This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Accusoft researched several of the factors driving technology and innovation in the financial services industry to better understand the current and future role of FinTech in the marketplace. Find out what they learned, discover assets that can help you solve your content processing, conversion, and automation challenges, andlearn more about their FinTech solutions >>

Upcoming webinar Title: Biometric authentication for SCA and beyond: the art of the possible Date: Wednesday, March 03, 2021 Time: 03:00 PM Central European Time Duration: 1 hour

The PSD2 requirement for Strong Customer Authentication, combined with Mastercard’s mandate on biometrics, has led to an increase in the deployment of biometrics as one of the 2 factors of authentication. A strong preference from consumers for its ease of use is also driving adoption.

Join this webinar, with BNPP Personal Finance, Mastercard, and Fabrick, as they share their experience of deploying ID Check Mobile (IDCM), MasterCard’s biometric authentication solution for online payments.

The expert panel will tackle the topics including how the solution can help issuers meet regulatory requirements and how biometrics can deliver additional value-added services to maximize return on investment. The speakers will take time during the discussion to answer questions from the audience – so use this time to get your queries and thoughts addressed.

Featuring:

Moderated by: Julie Muhn, Analyst, Finovate

Stephanie Chlala, Project Manager, Payments, BNPP Personal Finance, France

Register for thisupcoming webinar Date: Thursday, March 04, 2021 Time: 11:00 AM Eastern Standard Time Duration: 1 hour

Traditional wealth management processes are not designed for the digital age. Firms need digital solutions that address clients’ rising expectations for digital experiences and expand service offerings while reducing operational complexity.

Going digital, however, isn’t for the faint of heart. With 85% of projects going over schedule and 70% of large-scale digital IT programs failing to even reach their stated goals, developing enterprise software can be a painfully inefficient affair. This is where Unqork’s no-code platform can be a game-changer.

Join this upcoming webinar to learn more about how the wealth and investment management industry is being disrupted, and what you can do to stay ahead of the curve. Featuring: David Penn, Research Analyst, Finovate and Matt Singleton, Client Partner, Unqork.

The COVID-19 crisis has thrown a spotlight on the inefficiencies underlying many functional areas of financial firms and caused executives to reevaluate operational resilience in light of increasing volumes and volatility. There’s been a lot of industry discussion about the potential of Machine Learning and Artificial Intelligence (AI) to tackle challenges ranging from regulatory change management to improving the client experience.

AI has huge potential to augment and transform current market practices, but organizations need to make sure they are laying the groundwork for successful implementation by considering the underlying data infrastructure required to turn these technology ambitions into reality.

In this white paper, Firebrand Research discusses how to tackle the complex issue of data management and shares key reasons to invest in a smart data fabric, including:

Building the data foundation for next-generation initiatives

Enabling a firm to adapt to volatile markets via real-time analytics

Connecting and harmonizing data on demand from across a firm’s many silos

Keeping firms out of the regulatory hot seat by ensuring high data quality

Providing accurate and real-time insights and new innovative services to keep ahead of the competition

As part of our ongoing #WomeninFinTech series, we spoke with Kathy Strasser, Chief Operating Officer/Chief Information Officer at IncredibleBank about her experiences in and thoughts on the fintech industry today.

To start, please tell us a little about yourself and how you became involved in banking and fintech?

Strasser: After a 20-year career at Wausau Financial Systems (WFS) in various roles throughout the organization, I was approached by IncredibleBank’s CEO Todd Nagel (then River Valley Bank). He wanted a non-banker with a technology background to help him launch the internet-only division of River Valley Bank, IncredibleBank, into a leading digital bank reaching customers across the entire United States.

I never imagined myself working for a bank until 2015 when I joined as the EVP and Chief Operations Officer. Over the next few years, I’d play a key role in accelerating the growth of the bank and its digital transformation on both the technology and people side of our business.

While technology and payments are strong interests of mine, I’m most passionate about leading people, which is what IncredibleBank allows me to do. In my current position, I’m responsible for helping people find their motivation and providing them with purpose and the autonomy to be brilliant at what they do. By nature, I’m a problem solver, change guru, and love everything happening with digital transformation.

How have you seen the financial services industry change in 2020, and where is it headed in 2021?

Strasser: The work we’ve done over the past five years prepared us for this shift to digital technology. Our people were ready to meet the needs of our customers in a remote environment. We leaned on the expertise of employees from all parts of the organization for the PPP program, in addition to helping 1,000+ homeowners buy new or refinance their homes. We launched Zelle in September, made digital improvements to our customer experience, implemented new technology to help facilitate the PPP program, plus we became the first community bank to go live on TCH RTP in March.

We know that the momentum we have seen with digital is only going to continue and competition will shift as BigTech continues to make its foray into financial services. There are a few areas that are always top of mind for us: digital transformation and growth, continuing to master our incredible customer experience, talent management, employee engagement, and continuous growth in our business lines.

How can community banks make sure they’re not being left behind, especially when it comes to embracing new digital technology?

Strasser: Companies like Apple, Amazon, PayPal, and Starbucks are already in the payments space, which is traditionally a medium for banks to grow and retain deposit accounts as well as build customer relationships. We’ve remained competitive by prioritizing the customer experience and partnering with companies like Jack Henry to deliver new and innovative technology. Community banks need to stay at pace with this broader competitive market and having a differentiated customer experience that is both personal and meaningful is a strong start.

What does digital transformation entail within your institution?

Strasser: Digital transformation is about technology and people. Our people come first in our digital strategy and transformation, which is why culture must be approached with a growth mindset.

We start by mapping out our digital competencies and identifying areas of focus that will move the needle on customer experience. Some of these included the ability to confidently move between different devices and building relationships via digital channels. Our key values for our digital culture are speed, openness, and autonomy. Technology had to improve processes, productivity, and customer experience, delivering direct value to our institution and customers.

How can women help other women climb within the industry, and do you have any advice for those starting out their careers in technology or finance?

Strasser: The future is bright, and I highly recommend technology and finance for everyone, especially women. Women in the field can be a good example and share their experiences; I’m always willing to mentor, meet with young people getting ready to go to college, or those figuring out the next step in their career.

I’d give the following advice: 1) Focus on your role and how it contributes to the success of your company; 2) Seize new opportunities and don’t be afraid to ask; 3) Learn every single day; 4) Build relationships and your network; 6) Find guidance from someone greater.

What are fintechs and banks missing right now that women are uniquely positioned to help with?

Strasser: With diversity comes a background of many different experiences and approaches to problem-solving, disagreements, negotiations, leadership style, and approach. Dynamics and conversations change when the table is filled with both men and women and as a result collaboration and innovation happen. For example, knowing a large percentage of women make household decisions is important when creating and seeking feedback on new products and features. For any growing company, it’s important to have a diversified pool of candidates to choose from, and that includes women.

The below is a sponsored post by FinovateFall Digital exhibitor, Invest Puerto Rico.

Puerto Rico is poised to become the global model for how to roll out cutting-edge tools that enable blockchain, AI, and the Internet of Things (IoT). All of these technologies are designed to transform nearly every sector, notably financial services, bioscience, and aerospace. Technology represents the changes imminent in the 4th industrial revolution. Proper implementation and growth of these tools has been a critical priority contributing to the island’s economic diversity, development, and competitiveness.

Network

Advances in these fields would not be possible without a supportive Information & Communications Technology (ICT) network. As an island, Puerto Rico depends on its ability to communicate with the world to do business. As such, companies benefit from extensive island-wide 5G, broadband access, established LoRa network capabilities, and broad satellite connections. Every element of this network ensures producers are connected to suppliers, customers, and business partners. Puerto Rico’s tech expertise and nationally unique international banking policies—along with the growing demand for effective financial solutions and resources—has led to a boom in innovative fintech and investing services that extend to every industry.

Fintech

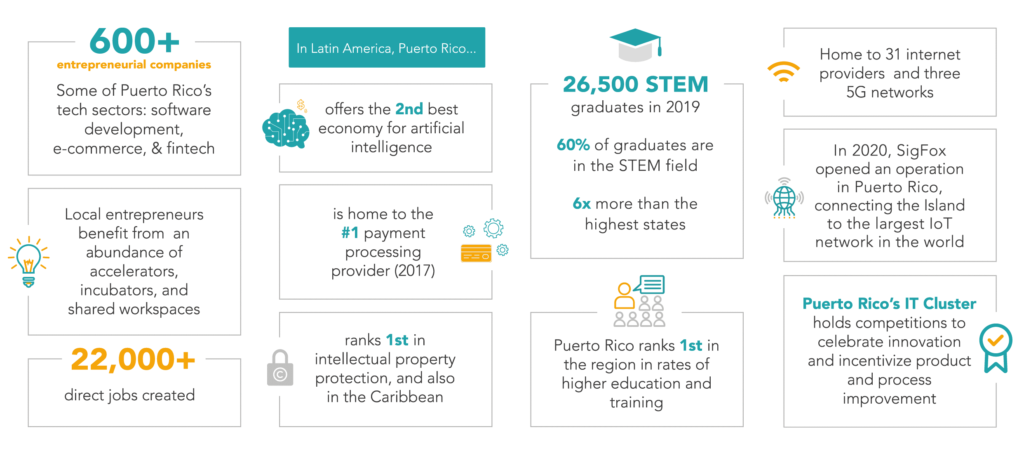

Fintech is growing fast, at a rate of 25% per year through 2022. Puerto Rico’s close proximity to the world’s financial center – New York City – gives island-based fintech firms the opportunity to remain connected while taking advantages of key local benefits such as STEM talent, local financial literacy, and attractive tax incentives. Puerto Ricans are open to technology providing financial solutions where traditional banks do not. Here are a few facts you might have known about the island.

In 2017, Puerto Rican firm Evertec was the #1 provider of payment processing services in Latin America, exporting financial services to 25 countries around the world

After just four years, Evertec’s money transfer platform, ATH Movil, reached over 1 million users, 6,000 businesses, and 80% of banks and credit unions

Banco Popular’s digital platform also leads the industry in the implementation of fintech solutions

Abexus Analytics identifies commercial lending solutions to SMEs as one of the key areas of opportunities in Puerto Rico’s fintech landscape

Among others, Act 60 applies to financial activities and export services. IFEs are eligible for 6% income tax rate on distributions to resident shareholders or members and are 100% exempt on distributions to nonresident shareholders and members

Innovation

Puerto Rico also leads the region in fintech innovation, and this is evident in the wide use of digital banking tools, mobile financial applications, and globally recognized payment processing technology. Banking with digital assets is quickly becoming a reality and the blockchain community is pushing innovations for tax credit trading and how to sell utility tokens within tax incentive regulations. The island is leading the way in helping fintech, insurtech, and blockchain become more ubiquitous. The local financial services industry is perfect for global companies and start-ups looking for a cost-effective domicile or fertile ground to develop ideas, scale, and expand into neighboring markets.

The Only Place

Combine U.S. federal regulations and exemptions with local tax benefits and operating incentives, and you get the only place for international financial entities and insurers on U.S. soil: Puerto Rico. The island offers companies experienced banking and insurance markets, with a broad base of financial experts in U.S. and international laws and regulations. Puerto Rico stands to be an international leader in the finance and insurance industries by providing banks and insurers, companies, and individuals unparalleled access to the U.S. market with global regulations.

Puerto Rico is the nexus of opportunity. Contact a member of the Invest Puerto Rico Business Development team to learn how you can locate your startup or established business to the island.

Leading the way in strengthening the island as a world-class business destination is the newly formed Invest Puerto Rico (InvestPR), a non-profit investment promotion organization created by law, via Act 13 – 2017. InvestPR’s mission is clear: promote the island as a competitive investment jurisdiction that attracts new business and capital investment to the island. Our vision is to be a transformational and results-oriented accelerator of economic development in Puerto Rico.

As 2020 comes to a close, the Finovate team and our faculty of expert contributors take a look at some of the trends that defined the year, and will continue to make a splash in 2021.

With a specialized focus on the latest in bankingtech and customer experiences, we bring together four, on-demand webinars featuring industry insights and practical steps to move your business forward in the new year. Webinar topics include:

Leveraging technology as a business strategy in financial services

Delivering customer knowledge augmentation and activation

Innovating in contact centers

Moving beyond customer expectations in the digital age

Download the eMagazine to access all the content from the week, plus the latest articles and insights from our Finovate analysts. You’ll also have access to an exclusive discount code for FinovateEurope Digital 2021.

The following is a sponsored post by Tracy Schlabach, Senior Manager, Product and Customer Marketing, Accusoft.

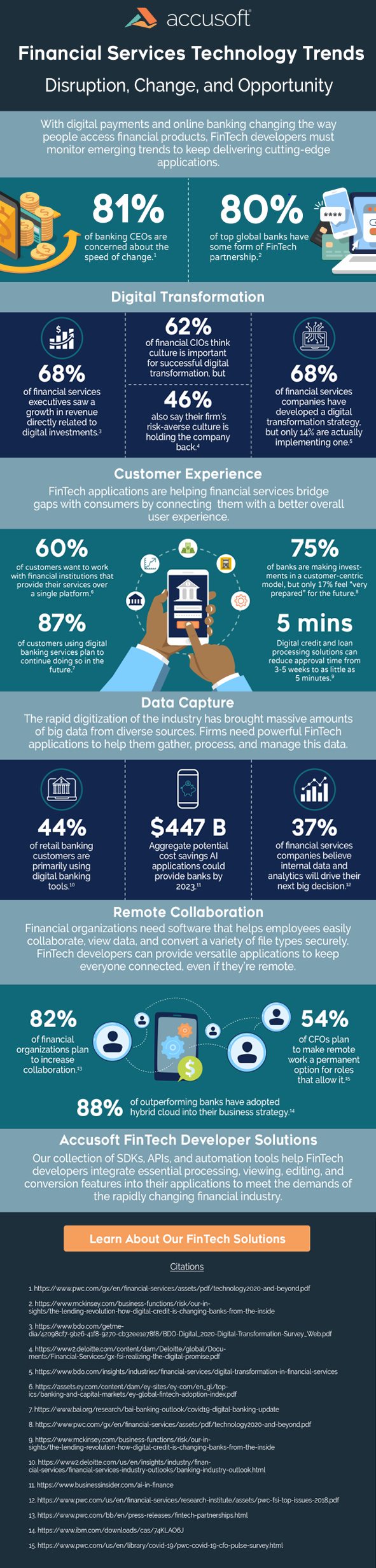

Digital transformation has been on the radar of most financial institutions for years. In a 2020 Digital Transformation Survey by BDO of financial services professionals, 68% of respondents in 2019 saw a growth in revenue directly related to digital investments. While many have made digital transformation a priority, some have faced roadblocks including risk-aversion and lack of corporate sponsorship.

With COVID-19 sweeping the globe, priorities are shifting, emphasizing the need for digital transformation. As noted in a state of the industry report authored by the Institute of International Finance and Deloitte, “COVID-19 has generated leadership and organizational support by highlighting the need for digital transformation as a means to reach customers and maintain operational resilience.” Of those surveyed by BDO prior to the COVID-19 outbreak, 36% see industry disruption as the primary digital threat. In addition, a recent survey by IDG Research states that 59% of respondents are seeing an acceleration of digital transformation in their companies driven by the pandemic.

Now that implementing the digital strategy has taken center stage on the fintech roadmap, developers are looking to meet the needs of leadership as well as customers and employees in a timely and budget efficient manner.

What Is Digital Transformation?

The name digital transformation embodies a wide assortment of initiatives, from the customer engagement experience to transforming legacy systems. In an article by The Financial Brand, financial executives were asked to select their top digital transformation priorities for 2021. Out of the long list of initiatives, four of the highest priorities are:

Improve Customer Experience

Improve Use of Data, Analytics, and AI

Enhance Innovation Agility

Improve Back Office Efficiency

Financial institutions are prioritizing several diverse initiatives to remain relevant during the global pandemic. Project managers need to shorten development time, meet executive mandates, and launch products that significantly improve the employee and customer experience.

SDK and API Integrations Streamline Fintech Development

Development teams can effectively meet those timelines by partnering with software manufacturers who build and maintain software development kits (SDKs) and application programming interfaces (APIs). Developers can integrate these SDKs and APIs into their product offerings to add unique document processing capabilities. By partnering with a high-tech software solution, your team can save development time, shorten sprints, and reduce maintenance cost. While these are significant benefits, partnering and integrating third-party software manufacturers come with many advantages, including the ability to:

Remove the burden of building and maintaining extensive document processing libraries

Access the manufacturer’s support and engineering team who can assist with implementation and resolve issues

Significantly reduce time to market of your product

Let’s take a deeper look at each of these advantages.

Integrate vs. Build & Maintain Document Processing Libraries – Consider how many different file formats are available in the market for submitting data to financial institutions. Fintech users receive everything from Word documents to PDFs to images taken with cell phones. All of those file formats need to be taken into consideration when building a fintech application that streamlines the process of capturing data from those files. Building out libraries of code that can address every possible option is extremely cumbersome and time-consuming. However, developers can leverage an SDK or API that has been developed specifically for document processing and open up time to focus on their core competencies.

Access to Support and Engineering Experts – When financial institutions embed third-party document and image processing solutions, they are also gaining access to a team of experts. At Accusoft, each customer has access to technical support and product developers that have helped hundreds of companies with implementing and utilizing these document processing SDKs and APIs. Digital transformation is a pressing concern for financial organizations. You can help them meet their needs with our SDKs and APIs. Get this new functionality up and running quickly in your application so your developers can focus on more mission-critical tasks.

Reduce Time to Market – As noted in the report by BDO, “Most financial services companies anticipate high returns on revenue and profitability from digital transformation.” Project managers that prioritize research and implement third-party software solutions can significantly reduce the time to market. This, in turn, will allow their company to realize profits faster than their competition.

With the recent changes in the world, the need for digital transformation is not slowing down. Financial institutions that prioritize those initiatives and research ways to develop and implement their new offerings quickly will be ahead in realizing revenues and returning profits to shareholders.

Accusoft is a software development company specializing in content processing, conversion, and automation solutions. From out-of-the-box and configurable applications to APIs built for developers, we help organizations solve their most complex content workflow challenges. Our patented solutions enable users to gain insight from content in any format, on any device with greater efficiency, flexibility, and security. Visit us at www.accusoft.com

The following is a sponsored post from InterSystems, Gold Sponsors of FinovateWest Digital, November 23 through 25, 2020.

In an increasingly digital world filled with chatbots, tap-and-go payments, and “buy now, pay later” credit lines, hyper-personalization is the new frontier on top of a new frontier in financial services.

What is hyper-personalization?

Hyper-personalization enables financial services organizations to leverage the huge volumes of customer data they have in their systems efficiently and effectively to make more specific and more relevant product recommendations, such as an increase of a credit limit at the point of sale, or a list of previous interactions pushed to the chatbot, allowing it to pick up where it last left off. It does so by analyzing the data available to it through the power of analytics, artificial intelligence (AI), and machine learning.

It offers immense growth opportunities for all financial services providers if they can cater to small and specific groups. Hyper-personalization can foster loyalty in an era in which loyalty has declined, and it pushes the next generation of consumers and investors towards those financial services which can be agile in what they offer.

Traditional firms and hyper-personalization

Traditional firms are often encumbered by processes built up over decades. These processes are ingrained and necessary for them to have operated the way they have successfully and for so long.

To these firms, those same processes hinder the uptake of advances such as AI, data analytics and machine learning.

Yet these and other new technologies do not require traditional firms to re-imagine how processes work, nor does implementing have to be as obtrusive and disruptive as a full digital transformation initiative, for example. Rather, technology can be implemented in the background and effectively manage itself, be installed quickly and efficiently in existing systems without disrupting the rest of the business. Some can even run adjacently to everything else the business does.

Traditional firms have decades or more worth of data. Analytics tools, AI, and machine learning work together to make sense of it all, wherever it might be and in whatever language it might be in, and surface actionable insights from all of it. Importantly, these technologies work in the background, without disrupting any mission-critical processes.

How can traditional firms hyper-personalize?

Traditional firms can deploy a smartdata fabric, which is effectively a layer which sits above all of the firm’s available endpoints and distributed services — whether it be in the cloud, on-premise or both — and ensures those endpoints and their capabilities speak the same language.

Next, the data needs to be put through proper governance procedures to ensure it is clean, relevant and has the necessary integrity to be used with confidence for the right reasons by the organization — it needs to be accurate, reliable, complete, appropriate, and credible. For this to occur, it goes through something of a digital centrifuge which analyses its health and cleans it before having it ready for primetime.

Once this is done, the rich streams of data inherent across the company can be mined, analyzed, and surfaced using the power of AI and machine learning.

This may sound like a lot of steps and go against the grain of what we’ve been discussing in this article. But rest assured, all of these technologies can be implemented with little to no disruption to operations, and they work in the background while delivering key insights for the data almost in real-time. It’s through using these technologies that traditional firms can, at last, unlock those rich and extensive streams of historical data dating back decades, which in turn provides a clear method to fostering loyalty. Research shows that customers want a hyper-personalized experience. According to Accenture, 91 percent of consumers are more likely to shop with brands who recognize them, remember them, and provide them with relevant offers and recommendations.

Conclusion

Traditional firms have a hyper-personalization advantage thanks to possessing a trove of legacy data and brand recognition. They just need to embrace what is available to help leverage their data and analytics to get them to their intelligent future — and trust that it can and will co-exist with existing processes.

If they allow technology to do the heavy lifting for them alongside their existing processes, traditional firms will be able to leverage decades of data to their advantage and engage in new ways with customers, without having to re-invent the wheel.

Drentlaw is a fourth generational banker, who is committed to serving her community and keeping the bank within the family. She is passionate about the uniqueness of community banks and their importance in the financial industry – especially given the role of community banks in the recent disbursement of Paycheck Protection Program (PPP) loans. Drentlaw continues to build on and add to the bank’s family-like culture, developing leaders, and helping her team achieve strategic plans. She’s also involved in her local chamber of commerce, mentorship organizations, and non-profits.

What got you interested in finance and banking, and what do you enjoy most in your role?

AnitaDrentlaw: Banking has been a family business for five generations, and I’m proud to carry on our family traditions and legacies. I’ve found community banking to be a perfect fit with my personality, lifestyle, and values.

What I like most about the role is the variety; it all starts with how we’re able to help and give back to the community. Community banking is about finding ways to work together to make something great. On any given day, I’m working with four generations of my family, including my daughter who worked with us over the summer.

I’ve also enjoyed being able to create a culture that makes everyone feel like they’re part of this family; they want to be here and are as proud of the New Market Bank as we are.

Are there family legacies you hope to pass onto future generations as it relates to the bank and its culture?

Drentlaw: Each generation builds upon our family’s culture to create something stronger. We have a great leadership development program focused on developing our team as well as the next generation of bankers. Our family is committed to staying a family-owned bank; our community has an appreciation for our commitment to staying a family-owned institution and giving back. That is a big part of our legacy.

I want to pass on the idea that not everything is black and white. I came from an accounting background where I believed everything always had to be perfect. But my dad changed this for me. He told me to accept that 80% is sometimes good enough and sometimes there’s gray in the world. This challenged me to think beyond my idea of perfection and do the same for others at our bank.

What is the difference between managing and leading? And how does it impact the bank’s culture?

Drentlaw: In the leadership development program that we have attended, our instructor, Erik Therwanger of ThinkGREAT, always says, “manage the work, but lead the people.” I think that statement is so true. We’re a bank that likes to lead; we empower our team to be leaders and provide them with the tools necessary to be successful. Being a leader requires having a stake in the game. We want our team to feel like they’re part of a larger vision and mission – one that they’ve helped create, have ownership in, and feel strongly about accomplishing. We’re not in the business of managing our employees, but want them to feel like the bank is just as much a part of their family as it ours.

Why is it important to strike a balance between in-person and digital interactions these days?

Drentlaw: There’s a place for both in-person banking and digital interactions, and the pandemic has certainly proved this concept. The need to move to a largely digital environment, for our team as well as customers, was possible thanks to the modern technologies we’ve added from partners like Jack Henry.

Moving forward, we must be available to customers whenever, wherever, and however we can be. While digital has expanded our customer touchpoints, it’s not – and shouldn’t be – the only way we communicate and build relationships. People bank at community banks like ours for the relationship; we’re the people who care – the ones at the football games, church events, restaurants. People might not think brick and mortar is important, yet branches aren’t completely obsolete, and customers still visit them. We want to be there for our customers for things they’d prefer to do in-person, as well as those that they choose to do online. For us, it’s about offering choices to our customers to meet their lifestyles and banking needs.

Why is advocating for women – and yourself – important in the industry?

Drentlaw: As women in the fintech industry, we have a duty to inspire and show other women what success can be. Advocating for yourself means standing up for what you believe in and never settling for anything less than you deserve. It’s about being brave enough to have the tough conversations and challenging the status quo. For younger women, it’s about finding their voice and tapping into the wisdom needed to reach the next level. We’re building the next generation of leaders in the industry, and that must include strong female leadership and influence.

Where do you think the future of fintech is heading over the next 12 months?

Drentlaw: This past year has shown the importance of community. We were able to help 360 small businesses in the South Metro tap into the Paycheck Protection Program – many of which were not existing customers. These loans infused more than $25 million into small businesses and our communities.

Next, fintech can help community bankers continue to revive our economies with greater customer insights that allow us to be more consultative and develop even deeper relationships. I have a feeling we’re going to see strong use cases launched to strengthen the relationships that consumers and businesses have with their bankers.

Reviewing critical challenges and opportunities in the fintech industry across 2020. With a specialized focus on the latest in lendingtech, bankingtech and customer experience.

Join Finovate for a week of webinars, thought-leadership and video interviews, all accessed online for free.

Here’s a snapshot of what’s to come…

All Finovate Fintech Fulltime Review registrants also get access to the Fulltime Review eMagazine at the end of the week, featuring key session recordings from FinovateFall Digital and FinovateWest Digital, plus an exclusive discount to Finovate events in 2021.

Log in from the comfort of your desk anytime and choose the content that suits you. Get involved now >>

Like most industries, fintech and banking have experienced massive disruptions in the past six months. As we’ve gone through the process of enforced change, the big question facing our industry is essentially the same as the one facing the entire world right now: what is the new “normal” going look like?

But before we get there, we’re living through a moment that people will remember. Customers will remember how they were treated by their banks, and banks will remember which tech companies helped them take care of their customers (and which didn’t). It will be important to stay focused on the big picture, and get remembered for the right reasons.

FinovateFall Digital 2020 honed in on the technologies changing the game this year, and put the thought leaders with a view for leveraging the opportunities this time offers up on the center stage. The event eMagazine was exclusively available to FinovateFall Digital attendees for the week of the event, but now we are making it available to the wider Finovate community.

Catch up on the insights from the week, including daily summaries from our Finovate’s analysts, expert insight from our Headline sponsor, Accusoft, Best of Show and Finovate Awards winner announcements, and exclusive interviews with our speakers, demoers and featured FIs from the event.