This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

Atomic’s payroll connectivity provides the infrastructure for consumers to permission access to financial data and automate setting up and updating direct deposit payments.

Features

Streamline setting up and linking accounts, cards, and mobile wallets with a source of funds from payroll with either a full or fractional direct deposit switch

Source of alternative data for VOI/VOE

Enable consumer-permissioned access to financial data

Why it’s great Atomic is the market leading provider of payroll APIs, trusted by 11 of the largest fintech firms, including digital-first neobanks, alternative lenders, and digital brokerages.

Presenters

Jeff Hendren, CRO Hendren has held C-suite titles at global financial services and enterprise software businesses including CCO at Quovo and CEO at Kurtosys, among others. LinkedIn

Lindsay Davis, Head of Markets Davis is the Head of Markets at Atomic and Forbes contributor. Prior, she was the Senior Fintech Intelligence Analyst at CB Insights and her research is cited in the FT, WSJ, and NYT, among others. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

ASA is a robust integration platform providing an unlimited number of certified fintech partners to help drive your ROI in a secure and compliant way. Welcome to the fintech app store for banking!

Features

FIs can offer any fintech to their customers

Fintechs promote their products and services, sending FIs new leads and customers

Customers never leave the ecosystem for the tech they want

Why it’s great Fintechs are competing for FI’s loans, accounts, and customers – ASA allows FIs to turn those fintechs into partners to future proof their tech stack and help them grow.

Presenters

Landon Glenn, CEO Glenn is a fintech entrepreneur with a successful exit, Best of Show winner at Finovate Fall 2018, and former owner of Banzai. LinkedIn

Tamio Stehrenberger, Head of Product Stehrenberger has been Head of Product of several consumer-facing tech startups and is excited to bring his knowledge into the banking sector. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

Facteus‘ Mimic unlocks the value of data by delivering actionable insights from hard-to-access financial transaction data while ensuring privacy is protected.

Features

Regulation compliance: manage privacy and data obligations

Product Innovation: use AI/ML tools to enable data-driven innovation

Safe and secure data monetization

Why it’s great Synthetic data is the “breakthrough” data set for maximizing your data potential, while minimizing your risk; it is the future of data and you should be using it now.

Presenter

Steve Shaw, SVP Marketing Shaw is responsible for the overall marketing, branding, and communications strategy for the company. Shaw has over 20 years of marketing experience at startups and Fortune 500 companies. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

U.S. BankCard as a Service (CaaS) empowers fintech partners or clients to extend corporate credit digitally and create a custom virtual payment experience in their ecosystem through API integration.

Features

Offers precise spend limits, tokenization, and encryption

Cards can be pushed to users’ mobile wallets in real time, with a touch of a button

Provides extensive controls around card security and fraud

Why it’s great U.S. Bank serves millions of customers around the world and is known for creating innovative ways for customers to bank how, when, and where they prefer.

Presenters

Jon Zimmermann, VP Product Development Zimmermann is a Vice President and Group Product Manager within the Corporate Payment Systems division of U.S. Bank. He is responsible for the U.S. Bank Instant Card and Card as a Service products. LinkedIn

Alex Hornbuckle, VP Product Development Hornbuckle is a Vice President and Senior Product Manager within the Corporate Payment Systems division of U.S. Bank. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

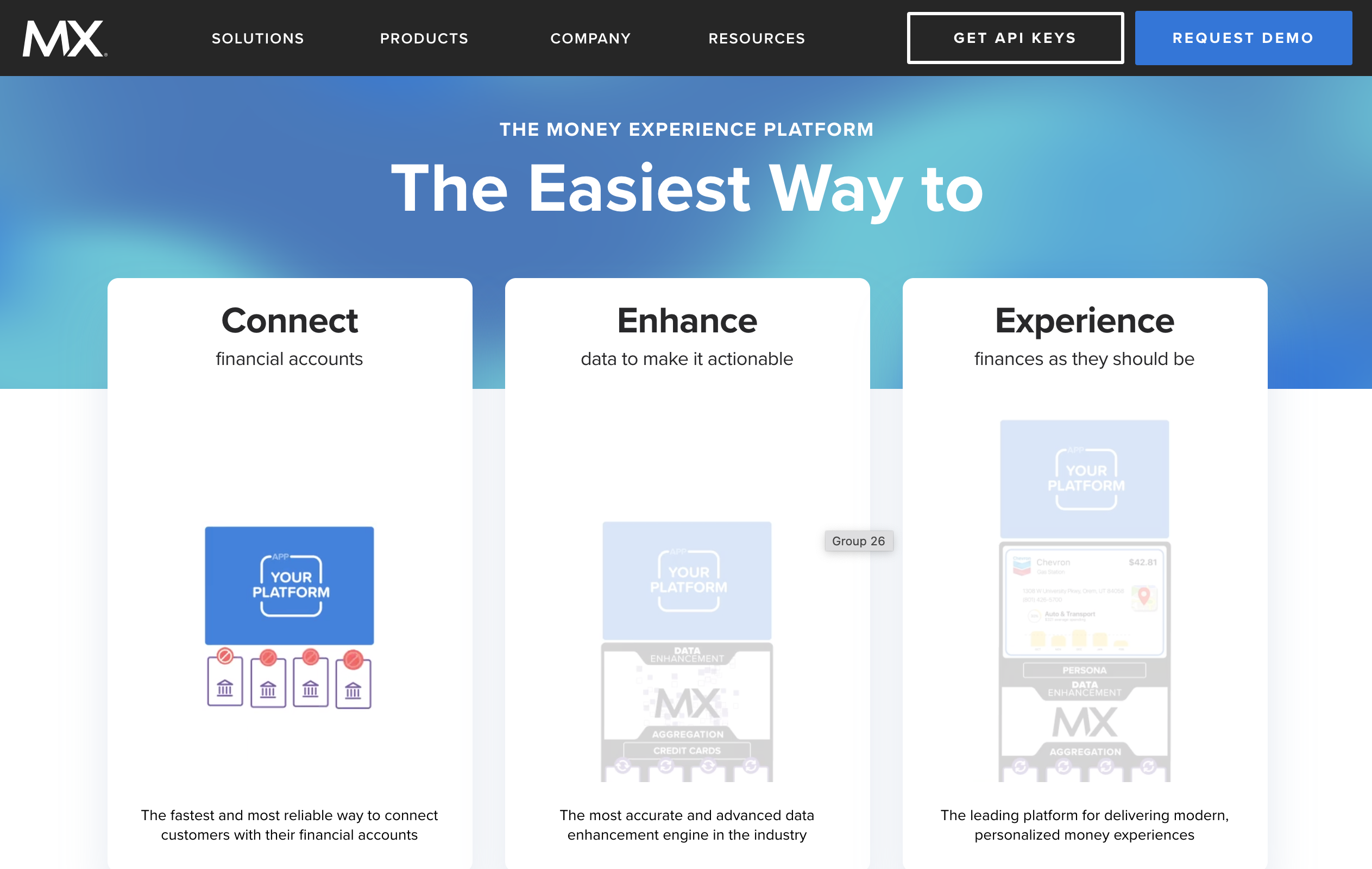

MXPortal is an open finance platform that improves the data sharing experience between data providers and data recipients on behalf of the customer.

Features

Gain a consolidated view into connection stability, requests, and health

Monitor active and pending connections to identify trusted vendors with whitelisted IPs

Access built-in legal documents

Why it’s great MX makes it easy for banks and credit unions to accelerate open banking.

Presenters

David Whitcomb, VP Product Connectivity Whitcomb leads MX’s Connectivity products and solutions, guiding how MX connects end users to their financial data and how FIs and Fintechs do as well. LinkedIn

Shayli Lones, VP Go to Market Lones leads MX’s Go to Market team, driving brand strategy and demand for products and services that align with market needs. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

The BackbaseEngagement Banking Platform helps financial institutions turn the threat of digital into an opportunity, and get ahead in today’s competitive digital landscape.

Features

Onboarding a new customer while linking external accounts

Empowering users to take control over their finances

Gaining critical insights on customers

Why it’s great A complete customer onboarding that involves consolidating their finances through direct deposit, bill pay auto linking, and debit card account opening.

Presenters

Marc Corbett, Solutions Engineer Corbett is a deviceful designer and solutions engineer who focuses on user experience design with a technical background in development and architecture. LinkedIn

Sajini Thirukumar, Senior Account Executive Thirukumar enables C-Suite executives to maximize their bank’s profitability and stay ahead of regulations. With Backbase solutions, her clients are able to continuously innovate their business. LinkedIn

A look at the companies demoing at FinovateFall on September 13-15, 2021. Register today and save your spot.

interface.ai is the leading intelligent virtual assistant provider. They will demonstrate an AI-powered call center that automates a majority of calls in 60 days while ensuring the best customer experience.

Features

Automate majority of calls in just 60 days with AI handling 100% of the calls

Respond instantly to pre and post-authentication questions

Save $2.5 million annually as an FI with a $1 billion in assets

Why it’s great Automate a majority of calls in 60 days with an interface.ai AI-powered call center.

Presenter

Srinivas Njay, CEO & Founder Njay has decades of AI-research and experience leading digital strategies to scale. Banks inspired Srinivas to embark on a mission to enable financial wellness through AI, with interface.ai. LinkedIn

Nerve differentiates itself by serving a unique customer segment– independent musicians. Available in both English and Spanish, the mobile bank helps musical artists “build stronger communities and sustainable careers” to help them manage their finances and plan for the future.

Co-founded by fintech veterans John Waupsh and Ben Morrison, Nerve is partnering with Piermont Bank to offer FDIC-insured business debit and savings accounts that will help users separate business and personal finances. The mobile bank also provides artists streaming and social follower data, access to 55,000 free ATMs, and free instant payments to other Nerve accountholders. Unique to Nerve is the bank’s private networking feature that helps professional musicians discover others in their field, network, and collaborate.

“Financial empowerment for musicians means giving them a banking platform that understands their unique needs with the tools to help them better manage their money,” said Waupsh. “Musicians and bands at all stages of their development need smart financial management, access to the real-time data that drives their business, not to mention two-minute digital account opening, and collaboration and business banking features to run their brands effectively.”

In addition to providing musicians with banking tools, Nerve is also piloting a music streaming app called Nerve FM. The app allows creators to earn subscription revenue from their audio and video content. Musicians keep up to 80 percent of the revenue generated from subscribers who stream their music. The best part is that the musicians get to keep all the user data as well. Move over, Spotify.

Nerve launches in the U.S. on September 15. You can catch Waupsh on stage at FinovateFall next month speaking on the neobanking panel on September 13. Register today or check out the FinovateFall homepage to learn more.

Mobile payments company BOKUannounced its expansion beyond carrier billing today with the launch of M1ST, a mobile payments network.

M1ST, also known as Mobile First, features 330+ mobile payment methods, including mobile wallets, direct carrier billing, and real-time payments schemes. The payment methods reach 5.7 billion mobile payment accounts across 90 countries.

“Today, we’re launching the M1ST Network to enable global merchants to acquire, monetize, and retain mobile-first consumers,” said BOKU CEO Jon Prideaux. “For merchants to capitalize on the massive potential of mobile-first consumers, they need to accept the payment methods they have and prefer, which are increasingly behind glass screens, not rectangular pieces of plastic.”

The new network, which runs via a single integration, is a solution for the currently fragmented mobile payments space. The technology circumvents many hurdles that come with with payments, including the myriad of tax and legal regulations associated with different geographies.

With M1ST, merchants receive a single, global settlement which eliminates the complexity of local taxes, foreign exchange, and cash repatriation. Additionally, BOKU’s payment licenses enable merchants to accept regulated payments in nearly 50 countries.

BOKU’s new launch comes at a good time in the payments space. As consumers continue transitioning to digital banking and transaction methods, many are becoming increasingly comfortable with digital payments via mobile wallets.

Founded in 2008, BOKU offers digital customer acquisition, customer onboarding, and mobile user authentication tools. The San Francisco-based company currently serves more than 600 global merchant partners and processes $9 billion in payments every year.

Financial data platform MX announced a collaboration with 1.2 million-member BECU (Boeing Employees Credit Union) to build a new mobile app feature called Quick Save that will help members boost their savings. Piloted last year with BECU members that had low savings account balances, Quick Save helps increase savings via an easy-to-use “slide to save” module that enables frequent, small dollar amount transfers.

“BECU is continually innovating and leveraging technology to improve our members’ experience and empower them financially,” BECU Director of Digital Strategy Liz Wagner explained. “It’s been inspiring to see Quick Save go from a concept to a fully functioning tool that members in this pilot are using to build their savings.”

The pilot project was conducted – and evaluated – in coordination with the Financial Health Network (FHN). Over the course of five months, FHN determined that BECU members using the new solution had transferred more than $2 million into savings accounts, representing an 18% increase in savings balance for the credit union’s low-balance savers, and a 26% increase in money movement via mobile transfers. Wagner credited the “combined power” of all three parties involved for both helping build and measure the effectiveness of the Quick Save offering, adding that the solution would “meaningfully improve our members’ financial health.”

Quick Save is only the latest example of the relationship that the Utah-based fintech and BECU have cultivated. More than five years ago, BECU went live with Helios by MX, a cross-platform framework that enables device- and platform-agnostic, full-featured digital banking.

“When it comes to mobile banking, every option we looked at functioned about the same,” BECU VP of Digital Banking Howie Wu said after the technology had been implemented. “We saw Helios as a chance to stand out and provide a very different experience.” Wu highlighted digital money management, aggregation, budgeting, and alert notifications among the offerings available via the framework – “all features that would enable our members to be financially strong,” Wu explained. Within 18 months of its deployment, BECU reported a 170% increase in billpay, a 56% increase in money transfers, and a 22% increase in check deposits.

Headquartered in Tukwila, Washington (a suburb of Seattle) and founded in 1935, BECU has assets of more than $26 billion. The institution is the largest credit union in Washington State and the fourth largest credit union in the U.S.

“BECU and MX have been aligned partners for years, both resolute in our determination to help strengthen the financial well-being of BECU members and their community,” MX Chief Customer Officer Nate Gardner said. He called Quick Save “yet another example of BECU’s wholehearted commitment to financial strength” as well as delivering “intelligent and personalized money experiences for the hundreds of thousands of members they serve.”

The following is a guest post by Todd Thomas, who has been in financial services for more than 20 years.

According to data from the Urban Institute, the median FICO credit score for Hispanic consumers is about 75 points lower than the median white consumer’s. The median credit score for Black consumers is more than 100 points lower than the median white consumer’s. And the approximately 10% of American adults without usable credit files are disproportionately people of color.

These racial, demographic, and geographic disparities are rooted in “historical inequities that reduced wealth and limited economic choices for communities of color,” according to the Urban Institute. It notes that subprime borrowers can pay $3,000 more in interest and fees on a $10,000 car loan over four years.

This unequal status quo has advocates calling for a more objective approach to consumer risk modeling. Innovators have created new technologies and data sources that could do just that.

The following four consumer risk modeling innovations are poised to disrupt the current credit scoring regime to varying degrees. Collectively, they could change the concept beyond recognition and eventually render obsolete what we think of today as “credit scoring.”

1. Forward-Looking Changes to Current Scoring Models

The most recent changes to the FICO scoring model, collectively known as FICO 10 and FICO 10T, are iterative rather than transformational updates. In other words, they don’t radically alter the calculation of credit scores.

But FICO 10 and 10T hint at the direction traditional credit scoring models are moving — and what they might have to do to remain relevant in the future as more disruptive innovations take hold.

FICO 10 and 10T pay closer attention to consumers’ credit mix in the context of their overall debt loads. Specifically, they penalize consumers who take out new personal loans to consolidate existing debts, then continue racking up debt on those current trades (most often, credit cards).

Essentially, they aim to reward good credit behavior(paying down debt) and discourage risky habits (living beyond one’s means).

2. Cash Flow Modeling

Another recent FICO update attacks credit scoring discrepancies more directly. The UltraFICO score — a joint venture between Fair Isaac Corporation, Experian, and Finicity — pulls in noncredit data to provide a more accurate and fair picture of consumers’ credit risk. Cash flow monitoring includes cash flow in a bank account and payment history.

By incorporating banking information, such as account balances and account age, UltraFICO supports credit scoring for about 15 million people who don’t have enough credit history to have traditional credit scores. Unfortunately, those people are disproportionately lower-income and POC — those most likely to be left behind by the credit scoring status quo.

UltraFICO is an example of cash flow modeling. Long used by business lenders, cash flow modeling is working its way into the consumer credit mainstream thanks to adoption by fintech lenders like Accion, Brigit, and Petal.

According to an analysis by FinRegLab, “the predictiveness of the cash flow scores and attributes was generally at least as strong as the traditional credit scores and credit bureau attributes,” suggesting it’s a reliable complement to or replacement for traditional scoring. And cash flow modeling is more equitable than conventional scoring, according to FinRegLab’s data.

3. International Credit Scoring and Risk Modeling

The current credit scoring regime also explicitly discriminates based on nationality. Non-U.S. nationals who come to the United States don’t have the requisite credit history to qualify for FICO scores. They’re essentially invisible to lenders that rely on FICO scores to make lending decisions.

Fortunately, border-based barriers to international credit scoring are already crumbling, thanks to global consumer credit risk models like Nova Credit. As more U.S. lenders begin to trust and adopt these models, new arrivals to the U.S. and Americans relocating abroad could find it easier to obtain credit without traditional country-specific credit scores.

4. A Post-Credit-Score World

Finally, noncredit and not-only-credit scoring models like FICO XD hint at what’s possible in a truly “post-credit-score” world.

FICO XD does not rely entirely — or even principally — on credit bureau information. The model pulls data from property records, leasing databases, and noncredit contracts like utility agreements to develop a comprehensive picture of a consumer’s likelihood of default.

According to Fair Isaac Corporation, FICO XD can produce FICO scores for up to 70% of previously unscorable consumers, including many historically disadvantaged demographic groups.

Final Thoughts

This is an exciting time for consumer risk modeling. From incremental changes to existing models (FICO 10, UltraFICO) to more radical shifts (cash flow modeling, FICO XD) that could supplant credit scoring entirely, we’re seeing a wave of innovation unlike any since the early days of modern underwriting.

These innovations can reduce long-standing credit scoring disparities and produce more accurate consumer credit risk models. But they offer no guarantees. Their actual impact on consumer finance will depend on who wields them and how.

Todd Thomas has been in financial services for more than 20 years.

This summer, as part of our Finovate Fintech Halftime Review, we helped make the case for the U.S. midwest as an under-recognized source of fintech innovation.

Today, our conversation with Nicole Lorch of the First Internet Bank is a reminder of what “America’s Heartland” has to offer in terms of leveraging technology to make online banking a reality for small businesses and families. Founded in 1999 and headquartered in Indiana, First Internet Bank was the first state-chartered, FDIC-insured financial institution to offer exclusively online banking services. At the same time, First Internet Bank has continued to emphasize the importance of personal connection and service to the community.

We caught up with Ms. Lorch recently to talk about First Internet Bank, the evolution of online and digital banking, and her goals as the institution’s new President and Chief Operating Officer.

You joined First Internet Bank as Director of Marketing at its launch in 1999. How has the idea of an “Internet bank” changed over the years?

Nicole Lorch: At the time of our launch, we operated as a direct-to-consumer bank with a fairly standard lineup of products: checking, savings, CDs, and credit cards.

While we actually were the first state chartered, FDIC-insured bank to operate entirely online, a number of competitors quickly emerged. However, many of them couldn’t make it work or were absorbed into another entity:

Compubank (Acquired by NetBank)

Netbank (Closed by OTS, 2007)

Wingspan Bank (Closed by its parent, BankOne, in 2001)

ING Direct (Divested U.S. operations, sold U.S. relationships to Capital One)

Security First Network Bank (Acquired by Royal Bank of Canada)

Telebank (Acquired by E*Trade)

Even with our early successes, many industry pundits believed that moving to more complex banking services, like mortgage and real estate lending, could not be done on a direct-to-consumer, nationwide basis. While we considered ourselves trailblazers in the new world of digital banking, it was critical that we created processes that allowed us to function in a sustainable, repeatable, and compliant way. As a result, we were able to efficiently – and profitably – become leaders in lending.

Imagination has always been fundamental to our existence. Our innovative approach to banking has continued to play an essential role in the development of First Internet Bank – and with it our ability to build a national lending platform with digital DNA behind it.

How has the challenge of educating the public about the Bank’s offerings changed from a time when there were very few if any “Internet banks” to now when the idea is more commonplace?

Lorch: One thing is certain: it is much easier for people I meet to wrap their heads around the concept of a branchless bank now than it was 22 years ago! The world has changed, and consumers have adapted and embraced the digital realm. From shopping and ordering food to conducting financial transactions, it’s all available instantly at our fingertips. But we need to remember, this is a very human business, not one that should be labeled “contactless.” We still pride ourselves in delivering the personal service our customers deserve.

Consumer demand and the way people want to access their money has moved in the direction we predicted: more electronic transactions, fewer cash-based transactions … with so few paper checks these days.

What are your first priorities as President and Chief Operating Officer?

Lorch: My new role with First Internet Bank is evolving. But our strategic agenda remains unchanged – which is good for our team because we move fast and get a lot of things done! We continue to concentrate on improving the customer experience by creating new solutions that foster greater efficiency and ease of use, strengthening our existing business and personal banking relationships, and diversifying our revenue streams. We have a great team that responds to challenges head-on, which makes achieving all our priorities much easier.

What are some of the bigger challenges that financial institutions like First Internet Bank are facing right now?

Lorch: Disruptive fintechs will continue to challenge our industry, bringing with them new consumer expectations and innovation. Fintechs have the ability to disrupt four primary categories of any traditional bank’s business: market share, margins, information security/privacy, and customer churn. However, financial institutions still maintain a greater sense of consumers’ trust.

Many fintechs do not face the same regulatory demands that chartered, insured depositories do, nor do they face the shareholder expectations of a publicly-traded company. Having a leaner virtual operation, more flexibility through not being regulated as a deposit-gathering institution and, in many cases, significant venture capital cash allows fintech startups to attract customers with competitive pricing and to move in a more nimble fashion when market conditions dictate.

We must continue to evolve and look for opportunities where they exist, to meet the changing demands of consumers. There is, however, one important area where we can continue to win: by providing great, high-touch (human) service that backs up our customer-facing technology.

What do your small business customers need most from First Internet Bank? And what kind of help do your retail customers most frequently request?

Lorch: Our customers need us to be creative. Sometimes they think they need a line of credit when they really need a term loan. Sometimes they think that they need a conventional product, when they need an SBA loan. We listen to their needs and customize our responses to their situation, instead of talking at them or selling them something they don’t need or want. If we can’t help them, we go so far as to make introductions to other financial institutions that can help them.

Most importantly, we have always believed that customers need surety of execution and respect for their time. On a loan request, a fast “no” is better than a long, drawn out “maybe.” Whether they are buying a business or a home, they need to know they can count on us to get them to the closing table – and closed – on time.

What of the popular enabling technologies have been most effective in helping First Internet Bank grow its top-line and better engage customers?

Lorch: AI allows us to leverage the data we have to acquire new customers as well as enhance our relationship with existing ones by identifying and offering products, services, features, and partnerships better tailored to their evolving needs. It also assists in fraud prevention.

APIs allow us to extend our platform and rapidly integrate new features, partnering with best-in-class service providers to create a robust, constantly-improving user experience while limiting the burden of legacy technologies and in-house coding.

What are some of the bigger initiatives the bank is pursuing this year?

Lorch: The last eighteen months have really tested our nation’s small business owners. We are poised to help entrepreneurs rebound and accelerate their growth. The pandemic pulled forward consumer acceptance of digital delivery of services by several years. We have a small window, albeit brief, to capitalize on the opportunity to layer our more than 20 years of direct-to-consumer know-how, with a next-generation user-interface, to give consumers a better way to bank.

We are growing our small business lending team while we overhaul the customer experience and our back office processes. It’s like flying the plane while we’re tuning the engine and refurbishing the cabin, but it’s necessary to ensure that our customers receive the level of service they expect from us.