This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

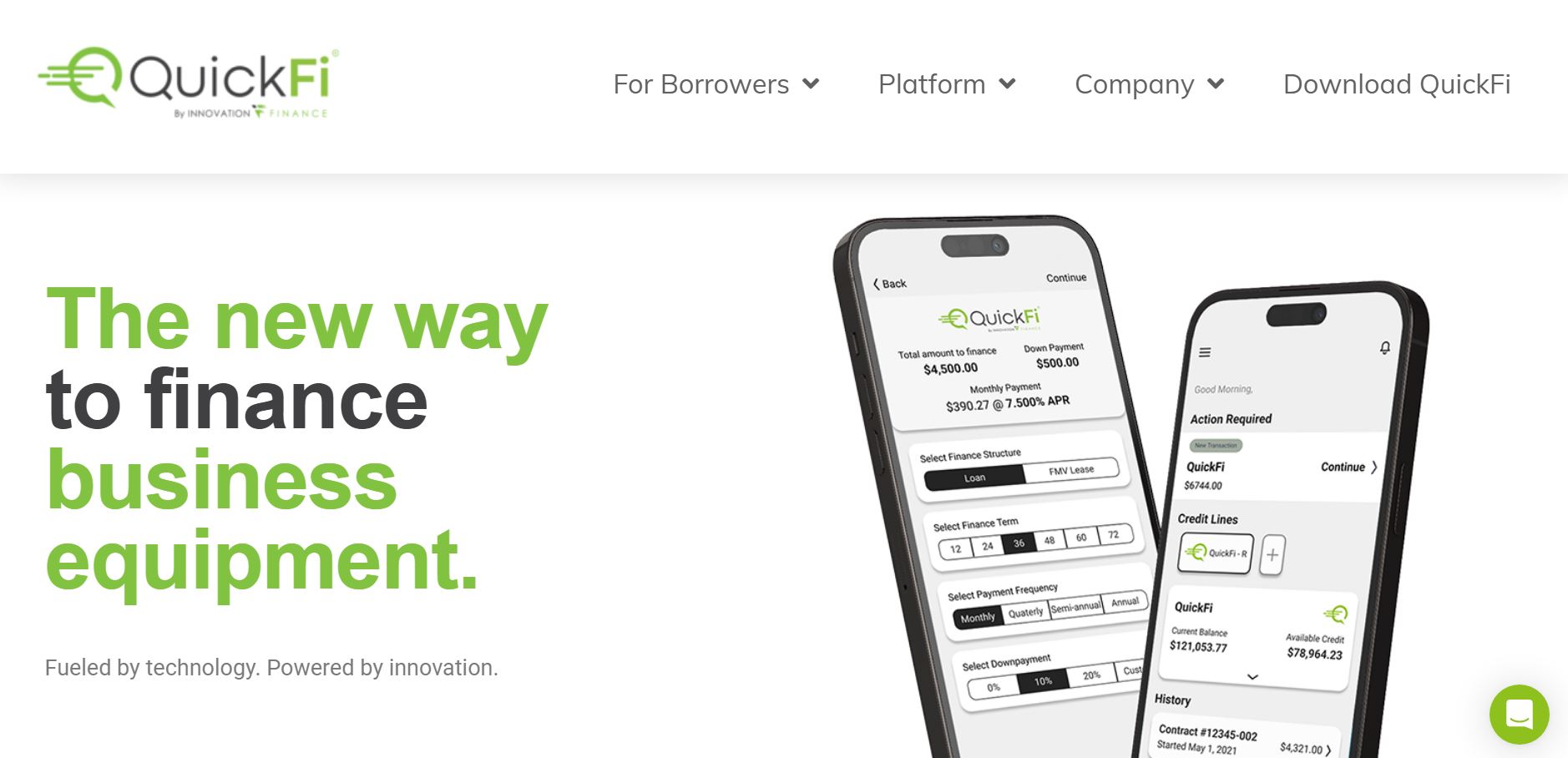

QuickFi’s latest e-commerce technology allows business borrowers to shop and consummate financing for business equipment – all within minutes, instead of days or weeks.

Features

Easily embeds into lender or manufacturer’s website

100% digital, borrower self-service, and accessible 24/7

Automated credit, contract structuring, and business verification

Why it’s great

With this latest technology, banks and manufacturers can now offer a combined online shopping and financing experience that is 100% digital, fully self-service, and able to be completed in minutes.

Presenters

Nate Gibbons, CXO Gibbons oversees QuickFi’s customer experience strategy, leveraging automation and technology to enable dramatic improvements to the borrower experience. LinkedIn

Jillian Munson, VP, Process & Automation Munson leads core technology projects at QuickFi. She develops seamless user experiences for both internal and external business processes. LinkedIn

Behavioral biometrics and fraud detection innovator BioCatch has raised $40 million in funding.

The investment gives Permira a “significant minority stake” in the Tel-Aviv-based company.

BioCatch made its Finovate debut at FinovateFall 2014.

Behavioral biometrics innovator BioCatch has raised $40 million in funding courtesy of an investment from Permira Growth Opportunities. The capital gives Permira a “significant minority stake” in the New York and Tel Aviv-based company. In fact, along with Bain Capital and Maverick Capital, this week’s capital infusion makes Permira BioCatch’s third largest shareholder.

“Permira is one of the leading global private equity firms in the world, with particularly strong experience in the technology space,” BioCatch CEO Gadi Mazor said. “We believe its deep sector expertise and company-building capabilities will help us to expand our business and strengthen our global position.”

The funding takes BioCatch’s total capital raised to more than $213 million. No new valuation information was provided. BioCatch will use the capital to help support geographical expansion, product development, and potential M&A.

BioCatch is a pioneer in behavioral biometric intelligence and advanced digital fraud detection. Its technology leverages AI and machine learning to collect thousands of data signals to analyze the cognitive intent of users. This enables BioCatch to provide highly accurate insights into the legitimacy of a user’s identity and behavior. Financial institutions using BioCatch’s technology have been able to better fight fraud, accelerate digital transformation efforts, uncover new revenue opportunities, and boost customer satisfaction.

Founded in 2011, BioCatch made its Finovate debut at FinovateFall in 2014. In the years since, the company has grown into a fraud detection leader with a global footprint of 22 countries. More than 100 international banks rely on BioCatch’s technology to fight financial crime and defend themselves against fraud. BioCatch announced early this year that 2022 had been the firm’s “most successful” – with annual recurring revenue growth of more than 40%. BioCatch also revealed that the company added more than 100 leading global banks as customers in 2022 and detected more than $1.5 billion in fraud, saving banks nearly $1 billion.

Global financial services innovator Revolut is becoming a bit more global today. The London-based company announced today it has expanded into Brazil. Today’s move of launching multi-currency account and crypto investments in Brazil, marks Revolut’s first expansion into a Latin American country.

Revolut’s expansion efforts into Brazil began last March. The company not only brought on Glauber Mota as CEO of its Brazil operations, but it also opened up a waitlist in the region. “There’s a lot of appetite for Revolut and digital banking services in Brazil,” said Mota. “Recent surveys show that more than 45% of Brazilians already use digital accounts as their primary account, and use more than five different applications to manage payments, transfers, and investments.”

The company will begin its Brazil expansion via a phased rollout, during which time it will continue adding to its waitlist. In addition to being available in Brazil, Revolut’s accounts are available to residents of the European Economic Area (EEA), Australia, Singapore, Switzerland, Japan, the U.K., and the U.S.

Revolut counts 29 million retail customers across the globe making 330 million transactions each month. The company debuted its multi-currency account at FinovateEurope in 2015 and also offers a peer-to-peer trading, an early wage access tool, an account for users under the age of 18, stock trading, business cards, commercial spend management tools, and more.

Revolut has raised around $2 billion since it was founded in 2015. While the company was once considered one of Europe’s most valuable fintechs, Revolut took a hit last week when company shareholder Schroders Capital Global Innovation Trust disclosed a $5.8 million (£4.7 million) writedown, shaking the value of its stake from $12.6 million (£10.1 million) in 2021 to $6.7 million (£5.4 million) in 2022.

Despite the valuation woes, however, Revolut continues to expand. The company launched credit cards for its Ireland user base earlier this year and is planning to launch a car insurance service in the region. Additionally, Revolut is working on expanding to more geographies, including Ecuador, Mexico, India, New Zealand, and Oman.

Retail software company Celerant Technology has partnered with BNPL innovator Sezzle.

Celerant will integrate Sezzle’s SezzlePay solution into its platform. SezzlePay enables consumers to pay for purchases in four, interest-free installments over six weeks.

Sezzle made its Finovate debut at FinovateSpring 2016.

Retail software provider Celerant Technology announced a partnership with consumer financing solutions company Sezzle. The partnership will enable retailers who use Celerant eCommerce to add Sezzle Pay to their payment choices. This option gives consumers the ability to take advantage of Sezzle’s buy now, pay later (BNPL) financing, with 0% APR. Retailers will also benefit from engagement with potentially millions of Sezzle users, an opportunity that could lead to increased online sales and new customers.

“We’re excited to partner with a leader in the retail software industry and to bring Sezzle’s Buy Now, Pay Later financing to the millions of consumers that shop at Celerant’s diverse ecosystem of brands,” Sezzle co-founder and Chief Revenue Officer Paul Paradis said.

Paradis underscored the popularity of BNPL financing among millennials and Gen Z consumers. He pointed to the fact that BNPL financing charges no interest and no fees when purchases are paid for on time, as well as the ability to use BNPL to build credit, as two factors in favor of the financing option. “It’s a runaway hit,” Paradis said.

Celerant’s eCommerce platform enables retailers to offer Sezzle to customers directly from their website. The process is straightforward. Customers select SezzlePay as their payment option during checkout. This will enable them to split the cost of the transaction into four interest-free payments over six weeks. Sezzle pays the merchant in full at the time of the transaction; funds are direct deposited in the merchant’s account within one-to-three business days. Sezzle also assumes full risk of any missed payments.

“With more consumers turning to instant credit apps to make ends meet, it was important to expand our technology with additional consumer financing options,” Celerant President and CEO Ian Goldman said. “As a popular ‘buy now, pay later’ solution in the industry, partnering with Sezzle provides more options for our retailers to offer their customers payment flexibility and help financially with larger purchases, and in turn increase our retailers’ online sales.”

Sezzle made its Finovate debut at FinovateSpring in 2016. The company returned to the Finovate stage two years later for FinovateFall. Sezzle began 2023 as the first BNPL company in Canada to offer free credit-building service to users. The firm also began the year as a profitable company, growing from a net loss of $75.2 million in fiscal year 2021 to ending 2022 with net income in Q4. The turnaround came as a result of major cost-cutting strategies. These efforts included layoffs; a retreat from potential expansion in Asia, Europe, and Latin America; and a renegotiation of merchant fees. Sezzle also benefitted from a premium membership drive that brought on more than 132,000 subscribers.

Founded in 2016, Sezzle is headquartered in Minneapolis, Minnesota.

Business budgets and digital payments platform inbanx has partnered with Corserv.

inbanx will leverage Corserv’s Payment Cards as a Service API to offer its business customers a Visa commercial credit card.

According to Juniper Research, the number of payment cards issued via digital platforms will grow 170% between now and 2027.

Business budgets and digital payments platform inbanx is boosting its offerings today by partnering with card issuer Corserv. Texas-based inbanx is integrating Corserv’s Payment Cards as a Service API (PCaaSA) into its platform to offer a more holistic business payments platform.

Integrating Corserv’s PCaaSA will enable inbanx to offer a Visa commercial credit card to its business clients. The new modern payment card solution will offer real-time, configurable spend controls and cooperative authorization for businesses that rely on hierarchical approvals and spending limits.

“Our highly configurable PCaaSA platform simplifies complex processes for inbanx to launch and embed commercial cards in a secure, compliant and flexible way,” said Corserv CEO Anil Goyal. “We are thrilled to work with inbanx to integrate with their innovative budget and expense management solution.”

Founded in 2021, inbanx helps businesses budget, manage their card program, and control spending across teams. By automatically reporting the expenses, inbanx’s solution eliminates the need for employees to fill out manual expense reports.

“We serve our customers with an innovative and easy-to-use solution that adopts the next generation of payment capabilities to allow businesses and their employees to spend efficiently,” said inbanx CEO Rob Kaczmarek. “Corserv’s payment card platform was the only solution that afforded us the customizability and flexibility to build exactly what we needed for our customers.”

Corserv has been helping banks and fintechs offer issuing processing and program management services for credit, debit, and prepaid cards since it was founded in 2009. The Atlanta, Georgia-based company has raised $2.1 million in funding and recently named Anil Goyal as its new CEO.

Modern card issuing is a hot space in the fintech realm, especially as banking-as-a-service and embedded finance becomes more popular. Juniper Research expects the number of payment cards issued via digital platforms to grow 170% between now and 2027, increasing from 500 million in 2023 to 1.3 billion by 2027. Global leaders in the modern card issuing space include Thales, G+D, FIS, Fiserv, and Marqeta.

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

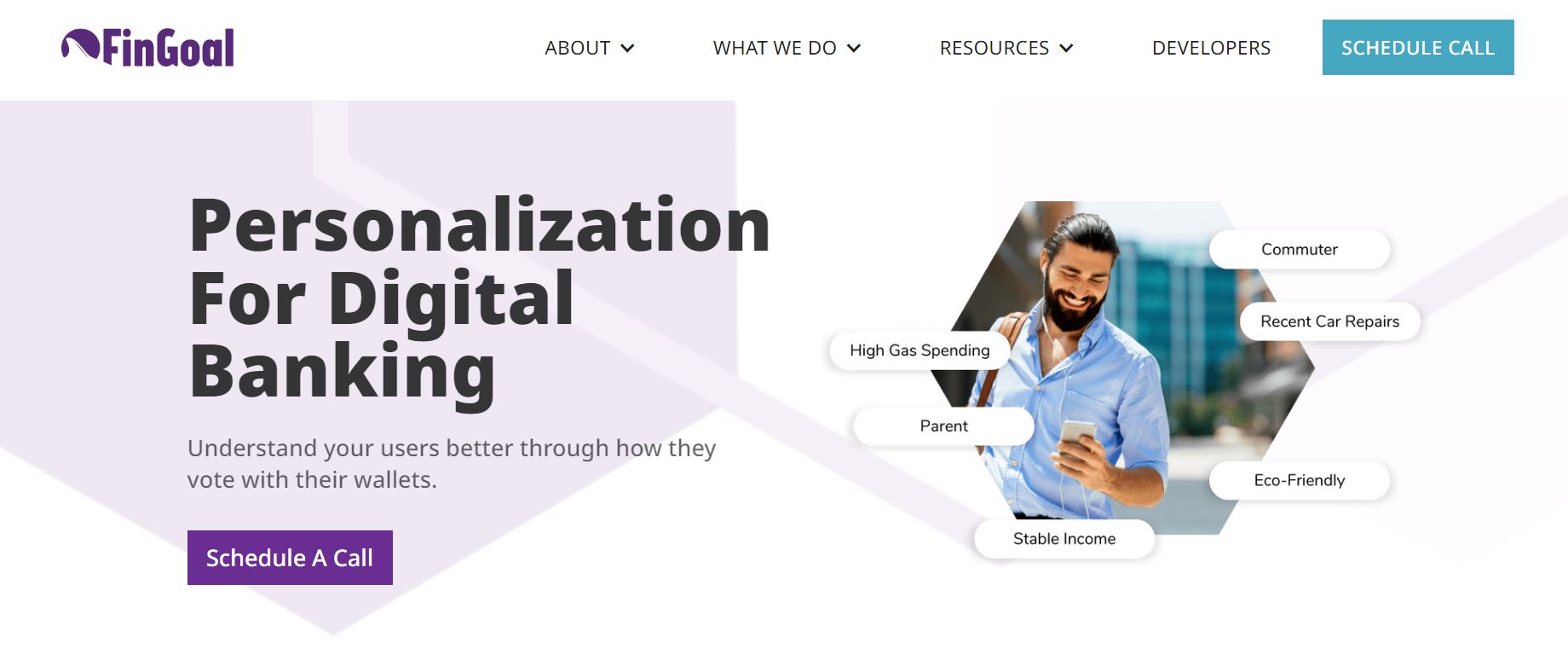

FinGoal’s new user tags enable financial institutions to understand their customers better and create more targeted offers resulting in higher cross-sells.

Features

Includes user tags based on transaction data

Applies user tags in any CRM to create targeted marketing campaigns

Results in higher cross-sells and more loyal customers

Why it’s great

FinGoal helps firms go beyond marketing based solely on demographics. They can use the information business’ already have – transaction data – to drive personalized marketing campaigns that will result in higher conversions.

Presenters

Ariam Sium, VP of Product Sium uses the tenets of focus and value to govern each product decision made in the rapidly adapting world of fintech. LinkedIn

Jenn Underwood, Product Analyst Underwood brings expertise in personal finance to FinGoal’s product development. Her passion for equitable financial services and value-based savings greatly enriches the UX. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

IDMERIT’s IDMlive can efficiently and accurately verify a customer’s identity with a live agent.

Features

Reduces customer acquisition costs

Provides faster onboarding of new customers

Offers a simple and low-friction process

Why it’s great

IDMlive is a simple and low-cost solution to manually verify new customers.

Presenters

Ray Weale, COO Weale, a tech executive for 25+ years, led international teams implementing SAP, Salesforce, and eCommerce for digital transformation. Previously Weale was the CTO at Etihad Airways and Nestle. LinkedIn

James Stubbs, Customer Success Manager Stubbs joined IDMERIT in 2021. As the liaison for their clients, he works diligently with each department to ensure that IDMERIT provides the best customer experience. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

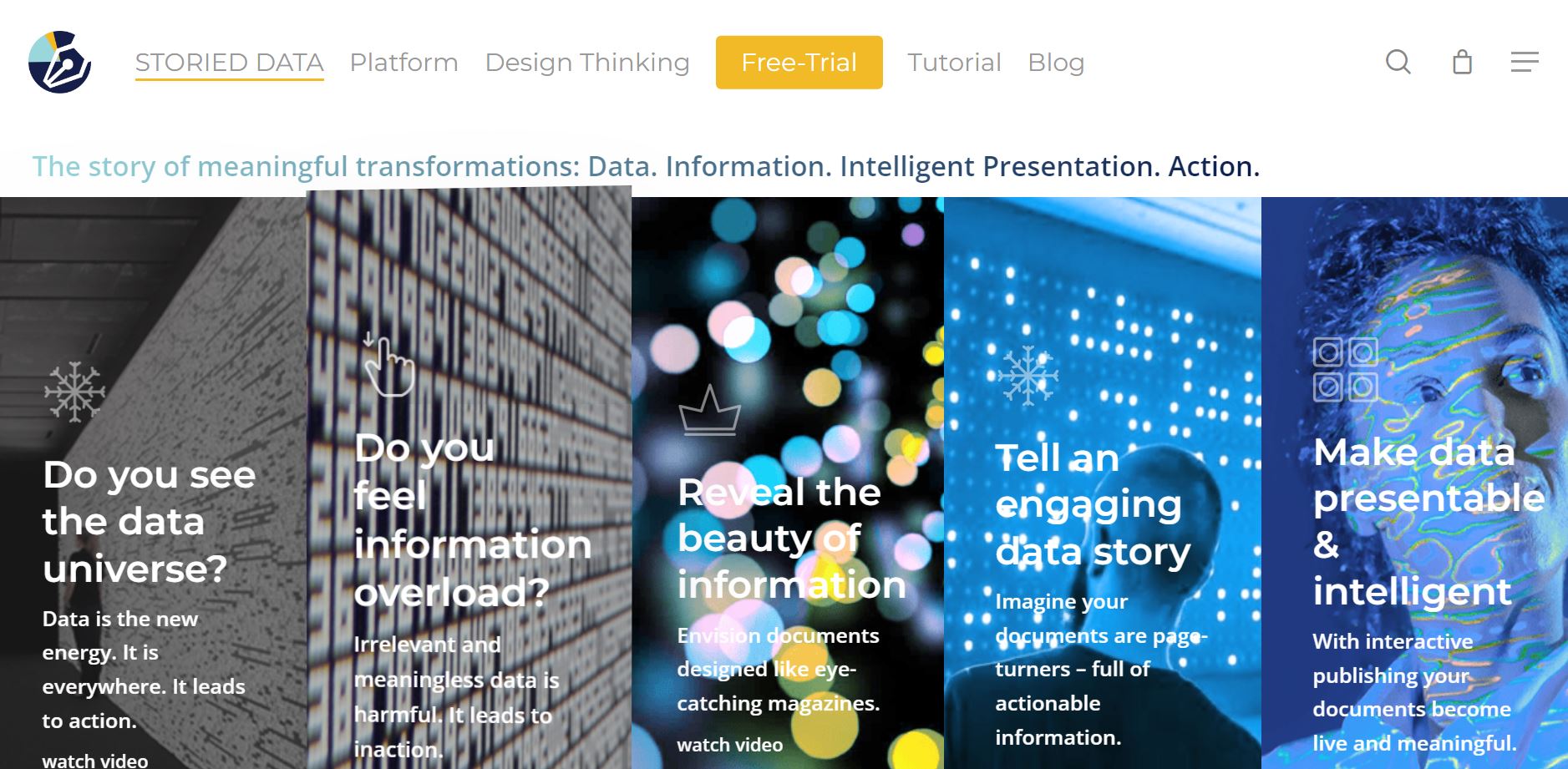

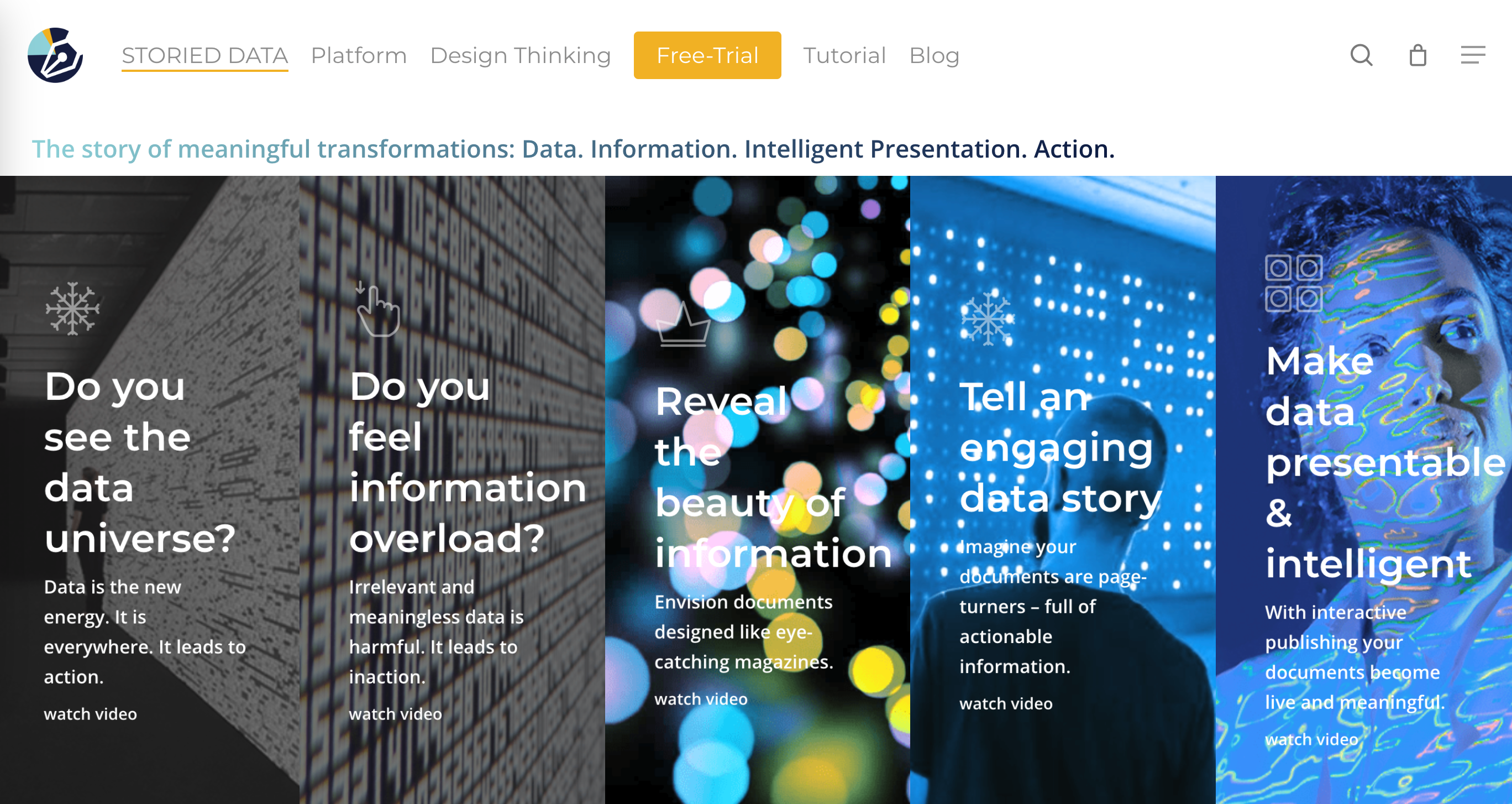

Storied Data’s smart information distribution platform transforms digital documents and powers information sharing and data publishing to millions of information consumers.

Features

Replace dull PDFs and static documents with smart digital documents

Transform the user experience with app-like in-document UI/UX

Improve cost, time, and ESG efficiency by 90%

Why it’s great

Businesses can deliver education, transparency, and trust through smart information distribution and data publishing at scale.

Presenters

Rado Kotorov, Founder & CEO A business leader and innovator with multiple patents, articles, and books. Passionate about data and digital technologies that create new business models and revenue streams. LinkedIn

Yoshiko Akai, CPO Innovative and results-driven technology leader focused on achieving exceptional results in highly competitive environments that demand continuous improvement. Experienced in driving product, process, and customer service improvements while building partnerships with the key business decision-makers. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

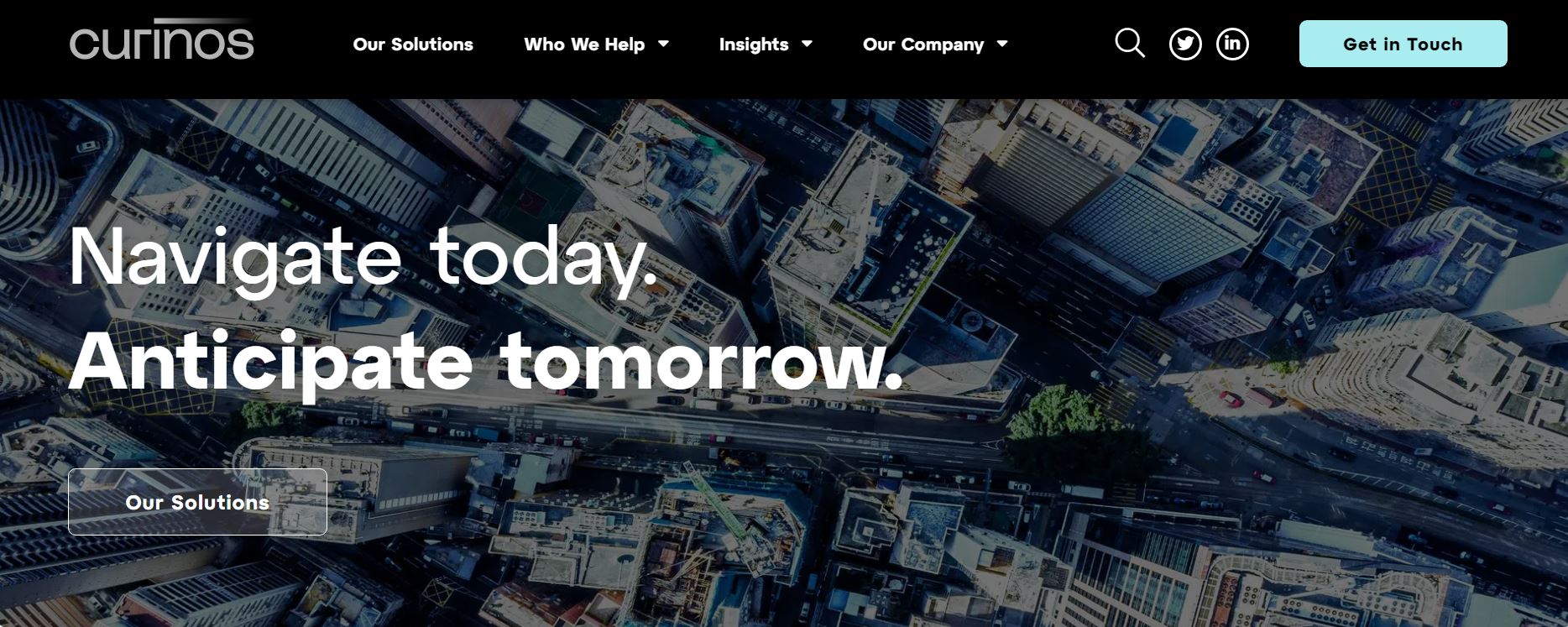

Curinos’ Amplero Personalization Optimizer introduces a new kind of marketing automation, making it possible for financial institutions to deliver optimal, hyper-personalized omnichannel experiences.

Features

Built by data scientists, tuned for financial services

AI engine enables personalization at scale within days, not months

Intuitive platform allows for seamless builds of content and user journeys

Why it’s great

Amplero Personalization Optimizer allows financial services marketing departments to add rocket fuel to their operations by utilizing existing tech stack and personnel.

Presenters

Sarah Welch, Managing Director Welch is a strategic and results-oriented innovator with 15+ years of experience launching and leading startups, new brands, and internal initiatives. LinkedIn

Tazmin Bailiff Curtis, VP, Amplero Bailiff Curtis has a diverse background in consulting, strategy, analytics and product management, successfully launching several platforms across industry verticals. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 23 and 24. Register today and save your spot.

TAZI AI is a machine learning (ML) platform, enabling business experts and data scientists to build and deploy ML models with patented continuous learning and explainable AI.

Features

Easy to use: Usable by business employees who don’t have data science training

Time to value: Deploy models in less than two weeks

Adaptive: Adapts to changes in data

Why it’s great

A no-code ML platform for business experts (and data scientists) to create, update and deploy ML models, allowing them to make smart decisions in dynamic business environments.

Presenter

Zehra Cataltepe, CEO & Co-Founder Cataltepe is a computer science expert with a PhD from Caltech. She is democratizing AI across industries and has 100+ publications in the field of AI and 14 patents. LinkedIn

“With eBay International Shipping, we’re making global connections even more accessible, affordable, and profitable, significantly increasing the volume of items available to shoppers in 200+ countries and making it even easier for our sellers to tap a universe of new business opportunities,” eBay U.S. VP and GM Adam Ireland said.

According to Juniper Research, the value of cross-border ecommerce will top $2.1 trillion this year. But the cross-border ecommerce market is not without its complications. Businesses must navigate through a range of customs duties and import taxes in a process that can be both complex and costly. Using Avalara’s software, eBay International Shipping determines Harmonized System (HS) commodity classification codes, identifies item-level trade restrictions, and generates landed cost pricing for more than 200 items hosted on eBay. The new offering will help the platform’s more than five million merchants sell to more than 70 million buyers worldwide.

“With Avalara’s cross-border solutions embedded within eBay’s International Shipping program, we’re able to simplify cross-border compliance complexity and reduce potential customer experience disruptions by providing more transparent landed cost pricing for global buyers and helping ensure parcels meet local customs requirements,” Avalara EVP and GM of Indirect Tax Jayme Fishman said.

Avalara made its Finovate debut at our developer’s conference, FinDEVr SiliconValley in 2015. In the years since, the company has grown into a leading regtech with more than 30,000 customers across 95 countries. Avalara went public in 2018. The firm was acquired in 2022 by Vista Equity Partners in a deal valued at $8.4 billion. Headquartered in Seattle, Washington, Avalara was founded in 2004. Scott McFarlane is CEO.

Raisin has appointed Cetin Duransoy as CEO of the company’s U.S. division, SaveBetter by Raisin.

Duransoy comes to Raisin from Fundbox, where he served as President and COO.

Today’s announcement follows Raisin’s $64.7 million capital raise in March of this year.

Savings and investment product marketplace Raisin has appointed a new CEO for its U.S. savings division. The Berlin-based company has selected Cetin Duransoy to head SaveBetter by Raisin, its U.S. savings platform originally launched in 2020.

Duransoy

Raisin launched SaveBetter in 2020 to serve as an online marketplace where customers can choose from a variety of savings products, including savings accounts, money market deposit accounts, and certificates of deposit. The savings tool enables users to access more favorable rates than most traditional savings accounts from a single portal.

SaveBetter has seen impressive growth recently, having added $1 billion in assets under management in the past three-to-four months. Additionally, over the same time period, the company has brought 30 financial brands onto its online marketplace.

In the release, Duransoy said this is an “exciting time” to join Raisin as CEO. “Having already established itself in the U.S. market, demonstrating scale to banking partners and tangible benefits in increased returns for everyday Americans, Raisin is poised to lead the way in further disrupting the American cash savings market and providing a valuable tool to help millions of savers secure their financial future,” he added.

Duransoy has more than 20 years of experience in financial services. He most recently served as President and COO Fundbox, and has also held senior positions at companies including Capital One and Visa.

Today’s announcement comes just over a month after Raisin raised $64.7 million (€60 million) in a Series E funding round led by M&G’s Catalyst and Goldman Sachs. The round boosted Raisin’s total funding to almost $305 million since it was founded in 2012.

Raisin counts more than one million customers and $31.7 billion (€38 billion) assets under management across the U.S., U.K., and European Union. The company taps its network of more than 400 banks and financial service providers from 30+ countries to offer its catalogue of savings, investment, and pension products. Tamas Giorgadse is Co-Founder and CEO.