This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

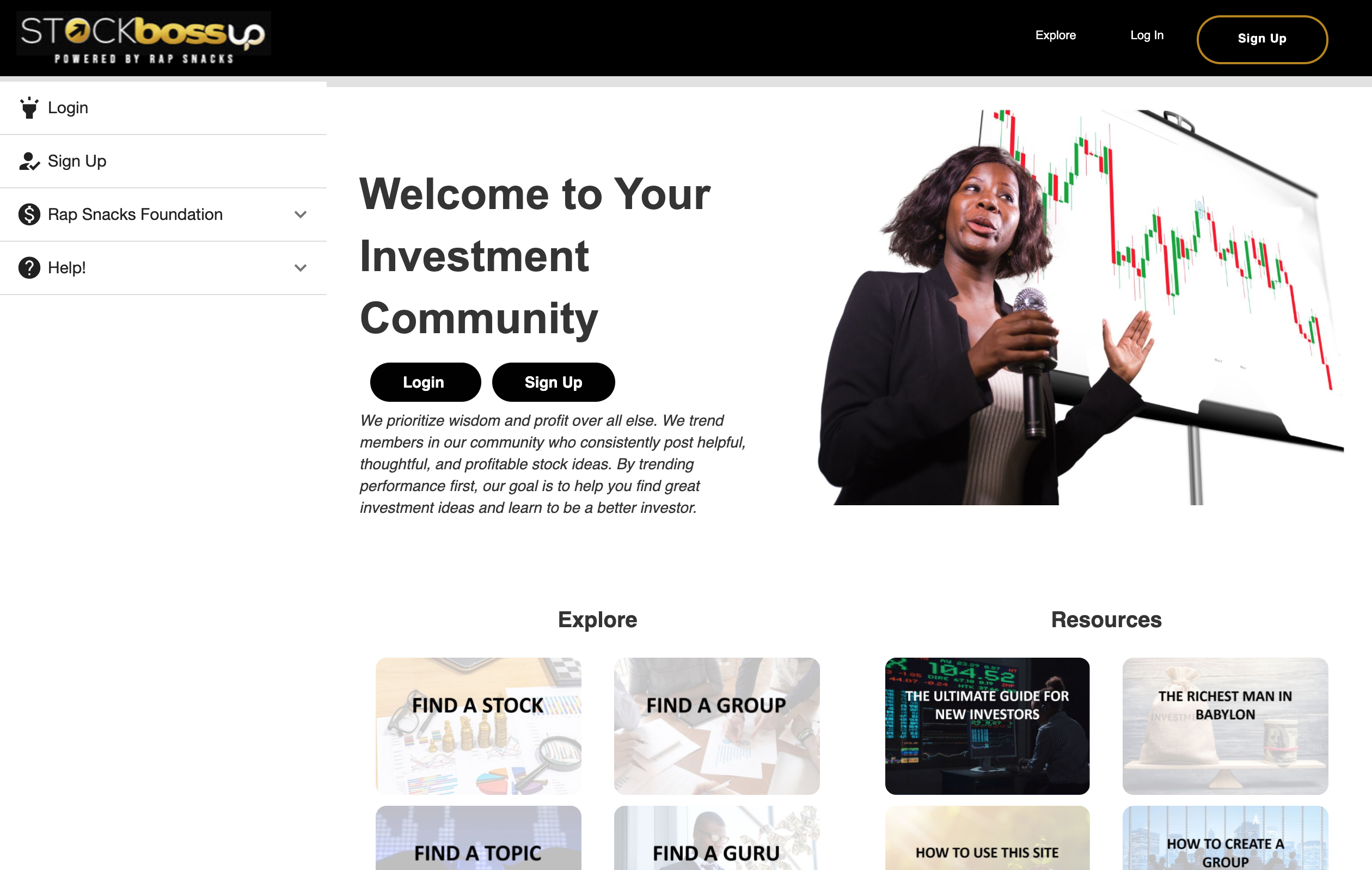

Stockbossup prioritizes wisdom and profit over all else. It trends members in its community who consistently post helpful, thoughtful, and profitable stock ideas.

Features

Engages users with investment ideas

Finds the best investment opportunities for your financial needs

Trends members in the community with profitable stock ideas

Why it’s great Stockbossup is a social media platform focused on engaging beginner and retail investors in the stock markets by trending performing stock picks.

Presenter

Chaster Johnson, CEO Johnson has 9 years of experience as an Aerospace Manager, one year of experience in the cryptocurrency hedge fund market, and two years spearheading the Stockbossup platform. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

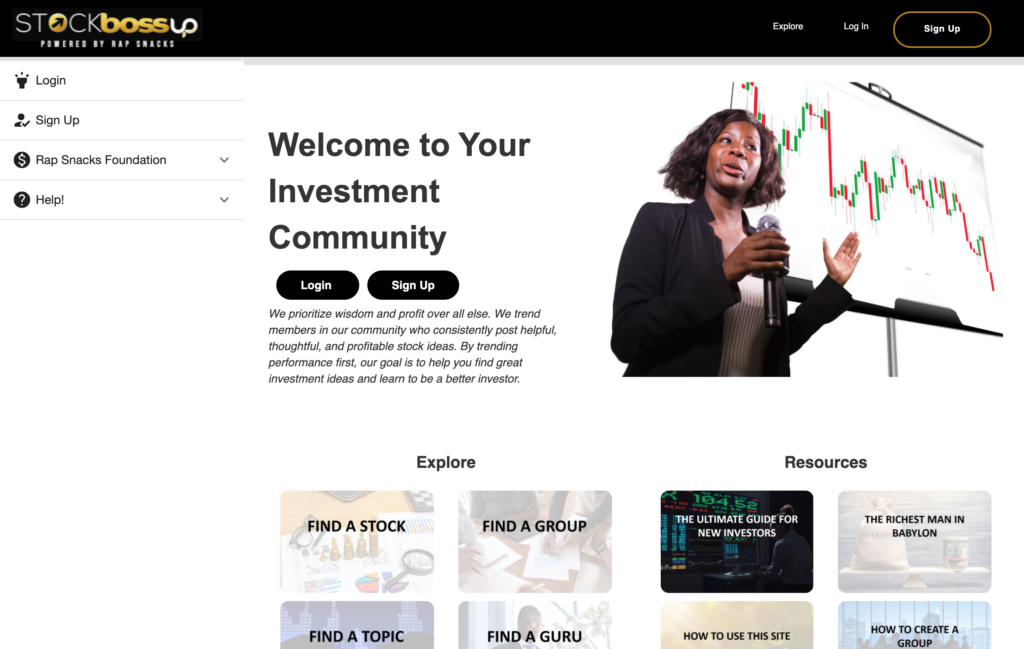

Railz is building the largest financial data network. It is a single point API connecting you to all major accounting service providers.

Features

API to all major accounting service providers

Normalization engine to organize messy data

Analytics and insights on your commercial customer financial data

Why it’s great Railz has the ability to normalize messy accounting data through its proprietary machine learning algorithm.

Presenter

Sohaib Zahid, CEO & Co-Founder Zahid is a serial entrepreneur with a decade of successful experience in building teams, products, and companies. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

MOSTLY AI‘s synthetic data platform allows users to replace sensitive data sets with programmable, synthetic lookalikes to accelerate AI, data science, and product development in a privacy-safe way.

Features

Fully automated synthesization process for easy use

Multi-table with referential integrity for synthesizing entire databases for testing

Programmable, better-than-real data for AI training

Why it’s great You can never have enough of the right data. MOSTLY AI’s synthetic data platform creates the data you need and more, using the data you have.

Presenters

Alexandra Ebert, Chief Trust Officer Ebert is MOSTLY AI’s Chief Trust Officer, AI, privacy, and GDPR expert with a deep understanding of the potential synthetic data unlocks for financial institutions globally. LinkedIn

Jim Hu, Pre-Sales Solutions Engineer Hu has ten years of experience in global tier-one investment banking and asset management firms. He specializes in applying synthetic data to business-driven financial applications. LinkedIn

Financial data and infrastructure platform Plaidannounced today that it received an undisclosed amount of new funding from J.P. Morgan Private Capital Growth Equity Partners and Amex Ventures, which first invested in the California-based company in 2016. The new round boosts Plaid’s total funding somewhere north of $724 million.

In a statement, the company said that today’s investment will help it “further accelerate efforts to meet rising consumer demand for digital finance; a shift powering the rapid growth of Plaid’s diverse customer ecosystem.”

The funds are an add-on to the company’s $425 million Series D round announced in April. While that investment valued Plaid at $13.4 billion, today’s new funds do not alter the valuation.

This may be J.P. Morgan’s first investment in Plaid, but the two have been data partners since 2018. There is also a storied history between Plaid and J.P. Morgan CEO Jamie Dimon. Earlier this year Dimon cited Plaid as an example of a company that improperly uses client data. However, Dimon did not cite any specific scenarios to back up his accusation.

Plaid was founded in 2013. The company builds APIs to connect consumers, financial institutions, and developers. Plaid also offers a suite of analytics products that provides further insights into transactions. As the rise of open finance in the U.S. has begun to impact firms both in and out of fintech, Plaid is on its way to becoming a household name.

“While we’re still in the early innings of the digital transformation in financial services,” said Plaid CEO Zach Perret, “we’re excited to work with the thousands of banks, fintechs and non-financial institutions in our network to create what’s next.”

In a round led by Sequoia Capital Global Equities, Chime Financial has raised $750 million in new funding. The investment gives the San Francisco, California-based company a valuation of $25 billion and likely anticipates the firm’s debut as a publicly listed company next year.

Also participating in the Series G round were SoftBank’s Vision Fund 2, along with existing investors Dragoneer Investment Group, General Atlantic, and Tiger Global Management. Chime CEO and co-founder Chris Britt said that the new funding would help support the company’s growth as well as the launch of new services. Chime also introduced a trio of independent directors to its board: Cynt Marshall, CEO of professional basketball team the Dallas Mavericks; Jimmy Dunne, Vice Chairman of investment bank Piper Sandler; and Sue Decker, founder and CEO of community building platform Raftr.

Founded in 2013 by Britt and current Chief Technology Officer Ryan King, Chime gives consumers a digital-first alternative to traditional banks. Chime offers an online checking account with no hidden fees or overdraft charges, and a spending account with a Visa debit card with no minimum balance or monthly fees. The company has an early payday service for customers who choose direct deposit, no fee money transfers, and a “credit builder” program with a secured, Visa-branded credit card to help customers improve their credit scores.

Chime’s banking services are provided courtesy of a partnership with The Bancorp Bank or Stride Bank (issuer of Chime’s Visa Credit Builder Card). With more than eight million account holders – and on track to reach more than 13 million account holders this year – Chime reached EBITDA profitability last year during the COVID-19 pandemic, according to CNBC.

In the latest fintech tie-up, Paysafe has acquiredSafetyPay. The all-cash transaction marks Paysafe’s 13th acquisition and is expected to close for $441 million in the fourth quarter of this year.

Paysafe aims to leverage Florida-based SafetyPay, which has locations in 16 countries– 11 of which are located in Latin America– to boost its own presence in that geography.

SafetyPay was founded in 2006. The company enables users to make online cash payments, bank transfers, and cross border transactions without a payment card. The company’s network includes more than 380 banks and it works with 180,000 brick-and-mortar locations as cash collection points.

U.K.-based Paysafe was founded in 1996 and offers similar payment services as SafetyPay, including an online cash payments tool. Paysafe also provides digital wallets, standalone and integrated point of sale tools, and a digital marketing marketplace where advertisers can acquire new customers, monetize their traffic and generate revenue through partnerships.

Once the acquisition closes, the SafetyPay team will work as part of Paysafe’s eCash and online banking solutions group. SafetyPay CEO Gustavo Ruiz Moya will become CEO of eCash for Latin America and Global Head of Open Banking.

Paysafe’s previous acquisitions have greatly increased the breadth of its services. The company’s brands include Income Access, Paysafecard, Paysafecash, Neteller, Petroleum Card Services, and Skrill. Among Paysafe’s clients are MindBody, RentMoola, Policy Expert, and Amilia.

From the snap election called by Canadian Prime Minister Justin Trudeau to the country’s recently expressed eagerness to accept refugees in the wake of the U.S. withdrawal from Afghanistan, there have been more than a few reasons for the Great White North to make news headlines of late.

Now fintech fans in particular have another reason to pay attention to what’s going on in the chronically under-discussed nation. FreshBooks, a cloud accounting software company based in Toronto, Ontario, has raised $130 million in new funding. This gives the firm a valuation of more than $1 billion, becoming Canada’s latest fintech unicorn.

FreshBooks CEO Don Epperson said that the funding, which included $50 million in debt financing, was an “injection of confidence” in the company’s mission to help small businesses digitize their accounting operations. Epperson added that the capital will fuel investment in markets that are experiencing significant increases in regulation and help those small business owners better “manage their finances” by “simplifying workflows.”

The Series E round was led by long-time FreshBooks investor Accomplice. Also participating in the funding were J.P. Morgan, Gaingels, BMO, and Manulife. New investor Barclays, one of FreshBooks’ platform partners, was also involved in the financing.

Founded in 2003, FreshBooks is active in more than 160 countries, including Croatia, Mexico, the Netherlands, and the U.S. – as well as its native Canada. The company’s technology has helped more than 30 million people better manage their finances, billing operations, and payments, while increasing customer engagement with its ten-time Stevie award-winning customer support. In July, the company announced that it was teaming up with the Ontario government in a data-sharing partnership to help understand the impact of the COVID-19 pandemic on small businesses. In May, FreshBooks co-founder Mike McDerment was featured in Profiles in Leadership where he discussed the company’s origins from its humble beginnings in “his parents’ basement” to the 500-employee company that is now among the top cloud accounting software firms in the world.

Here is our look at fintech innovation around the world.

It seems like only yesterday when Finovate VP and host of the Finovate Podcast Greg Palmer was introducing his first guest (Jim Bruene, founder of Finovate, by the way). Nearly two years later, having sat down with fintech innovators and influencers from Jim Marous and Louise Beaumont to Brett King and Tosin Agbabiaka – Palmer is celebrating the 100th episode of the Finovate Podcast.

In this centennial edition, Palmer discusses the Three Gold Rules of Fintech that he has learned from his years in the industry and the conversations he’s had – both on-air and at our Finovate conferences – with professionals from every corner of the fintech and financial services ecosystem.

Launched in 2019, the Finovate Podcast began as a way to continue and extend the conversation beyond the live demoes and insightful observations of our fintech conferences. In the months and years since, the program has grown into one of the key forums for fintech’s most visionary entrepreneurs and thought leaders to discuss the most important trends in our industry – from the rise of challengers and neobanks to the growing emphasis on financial inclusion and bringing banking to underserved communities around the world.

Check out the 100th episode of the Finovate Podcast featuring the Three Golden Rules of Fintech – and then visit the Podcast archives for hours of great conversation and valuable insights into trends driving one of the fastest growing fields in technology today.

We spoke with Pauline to discuss the importance of DEI in current fintech trends, the benefits of finding one’s community, and her journey to founding Pasito, the fintech that delivers financial wellness through inclusive employee benefits.

Pauline will be joining our Women In Fintech Power Panel: Paving The Way For The Next Generation Of Female Founders & Executives – How Can We Reach A Gender-Neutral Future In Financial Services? at FinovateFall next month.

Tell us about yourself.

Pauline Roteta: I went to college to be a Civil Engineer. Growing up in a small town in Argentina, I was awestruck by the sheer size of development in New York and wanted to be part of that continuous cycle of growth. While I cherish the process thinking engineering gave me, after a couple of civil and construction internships, I was hired by Goldman Sachs for the summer and have never looked back.

In finance, I found a community of the sharpest minds tackling global challenges and saw the opportunity to effect impact at scale.

Now a decade later, I can safely say that finance has given me the development and growth I was after. I’ve been part of teams that grew multi-billion dollar businesses from scratch, led acquisitions, raised private equity funds, and I have been the most senior female investor of a private markets investment fund. In 2021, with this experience under my belt, I co-founded Pasito, a female-led fintech delivering inclusive benefits for working parents. As a founder and business leader, I am now even more excited than at the start of my career for the tremendous growth opportunity ahead for fintech companies like Pasito.

How have you seen the industry change across your career?

Roteta: So much has changed in 10 years. When I first joined BlackRock, we were focused on the European Debt Crisis and unraveling legacy portfolios from the 2008 Financial Crisis. While technology was important to the business model, most of our analysis and delivery was in person. The active-passive debate was just starting. Fintech wasn’t mainstream and wasn’t seen as a threat by incumbents.

Fast-forward to today: we’ve seen a proliferation of fintech companies that are effectively competing with long-time incumbents in wealth, banking, and payments. In the space where we are building, there has been less disruption. Plan administrators continue their manual processes. Technology looks like it’s from the first days of the internet. Customers haven’t yet been delighted. Pasito is working on changing that.

Where do you see fintech heading in the next 12 months?

Roteta: After the events of 2020, financial health and diversity, equity, and inclusion will remain top of mind for businesses and the government. We’re seeing employers treat financial and mental wellness with the same care that they treat physical health. That’s a huge win for the retail consumer and creates an opening for new business models in fintech to fill in the gap left behind by wealth management.

When it comes to DEI, we see fintech pushing the boundaries of financial product and service personalization.

While we’ve seen an explosion in fintech, it’s important to remember most of the big problems remain without a solution. The U.S. has never been more unequal. The wealthiest families, who are primarily white, own most of the stock market. Black and Latinx families have limited access to financial advice, and their assets amount to a fraction of the average American household wealth. At Pasito, we are working on closing this gap, one product at a time. Our hope is that more fintechs will build with this mission in mind, rather than continuing to develop products that solidify the status quo.

What more do you think can be done to support women in fintech?

Roteta: We have a long way to go in fintech to reap the benefits of a diverse workforce. The easiest way to begin this work is for leaders in the space – both men and women – to first look inward and ask:

What am I doing to actively advance women in fintech?

How am I contributing to female-founded and women-led companies and initiatives?

How many women are working for my company? (if the answer is not many, then ask WHY?)

How is my culture inclusive and inviting to women?

The second easiest way to support women in fintech is to simply listen. What do women need to join the industry? If you ask, they will tell you. (Hint: it usually boils down to equal pay, family-friendly benefits, and flexibility.)

Lastly, invest social and financial capital in women. Women with powerful ideas will not only increase the return on your investment, but also the overall positive impact you can have on the world.

Where did you find support in the fintech world?

Roteta: We’ve seen tremendous support from Startup Boston, Parenthood Ventures, The Capital Network, other fintech founders, and personal mentors. The insight and community from these networks have been invaluable for Pasito’s early growth stage. Our leadership team is now paying it forward to other founders, so we can collectively level the playing field in hiring, building, and fundraising.

What advice would you give to women starting their careers in the industry now?

Roteta: Be confident. Find your community. Listen to founders who have been there before. Conduct market validation before spending your money. Be selective of your investors. Above all else, stay true to your mission and values.

After a year of hosting our fintech conferences in an all-digital format, FinovateFall 2021 marks our return to in-person events. We’ll be back at the Marriott Marquis Times Square in the heart of New York, from September 13 through 15, 2021. Make sure you check out the agenda and book your ticket!

FinovateFall is your chance reconnect face-to-face with the fintech community and plot your course for the future. With live demos of innovative fintech solutions, expert advice from key influencers, and unparalleled networking opportunities, there’s no better place to find your path forward. It’s up to all of us to define what “normal” is going to look like in the future, so join us next month at FinovateFall and make sure you’re a part of the discussion!

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

Infocorp has created a user-centric, mobile native banking app. It’s a personalized experience for every user.

Features

Delivers a hyper-personalized experience for each user

Shows relevant content and gives proactive advice

Integrates with other services to increase app usage

Why it’s great We are disrupting the whole bank app traditional concept.

Presenters

Ana Inés Echavarren, CEO Echavarren is a Systems Engineer and MBA, with a solid track record in the financial software market. She helped make the company a benchmark in digital channels for banking in Latin America and the Caribbean. LinkedIn

Gonzalo Laguna, Product Manager Laguna is the Product Manager at Infocorp and Professor of Software Architecture & Design on the Engineering faculty at ORT University, Uruguay. He is the former member of the Microsoft Regional Director program. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

Long Game‘s gamified finance app helps banks acquire new customers and increases engagement with their current customers in the Millennial and Gen Z demographics.

Features

Engagement with bank products

Acquisition of new accounts

Promotion of financial literacy

Why it’s great Long Game is a turn-key, bank-branded mobile game that drives new account sign-ups, savings, financial literacy, and brand affinity with Millennial and Gen-Z customers.

Presenter

Lindsay Holden, CEO & Co-Founder Holden is Co-Founder and CEO of Long Game, a mobile app that uses gamification and behavioral finance to make finance fun. LinkedIn