Financial infrastructure is becoming increasingly valuable as it powers payments and financial products. Instead of operating within closed systems, banks are now operating within broader ecosystems in which customers expect seamless integrations, faster money movement, and financial services experiences that become invisible within the customer journey.

Fintechs are working to satisfy the demand for this infrastructure using API-driven tools that can support real-time payments, cross-border transactions, and embedded finance use cases. At FinovateSpring 2026, we’re hosting a group of fresh fintechs that will showcase their solutions designed to simplify payments, modernize infrastructure, and unlock new revenue opportunities. From digital asset infrastructure to cross-border payments and operational platforms, these four companies leading the way.

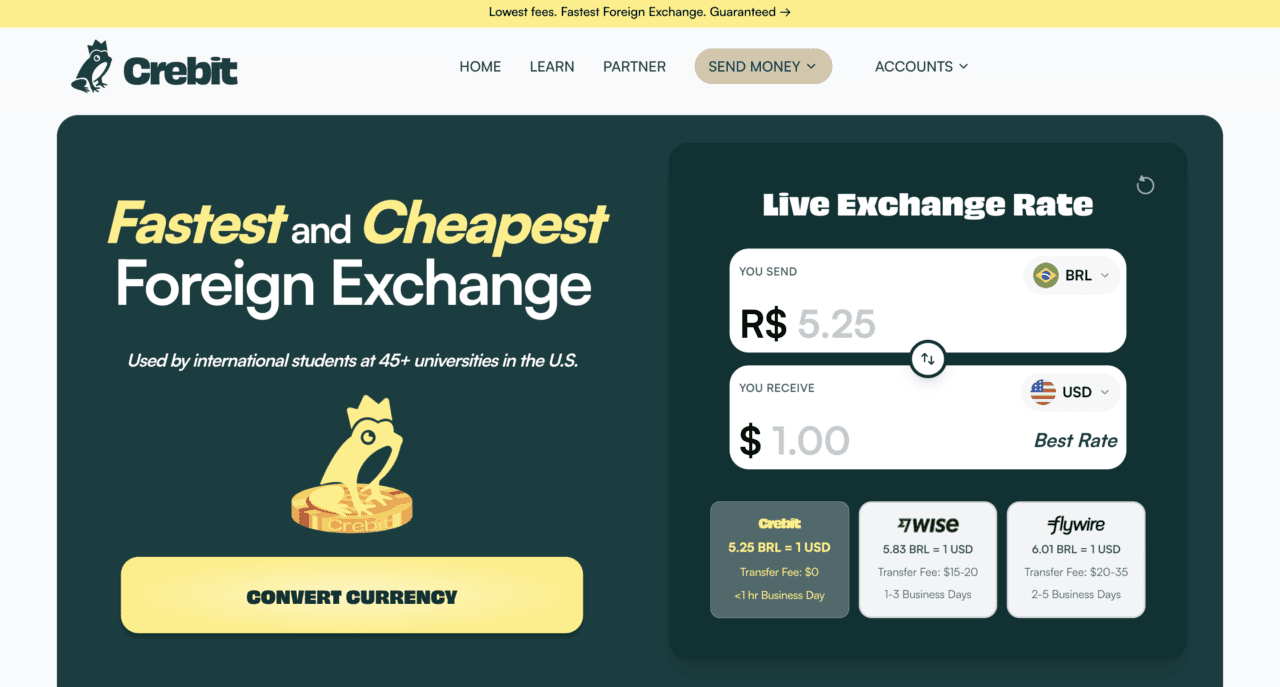

AlphaPoint enables smaller financial institutions to adopt stablecoin payments and treasury capabilities without the cost and complexity of building in-house infrastructure. Its platform provides the tools banks need to support digital asset transactions, helping them modernize payments and compete with larger, more technologically advanced players.

Founded in 2013 and headquartered in New York, AlphaPoint gives banks a faster path to integrating blockchain-based financial services, positioning them to participate in real-time, programmable money.

Quanto helps businesses reduce operational friction across financial workflows by streamlining back-office processes, allowing companies to focus on growth.

Founded in 2025 and headquartered in Chicago, Quanto helps organizations scale more efficiently, reduce complexity, and accelerate time to scale.

Reativ’s cloud-based treasury management system offers financial institutions real-time visibility into cash positions, liquidity, and risk. Its platform combines automation and AI-driven insights to help banks optimize cash usage, reduce operational costs, and improve decision-making.

Designed for regional and community banks as well as credit unions, Reativ can reduce operational expenses by up to 50% while enhancing regulatory readiness. Founded in 2026 and headquartered in Portland, Oregon, the company offers a modern, centralized approach to treasury management.

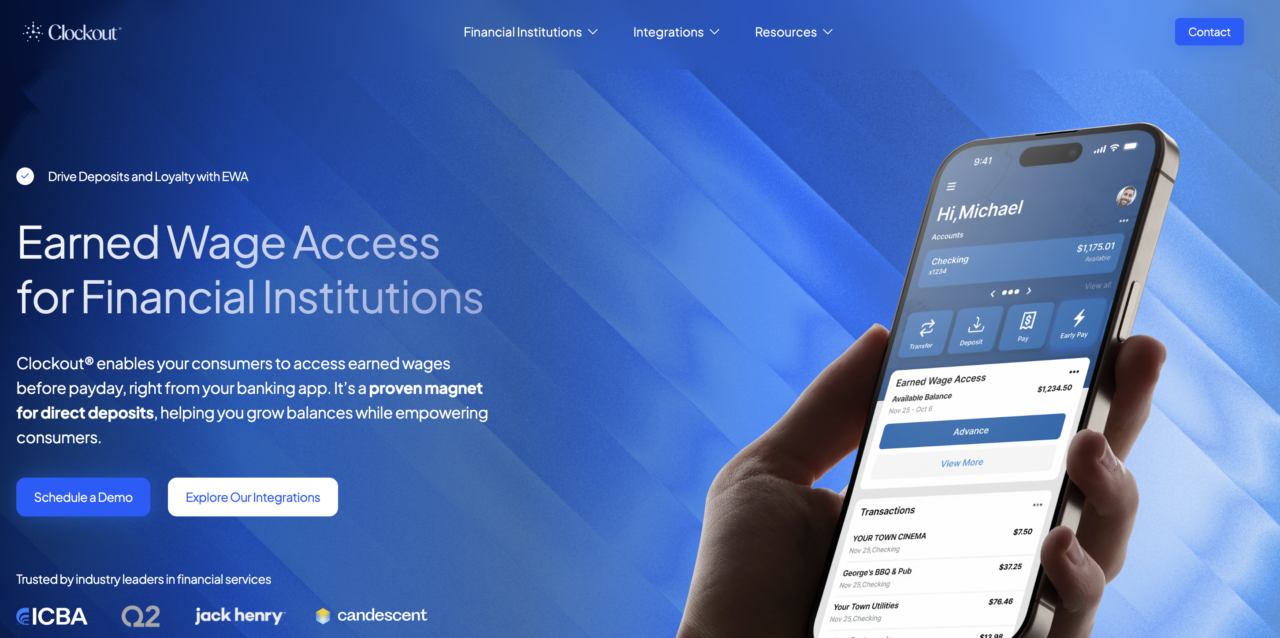

Clockout helps financial institutions drive deposit growth and customer engagement through embedded financial wellness tools. Its platform is designed to increase direct deposits, boost per-user revenue, and differentiate banks and credit unions in competitive markets.

Founded in 2022 and headquartered in Tennessee, Clockout enables institutions to deepen relationships with their customers while creating new revenue opportunities tied to everyday financial activity.

Why banks should care

Banks are under pressure to offer faster money movement, integrate with third-party platforms, and meet rising customer expectations. At the same time, firms need to manage costs and are constrained by legacy systems.

Fintechs are helping bridge this gap with solutions that simplify treasury management, enable stablecoin and real-time payments, and streamline operational workflows that allow institutions to modernize without large-scale overhauls. At the same time, embedded finance and deposit-driving tools create new opportunities to grow balances, increase revenue per customer, and stay competitive in an increasingly platform-driven financial ecosystem.

Photo by Artur Łuczka on Unsplash