This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Trustly, the company that helps customers pay directly from their bank account, launchedInstant Payouts for U.S. users this week.

The service helps U.S. businesses provide their clients with near-instant payouts to their bank accounts. Instant Payouts in the U.S. is made possible via a partnership with Cross River Bank, which participates in The Clearing House’s (TCH) RTP network, a real-time payments rail.

Trustly’s business users can fund payments with Cross River Bank, which will send RTP payments on their behalf to their customers’ accounts at other participating RTP banks.

“The RTP network provides a platform for financial institutions and their corporate users to create innovative new payment products for their customers,” said TCH SVP of technology and Innovation Bijan Chowdhury. “Trustly’s partnership with Cross River Bank to deliver Instant Payouts to U.S. businesses and Cross River Bank’s use of the RTP network to send instant payments to the the businesses’ customers illustrates the power of the RTP network to boost innovation in the payments industry.”

Trustly was founded in 2008 and supports card-not-present payments for online merchants to offer a secure way for consumers to transact using their online banking access credentials. Last year, the company processed over $21 billion in transaction volume in its network. At FinovateEurope 2017, the company debutedDirect Debit, a payment offering that removes the pain of entering payment card information by allowing users to transact using their current account by entering their bank login credentials.

Trustly works with more than 8,100 merchants, helping them connect with 525 million consumers and 6,300 banks across 30 countries. The company has 500 employees across Europe, North America, and Latin America.

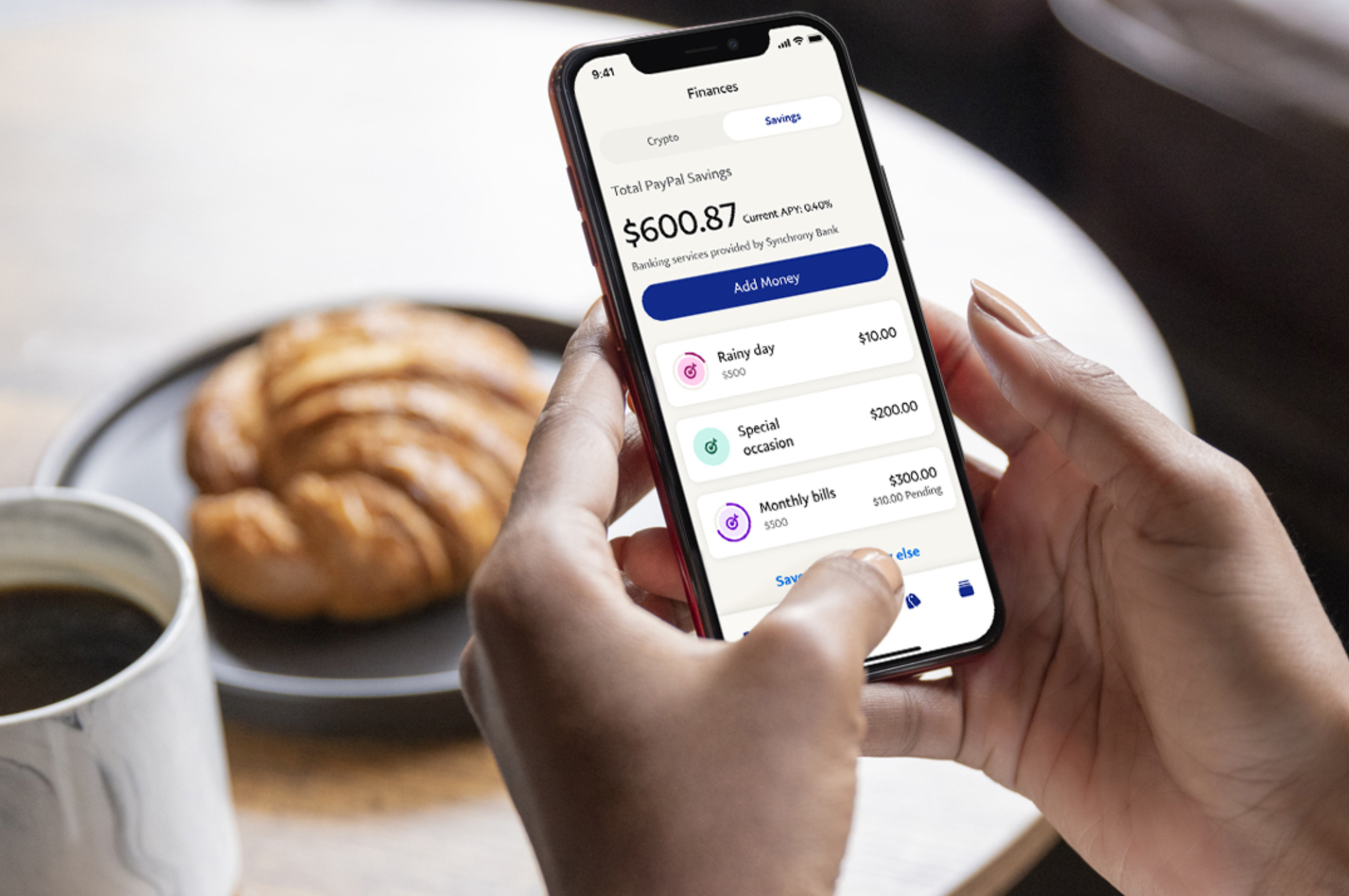

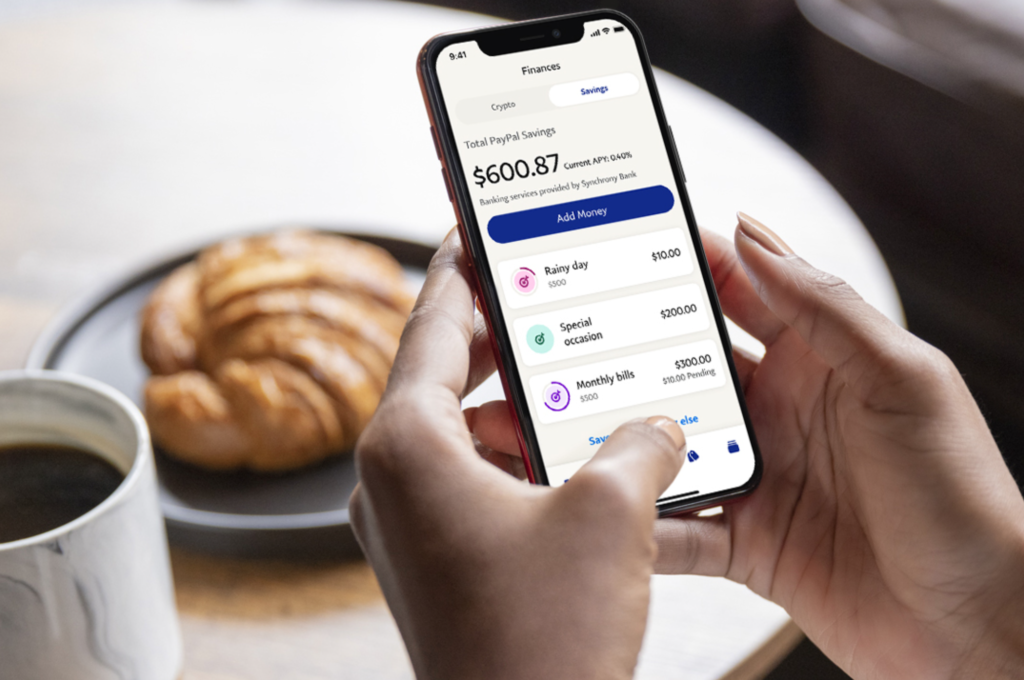

The company is adding a handful of features that bring it into “super app” territory, competing with the likes of WeChat, Alipay, and Paytm. PayPal’s app already offers a peer-to-peer payment tool, a mobile wallet, and a charity donation feature.

The new release, however, will offer more features and new banking capabilities. Here’s a rundown of what to expect:

PayPal Savings, a new, high-yield savings account provided in partnership with Synchrony Bank that pays 0.40% APY

In-app shopping tools that allow customers to discover and earn loyalty rewards

Billpay management tools that help users track, view, and pay their bills

A new Direct Deposit feature that fronts users their paycheck up to two days early

Rewards capabilities

Gift card management

Credit access

Buy Now, Pay Later services

Crypto purchasing, holding, and selling abilities

The app will show users a personalized dashboard of their account; a wallet tab to manage payments and direct deposits; a finance tab to access savings and crypto accounts; a payments tab that enables users to send and receive money, make a donation, and manage billpay; and a messaging feature built around peer-to-peer payments.

“We’re excited to introduce the first version of the new PayPal app, a one-stop destination for our customers to take charge of their everyday financial lives, with new features like access to high yield savings, in-app shopping tools for customers to find deals and earn cash back rewards, early access Direct Deposit, and bill pay,” said PayPal CEO Dan Schulman. “Our new app offers customers a simplified, secure and personalized experience that builds on our platform of trust and security and removes the complexity of having to manage multiple financial or shopping apps, remember different passwords and track loyalty rewards.”

What’s next for PayPal’s Super App? The company will add investment tools, offline QR code payments, and new shopping and deals capabilities.

PayPal is currently the closest thing the U.S. has to a super app. However, the new app is still missing some key elements that Asia’s successful super apps have, including food delivery, transportation, travel, health, insurance, government, and public services.

A strategic partnership between Finovate alums Q2 and Plaid will give 18 million consumers across more than 500 banks and credit unions the ability to access 5,500+ fintech apps and other digital banking features. The alliance, announced today, combines Q2’s digital banking platform and Plaid’s open finance platform, Plaid Exchange. The goal is to provide customers with a secure and reliable way to both connect accounts to digital apps and services, as well as give them the tools to manage these connections.

“At Plaid, we believe all consumers should have access to digital financial services, regardless of where they bank, and the Q2 team shares this same mission,” Plaid director of strategic partnerships Reed Bouchelle said.

The partnership also will enable Q2’s financial institution customers to leverage Plaid’s APIs to give accountholders fast, easy, and secure digital account funding. New customers will be able to save time and effort by linking their bank accounts during the account opening process to fund new accounts in seconds rather than days.

“Our partnership extends beyond data access,” Bouchelle continued. “With Plaid, Q2 financial institutions will enable consumers to more easily fund new accounts and see a holistic view of spending and net worth across all of their financial accounts,” he said. Bouchelle credited a quartet of Plaid solutions – Exchange, Auth, Identity, and Transactions – for ensuring the comprehensive nature of the new functionality.

Q2 Chief Technology Officer Adam Blue highlighted the needs of financial institutions serving diverse communities in emphasizing the importance of the partnership with Plaid. “To stay competitive in the market, and provide unparalleled customer experiences,” Blue said, “FIs need to offer the services their customers expect. By integrating Q2’s digital banking platform with Plaid Exchange, Q2’s financial institutions will be able to effectively partner with fintechs while providing improved end-user experiences to their customers.”

Austin, Texas-based Q2 was founded in 2004 and made its Finovate debut (as Q2ebanking) at FinovateSpring seven years later. The digital banking and lending solution provider went public in spring of 2014 under the ticker symbol QTWO, and currently has a market capitalization of $4.8 billion. The company’s Plaid partnership announcement comes just weeks after Q2 inked a deal with Stanford Federal Credit Union ($3.6 billion in assets; 77,000 members) to deploy both its digital banking platform and its Q2 Innovation Studio. Q2 also recently announced core processing partnerships with b1BANK ($3.9 billion in assets), Citizens Bank of Edmond ($350 million in assets), and fellow Finovate alum Moven.

Financial data network Plaid works with more than 11,000 financial institutions to ensure broad access to the thousands of digital financial services built on its platform. Making its Finovate debut in 2014 as a presenter at FinDEVr SiliconValley where the company demonstrated its “API for Financial Infrastructure,” Plaid has become synonymous with the movement to democratize digital finance. The company secured a Series D extension – amount undisclosed – from American Express and JP Morgan in August and, later that month, announced a new partnership with advanced bank-to-bank transfer solutions company Astra. Earlier this month, Plaid announced a collaboration with Silicon Valley Bank to make the institution the first to offer ACH account token integration with its technology.

“With Silicon Valley Bank,” Plaid Head of Revenue and Partnerships Paul Williamson said when the partnership was announced, “thousands of fintech innovators now have access to an integrated payment processing solution that combines the power of SVB and Plaid to deliver seamless, convenient digital finance experiences.”

Plaid was founded in 2013 by William Hockey and Zachary Perret (CEO). The company achieved unicorn status in 2018 after securing a $250 million Series C investment that gave the San Francisco, California-based firm a valuation of $2.65 billion.

In a round led by Valar Ventures, Neo Financial, a fintech based in Alberta, Calgary and Manitoba, Winnipeg, has raised $50 million ($64 million CAD) in new equity funding. The fresh capital takes the Canadian company’s total funding to $89 million ($114 million CAD), and will help enable the company to add talent and launch new integrated fintech partnerships with retailers.

“Reimagining the way Canadians bank is no easy feat, but it’s a challenge that our team is taking head on,” Neo co-founder and CEO Andrew Chau said. “This raise is validation of not only the problem Neo is tackling, but (also) our team’s ability to solve it.”

Going live last year, Neo offered a high-interest savings account, and a no-fee Mastercard that offers up to 6% cash back at partnering companies and at least 1% cashback across all other spending, called Neo Card. Since its 2020 launch Neo has inked partnerships with more than 4,000 retailers, including a strategic partnership with Hudson’s Bay to power the company’s new Hudson’s Bay Mastercard offering. Today’s funding announcement comes on the heels of Neo’s purchase of office space in Winnipeg’s Exchange District, enabling the company to open a second headquarters in the city.

Joining today’s Series B were new investors Greenoaks Capital – which has backed fintechs and ecommerce innovators like Robinhood and Stripe – as well as South Korean challenger bank Toss, a unicorn valued at more than $7.3 billion ($9.4 billion CAD). Other investors included Breyer Capital, Golden Ventures, Afore Capitaal, Inovia Capital, Thornvest, and Maple VC. In addition to leading Neo’s Series B round, announced today, Valar Ventures also led the company’s previous round of funding – a $19.5 million (CAD $25 million) Series A round – in December 2020.

“As one of the largest Series B raises for a Canadian fintech, this new round of funding will allow us to continue building innovative products and features for all Canadians and businesses,” Chau said. “It’s an exciting time to grow our team from both our Calgary and Winnipeg offices.”

Neo Financial was founded by two of the co-founders of SkipTheDishes, an online restaurant food delivery firm launched in 2012. SkipTheDishes was acquired by JustEast four years later for $200 million.

The payments space is one of the areas within fintech that has benefitted from the acceleration in digital transformation trends over the past year. And within the payments industry, innovation in billpay has been especially vigorous, as a growing number of individuals and businesses turned toward digital channels to make and receive transactions during the COVID-19 crisis.

We caught up with Anne Hay, Head of PayNearMe’s consumer research initiative, to discuss the company’s new collaborations with Green Dot and Walmart, as well as PayNearMe’s findings from a study of consumer payment preferences the company launched earlier this year. Have consumers become more or less interested in digital payment solutions since the pandemic? And what can financial services organizations do to take advantage of these trends? Anne Hay explains.

What problem in the payments space does PayNearMe solve? And for whom does it solve it?

Anne Hay: Today’s consumers are used to making quick, easy payments when shopping online or sending money to friends, and they now expect that same level of convenience for all their payment interactions.

PayNearMe clients are largely recurring billers, such as consumer lenders, mortgage companies, municipalities, and iGaming operators, and we are helping them bring that frictionless, flexible payment experience to their customers.

With PayNearMe, their customers can choose how, when, and where they want to pay. For instance, they can pay with all major payment methods including cards, ACH, and mobile-first payment methods including Google Pay and Apple Pay, as well as with cash at more than 31,000 retail locations, including 7-Eleven and Walmart.

This focus on the customer payment experience is crucial as it is often the most frequent touchpoint our clients have with their customers. Our modern payment experience platform is also the first to enable our clients to fully own the customer payment experience — from facilitating transactions across payment types and channels, to sending payment reminders, to analyzing data for business insights.

PayNearMe recently announced an expanded partnership with Walmart and Green Dot. Can you tell us more about this collaboration?

Anne Hay: PayNearMe is rethinking payments with an emphasis on the payment experience, customer satisfaction and, of course, increasing our clients’ ability to get paid reliably. This expanded partnership with Green Dot makes on-time bill payment more convenient by bringing easy cash payments to the same location where customers do their everyday shopping. Now millions of consumers who prefer to — or need to — pay in cash can quickly and easily pay their rent, car payments, and utility bills at Walmart.

Customers simply show their scannable PayNearMe cash barcode on their smartphone to an associate in the Walmart MoneyCenter, pay with cash, and collect a receipt confirming that the payment is complete.

The expanded partnership with Green Dot adds participating Walmart locations across the country to our ever-expanding electronic cash network, and we expect to launch additional retailers in the near future to extend the convenience of our cash pay experience to our clients and their customers.

Enabling cash payers is a strategy that can help retailers, such as Walmart, bring more shoppers into their stores on a regular basis. Each visit to Walmart to pay a bill presents an opportunity for these customers to make additional purchases.

PayNearMe recently took a look at consumer preferences with regard to modern billpay options. What were the top takeaways from that survey?

Anne Hay: With all the innovation going on in e-commerce and peer-to-peer payments, we wanted to better understand consumer expectations around bill payments. There’s already a lot of research and data out there about how consumers are paying bills, but we wanted to ask consumers about what would make their bill payment experience easier.

Overall, the study uncovered a significant disconnect between consumers and businesses regarding how consumers want and expect to pay their bills, and the current bill payment options offered by most businesses today. About 75% wish managing and paying bills were easier, with 38% even preferring to do laundry over paying bills.

We found three big issues that need to be addressed.

Billers are slow to offer bill payment choices consumers have come to expect in other facets of their lives, such as Venmo, PayPal, and Apple Pay.

Consumers are struggling with disorganization, and it’s causing bill payment problems, including late payments.

Accessing bill payment information and paying bills is a cumbersome and difficult process for a good portion of those surveyed.

A couple of interesting and surprising findings were the number of consumers, especially young adults, that call in, likely when they are not able to seamlessly complete their payment transactions on their own, and the number of respondents willing to use QR codes to make bill payments.

Respondents said that the billpay experience itself was a more significant stressor than the fear of not being able to pay the bill. What does that tell you? Where is the experience going wrong?

Anne Hay: According to the bill pay study, nearly 1 in 3 adults revealed that paying bills causes them stress and anxiety. Surprisingly, for 70% of them, it’s not because of money issues.

Remembering logins, passwords, and account numbers top the list of what makes bill payment cumbersome. Keeping track of payment due dates is challenging for 41% of those surveyed, especially for younger adults. 30% cite having to navigate poorly designed biller websites and 26% report manually entering payment information further add to consumers’ dissatisfaction with their current bill payment experience. This expectation mismatch is not only potentially damaging billers’ relationships with their customers, but it is also hurting their bottom line as these frustrations can lead to late or missed payments. In fact, more than half of the respondents paid at least one bill late during the past 12 months.

This finding shows just how important focusing on the customer experience is and how much that experience is shaped by expectations. Even though consumers have the financial ability to pay their bills, they are still stressed because the bill payment process is not as seamless as making an Amazon purchase or paying a friend with Venmo.

The survey suggested that nearly a third of respondents saw mobile payment options as key to easier billpay. What are the obstacles to broader mobile payment adoption?

Anne Hay: One of our survey’s key findings was that billers are slow to adopt new technology. Mindsets need to change. They are not just competing against other entities in their industry, but against the consumer experience expectations influenced by Amazon, Apple, and Uber. They are competing against fast, easy, frictionless innovation.

As payments software is not often a core capability for many billers, working with a modern, future-looking enterprise software platform partner like PayNearMe is key to meeting new customer preferences such as mobile. Not only do we offer a choice of mobile payment channel options, including pay by text, digital wallets (including Apple Pay, Google Pay and more to come soon) and QR codes, but we also incorporate the security features needed to protect mobile payments. With 38% of respondents saying they would be likely or very likely to use Apple Pay and Google Pay to pay their bills if they had this option, innovation matters. The right partner can help billers stay ahead of the latest trends and perfect the customer experience.

Given the rise of QR codes, cryptocurrencies, real-time payments, embedded finance, and more, which innovations in payments excite you most?

Anne Hay: More and more we’re seeing that the phone is primarily the way people interact with the web these days. So not only Apple Pay and Google Pay, but digital wallets as well. Apple just broke news that they signed agreements with eight states to embed driver’s licenses and IDs within their wallets; more and more, digital wallets are becoming the de facto way to handle important personal and financial matters.

Consumers are storing everything in their wallets, and this can include their bills. In fact, our survey found that if given the opportunity, 42% of consumers would be likely or very likely to use their digital wallet to store, view, and pay their bills from a single place. By storing bills in their digital wallets, consumers can access all of their billing information, including their history, which solves a key pain point our survey found.

For those living on their phones, digital wallets give them everything they need, including reminder notifications and payment channels. With a thumbprint or face scan, payment is done. It’s about meeting the consumer where they live. It’s more than just payments; it’s about making the experience as easy as possible for the customer and merchant.

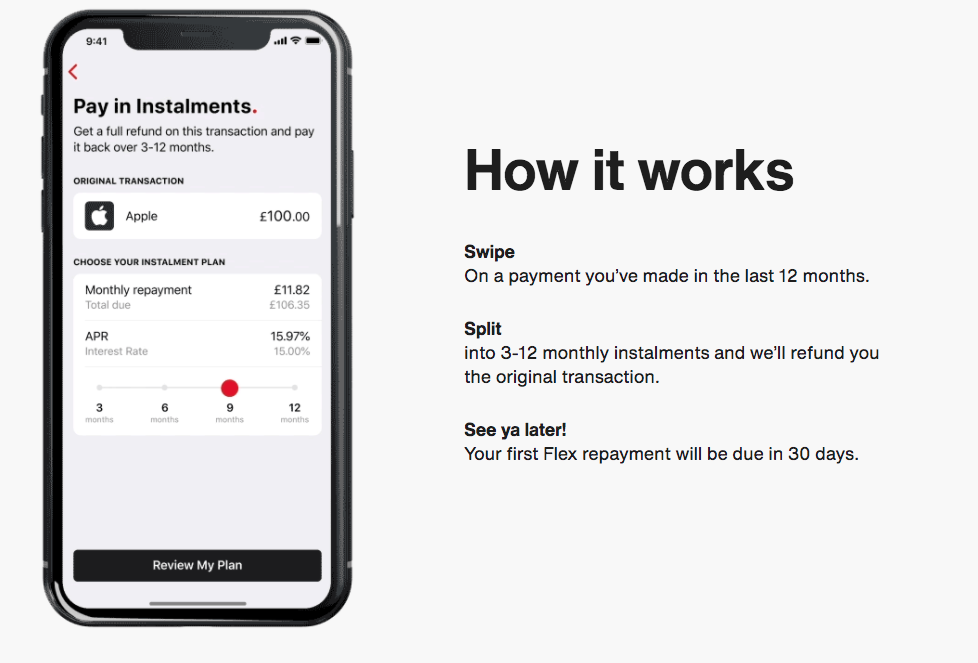

Curve, a U.K.-based payment card technology company, announced its own version of a buy now, pay later (BNPL) product this week.

The company is known for its unique payment solutions, such as its Go Back in Time feature that lets consumers switch payments from one card to another for up to 90 days after the transaction was made. Today, Curve is launching Curve Flex, a tool that builds on Go Back in Time.

Curve Flex allows consumers to convert almost any purchase from the past 12 months into an installment plan, as long as the card they used is linked in the Curve Platform. After the customer makes a purchase, all they need to do is swipe the transaction and select the number of installments. Then, Curve refunds their transaction in full almost instantly.

Unlike most BNPL tools, Curve Flex isn’t limited to specific merchants, cards, or products. It can be used on retail purchases, online orders, household bills, and more. Also unlike many BNPL tools, Curve’s offering charges interest based on the purchase amount and the number of installments.

“Curve is giving customers the unprecedented ability to convert transactions made up to a year ago into free or low-interest installment loans,” said Head of Curve Credit Paul Harrald. “Being able to Go Back in Time and Pay Later is going to forever change how U.K. customers think about managing their personal finances and cashflow.”

Curve Flex, which has been in beta for a year, already has 1,600 users that have opted to pay later on 7,000 transactions worth over $1.4 million (£1 million).

Earlier this week we celebrated the return to in-person events with FinovateFall. Though this year’s event felt a bit different from years past, with vaccination wristbands and social distancing replacing handshakes and hugs, there was an undeniable energy present. While it was wonderful to see many familiar people face-to-face, it was also refreshing to see new ideas and technology presented by the experts themselves.

With three days of demos, panels, keynotes, and networking, there was a lot to take in. Whether you attended in person or digitally, you were able to see some of the newest ideas and technology in banking and finance. And if you weren’t able to attend this time around, here’s a recap of what you saw and what you may have missed.

Overarching themes

Consumers have changed how they choose their bank. This one seems like a theme we’ve been hearing for a couple of years now, but I think it is becoming even more concrete as the move to digital is ever-accelerating. The anecdote I heard multiple times was how consumers used to base their banking relationship on which FI had the closest branch or the most ATMs in their region. Today, with the abundance of neobanks, consumers have a different mindset. They choose their banks based on the brand. Does it appear trustworthy and transparent, or is there too much fine print? Does it offer unique features such as early wage access that speak to the customer’s needs? Does it benefit the community? Does it speak to the unique needs of the customer’s tribe?

Cybersecurity should still be top-of-mind. The cybersecurity and fraud prevention theme is one that has been around since the dawn of fintech. It is also one that isn’t going away any time soon. With the push to digital, fraudsters are finding increased profits. At this week’s event, we saw multiple fintechs looking to stem the flow of cash into criminals’ pockets.

Regtech is rising. The U.S. has been slow to adopt existing regtech tools and create new ones. However, we’ve seen an increase in regulation around consumer data and customer communication. Not only that, but new technologies are also bringing pending regulation around AI, smart contracts, and cryptocurrencies. Fintech is here to fill the dearth of regtech solutions and save financial services companies and fintech alike from legal headaches.

Consumers are ready for self-service. We now live in a world where people no longer want to make a phone call to order a pizza, but would rather do so via an app. On top of this mobile-first preference, consumers also expect things on-demand. For these reasons, the chatbots that were dismissed in years past as a solution-looking-for-a-problem. At this week’s conference, however, we heard that chatbots are now some of the most practical tools FIs can implement to best serve their clients.

My highlight

My favorite session was the Investor All Star panel featuring Alexa Von Tobel, Founder and Managing Partner of Inspired Capital, and Matt Harris, Partner at Bain Capital Ventures. The two discussed the new “creator economy,” a sub sector of the gig economy that represents not just social media influencers, but anyone who monetizes content online.

Harris pointed out that, in general, relatively little money trickles down to creators such as musicians and artists because much of the funds are gobbled up by middlemen such as studios, auction houses, galleries, and publishing companies. However, with the advent of NFTs it is now possible for any artist to directly reap the rewards of their labor using only an NFT Marketplace.

Von Tobel added that banks need to be ready to serve the unique needs of this new workforce, many of which are Gen Z, that wants to ditch traditional jobs to work for themselves.

Hints at what to expect for 2022

We’ll see more no code and low code solutions. At FinovateFall this year, it was obvious that the no code movement is having a moment. It democratizes the internet, making it easy for almost anyone to launch a new tool, product, solution, or even an entire business. Competition in this arena has been slowly heating up for years and next year we can expect it to explode.

There will be more chat bots and AI-enabled help channels. With all of the mentions of self-service technology that pulsed throughout this week’s conference, it became clear that the chatbot movement isn’t just a passing fad. Given this, combined with the difficulty of creating self-service tools that actually meet customers’ needs, we can expect to see more, smarter chat bots and a wider variety of self-service tools.

This was Finovate’s last event for the year. Keep an eye out for updates on our conference roster for next year, including:

The future of finance is being ushered in. And the pioneers of the new era lead the change from the FinovateFall stage this year.

We can’t tell you how exciting it was to welcome so many people back to Manhattan. It was made even sweeter by the fact that we were able to engage so many digital attendees at the same time. It felt good to be able to bring our community together again!

Following the long-anticipated meeting of minds and ideas, we looked back on the themes that emerged and will steer the industry forward into unchartered territory. It’s impossible, of course, to distill so many conversations down to a few high-level takeaways. However, within these pages are snippets and insights from on-and-off-stage to give you a taste of the action and a spark of the knowledge shared.

After two days of live demos from innovative fintechs and financial services companies, today is a day dedicated to discussing the key themes and critical issues facing our industry today.

From our Investor All-Stars presentations to our special focus tracks on Future Tech, Future Payments, SME and Consumer Lending, and Digital Transformation, Day Three of FinovateFall gives us the opportunity to put two day’s worth of fintech innovation into context – and to turn that context into action: to grow and evolve, to improve ROI, and to change the customer experience for the better.

Thank you for spending the week with us here at FinovateFall. Here is the agenda for today. All times Eastern.

8:15am – 9:00am | Registration, Breakfast, and Networking

9:00am – 9:05am | Welcome from Finovate

9:05am – 9:35am | Investor All-Stars

9:35am – 9:50am | Mastermind Keynote featuring Jon Curtis of Samsung Electronics America

9:50am – 10:40am | Seven in Seven: 7 Expert Speakers Tackle Top Issues in Fintech

10:40am – 11:10am | Networking Break

11:10am – 11:25am | Special Address: The Growth of In-Car Intelligent Assistants

11:25am – 11:40am | Mastermind Keynote: The Future of Digital Identity is NOW

11:40am – 12:05pm | Five in Five: 5 Expert Speakers Tackle Top Issues in Fintech

12:05pm – 1:05pm | Lunch and Networking Break

1:05pm – 2:25pm | Finovate Focus Tracks

Future Tech

Fireside Chat: Digital Currencies, Diem, Central Bank Digital Currencies & Blockchain – Are Digital Currencies & Blockchain Finally Gaining Traction with FIs?

Mastermind Keynote featuring Nick Mates of Lendr

Keynote Address: Harnessing AI to Improve Efficiencies, Increase Margins, and Prevent Fraud

Power Panel: The Conversational AI Market is Expected to Reach a $14 Billion Valuation by 2025 – How Can You Leverage It to Deliver ROI-Driving CX?

Future Payments

Mastermind Keynote: Creating a Winning Cardholder Experience

Fireside Chat: The Need for Speed – Where Next with Faster Payments?

Keynote Address: eCommerce and Post-Pandemic Priorities

Power Panel: How Will New Technologies, New Competitors, and New Business Models Shape the Future of Payments? Is Payments Orchestration About to Have its Moment?

2:25pm – 4:00pm | Finovate Focus Tracks

Digital Transformation

Keynote Address: Customer Insights – Sharing Real Life Examples of Best Practices in CX and How to Blend Human and Digital CX

Keynote Address: Financial Services Digital Transformation: Embracing the Next Generation of Technology

Power Panel: How Open Innovation & Strategic Partnerships Can Help You On Your Digital Transformation Journey

SME & Consumer Lending

Keynote Address: PPP Loans – How Community Banks Rose to the Occasion & What Lessons Can We Learn from Their Success?

Mastermind Keynote: Onboard at the Speed of Digital – Flatten Silos, Fuel Lending, and Regain Control

Power Panel: Lending 2.0 – What Are the Problems that Need to Be Solved for Consumers & SMEs in the New COVID-19 World?

The Best of Show winners of FinovateFall this year featured both veterans and newcomers, established companies and bold, Millennial-led startups, fintech innovators from as far away as Europe and Latin America, as well as home-grown talent from right here in the U.S.A.

To be honest, we could not imagine a better way to celebrate Finovate’s return to New York!

So please join us in offering a hearty congratulations to the companies selected by our attendees as the FinovateFall 2021 Best of Show.

Array for its personalized consumer credit, identity, and financial wellness tools available via both API as well as embeddable components. Video.

AutoBooks for its small business digital invoicing and online payment acceptance tools for FIs. Video.

Bambu for its B2B robo-advisory platform for financial institutions and fintech disruptors. Video.

Dreams for its banking platform that leverages behavioral science to boost customer engagement and financial well-being. Video.

Horizn for its platform that helps banks accelerate digital banking knowledge, fluency, and adoption. Video.

Infocorp for its Mobile Native App, that brings hyper-personalized experiences for every user in one single bank app. Video.

Long Game for its gamified finance app that helps banks acquire new customers and increase engagement with their Millennial and Gen Z customers. Video.

Ocrolus for its intelligent automation technology that transforms documents into data analytics, helping lenders make timely, high quality credit decisions. Video.

PwC for its Customer Link solution that turns customer data into smarter action and provides a 360 degree view of your customers. Video.

Thanks to all the demoing companies, our sponsors and speakers, and our attendees for making our return to live fintech conferencing such a resounding success. Keep in touch with us via the Finovate blog for updates on our upcoming events next year in London for FinovateEurope, in San Francisco for FinovateSpring, and beyond!

Notes on methodology:

1. Only audience members NOT associated with demoing companies were eligible to vote. Finovate employees did not vote.

2. Attendees were encouraged to note their favorites during each day. At the end of the last demo, they chose their three favorites.

3. The exact written instructions given to attendees: “Please rate (the companies) on the basis of demo quality and potential impact of the innovation demoed.”

4. The nine companies appearing on the highest percentage of submitted ballots were named “Best of Show.”

5. Go here for a list of previous Best of Show winners through 2014. Best of Show winners from our 2015 through 2021 conferences are below:

SellersFundinglanded $166.5 million in Series A debt and equity funding this week. The company, which provides working capital to ecommerce marketplaces, now has almost $275 million in total debt and equity funding.

The investment was led by Northzone with additional investments from Endeavor Catalyst and Fasanara.

Founded in 2017, SellersFunding offers working capital solutions, payments tools, and analytics to help online marketplace sellers unlock capital, access invoice payments faster, collect payments, manage taxes, and more.

The New York-based company will use the financing to enhance its technology and payments platforms, grow its team, boost sales and marketing efforts, and fuel both domestic and international expansion. SellersFunding plans to gain more clients not only in the U.S. but also in the U.K., Europe, and Australia.

“We are thrilled to complete our capital raise and have Northzone and Endeavor joining our company, and to see the renewed commitment of Fasanara in supporting the expansion of our portfolio,” said SellersFunding CEO Ricardo Pero. “This underscores our dedication to providing world-class financial solutions for our clients and partners and is a testament to the overall growth of the global ecommerce space.”

Today we’re busting out the virtual confetti to announce the winners of the 2021 Finovate Awards, recognizing excellence in fintech across 25 different categories. This is the third annual Finovate Awards competition, which aims to highlight strong work done by the companies who are driving fintech innovation forward and the individuals who are bringing new ideas to life.

We may not get to congratulate the award winners with handshakes this year, but that doesn’t make the accomplishments any less compelling. These companies and individuals have proven that they have what it takes to capture the attention of the fintech world through standout products, services, and overall excellence.

Judges for the awards include media analysts, board members, bankers, fintech founders, and more. Each were given the difficult task of taking a record number of nominations and distilling them down to just a single winner in each category.

Best Alternative Investments Platform: Pipe

Best Back-Office / Core Service Provider: MANTL

Best Consumer Lending Platform: Salary Finance

Best Customer Experience Solution: TMRW by UOB

Best Digital Bank: Oxygen

Best Digital Mortgage Platform: LendingHome

Best Embedded Finance Solution: ApexEdge

Best Enterprise Payments Solution: GoCardless

Best Financial Mobile App: Simplifi by Quicken

Best Fintech Accelerator/Incubator: Financial Solutions Lab

Best Fintech Partnership: T-Mobile and BM Technologies

Best ID Management Solution: IDology

Best Insurtech Solution: FloodFlash

Best Mobile Payments Solution: Simpl

Best RegTech Solution: Featurespace

Best SMB/SME Banking Solution: Ramp

Best Use of AI/ML: Zest AI

Best Wealth Management Solution: Charles Schwab

Excellence in Financial Inclusion: Airtel Money

Excellence in Pandemic Response: Biz2Credit

Excellence in Sustainability: BlocPower

Executive of the Year: Barbara Morgan, FIS

Fintech Woman of the Year: Jo Ann Barefoot

Innovator of the Year: Jon Schlossberg

Top Emerging Tech Company: Synctera

While only one company can win each category, it’s also worth recognizing the quality of all of the finalists who made it to the last stage in the process.

We owe a huge thank you to the panel of judges, followers, and everyone who took the time to submit a nomination. Congratulations to the winners!