance. Sood explained that the integration was a “perfect example” of supporting the growth of its end users while simultaneously giving OurCrowd tools to add to the services they are able to offer. “From streamlining payment processes for investors and startups to minimizing FX costs, embedded finance is simplifying the way businesses operate across borders,” Sood explained.

Headquartered in Melbourne, Australia, Airwallex helps more than 100,000 businesses streamline their international payments and financial operations. The company offers solutions for payments, treasury and spend management, as well as embedded finance, and processes $50 billion in annualized transaction volume. In recent months, Airwallex has forged partnerships with Brex, payments network TrueLayer, business payments platform MODIFI, and Expedia. Founded in 2015, the company has raised more than $900 million in funding at a valuation of $5.6 billion.

OurCrowd made its Finovate debut at FinovateSpring 2016. At the conference, the Israel-based company showed how its app provided an interactive investment discovery and review process to help accredited investors make better, more informed decisions. One of the most active venture investors in Israel over the past ten years, according to Pitchbook, OurCrowd has more than $2.2 billion in commitments. The company has deployed capital into more than 420 portfolio companies and 50 funds across five continents. Founded in 2013, OurCrowd has more than 225,000 registered members from 195 countries on its platform today.

Rumors have circulated that the partnership between one of the biggest names in finance – Goldman Sachs – and one of the biggest names in tech – Apple – is coming to an end.

Specifically, the reports suggest that Goldman Sachs is looking to exit its financial relationship with Apple. Goldman Sachs is Apple’s partner for its Apple Card – and has been since 2019. Goldman Sachs is also Apple’s partner for its Buy Now Pay Later service, currently in beta. Reports from the Wall Street Journal indicate that Goldman Sachs is looking to off-load its Apple credit card business to American Express.

So why has the relationship soured? Here are four possible factors:

Know Your Customer

One of the big headline issues hinting at friction between Goldman Sachs and Apple occurred when Apple CEO Tim Cook was testing the Apple Card and was unable to get approved. The issue had to do with fraud protection protocols on Goldman Sachs’ side. The company’s underwriters rejected the application because, as a well-known, high-profile individual, Tim Cook is often impersonated by fraudsters. This appeared to be a one-off problem at first. But an investigation by the U.S. Consumer Financial Protection Bureau led to additional concerns about disputed transactions and, ultimately, reports of gender bias in the granting of credit limit increases. Goldman Sachs was cleared of any wrongdoing, but the drama helped stoke tensions between the company and Apple.

Culture Clash

It’s not surprising that there were issues between the East Coast Wall Street culture of Goldman Sachs and the West Coast Silicon Valley culture of Apple. But there were very real challenges in the working relationship between the two firms. As is often the case when “move fast and break things” technologists team up with the rules-based world of finance, there was a tension between what one person called a focus on “the sleek technology and product pizazz” on the one hand and “regulatory compliance and profitability” on the other. Even at a more mundane level, basic issues such as the timing of billing statements and card design became grist for conflict and development delays.

The Bank Behind the Curtain

Writing at 9to5 Mac, Chance Miller noted that in addition to losing a ton of money with Apple Card – more than $1 billion by January 2022 – there are other ways that Goldman Sachs was losing out on the Apple partnership. Miller points out that not only was Apple developing its own in-house financial service project (called “Project Breakout”), but also there were other aspects of the relationship that ill-served Goldman Sachs. “One thing to keep in mind is that most Apple Card users likely don’t even know Apple Card is backed by Goldman Sachs,” Miller wrote. “Goldman Sachs exists in the backend, and everything else is managed directly through the Apple Wallet app.”

While this relationship is common in fintech and financial services, it seems like a poor approach for Goldman Sachs, which is newer to the consumer business than Chase or American Express and was likely seeking to build its consumer brand via its association with Apple. Couple that issue with the financial losses, and the potential of Apple “breaking out” on its own, and Goldman Sachs may have one more reason to start second-guessing its Apple Card gambit.

Whose Idea Was This Anyway?

When Goldman Sachs first announced its partnership with Apple, there were many who questioned the financial institution’s deepening foray into consumer banking. Goldman Sachs earned its lofty reputation in the world of finance as a leading investment bank and investment management firm. To say that consumer banking was not a core Goldman Sachs competency would be an understatement. But in the wake of the financial crisis, with Wall Street banks desperate for new revenue sources, consumer banking and the rise of fintech were alluring opportunities to an institution like Goldman Sachs. Goldman Sachs had room to grow – and money to burn. The firm also had a brand name and reputation that would help it gain the attention it would need in an increasingly competitive market.

But projects like Marcus rose and plateaued, with an initial rush of deposits leading to overly optimistic profit forecasts and, ultimately, significant losses. Efforts to expand into areas such as investing via Marcus revealed that Goldman Sachs was not as innovative as smaller upstarts like Robinhood. An attempt to leverage opportunities in consumer lending with the acquisition of Buy Now Pay Later startup GreenSky proved costly.

Seen through this lens, Goldman Sachs’s issues with Apple Card may have more to do with Goldman Sach’s issues with consumer banking.