This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

It’s clear that we are entering a new, substantially more digital era in finance and banking. Customer behavior has changed forever (and so have customer expectations), and it’s not going to change back. We’re a long way from a new status quo, and things are going to keep moving quickly. It’s up to all of us to decide if we’re willing to move quickly too.

Last week saw the second Finovate Halftime Review, exploring the critical trends for banks, FIs and fintechs from 2021 so far and looking ahead, and designed to open up the discussion for those in the industry on what the future of finance should look like.

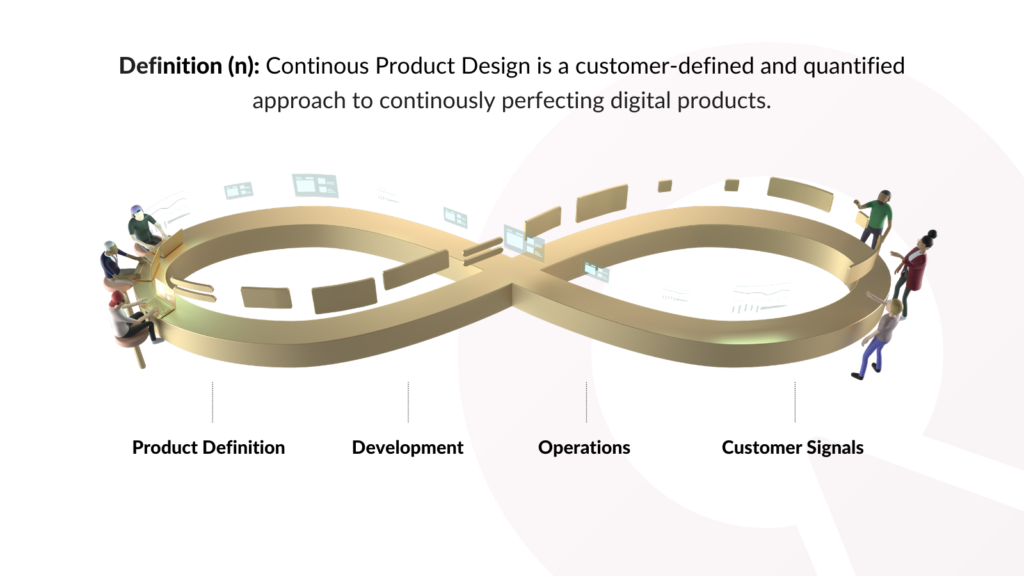

The partnership between Quantum Metric and U.S. Bank was major part of the conversation on digital transformation in financial services at FinovateSpring in May. Quantum Metric, headquartered in Colorado Springs, Colorado, and founded in 2015, leverages its Continuous Product Design (CPD) platform to enable business, product, and technical teams to build better digital products faster. With partners ranging from Alaska Airlines to Western Union, Quantum Metric helps businesses access the customer insights that guide and inform development process.

We caught up with Michael Hanson, Regional Vice President of Banking and Financial Services at Quantum Metric, to find out what banks and fintechs can learn from Quantum Metric’s experience in collaborating with U.S. Bank. A textbook case of “two great tastes that taste great together,” Quantum Metric and U.S. Bank showed attendees what’s possible when companies with track records of innovation and a shared commitment to collaboration come together.

On the breadth of digital experience in financial services

When you think about digital experiences, it’s more than just a website. It can be a native application. It could be your tablet experience – depending on the demographic. It could be ATMs – ATMs are essentially a branch within a digital device – as well as kiosks in the traditional storefronts and branches that tend to be the bridge between the traditional banking relationship and a digital self-service relationship.

On the value of a company-wide embrace of agile operations

That means that marketing is now going to be agile. So instead of trying to craft some type of new product or new pitch and then releasing it out in the wild and seeing maybe in six months if it worked and delivered … No! We want to launch something, but we want to know immediately, in real-time, (and) understand if it’s working or not working, if there’s an opportunity to drive some type of improvement. It’s literally agile operations, which has been around for decades, but is now being deployed across the organization.

On the challenge of overcoming “technical debt”

There are long-term contracts and on-premises solutions that are baked into current workflows and current processes. And so as you’re learning new tricks, so to speak, (the question is): how do we quickly retool and empower our employees with the technologies that are going to support those new processes and support some of those new tricks that we’re teaching folks?

This is a sponsored post in collaboration with Sean Hunter, CIO at OakNorth

When it comes to commercial lending, banks rely on risk models to make decisions. These models have been built up internally over decades of lending across thousands, if not tens of thousands of loans, but COVID-19 has exposed unexpected flaws in them. As a result, lenders are re-assessing how best to manage commercial credit risk in the future when other unprecedented events will inevitably occur.

Challenges

The first challenge is that traditional risk models are based on historical data, but in a rapidly changing world, extrapolating from the past is an approach that is no longer fit for purpose. Events such as trade wars, pandemics, natural disasters, and climate change are by their very nature situations that are hard to predict or plan for. We can make assumptions based on what we have seen with similar crises in the past, but no two are the same. Therefore, any data needs to be supplemented with a forward-looking view, which takes into account future challenges that may arise and that provides the much-needed foresight to make more informed credit decisions.

The second challenge is that most banks’ risk models tend to lump all businesses into one of a dozen or so categories – all restaurants, bars and hotels for example, are classified as “hospitality”. This disregards the fundamental differences in how these businesses operate, and makes it harder for lenders to identify the most vulnerable businesses in their portfolio. The experience of a pizza delivery / takeaway chain in New York City throughout the pandemic will have been very different to a Michelin-star fine dining restaurant in The Hamptons for example. Under lockdown, the Michelin-star fine dining restaurant is unlikely to have experienced any business, whereas the pizza chain may have seen an increase in trade as people were spending more time at home. When lockdown eases, however, and restaurants are allowed to reopen (but with strict social-distancing and cleaning measures in place), the situation could be quite different. The formerly empty Michelin-star fine dining restaurant may experience a surge in reservations as many diners would have saved money from a lack of socializing for several months, and look to make their first meal out “special.” Meanwhile, the pizza chain may see demand for deliveries shrink as people rush to enjoy the outdoors and take advantage of their freedom.

In a fast-changing world, a timely change of course informed by insight and foresight is much preferred to 20/20 hindsight when it’s too late to avoid a problem.

– Sean Hunter, CIO at OakNorth

Unprecedented events such as the pandemic can also lead to structural changes which have permanent or long-term implications for the sector. Take a paper and board packaging business for example – during the pandemic, it will likely have seen revenue from paper sales decrease as businesses moved to remote work and instituted digital solutions such as DocuSign. However, on its balance sheet, year-on-year sales for the entire business in 2020 may not seem too different than in 2019. This is because the decrease in demand for paper has been offset by an increase in demand for cardboard as people under lockdown shop online and order items to their home. While the move away from heavy paper use is likely a permanent change from the pandemic, the increase in online shopping is unlikely to stay at peak pandemic levels once people are able to return to in-store shopping. Therefore, if the business fast forwards six to 12 months, it could see a decrease in revenue that it hadn’t been expecting and therefore, hadn’t planned for.

In this example, the lender, armed with this data, can take an informed, consultative role and share this analysis with the borrower, suggesting that they think carefully about any changes that will add to their cost base. Equally, the business’ management team can now be better prepared for changes further down the line. In a fast-changing world, a timely change of course informed by insight and foresight is much preferred to 20/20 hindsight when it’s too late to avoid a problem.

The third and final challenge is that traditional risk models don’t take into account how quickly the situation changes day to day. The approach taken by the Trump administration to address the impact of climate change for example, were completely different to the steps being taken by the Biden administration. Lenders therefore need the ability to re-run analyses and stress test on an ongoing basis in order to determine how governmental or socio-economic changes are impacting their loan book.

Solutions

At OakNorth, we’ve created the ON Credit Intelligence Suite to enable banks to lend smarter, lend faster and lend more to businesses. In order to ensure lenders can obtain an incredibly granular, bottom-up view of every business in their portfolio, we’ve split the economy into 262 different sub-sectors. The software is made up of three components:

ON Credit Analysis: which provides lenders with a 360-degree view of borrowers with instant financial forecasting, sector insights and peer analysis.

ON Portfolio Monitoring: which enables lenders to easily track sub-sector industry trends and set early warning alerts for potential covenant breaches.

ON Portfolio Insights: enables lenders to instantly segment their portfolio and rate loans based on level of vulnerability.

Find out more and join the upcoming webinar with OakNorth to dive deeper into this topic, featuring Jeremiah Norton, former FDIC; Bruce Richards, former Federal Reserve Bank of New York; and Mark Levonian, former OCC. Register now >>

Back by popular demand, theThe Finovate Halftime Review returns June 21 through June 25 to bring you daily, one hour, expert-led discussions with interactive Q&A, all delivered online. Register for one session or all – pick the topics that interest you and listen in as our guest contributors shed light on the critical challenges impacting financial services right now.

What’s coming up?

Live webinars on topics critical for the fintech industry…

A Practical Path to Machine Learning Success for Financial Services with InterSystems

The “New Normal” of Working in Finance: Getting to Grips with the Opportunities, Challenges and Risks with Hysolate

Fintechs and the Era of Radical Inclusivity: Leveling the Playing Field Through User Experience with CleverTap

The “New” Frontier – Find Innovation, Adaptation & Growth in America’s Heartland with JobsOhio

Plus, on-demand webinars to set you ahead of the competition…

Customer Engagement Tactics to Boost Loyalty and Monetization

The New C-suite Challenge: Rise of Customer Experience

Pandemics, climate change, recessions – Oh my! How do you manage commercial credit risk in an ever-changing landscape?

Building Trust: How Video is Reshaping Digital Customer Engagements in Banking

Insightful new and analysis from our resident analysts…

We’re bringing all of this, plus the Finovate Halftime Review eMagazine, which collates all the best bits of the week into one easy-to-access magazine.

Upcoming webinar Title: Pandemics, Climate Change, Recessions – Oh my! How Do You Manage Commercial Credit Risk in an Ever-Changing Landscape? Date: Thursday, June 10, 2021 Time: 1:00 pm Eastern Daylight Time Duration: 1 hour

Once we’ve overcome the pandemic, the next crisis regulators will be turning their attention to is climate change. Unlike Covid-19, climate change isn’t something we can develop a vaccine for – and it is here to stay. Climate change risk will therefore be a key focus area for regulators going forward, so banks need to be thinking about how they’ll address and analyze climate-related risks and opportunities at a portfolio level.

Featuring Jeremiah Norton, former FDIC; Bruce Richards; former Federal Reserve Bank of New York; Mark Levonian, former OCC; and David Penn, Research Analyst, Finovate.

It’s hard to believe that we’ve now done a full calendar year of digital events! FinovateSpring was our fifth completely digital event, and while we’re excited about the return to in-person events later this year, it’s already clear that things aren’t going to return to the same “normal” that existed in 2019.

This same pattern holds for the larger banking ecosystem as well. It’s clear that we are entering a new, substantially more digital era in finance and banking. Customer behavior has changed forever (and so have customer expectations), and it’s not going to change back.

Over the past year, the industry has (understandably) been focused on dealing with immediate challenges, but now it’s time to start looking at fintech more broadly again. We’re a long way from a new status quo and things are going to keep moving quickly. It’s up to all of us to decide if we’re willing to move quickly too.

This is a sponsored post in collaboration with InterSystems, Gold Sponsors of FinovateSpring, and Monica Summerville, head of capital markets, Celent, a division of Oliver Wyman.

Financial institutions and data have had a love-hate relationship for many years.

On the one hand FIs and data are a match made in heaven. It is a symbiotic relationship where business functions create and consume data over and over until the result exceeds the sum of the parts. Ideally this partnering results in revenue or alpha-producing insights. On the other hand, siloed, unreliable or simply too much data creates frustration and risk as the business potential is teased, but ultimately unattainable as FIs struggle to extract value from their data (see figure 1).

Business use cases for leveraging data across financial services are plentiful, from management reporting, enterprise risk, liquidity and treasury management, and more recently, driving innovative customer experiences. More specifically within capital markets and banking, trends such as the embracing of multi-asset trading or the desire to simplify architectures have triggered a rethink of data approaches. There is also, now more than ever, the desire for cost savings – equally important to FIs whose margins are increasingly coming under pressure from increased regulation and competitive factors. Indeed, research by Oliver Wyman and Morgan Stanley found that the benefits from having clean, consistent, and automated data management could be a two-to-four percent reduction of infrastructure and control costs. When IT spend ranges into the billions of dollars, as is the case with larger FIs, every percentage point of savings is a big win.

No wonder then that cracking the data management challenge has long been considered the perfect marriage of technology achievement and business function. FIs have made repeated attempts and invested hundreds of millions of dollars through the years to get this right. From simple relational databases storing structured data, to data warehouses and more recently data lakes capable of holding all types of data, there has been no shortage of excitement that maybe (whisper it) this latest approach could be “the one.” Heartbreaks inevitably followed as the heady days of getting to know new technologies turn into frustrations and recriminations. A pristine data lake becomes a swamp.

The latest research by Celent discovered that leading FIs including Bank of America, Citi, Goldman Sachs, JP Morgan and RBC, to name a few, have lately been getting serious with a new data management approach called Smart Data Fabric. As these entities move from a process- to platform-driven organisation, their business focus has shifted to ensuring the best customer experience possible. This shift however requires mastering and leveraging data to generate insights at an enterprise level. The reality is that a history of disjointed business expansion common to financial services, means data is siloed across numerous platforms, tuned for very different use cases. There are multiple “single sources of truth,” and these vary depending on whose truth you are seeking.

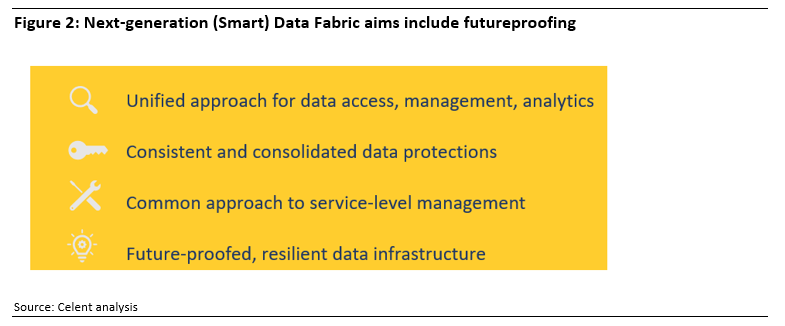

The right data management approach should empower FIs to become better versions of themselves, without fundamentally changing who they are. Unlike previous data management architectures, Smart Data Fabrics offer centralized access and a single unified view of data across the organization. Crucially, Data Fabrics do not require that copies of the data be created and stored outside its original location, so can offer a useful bridging solution between modern and legacy systems – the latter often holding the most business crucial data. In this way Data Fabrics can also avoid the creation of more data silos, which is especially important as FIs increasingly embrace cloud. A Data Fabric becomes “Smart” when it inherently supports advanced data analytics and aims to future-proof data management (see Figure 2).

Financial institutions, from asset managers to banks and brokers, have always known that they need to become smarter about data. Business end-users and clients are demanding better user experiences, targeted insights, and increased access to analytic capabilities which requires free access to accurate and harmonized data drawn from disparate sources across the entire enterprise. At the very core of modernization is the ability to innovate at scale, and this relies on freer access to data. Celent’s latest research report sponsored by InterSystems found that the business necessities and benefits of better data management is driving adoption of Smart Data Fabrics. This time it might just be for real. Read the full report here >>

Upcoming webinar Title: Beyond Images: How Video is Reshaping Digital Customer Engagements in Banking to Drive Agile Growth Date: Wednesday, June 09, 2021 Time: 2:00 pm Eastern Daylight Time Duration: 1 hour

Leading brands are adding real-time video to digital customer engagements as a way to improve customer service and sales effectiveness. Video can enable service and support workers to add human empathy to digital customer engagements. Forrester advises that adding video can boost loyalty and revenue.

Join the latest webinar to explore:

How the COVID pandemic accelerated the need for better digital customer experiences that can convey humanity and empathy

Review real-world success stories of enterprises that have created a video-based “guided customer experience” in their apps and websites to drive higher customer satisfaction, higher revenue, and higher customer retention

The difference between using a third party video meeting tool and adding video-as-a-service embedded into your existing website or app… and which strategy is right for you

Featuring Tom Martin, CEO, Glance Networks and David Penn, Research Analyst, Finovate.

This is a sponsored post from Michael Hom, Global Head of Financial Services Solutions, InterSystems, Gold Sponsors of FinovateSpring.

The banking and finance industry has always been capable of adapting. But as the world recovers from the pandemic, banking and financial services face a new disruption from fintechs and “neobanks.” With lower cost bases and a very different, technology-driven approach to customer experience, these newcomers have been developing fast.

The financial services sector has also experienced a massive rise in digital banking usage caused by the Coronavirus pandemic. For institutions with healthy infrastructure, this was a big positive, whether it was in high net worth advisory or remote banking. It also showed the centrality of high-quality digital user experience to today’s customers.

We must not assume, however, that all is well on the disruptor/innovator side. Some internet-only banks were laying off staff during the pandemic because their ramp-up costs are high – and their paying customer bases are still growing. They also have market share and profit margin challenges through stiff competition from other fintechs.

Established finance institutions, on the other hand, have huge numbers of customers and significant revenue streams. Their challenge: to innovate and make their legacy systems and data management strategies swift enough to keep up with their new upstart challengers. These legacy systems and problems with data management have hampered innovation.

The challenger banks and fintechs, by contrast, are far more agile: they have perhaps two-thirds lower technology costs and offer the interfaces and functionality younger consumers and companies want. They also have investors who support them. Yet they don’t have the scale of the big banks, nor the data. In banking, success is all about scale and achieving it is not easy. Each side also has different cost-pressures. While the fintechs concentrate on the cost of getting a new customer through the door, banking industry incumbents want to be more efficient and reduce the cost of execution.

How the industry will evolve

Large banks know if they get the connection right with consumers and corporations, they will be in a much better position in the next five or ten years. To do this, however, they need the fintechs’ agility. They must simplify their data management so they can adapt to changes in demand rapidly and scale as workloads increase. They must be capable of building and deploying data-intensive AI applications faster so they can transform the user experience for consumers. There needs to be a wider recognition that simpler approaches can be highly effective.

Fintechs and neobanks, on the other hand, need a compelling value proposition to attract consumers and generate meaningful revenues.

This is why the incumbents and the fintechs will draw closer through collaboration or acquisition. By collaborating with incumbents, fintechs and neobanks can use their digital skills and innovation to make niche areas of the established institutions’ operations far more profitable while benefiting from access to a massive customer base it would otherwise take them years to acquire.

Modern data management technology such as microservices, APIs and API management, have lowered barriers to publish and consume services, creating a dynamic ecosystem that allows organizations to focus on their core competencies and differentiation. They can rely on the ecosystem for commoditized, non-core, and non-differentiating capabilities.

Acquisition, on the other hand, brings its own problems, since the pace of innovation often slows once a young organization has been bought by an established competitor.

For these reasons, we may see a hybrid model between collaboration and acquisition, in which the big incumbents develop through consolidation into aggregators, becoming open banking marketplaces and acting as the nexus between customers and services. A new digital retail bank may, for example, use a major player’s credit expertise, risk and control mechanisms while designing a new user experience from scratch.

Whichever model of cooperation it is, the new offerings devised together by incumbents and fintechs will have to stand out. With so much competition, differentiation through excellence in technology, customer experience and support will be essential.

What does the future require?

Agility is vital to the future of banking and should be a major aim for all ambitious financial organizations. Mindsets must change as well as technology.

From now on, senior management in banks must think like their counterparts at software companies. That means constantly gleaning what is going well or wrong and acting on it. When there are problems, they should be fixed before customers are fully aware. Many neobanks are leading the way on this, updating their apps weekly. Big banks, by contrast, are much slower, updating apps yearly or quarterly, with a few in the four-to-six week timeframe. This has to change.

When deciding how to transform, incumbent organizations must ask themselves how they are addressing client and employee needs in terms of products, services, and information. They must build a picture of where banking is going and be confident they are heading in the same direction. Established banks must become product-oriented organizations just like digital native rivals, abolishing internal boundaries and creating cross-functional teams under product owners.

Keep the organizational DNA alive

Scale, innovation, and agility have become vital attributes in banking. Yet as incumbent institutions adapt and assess which newcomers to partner with or acquire, it is essential they do not lose sight of what it is that makes them special or forget what their goal is. Banks are still about people, processes, and technology, and the people side of the business is where high levels of service and distinctiveness enable the organization to stand out and build profitable long-term relationships.

If organizations lose their DNA, they will crumble. Incumbent banks have a larger and more diverse customer base that is difficult to please and, in today’s world, less likely to tolerate low levels of service from loss of organizational focus.

Established banks must be as nimble as possible and collectively approach their work as if their business model is at risk every day. It is not only digital transformation that is necessary, but also a mental mind-shift. Only then can banks believe they are on the path to digital transformation, resilience, and long-term profitability.

Upcoming webinar Title: Innovating for success: How insurers can embrace innovation to drive growth Date: Tuesday, May 18, 2021 Time: 02:00 British Summer Time Duration: 1 hour

Technology and innovation are key to driving growth and creating scalable and agile business models in a challenging environment. It is an exciting time for insurers and many are seizing this opportunity to transform by investing in innovation, accelerating the evolution to digital, and evolving in ways that appeal to customers.

Join our latest webinar to explore:

Is innovation important and why?

Are insurers truly getting return from their investment in innovation?

What insurers can do so that their innovation endeavours lead to genuine growth?

Top tips that drive innovation – critical tasks and internal challenges?

How insurers can build an innovation funnel /roadmap?

Featuring Preetham Peddanagari, Digital Insurance Leader, EY EMEIA; Roy Jubraj, Chief Strategy & Transformation Officer, esure Group; Emmanuel Djengue, Innovation Director, RGAX Europe and Marcin Kurczab, Head of Innovation Lab, PZU Group.

Julie Muhn chats with Rita Martins, FinTech Partnerships Lead – Innovation Finance and Risk at HSBC about her experience as a woman in fintech, trends she’s seeing across the industry, and what can be done to encourage more female founders.

Tell us about yourself and your career path to your current role.

RitaMartins: My career started with an internship at Santander in Asset Management managing mixed portfolios. After a few months, a great opportunity came up to join the consulting world. Working at Ernst and Young and later at Accenture, I travelled the world driving large scale transformation projects and advising C-Suite on the applicability of new technologies in finance. During this time, I started diving into the fintech world and noticing first-hand how fintechs were making a difference in developing countries (despite challenging conditions, everyone had a phone and used it for payments).

In 2018 I moved to HSBC, where I currently Lead FinTech Partnerships for Finance and Risk. I am responsible for managing relationships with third parties and driving collaboration between fintechs and traditional financial services SMEs.

What trends are you seeing driving fintech this year? Are they different to previous years, or when you first started in the industry?

Martins: Nowadays, fintech companies are much more mature than when I started in the industry. Fintechs discovered where they can have an impact and when to partner with others in the market.

This year we continue to see fintechs emerging in the Artificial Intelligence (AI) and Cloud spaces. Additionally, there is a new trend in ESG (Environment Social and Governance), with many new fintechs researching and developing solutions in this space.

In your opinion, what is the secret to a successful partnership between bank and fintech?

Martins: There isn’t one factor but a combination of factors that lead to a successful collaboration. Before a partnership is created, both parties need to understand if their culture, goals, and strategy are aligned. An ideal partner will be someone who complements the other and brings new ideas to the table to ensure continued innovation.

After papers are signed, there needs to be an open and frequent dialogue to ensure issues are quickly solved, targets are met, and any changes needed are settled.

What is important to you to see from a fintech leader/ founder of a new start-up you’re looking to work with?

Martins: A fintech-bank partnership is much more than finding great technology; human interaction is vital. When looking for new partners, the fintech leader or founder is often the one representing the company, so in the initial discussions, we would be looking at a combination of factors:

1. Their knowledge of the technology and industry

2. Their values and how they connect with our team

3. How innovative they are and what new ideas they bring to the table

4. What their goals for the partnership are, and how flexible they are

Do you see many women leading fintechs or in senior positions? Is there enough diversity across the board in these roles?

Martins: No, there is still a noticeable lack of women and minorities in senior positions and even fewer women founders.

Typically, women who work in fintech will have roles in sales, communications, or marketing with a noticeable gap in the technology and senior roles.

So, what can the industry do to better encourage women to get involved with fintech?

Martins: I would challenge the industry to do more at the senior level. Those changes will empower young women to join the industry, retain existing leaders, and decrease the pay gap.

Two key areas that need immediate change are:

More investment needs to go into female-founded fintechs. In 2020, only 2.3% of VC capital went to female-only founded start-ups (according to Crunchbase)

Banks and fintechs boards and leadership need to be more diverse. In 2020 women represented only 14% of fintech boards (according to Oliver Wyman)

Listen to more from Rita as she looks back on her experience at FinovateEurope 2021 below

One of my favorite sayings about digital banking is that the largest branch in the world is now in your pocket.

The retail banking customer journey has become more complex than ever before. Each day, clients are moving between a number of devices, which means that banks need to find new ways to study, monitor, view, and study the cross-device journey, especially on mobile devices.

It goes without saying that, for traditional retail banks, Covid-19 accelerated the shift to digital. But in-person branch use was already declining before that.

The good news for retail banks? Current federal regulations mean that elements of the in-person experience will remain important, so branches aren’t disappearing entirely. In addition to finding ways to boost in-person engagement at branches, retail banks have the extra challenge of offering omnichannel digital experiences that are on par with those offered by the latest fintech startups, like Robinhood, as well as other household apps, such as Amazon, Airbnb, and Twitter.

The boom in fintech, and especially the rise of neobanks like Chime and Ally, means that more clients are choosing banks that don’t offer in-branch services, where customers get the typical one-on-one service from a teller. Popular peer-to-peer and peer-to-business payments services such as Venmo, PayPal, Square, and CashApp have put additional pressure on retail banks to offer standout mobile experiences.

As traditional banks look to remain competitive with fintech startups, they will need to offer digital experiences that streamline everyday banking processes. Clients want to open new accounts, apply for credit cards, and deposit mobile checks with as few clicks as possible, and directly from their mobile devices.

Fintech startups have a leg up on retail banks because they offer fewer services and leverage the most advanced cloud technology. Many retail banks are burdened by legacy platforms, outdated processes that slow things down, and poor alignment within the organization.

Many banking clients miss the benefits of in-person engagement, especially seeing a friendly face at their local banking branch. Retail banks can approximate the friendliness of in-person service by doubling down on their digital channels, which means offering applications with intuitive user interfaces and user experiences. Above all, people want simplicity, transparency, and speed.

Banks and other financial institutions have the added burden of navigating complex federal regulations. These institutions are responsible for safeguarding clients’ money and remaining compliant with both local and federal laws. A few small errors can not only break trust with clients, but lead to millions of dollars worth of fines.

As banks double down on digital channels, they need to introduce the perfect amount of user friction for tasks such as opening accounts, filling out loan applications, and transferring funds. One small click can lead to major problems or misplaced funds, so making clients re-enter passwords or confirm transactions can build major trust.

On the other hand, too many steps in a workflow leads to abandoned applications, lower conversion rates, and frustrated customers. Worse yet, clumsy designs and technical errors often make it impossible for clients to complete tasks without assistance from a call center. There will always be technical errors, and to solve this, banks can put clients in contact with agents by providing pop-ups that include a direct phone number or a chat window when a problem arises.

Once banks have the basics down, they can invest in hyper-personalization, which helps clients feel more connected to their products. Erica, Bank of America’s Voice Assistant, has helped revolutionize the mobile banking experience. The AI-powered chatbot helps clients answer pressing questions about their banking needs, making it easier for them to find answers for common questions.

As retail banks rebound from the Covid-19 pandemic, they will need to engage in data-driven design thinking to ensure that each digital product decision benefits clients. That is why we have built the Quantum Metric platform, which helps retail banking teams act with more agility. Our methodology, known as Continuous Product Design, helps teams from across an organization align on the product decisions that will have the greatest impact on customers and the business’s bottom line.

In today’s digital-first world, retail banks need to identify problems before they impact a large segment of users, as well as anticipate potential issues as before they happen. That’s why our platform offers real-time analytics and anomaly detection technology. Our platform can help digital teams at retail banks pinpoint a broken button that causes conversion rates to plummet, pinpoint fraudulent activity from bots (e.g., too many login attempts), and much more.

Once retail banking teams get a handle on their omnichannel experience, they can begin expanding into other services and offering additional resources, such as financial education resources. The move to digital provides ample opportunities for diversification. Now banks need to use data-driven design thinking to determine what’s next.