This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

CB Insights is out with its State of Insurtech Q3’25 report. The top takeaway? With the total number of deals down and merger and acquisition activity at record highs, the insurtech industry appears to be reorganizing to maximize the opportunities of scale, digital modernization, and market reach.

Deals Down

According to CB Insights’ research, the number of insurtech deals dropped to its lowest level since the second quarter of 2016. Q3’25 featured 76 insurtech deals, 65% less than the industry’s peak of 219 deals in the first quarter of 2021.

In addition to the number of deals being down, the median insurtech deal size has also decreased on a year-to-date basis from $3.8 million in 2024 to $2.9 million in 2025. The report indicates that a diminished early-stage pipeline is to blame. Year-to-date, 60% of all deals have gone to early-stage startups, the lowest deal-share percentage since 2011.

Lastly, the number of active investors in insurtech in Q3’25 shrank to the fewest since the first quarter of 2017. Especially notable was the quarter-over-quarter decline in investors making multiple investments, from 13 in Q2’25 to 4 in Q3’25.

Mergers and Acquisitions Up

At the same time, M&A activity in insurtech was on a tear, reaching its highest levels in three years. There were 21 insurtech M&A deals in Q3’25—the most since Q3’22 when there were 23 deals. This compares favorably to 16 deals in Q2’25. The report notes that the gains in the third quarter of this year helped reverse a trend of decreasing M&A activity between 2022 and 2024.

The reasons for the uptick in M&A activity are varied and interesting. Some analysts have suggested that business leaders are becoming increasingly confident in dealing with uncertainty and have embraced a “move through uncertainty” mentality, in the words of WTW analyst Jana Mercereau. Other factors include high stock market valuations, which can facilitate acquisitions; relatively stable interest rates; and the relatively weak M&A period from 2022 to 2024. The drive for digital modernization also plays a role. For its part, CB Insights offers an intriguing idea that the relative lack of attention from investors gave established insurance companies the opportunity to “engage more closely with emerging insurtechs.”

Insurtech in Q4 and Beyond

Heading into the final quarter of the year, there are a number of questions for insurtechs and many of them mirror concerns and issues in fintech more broadly. Which companies are actually putting AI to work in interesting use cases, and which are still in a pilot phase purgatory? How well are investors and establishment insurance companies recognizing where the value lies? How will evolving regulatory requirements incentivize regtechs to develop innovative compliance solutions for insurers? These are some of the questions that come to mind when reading CB Insights latest insurtech report. It will be interesting to see how the events of the fourth quarter and beyond help us answer them.

October is National Cybersecurity Awareness Month in the US—although those in fintech and financial services can be forgiven for feeling as if every month is cybersecurity awareness month.

This is not to say that the threat of fraud and financial crime is any less important in health care, consumer technology, or any other sector of the economy. But the facts are hard to ignore. According to the New York Federal Reserve, financial services companies face 300x more cyber attacks compared to companies in other industries. After all, that’s where the money is—to say nothing of a treasure trove of data on banking customers, borrowers, investors, and more.

Additionally, the impact of fraud and financial crime on financial services companies and their customers can be significantly greater, as well. Estimates indicate that the average breach cost in the financial sector is more than $6 million, compared to the global average of $4.9 million. In fact, the financial services sector is second only to healthcare when it comes to the average cost of a data breach.

Released in the first half of the year, Alloy’s 2025 State of Fraud Report noted that a sizable number (60%) of financial institutions and fintechs reported fraud growth across both consumer and business accounts over the past year. The good news is that, unlike in AI, where there remains some skepticism about the potential benefits versus costs and risks, Alloy observed that 87% of institutions queried believed that investing in fraud prevention—especially via deploying identity risk solutions, building in-house anti-fraud solutions, and adding talent to fraud teams—outweighed the costs.

More recent reports on fraud and financial crime underscore additional challenges. The Kroll 2025 Financial Crime Report, which surveyed 600 international executives, noted that a growing number of executives fear an acceleration in financial crime, with 71% believing financial crime risks will increase in 2025 compared to 67% in 2023. Alarmingly, the executives also confessed a sizable gap between their concerns about the accelerating pace of financial crime and their own organization’s preparedness to fight it, with only 23% of those surveyed believing their compliance programs were up to the task.

As for the question of whether AI is an effective tool to fight financial crime or a new and dangerous weapon in the hands of fraudsters, the answer, unsurprisingly, is “yes.” Just over half of those executives surveyed (57%) believe AI is a benefit to fighting financial crime while just under half (49%) believe AI represents a significant risk and vector for fraud.

Best of Show winners lead the fight against financial crime

With fraud and financial crime threats on the rise, it is no surprise to see a growing number of companies on the Finovate stage whose innovations are dedicated to fighting fraud, scams, and other financial crime. In fact, 2025 was the first year since COVID that featured a fraud fighter in every Best of Show winning cohort: FinovateEurope, FinovateSpring, and FinovateFall.

Here’s a look at some of our Best of Show winning alums from recent years who are innovating in the field of financial crime and fraud prevention.

Casap – Offers a co-pilot and collaboration platform that fully automates dispute management and empowers financial institutions and fintechs to more effectively fight first-person fraud.

Founded in 2022

Headquartered in New York

Shanthi Shanmugam is CEO and Co-Founder (LinkedIn)

Herd Security – Leverages AI-driven detections, training content, phishing simulations, and exercises to make users an active and engaged part of defending their companies and organizations from fraud and cybercrime.

Keyless – Equips companies with biometric authentication technology that reduces account takeover (ATO) fraud by up to 80%, and verifies a user’s genuine identity in addition to their device in 300ms or less.

Founded in 2019

Headquartered in London, UK

Andrea Carmignani is Co-Founder and CEO (LinkedIn)

Illuma – Offers a real-time voice authentication solution that replaces traditional knowledge-based authentication, enhances the caller experience, and improves operational efficiency while preventing fraud in contact centers.

Corsound AI – Leverages 200+ patents to provide voice-to-face and real-time deepfake detection. The company’s technology leverages the unique correlation between voice and facial features to authenticate identities accurately.

1Kosmos – Combines identity proofing, credential verification, and strong authentication to enable remote identity verification and passwordless multi-factor authentication to enable workers, customers, and residents to securely utilize digital services.

Trulioo – Covering 195 countries, Trulioo offers an identity platform that verifies more than 14,000 ID documents and 700 million businesses, while checking against more than 6,000 watchlists.

Founded in 2011

Headquartered in Vancouver, British Columbia, Canada

At a time of uncertainty in both politics and policy, an entreaty to think about “what’s possible” might sound naive—if not terrifying.

Yet, at the onset of FinovateFall 2025, which just wrapped up last week, thinking about “what’s possible” was the challenge laid down by Finovate VP and Master of Ceremonies Greg Palmer. And to the delight of our FinovateFall audience, it was a challenge that our demoing companies, keynote speakers, and insightful panelists were more than ready to accept.

What we heard from the experts

What’s possible … AI as a tool to empower and augment human action was an especially persistent theme over the three days of FinovateFall. In fact, even our pre-conference, invitation-only, Leaders+ event on Sunday evening featured a reminder that AI was increasingly the tool of choice for those under 30 when it came to a range of financial tasks from establishing a budget to making better credit decisions. Crucially, as J.D. Power’s Jennifer White pointed out, Gen Z is using AI for answers to more immediate questions, not exclusively for long-term planning. For them, AI is a co-pilot rather than a forecasting or projecting tool.

This sentiment was elaborated on by Alex Johnson of Fintech Takes in his Analyst All Stars presentation Tuesday morning. Johnson took on the notion of AI as a tool for automation, suggesting instead that AI—and Large Language Models (LLMs) more specifically—be thought of as ways to augment human activity rather than replace it outright. Johnson underscored LLMs as “probabilistic guessing machines” rather than “determinist systems,” and explained that to the extent that the latter is what’s required in financial services, LLMs alone can fall short.

That said, Johnson noted that by applying LLMs in ways that maximize what they are good at, financial institutions can leverage processes like mortgage servicing to better understand the diverse and even niche preferences of their customers. This data can be used not only to introduce new products and services, but also to scale up entire new businesses built around these edge cases.

No conversation about AI at FinovateFall would be complete without a reference to Jon Lakefish’s return to the Finovate stage for another mind-bending conversation on the latest AI tools. His Wednesday morning keynote—Creating Trust and Loyalty through AI-Enhanced CX—helped attendees understand the powerful resources available to not only build new products, but also to discover what new solutions are possible given a deeper, AI-enabled analysis of a business, its customers, and goals. In less than five minutes, Lakefish showed how a variety of readily available AI tools could enable, say, a Finovate sponsor, to uncover and pursue a new niche product line. From the latest innovations in ChatGPT—”the LLM platform for almost everything”—to Manus.AI, the first publicly available Agentic AI platform Lakefish has felt comfortable showcasing, the message was clear: the world of what’s possible is becoming larger every day and AI is a primary resource for navigating and creating within it.

One telling insight shared during our Investor All Star panel at the end of Day Three underscored the power and potential for AI when it comes to emerging fintechs, in particular. During a discussion on which trends investors were most drawn to, our panelists cited fraud prevention and compliance technology among the most attractive areas for investment, with personal finance management (PFM)-related solutions increasingly less so. Nevertheless, panelist Lindsey Fitzgerald of Vesey Ventures noted that even within this group, it was possible for truly innovative startups to stand out if they are able to deploy enabling technologies like AI in new and novel ways. “AI changes the possibility of a startup being 10x better (than its rivals) in any category,” she explained.

What we saw from the innovators

I have long contended that the roster of companies that win Best of Show at Finovate conferences in any given year is as good a heat check on the state of fintech innovation as you’re likely to find. This year’s batch of FinovateFall Best of Show winners was no exception.

By theme, FinovateFall attendees were impressed by innovations in a wide range of areas. Nevertheless companies innovating in the fraud prevention space probably experienced the greatest amount of on-stage competition—a point I’ll return to. Kudos to Casap for standing out from an impressive pack with its technology that helps combat fraud, including an especially pernicious form of e-commerce crime called “first-party fraud.” Founded in 2023 and headquartered in New York, Casap recently raised $25 million in Series A funding for its payment dispute resolution solution.

Arguably the most compelling case for financial institutions to offer services like investments came from Eko CEO Mart Vos. His company, now a two-time Finovate Best of Show winner, provides a solution that enables financial institutions to integrate digital investing functionality directly into their platforms. Vos warned banks and credit unions not to be complacent as their customers open investment accounts with innovative brokerages like Robinhood. While mere brokerages today, many of these firms are looking at ways of expanding their banking offerings, or obtaining banking licenses outright. By integrating investment services into their platforms and making them seamlessly accessible, financial institutions incentivize customers and members to keep their funds “at home.”

Enabling more qualified borrowers to secure funding is a cause championed by many innovative fintechs and it is no surprise to see two such companies among this year’s Best of Show winners. This year at FinovateFall, New York-based Krida demonstrated its AI intelligence layer for business lending. The company’s solution leverages AI to provide bankers with automated workflows for document collection, lead tracking, and data management. This enables new bankers to be more effective sooner and empowers all bankers to spend more time with their client relationships and less time with paperwork. Hailing from the other side of the country, Irvine, California-based LendAPI is a super orchestration platform that enables CTOs, CROs, and CCOs to work together to build enterprise platforms. At FinovateFall, LendAPI CEO Timothy Li demonstrated how to use the technology to launch a 1003 mortgage application in minutes. Both Krida and LendAPI are newcomers to the Finovate stage.

Another Finovate newcomer to take home Best of Show honors from FinovateFall last week was VerticeAI. The Atlanta, Georgia-based fintech provides credit unions and community banks with tools for predictive analytics, AI-powered marketing content, and targeted customer acquisition. The company began the year announcing new partnerships with Texas-based Education Credit Union and North Carolina-based Duke University Federal Credit Union.

Last but certainly not least, it was great to see the positive impression LemonadeLXP made on our FinovateFall audience last week. A Finovate alum since 2022 and, like Eko, now a two-time Best of Show winner, LemonadeLXP offers a learning experience and digital adoption platform for both the staff and customers of financial institutions. At the conference, the Ottawa, Canada-based company demoed its InsightAI solution which enables firms to develop and deploy their own employee training programs.

Where we go from here

This year I was struck by the number and quality of solutions on display that were dedicated to fighting fraud and dealing with related concerns like dispute management and chargebacks.

Fraud prevention may not be the most glamorous corner of fintech. Fraud in the digital space is a persistent, if not growing, threat to all of us; someone very close to me lost their life savings in a phishing scam earlier this year. But it’s not something that we like to talk about very much. Victims feel shame. Institutions suffer reputational damage. Providers scramble to offer their own proprietary solutions. The fraud lifecycle, so to speak, is silent and siloed. And this makes fraud harder to fight.

Perhaps this is why some of the most novel technology innovations and business strategies are found among those engaged in the fight against fraud. Consider the aggressive deployment of AI to combat deepfakes or the increasingly common collaborations between institutions—particularly credit unions and community banks—to share best practices to keep their members and customers safe. At a time when personal security concerns are paramount—in financial services and beyond—it is heartening to know that so many of fintech’s best and brightest are on the case.

Now that the “One Big Beautiful Bill Act” is the law of the land, is there anything in there that fintechs and financial services companies need to be ready for?

There are two little-discussed items in the 900+ page statute may be of interest to the fintech and financial services industries One is a bit of a bankshot, the other represents a potential new hurdle for fintechs involved in payments, including cross-border transactions and micropayments.

Let’s start with the bankshot. The OBBBA includes a requirement that the Federal Communications Commission (FCC) and the National Telecommunications and Information Administration (NTIA) auction 600 MHz of spectrum behind 1.3-10 GHz by the year 2034. Why is this important? For one, the government stands to earn as much as $88 billion from the proceeds. At the same time, telecoms like T-Mobile and AT&T stand to gain bigly from greater access to a mid-band spectrum that represents the foundation of not just 5G but also future 6G networks, as well.

“Wireless spectrum acts as the invisible backbone for our digital economy,” Shane Tews, Nonresident Senior Fellow at the American Enterprise Institute, wrote last month. “Every smartphone call, streaming service, autonomous vehicle communication, and Internet of Things (IoT) device depends on this limited resource. As we approach widespread deployment of 5G and look ahead to 6G, the availability of commercial spectrum becomes increasingly vital to maintaining America’s competitive edge in the global technology race.”

While the biggest and most direct winners will be the telecoms who are able to buy the additional bandwidth, faster, low-latency connectivity will be a boon to fintechs and financial services companies when it comes to delivering current solutions faster, as well as offering new products and services that can take advantage of modern networks. Everything from account updating to more sophisticated anti-fraud technology to high-definition video banking could be positively affected by more robust 5G/6G connectivity. The broader network coverage could also support financial inclusion by making it easier for financial institutions, including regional and community-based financial institutions, to reach un- and underbanked communities in their vicinities.

The other aspect of the OBBBA that relates to fintech and financial services is the repeal of the de minimis tariff exemption. The de minimis tariff exemption allowed packages valued at less than $800 to enter the US duty-free and with less restrictive customs screening. The exemption came under fire from critics who feared a wave of low-value shipments from China and Hong Kong that would take advantage of the exemption.

Unlike much of what happens in Congress, there was actually bipartisan support for repealing the exemption; repeal also helped sync Senate and House versions of the legislation. The repeal is slated to take full effect by July 1, 2027—though partial implementation for Chinese imports has already begun.

How might this little-discussed feature of the OBBBA impact fintechs and financial services companies? Greater complexity in payments and cross-border transactions is one potential outcome as previously exempt transactions become subject to new tariff calculations. Along with this there are likely to be additional—and often more complex—compliance steps that firms will need to take including more extensive documentation, enhanced duty calculation functionality, and more. Companies will also have to explain and deal with the impact of higher prices on customers, who have become increasingly cost-conscious in recent years.

That said, there may be opportunity in this development for fintechs in the regtech space in particular. Firms with talent and technology in trade compliance, logistics, as well as tools to help automate new and complex regulatory requirements, will be ideal partners for fintechs, banks, and other companies as they navigate a world with far more dynamic trade and tariff policies than we’ve experienced in a long time.

According to the New York Fed, US total household debt reached $18.2 trillion in the first quarter of this year.

While there were positive signs—credit card balances were lower quarter-over-quarter—the $16 billion uptick in student loan balances, including the number of loans that had moved from “current” to “delinquent,” was a reminder of how dynamic the US household debt landscape can be. The report also noted that, while there were no significant increases in the number of auto loans and credit card balances that had “transitioned into serious delinquency,” there was an increase in aggregate delinquency rates versus the previous quarter.

It is against this backdrop that we learned that debt recovery and credit rebuilding innovator Remynt has secured a strategic investment from One Washington Financial, the wholly-owned holding company of WSECU (Olympia, Washington). As part of the investment, Remynt, which won Best of Show in its Finovate debut at FinovateSpring last year, will also become a Credit Union Service Organization or CUSO.

“Since Remynt’s founding, our goal has been to support credit unions because we align closely in our support for financial wellness,” Remynt Founder and CEO Gwyneth Borden said. “We are thrilled to have the support of One Washington Financial and WSECU. This investment will help us scale our business and serve more credit unions to achieve higher recoveries while supporting member financial health.”

Founded in 2022 and headquartered in San Francisco, California, Remynt is a digital-first debt and credit recovery company. Remynt enables creditors to recover revenue from non-performing delinquencies and empowers consumers to resolve debt on their own terms thanks to a customer-centric, resiliency-oriented approach. Users of Remynt resolve their outstanding debts via a credit builder that links debt payments to a positive credit tradeline. The Remynt platform features credit score insights, personal finance management tools, and access to other financial wellness resources.

Thanks to this week’s strategic investment, and Remynt’s new status as a CUSO, the company will be able to quickly scale its solutions to support more credit unions and help them achieve economies of scale and operational efficiencies through shared resources and specialized expertise.

“Our partnership with Remynt aligns with our mission to create meaningful community impact by providing access to equitable and innovative financial solutions,” One Washington Financial Principal Scott Daukas said. “By including Remynt as part of WSECU’s financial wellness strategy, we directly contribute to our members’ financial stability, growth, and development.”

I caught up with Gwyneth Borden late last week to talk about Remynt’s investment news, its goals as a CUSO, and what credit unions want—and need—from their fintech partners. An edited transcript of our conversation is below.

As a small business owner in this space, how did you feel about 2025 as the year began?

GwynethBorden: I think there had been this sense of optimism. The stock market was going up. People thought things were going to be moving in a better direction.

And so I think we were optimistic going into 2025, initially thinking that consumer confidence had diminished and that 2025 might be a better year if people felt like things were moving in a different direction in the country and maybe that would be a positive thing.

Obviously what we didn’t anticipate were the tariffs, and the crazy back and forth and fluctuations in prices as a consequence. The uncertainty. People losing their jobs.

What’s interesting now is that this is kind of a wait-and-see economy. A lot of people are holding back. Talking with others—with credit unions or people in the collections world—typically tax season is a huge windfall. Everybody pays their debt off in the tax season and we didn’t really see that this year.

Why become a CUSO—a Credit Union Service Organization—now?

Borden: A big part of it, of course, is that we were fortunate to get an investment from One Washington Financial, which is WSECU. And in order to accept that investment, you have to be a CUSO, a credit union service organization. That was fine with us because it very much was aligned—from the very beginning—with our focus on supporting credit unions. We’re just delighted about the opportunity, to really stake our claim in the credit union space and say, “We are really here to be your partner.”

We are especially interested in serving a lot of smaller credit unions; in fact, part of our goal for our CUSO is at least 20% of the credit unions we serve be smaller than $300 million. A lot of tech companies don’t want to serve those businesses because they find it not to be enough revenue or volume for them. But the way our platform is built, it doesn’t really matter if you have two members on the platform or hundreds of members on the platform. It doesn’t cost us any more.

We’re also excited about bringing on WSECU as a customer, as well. They are a $5 billion-plus credit union, so it’s a really exciting opportunity for us to really scale substantially the number of people that we’re getting to serve.

Based on your conversations, what is it that credit unions want—or need—most from their fintech partners?

Borden: For credit unions in general, most of them are really trying to figure out how they can grow their businesses. Every single financial institution, including credit unions, makes money from lending. And in these precarious times, being able still to lend and provide the products people need for their lives (is important). A lot of them are starting to ask: Do we do small dollar loans? Are there credit voucher products? They are looking to see how they can expand their services to better serve the communities around them.

What can we expect to see and hear from Remynt over the balance of the year and into the next?

Borden: We are going to be expanding exponentially and bringing on more credit unions. We are going to release a white-label version of our platform in the latter part of the year that includes some AI agents. So it’s kind of an exciting development in the digital collections space. You’ll see a number of developments on our platform that we’ll be launching later this year, as well as some exciting partnerships with additional credit unions. We’re really staking our claim in a particular area in the credit union space, which I’m really excited about.

The challenge of third-party risk in financial services was one of the biggest stories in 2024. From the fallout from the Synapse bankruptcy to the data breaches at firms such as Fidelity and Finastra, banks, fintechs, and financial services alike have been put on notice to put greater scrutiny on whom and how they forge partnerships.

These challenges have only become more intense this year. While regulations are tightening in Europe and the UK, a more permissive regulatory environment is developing in the US. How can banks, fintechs, and financial services companies navigate this emerging landscape to bring new products and services to customers while ensuring that their data and finances are safe?

We interviewed Jenna Wells, Chief Operating Officer with Supply Wisdom, to talk about the issue of third-party risk management in financial services in 2025. Wells talks about how third-party risk in financial services is evolving, and what companies need to do in order to better manage it.

Headquartered in New York and founded in 2017, Supply Wisdom made its Finovate debut at FinovateFall 2022. The company helps businesses better manage risk and build operational resilience. Supply Wisdom provide continuous full-spectrum third-party and location risk intelligence and risk actions in real-time to prevent disruptions, enhance risk management efficiency, and lower costs. Tom Thimot is CEO.

Our conversation with Jenna Wells is also the final installment of Finovate’s commemoration of Women’s History Month for 2025. Previous interviews include our Q&As with Tracy Moore of Fenergo and with Stav Levi-Neumark of Alta.

What are the current challenges your customers are facing?

Jenna Wells: The biggest challenge our customers face today is the sheer complexity and speed at which third-party risks are evolving. As a whole, companies are under immense pressure to monitor their vendors, suppliers, and other third parties more effectively across financial, cyber, ESG, geopolitical, and operational risk domains without adding significant costs or delays to their business processes. Traditional risk assessment methods, which rely on periodic reviews and self-reported questionnaires, are no longer sufficient in an era where threats emerge in real time and rarely any warning.

Additionally, companies are struggling with regulatory compliance, particularly with new frameworks like DORA in the EU, new AI risks and regulations, and emerging cyber risk mandates. Many organizations simply lack the tools, resources, or expertise to stay ahead of these challenges.

Lastly, the evolving geopolitical landscape and regulatory environment require companies to keep an eye out for location-specific risks on top of the traditional domains. Monitoring third parties alone is no longer sufficient—you must monitor the locations that they are operating from!

Can you talk about the challenge of third-party risk specifically, which became a major concern in 2024?

Wells: Third-party risk became a critical concern in 2024, exposing just how fragile global supply chains can be. This was starkly evident in global events like the collapse of the Francis Scott Key Bridge in Baltimore and earthquakes in Taiwan, which disrupted key transportation routes and severely impacted businesses dependent on the affected port. Companies with suppliers, logistics partners, and critical infrastructure tied to these regions faced massive operational slowdowns, financial losses, and regulatory challenges. These disruptions reinforced a key lesson: risks stemming from a single geographic point of failure can have widespread consequences across all industries.

Static, periodic risk assessments are no longer enough. The new standard is continuous, real-time risk monitoring that provides visibility into financial stability, cybersecurity, compliance, and operational resilience—not just for direct suppliers, but across the entire supply network.

This shift is particularly crucial in industries reliant on complex, geographically dispersed supply chains, where a localized disaster—whether infrastructure failure, geopolitical instability, or extreme weather—can ripple outward, affecting entire markets. The challenge is no longer just about assessing third parties. It’s about identifying vulnerabilities deep in the supply chain.

How does Supply Wisdom help companies manage these risks?

Wells: Supply Wisdom provides real-time, AI-driven continuous monitoring across seven critical risk domains: financial, operational, compliance, cyber, sustainability, Nth party, and location-based risks. Instead of relying on outdated, self-reported assessments, or the need to use multiple tools to monitor single domains, we aggregate and analyze data from hundreds of thousands of open sources, giving our customers a live, always-on view of their third-party supplier and critical ecosystem.

By leveraging AI to turn massive amounts of data into actionable intelligence, we enable organizations to identify emerging risks early, mitigate issues proactively, and avoid costly disruptions. Our platform reduces the manual burden of risk management, allowing teams to focus on strategic decision-making rather than chasing data.

Supply Wisdom recently published its top 10 predictions for third-party risk management in 2025. Of those predictions, which do you think is the least conventional?

Wells: One of the more unconventional predictions is the rise of “Nth-party accountability” as a regulatory and business priority. Until now, companies have focused primarily on direct third-party risks, but regulators and stakeholders are increasingly scrutinizing deeper layers of the supply chain. This includes fourth, fifth, and even sixth-party risks.

As supply chains become more interconnected and reliant on subcontractors, understanding who your third parties depend on and where they are located has become just as critical as assessing the vendors themselves. Geographical risks like political instability, natural disasters, regulatory changes, and ESG concerns can have cascading impacts throughout the supply chain, even if they originate at the Nth-party level.

We anticipate that in 2025, organizations will be expected to not only monitor but also take responsibility for the risk posture of their vendors’ vendors. This requires real-time visibility into where these extended third parties operate and the regional risks that may affect them. This shift demands an entirely new approach to risk visibility, and Supply Wisdom is already helping companies address this challenge with location-based monitoring, real-time risk intelligence, and deep Nth-party insights.

What role do technologies like AI and strategies like predictive risk modeling play in Supply Wisdom’s approach to risk management and intelligence?

Wells: AI and predictive risk modeling are foundational to how we help companies stay ahead of emerging threats. Our AI-powered platform continuously scans and analyzes millions of risk signals across financial, cyber, ESG, geopolitical, and operational domains, detecting anomalies and trends that may indicate potential threats before they materialize into full-blown crises.

Predictive risk modeling and trend analysis takes this further by using historical data, machine learning algorithms, and real-time signals to forecast risks before they impact business operations. For example, we can predict financial distress in a vendor before it becomes public knowledge or identify early signs of operational instability in a supplier’s key locations.

In short, Supply Wisdom stands for proactive risk management and innovation. We’re known in the industry as the only full-stack risk intelligence platform that provides real-time, continuous monitoring with actionable insights.

A wave of new regulatory policies is coming, particularly in the EU. Are you optimistic about the new policies? Do you feel as if organizations are ready to comply?

Wells: I am optimistic about these policies because they are pushing organizations towards a higher standard of operational resilience and risk management. Regulations like DORA in the EU are reinforcing the idea that businesses cannot afford to be passive when it comes to third-party risk—they need real-time, continuous oversight. However, I don’t think most organizations are fully prepared for these changes.

A majority of organizations do not have a complete inventory of their third parties or outsourced services and, without this, they cannot ensure compliance with these regulations. Unfortunately, it’s most likely that these companies still rely on outdated, static assessment models that won’t meet compliance requirements.

The good news is that regulatory clarity is driving investment in solutions like Supply Wisdom, which help organizations not only meet compliance mandates but also improve their overall risk posture in the process.

In the US, there is more uncertainty about which direction regulations are likely to go. What do you see happening with financial services and fintech regulation in the US this year?

Wells: If US firms want to compete and do business in Europe; they need to comply with those specific mandates. But unlike the EU—which has taken a structured approach with DORA—the US regulatory landscape is evolving in a more fragmented manner. However, we expect to see increased scrutiny from agencies like the SEC, OCC, and CFPB on third-party risk, particularly in areas like cyber resilience and AI disclosures.

The financial services and fintech sectors will likely see more pressure around vendor risk management, with a greater emphasis on continuous monitoring, and incident reporting requirements. As regulatory guidance increases, companies will need to be proactive in adopting best practices that align with global compliance trends, rather than waiting for enforcement actions to dictate their next steps.

What are your near-term goals for Supply Wisdom?

Wells: My immediate focus is on accelerating customer adoption of continuous risk monitoring. We want to ensure that organizations not only understand the importance of real-time risk intelligence through continuous monitoring, but also have the tools to integrate it seamlessly into their existing workflows.

Additionally, I’m prioritizing scaling our operations to meet the growing demand for proactive risk management solutions. That means enhancing our AI capabilities, monitoring for AI as an emerging risk, expanding our risk intelligence coverage, and strengthening our partnerships with other industry leaders.

What can we expect from Supply Wisdom in 2025?

Wells: 2025 will be a transformational year for Supply Wisdom and the third-party risk management industry as a whole. We are investing heavily in AI-driven risk prediction, enhanced regulatory compliance automation, and planning ways to go deeper and wider into Nth-party risk visibility.

You can also expect to see more partnerships with technology and service providers to create a more integrated risk management ecosystem. Our goal is to make continuous risk monitoring the new standard, so that businesses can operate with greater confidence, resilience, and agility in an increasingly complex world.

As European financial services companies and fintechs brace for a wave of new regulations, their counterparts in the U.S. are anticipating a strong trend in the opposite direction as President Trump and the Republicans take control of the government.

Right now, with 2025 barely underway, U.S. regulators in a number of instances are still in crack-the-whip mode with regard to fintechs and financial services companies.

Last week, we learned that Digital Currency Group will pay a combined $28.5 million in civil penalties for misleading investors about the financial condition of its subsidiary, Genesis Global Capital. Also last week, American Express agreed to pay $230 million to settle charges of alleged deceptive sales charges for credit card and wire transfer products to small businesses. Mastercard will have to pay $26 million to settle a gender and race bias-based class action lawsuit.

A little earlier this month, the Consumer Financial Protection Bureau (CPFB) announced that it was suing Capital One for allegedly cheating millions of consumers out of more than $2 billion in interest. The Commodity Futures Trading Commission convinced a U.S. District Court to enter a consent order against Gemini Trust Company with a $5 million civil monetary penalty. Also this month, the SEC reported charges against nine investment advisers and three broker-dealers for recordkeeping failures and issued fines totaling more than $63 million. Speaking of the SEC, it has ordered popular brokerage Robinhood to pay $45 million in penalties over a variety of compliance failures.

You get the picture. The question is, with the arrival of the Trump team, how much of this regulatory oversight is likely to go dark?

In the U.S., the focus will be on agencies like the SEC and the CPFB. On his first day in office, President Trump issued a regulatory freeze. This will prevent agencies from implementing proposed rules until an agency appointed by the Trump administration reviews the specific regulation. The Trump administration has not spoken directly about the CPFB, though it is widely believed that the current director Rohit Chopra will be fired if he does not resign.

What proposed rules from the CPFB might find themselves in the freezer? There are a few worth highlighting. These include the CPFB’s rule limiting the ability of financial institutions to charge overdraft fees, which is slated to go into effect in October, as well as a rule banning the listing of medical debt on credit reports that was issued just last month. Another key ruling relates to aspects of the Truth in Lending Act (TILA) and its requirements for Property Assessed Clean Energy (PACE) transactions.

The CPFB is sufficiently concerned about the changes likely to come from the Trump administration that it has issued a report called “Strengthening State-Level Consumer Protections.” The report, which states the case for consumer financial protection laws going all the way back to the Woodrow Wilson administration at the beginning of the 20th century, speaks loftily about the importance of federal-state partnership when it comes to protecting consumers. It even praises state-level legislation for providing “an important source of information” to Congress and federal regulators, enabling them to better “adjust standards over time.”

Nevertheless, analysts have suggested that the report appears to be an attempt to encourage state legislatures to adopt their own consumer protection laws in the event that consumer financial protection laws at the federal level are weakened or removed entirely. Given the intensity and eagerness with which the Trump team is taking to its task, that might not be such a bad idea.

How can banks and other financial institutions defend themselves and their customers and members against increasingly sophisticated, increasingly organized financial crime? What are the most challenging fraud threats and, critically, what tools and tactics are available to help institutions deal with them successfully?

We talked with Gus Tomlinson, Managing Director, Identity Fraud, with identity verification, location intelligence, and fraud prevention solutions provider GBG, about the challenges faced by companies and organizations when it comes to fighting evolving fraud threats.

Helping companies around the world onboard customers safely, fight fraud, and stay compliant, Tomlinson has more than a decade of experience in the identity industry. She has worked in strategic, commercial, data, and product roles and, this year, was named to Management Today’s 35 Women Under 35 roster for 2024.

Tomlinson is also a supporter of Women in Identity, a non-profit that promotes a more diverse workforce in the digital identity industry.

We wanted to talk with you about the spike in Synthetic Identity Fraud (SIF). What is SIF? What industries are being impacted most?

Gus Tomlinson: Synthetic identity fraud is a fraud tactic many businesses struggle to identify. This is because it uses a mix of genuine, stolen personally identifiable information (PII), and manufactured synthetic data to create a fake identity. This fabricated identity is then used to open accounts, make purchases, and commit other fraudulent activities.

The blending of real PII such as name and address with a different date of birth data for example, is common, and amongst more sophisticated scams, fraudsters will go beyond data to include fake identity documents, fake photos and videos, and even other biometric characteristics, like fingerprints. These ‘identities’ allow fraudsters to apply for low-friction accounts where there are no or limited checks to build up their credit history.

Often synthetic identity fraudsters will play the long game as their credit history improves – increasingly getting access to higher value finance and goods before disappearing without a trace, leaving the affected businesses trying to collect from people who never existed in the first place.

The industries particularly vulnerable to synthetic identity fraud are those that handle high value data and offer potential financial gains for fraudsters – financial services, gaming, and government sectors are key examples. Though it’s important to remember that all industries are vulnerable – fraudsters don’t limit their activities to one organization, sector, or even stop at national boundaries. They target where they see an opportunity.

What makes fighting SIF a challenge?

Tomlinson: Fighting synthetic identity fraud is a challenge due to the sheer scale it’s being – and has been – leveraged by fraudsters. The lack of preparation from businesses has led to them letting in huge numbers of sleeping identities that are now ready to attack.

Organizations need to act now as this threat will only continue to increase. On the dark web, thousands of sites are selling cheap bundles of identity data from billions of records stolen in cyberattacks and data breaches every year. All the info needed to impersonate someone is easily available within a few clicks and for a few dollars.

Digital identity is complicated, and synthetic identity fraud takes advantage of that by blending real and fake data to slip through the cracks. Technological advancements, such as Generative AI (GenAI), are also increasing the sophistication of synthetic identities, making it even harder to spot. To catch this kind of fraud, detection methods need to handle that complexity and use all the digital identity data out there to spot the fraud signals. Building up several layers of defense is critical.

How high on the list of priorities is this for companies? Do they understand the threat posed by SIF and other AI-powered fraud tactics?

Tomlinson: Fraud is hitting the bottom line – estimates show businesses are losing around five percent of their revenues to fraud annually. Now GenAI has given fraudsters new capabilities to work faster, scale attacks, and create more believable scams. The threat has risen to a new level.

As a result, digital identity verification and fraud prevention has moved from a tick box exercise to a business imperative and more than ever identity fraud is a boardroom topic.

While this is a step in the right direction, what is still missing is an appreciation for – or acceptance of – the true extent of the problem.

Synthetic identity fraud isn’t new, it’s been happening for years. Many organizations are far more exposed today than they might think.

What we see is that many companies try to ignore that the problem is already intrenched in their operations. They need to accept this part of the problem to truly protect against it.

You’ve spoken about “cross-sector industry collaboration” as key to helping deal with AI-powered fraud. Why is this the best strategy?

Tomlinson: Synthetic identity theft is just one of the fraudulent threats today. Businesses need to build a layered defense to fraud prevention to protect against current and new fraud tactics. For example, a combination of credit bureau data checks, mobile data, document verification, biometric checks and other alternative data, such as cross-sector intelligence, is a key part of a proven multi-layered approach that strengthens the identity verification process by providing a more robust and informed way of validating identity and spotting fraudsters.

Ultimately, it’s about leveraging the strengths of each component. AI can process vast amounts of data and identify patterns quickly. Human fraud experts bring critical thinking and experience to interpret AI findings and make nuanced decisions. Cross-sector collaboration allows for sharing of intelligence and best practices, making it harder for fraudsters to exploit gaps between industries and organizations.

How difficult is it to coordinate all those pieces into a coherent, fraud-fighting operation?

Tomlinson: It shouldn’t be complex for organizations – identity experts like us are doing the hard work in the background to bring everything together – that’s why we exist! Plug-in onboarding systems are available to orchestrate identity verification at an intelligent, adaptable level. These identity verification and fraud prevention technologies deliver greater speed and accuracy, calculating the absence or presence of fraud signals and adjusting the customer journey accordingly so there is minimal friction for genuine customers.

How can effective fraud-fighting co-exist with the kind of seamless, real-time experience that consumers have come to expect?

Tomlinson: Actually, more than ever consumers value and prioritize security over convenience. In fact, our latest Global Fraud Report revealed 68% of U.S. customers place greater importance on the security of the onboarding process over its speed.

In the recent past, with organizations fighting in competitive landscapes to provide the best onboarding customer experience, reducing friction has been seen as critical. However, as fraud, data breaches and security news stories increasingly become dinner-party conversations, consumers are more actively looking for and comforted by visible security measures. Now, it’s critical for organizations to understand that friction doesn’t equal a bad customer experience.

With cross-sector intelligence, organizations can detect bad, good, and great customer prospects and give them a tailored experience corresponding to their risk level, including when and how to use step-up authentication through documents or biometrics in this time of increasing use of GenAI by fraudsters.

What is GBG doing specifically to help businesses combat SIF and other forms of AI-powered fraud?

Tomlinson: Data tells a story and we help you read it. We understand the data that is being presented and verify against it, giving businesses clarity on exactly what they are making decisions on. This is fundamental to preventing synthetic identity fraud.

While GenAI is making fraud tactics smarter, the same is true for fraud detection and prevention. Our solutions leverage AI to quickly sort through and scrutinize huge amounts of digital data, flagging identities that are high, medium, and low trust. We also implement injection attack detection technology for the new era of synthetic identities where fraudsters are matching data with biometric images.

Critically, we layer documents, biometrics, digital, and data checks to give businesses complete defense. Our multi-layered approach strengthens the identity verification process by providing a more robust and informed way of validating identity and spotting fraudsters.

Looking to 2025, what do you expect to see in terms of new trends in the fraud and financial crime landscape?

Tomlinson: In the coming year, expect to see:

A rapid pace of attack – established organized crime groups have made fraud their profession and stable source of income. GenAI combined with the industrialization of fraud means more fraud at a faster pace.

Brand damage attacks and an ulterior motive of fraudsters – the damage to a business’ reputation can cause more financial loss than the actual fraud itself. This is a powerful tool for a malicious actor to have in their toolbox.

Increased cross-border fraud – fraudsters don’t limit their activities to one organization, sector, or even stop at national boundaries. They target where they see an opportunity, which is increasingly cross border attacks.

Fraudsters recycle old methods –as companies pivot to defend against new fraud vectors with the latest technology, we’ll see fraudsters go back and use old fraud tactics to see if they can find a re-opened gap in the system to slip through. Businesses can’t afford to get complacent.

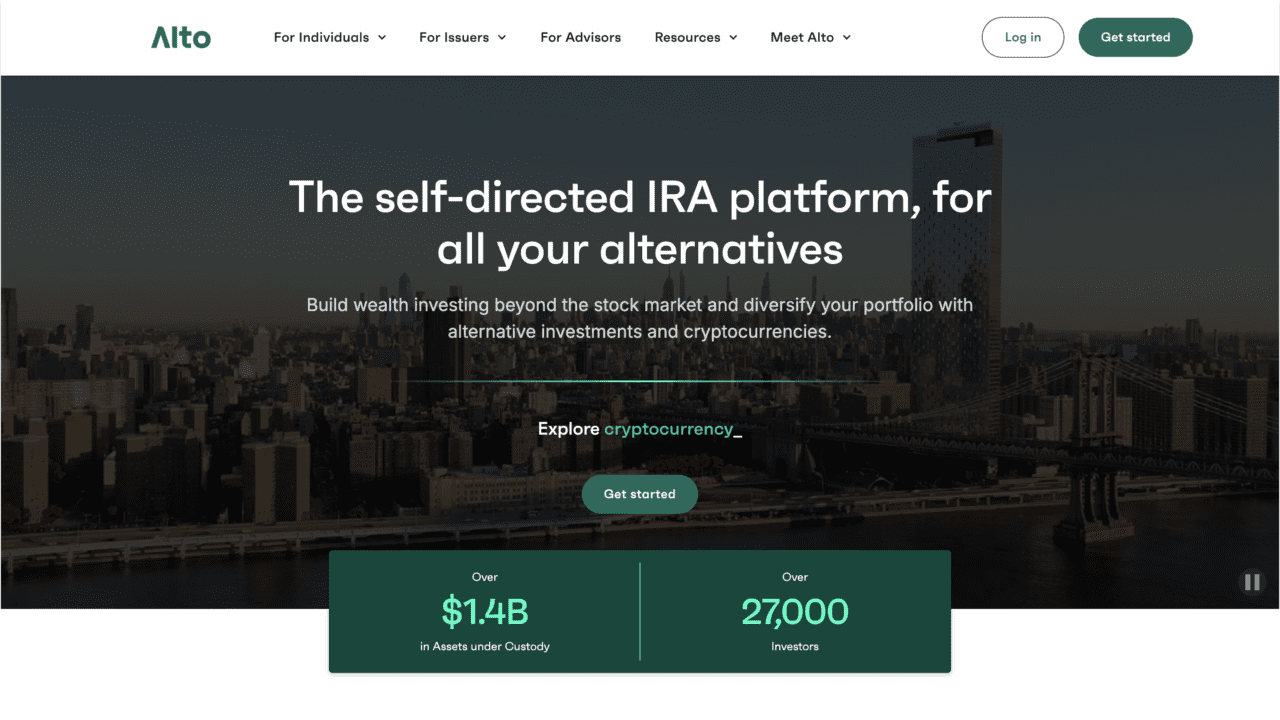

With markets near all-time highs and Bitcoin teasing the $100,000 mark, investors have become increasingly interested in new opportunities to diversify their investments, reduce risk, and grow their wealth. Unfortunately, there are many assets — from cryptocurrencies to real estate to art — that can be difficult for investors to access and incorporate in their overall investment plan.

In this month’s column, I caught up with Scott Harrigan, President of Alto and CEO of Alto Securities. Alto provides a self-directed investment platform that empowers investors to build their wealth by investing not just in stocks, but also in alternative investments, including cryptocurrencies. The platform supports more than 27,000 investors and has more than $1.4 billion in assets under custody.

Alto has three primary divisions: Alto Solutions, a self-directed IRA administrator; Alto Securities, a wholly-owned registered broker-dealer; and Alto Capital, an exempt reporting advisor that provides alternative investment opportunities to accredited investors. Alto Solutions made its Finovate debut at FinovateFall 2023 in New York with founder and CEO Eric Satz leading a demo of the company’s Alto IRA offering.

In this conversation, Harrigan talks about the pain points investors have when trying to integrate alternative investments into their portfolios and what Alto does to help resolve these issues. We also talked about the opportunities a growing number of investors are seeing in crypto and the challenge of making historically difficult-to-access private investments available to a broader community of investors.

Headquartered in Nashville, Tennessee, Alto was founded in 2015.

What problem does Alto solve and who does it solve it for?

Scott Harrigan: Alto aims to lower the barrier to entry for alternative investments, making alternatives available within an IRA so investors can diversify their retirement savings, reap the benefits of reduced volatility, and have the potential to increase returns. Alto IRA account users can benefit from tax-advantaged investment options in a wide range of alternative assets, including private equity, venture capital, real estate, art, crypto and more, providing them with the opportunity to diversify their investment portfolio while planning for retirement.

How does Alto solve this problem better than other companies or solutions?

Harrigan: With the goal of lowering the barrier to entry, Alto addresses these two pain points: investors want to understand their various alternative investment options and they want easy access to these types of investments in a streamlined platform.

Alto is the only digitally native self-directed IRA provider with multiple alternative investment options. This is unique because many legacy IRA providers have been around for decades and continue to operate in the same fashion they always have, showing no urgency to grow or evolve. They are overlooking the importance of the digitally-oriented experiences that individuals demand these days. Alto understands the importance of being digital-first and bringing a seamless and enjoyable experience to investors.

As for providing multiple alternative investment options, we are forging diverse opportunities in how and where individuals invest their retirement dollars. Alto offers Traditional, Roth, and SEP IRAs so investors can select the right vehicle for their money based on their unique goals, and individuals have the option to put their retirement funds toward anything from biotech to bitcoin, wine to whiskey, and farmland to fine art.

Who are Alto’s primary customers and how do you reach them?

Harrigan: Our goal is to bring alternative investments to everyday investors, and we do this by removing the hurdles that have long prevented them from investing in this sector. There are three areas key to our success in expanding access and awareness. The first is expanding the number and type of investment opportunities offered, so that individuals have freedom of choice and can identify what options are right for them. The second is creating a user-friendly digital experience that makes investing in alternatives more approachable. Last, but certainly not least, is providing education, and disseminating more information and resources to help investors make confident investment decisions.

In addition to expanding our reach more broadly, we also curate opportunities for accredited investors. This past year, we launched Alto Marketplace, a new part of the Alto platform dedicated to curating private alternative investment opportunities for accredited investors. The platform allows eligible investors to invest in historically difficult-to-access private investments which are curated specifically by Alto. Investors now have access to private equity, venture capital, real estate, fine wine, art, and more, all in one platform.

Can you tell us about a favorite implementation or deployment of your technology?

Harrigan: Our technology provides investors access to unique investment opportunities in the alternatives space within an IRA. We provide opportunities for investors to build wealth beyond the stock market and diversify their retirement portfolio with alternative investments.

As part of our commitment to enabling individuals to invest in a wider variety of alternative assets, we were proud to go live with the Alto Marketplace this past year. Marketplace enables Alto’s users to enjoy a streamlined, consolidated investing experience as they explore offerings that range across a variety of different asset classes. Accredited investors can benefit from alternative assets that may offer portfolio diversification and a chance of achieving long-term financial stability in today’s volatile market.

What in your background gave you the confidence to tackle this challenge?

Harrigan: My experiences have helped me become deeply familiar with SEC and FINRA guidelines, critical to bringing fair, transparent and compliant opportunities to the everyday investor. Having worked in private markets for the past seven years, I gained a much deeper understanding of how alternative asset investment structures work and how we could work within regulatory guidelines to provide the access that we have today. Creating special purpose vehicles is complex, but we do it because we want to bring a modernized and simplified experience for investing in alternatives.

You recently announced a partnership with SignalRank? Why team up with SignalRank? What will this partnership accomplish?

Harrigan: As mentioned, we launched Alto Marketplace to curate exciting private alternative investment opportunities for investors. Partnering with SignalRank, the first private markets index made up of preferred Series B shares in high growth venture-backed companies, is in line with our commitment to provide investors with wider access to investment opportunities that, by nature, were formerly more exclusive.

We have had prior venture capital opportunities through our Marketplace, but SignalRank is unique in that its algorithm has successfully predicted successful transitions of Series B startups to billion dollar companies. This partnership will help us accomplish our goal to bring unique strategies that aren’t more widely publicly available, and have been largely limited to ultra-high-net-worth individuals and institutional investors, to more investors. Alto’s special purpose vehicles bring investors these opportunities at lower thresholds, for example by lowering the minimum investment to $25,000 whereas typically it might be closer to $500,000 or even higher.

What excites you about the growth of the alternative asset market? Is there an education gap to be covered in order to get more eligible individual investors interested in alternative assets?

Harrigan: I am excited about how we’re in the early days for the alternatives space. The industry is just starting to recognize how big alternative investments will become in the next five years. If you don’t know what this business is about, you’re going to need to, because this is where wealth management is headed in the next five years.

Because we are in the early days, there is absolutely an education gap. Our original study found that a lack of familiarity with alternative investments was the most significant barrier to investing in these assets as part of a diversified retirement portfolio. One common misconception is that the long-term nature required of some alternative assets is a drawback. However, there is a definite advantage in combining the tax efficiency of self-directed IRAs with the extended investment horizons of alternatives. This long-term alignment allows investments to compound and realize strong returns.

As alternatives are poised on this incredible growth trajectory, we’re excited to be ahead of the curve in providing education on how Alto IRA account users can benefit from tax-advantaged portfolios and outsized returns.

What are your goals for Alto? What can we expect to hear from you in the months to come?

Harrigan: In 2025, we expect to bring a much larger variety of alternative investments to our platform. In 2024, we launched 15 deals, so we expect to continue on this momentum and bring investors even more optionality and choice.

We’re also keeping an eye on the preferences of Gen Z and Millennials, two groups that research shows are engaging with investments differently than the generations before them. Notably, those aged 21 to 43 are currently more likely to choose alternatives over stocks.

Last, we will continue to advance our proficiency in how we educate investors. We feel a significant obligation to provide investors with as much information as possible so that they can make informed, confident decisions about their retirement savings. In line with this strategy, we plan to focus on scaling information about and access to Alto CryptoIRA. Crypto presents an immense opportunity for investors to diversify their portfolios and realize greater returns. We want to make more individuals aware of the opportunity they have to invest in crypto as part of an IRA.

Which presidential candidate will be better for fintech over the next four years?

Of all the issues roiling the presidential campaign in 2024, it is safe to say that the future of fintech is not among the top two or three. Nevertheless, it is also safe to say that the fintech industry under a Trump administration will face different challenges and opportunities than it would under a Harris administration.

Let’s first look at how the policies of Republican candidate Donald Trump might impact fintech and financial services more broadly.

“The Crypto President”

Whether or not “they” are calling Donald Trump “The Crypto President,” the man who once called Bitcoin “a scam” has since had a change of heart when it comes to cryptocurrencies.

The now-famous quote — “You know, they call me the crypto President …” — comes from an ad the former president ran in August marketing his fourth series of non-fungible token (NFT) digital trading cards. Earlier this year, Trump suggested creating a “strategic national bitcoin stockpile” with the goal of ensuring that America is the “crypto capital of the planet.”

While not prominently noted on the Trump campaign’s website, the Republican party platform with regards to digital assets includes a reference to the opposing party’s “unlawful and unAmerican Crypto crackdown” on the one hand and opposition to “the creation of a Central Bank Digital Currency” on the other. The party, whose positions are likely identical to those of the former commander-in-chief, also pledges to defend the right of American citizens to mine Bitcoin and to self-custody of their digital assets.

Republican re-deregulation

The idea of a Republican president embracing deregulation in general has been baked into voter perceptions of the party since the 1980s, at least. And as Jamie Dimon, Chair and CEO of JPMorgan Chase, rails against regulators (“if you’re in a knife fight you better damn well bring a knife,” he recently told attendees at the American Bankers Association Convention), the question is whether the Trump administration is likely to supply Mr. Dimon with the silverware he seeks.

Looking again to the RNC platform, the most specific reference to deregulation is a pledge to “reinstate President Trump’s Deregulation Policies” as part of the former president’s plan to “Cut Costly and Burdensome Regulations.” If past is prologue, then Trump’s signing of the Economic Growth, Regulatory Relief, and Consumer Protection Act in 2018 could provide some clues. Here, we find initiatives to expand access to mortgage credit, incentivize capital formation, and provide additional protections for student borrowers.

Do tax cuts + tariffs = inflation?

Aside from tax cuts, the most noteworthy element of Trump’s economic plan is his embrace of tariffs on goods manufactured outside of the United States. In fact, the former president has gone so far as to suggest that the income tax be eliminated in favor of his new, tariff-based approach to funding government operations.

And while this is extremely unlikely, the combination of Trump’s tax cut proposals and his enthusiastic attitude toward tariffs could ironically pave the way for an economy that is more vulnerable to inflation. This could lead, ultimately, to higher interest rates and tighter monetary policy compared to where the American economy is at the end of 2024.

You don’t have to be a long-time, fintech veteran to remember the devastating impact that higher borrowing costs can have on the startup community — or its financiers. And it is hard not to fear that a “double-dip” resumption of these conditions could leave startups and their backers in an even more constrained and risk-averse position than they have been this year.

Now let’s look at how the policies of Democratic candidate Kamala Harris and how they might impact the fintech industry.

From big banks to junk fees

A story in today’s Washington Post highlights Vice President Kamala Harris’s tenure as California attorney general and her role in strengthening a “multibillion dollar mortgage settlement” with major banks in the wake of the Great Financial Crisis. Not only is this a significant component of Harris’s resume, it is also a tale she eagerly tells while on the campaign trail.

It is worth noting that, for all the fighting words, most observers expect the Vice President to be more business-friendly than the notoriously pro-labor current President. Nevertheless, it is easy to see a Democratic administration looking to fortify and even extend a range of consumer protections in financial services.

That said, the emphasis from the campaign is less about bashing the big banks and more about addressing the smaller annoyances of everyday consumer life. Under the banner of ‘Lower costs by protecting consumers from fees and fraud,’ for example, the Harris campaign pledges to ban junk fees across the board and make it easier to cancel unwanted subscriptions.

Economies of opportunity

The Harris campaign has touted its concept of an “Opportunity Economy,” in which the federal government plays an active role in helping individuals, families, small businesses, and communities maximize their ability to thrive in a capitalist economy. This includes launching a small business expansion fund that leverages low- or zero-interest loans to help entrepreneurs grow their businesses and create jobs. This “Opportunity Economy” also mandates that the federal government commit to allocating a third of its contracts to small businesses, reducing the number of excessive occupational licensing requirements, and helping small businesses cut bureaucratic red tape and file taxes more easily.”

The Vice President’s plan does target startups specifically, setting a goal of 25 million new business applications over the next four years, and a tenfold expansion of the startup expense deduction from $5,000 to $50,000. Additionally, Harris’s campaign calls for an “America Forward” tax credit designed to incentivize investment and job creation in “key strategic industries” as well as “scaling up and making permanent” the National Artificial Intelligence Research Resource. The latter is a shared research infrastructure that provides startups and researchers with access to computing power, data, and analytics tools to support innovation in AI.

Housing and the “sandwich generation”

Two areas of the Vice President’s agenda — the pledge to build more housing and the goal of making both day care and elder care easier and more affordable for caregivers — could have interesting impacts on financial services and fintech. The former, which includes a plan to build three million additional homes and provide $25,000 in down payment assistance, could send a jolt through the financial services industry that would impact bankers, lenders, and mortgagetechs alike. The campaign is also championing tax credits to encourage homebuilders to build affordable homes and a Neighborhood Homes Tax Credit, which supports “investment in homes that would otherwise be too costly or difficult to develop or rehabilitate.”

The latter proposal — to ease the financial burden of Americans who are caring for both young children and elder parents — does not make a prominent appearance in the Harris campaign’s website. But those who have heard the Vice President speak in recent weeks are familiar with the challenge, which she describes as the fate of the “sandwich generation.” The Harris campaign has suggested a number of remedies — from Medicare expansion to boosting the pay of homecare workers. What is interesting from a fintech perspective is the idea that resources devoted to eldercare in particular could draw attention to the work of fintech innovators from Golden, to Eversafe, to Bereev that specialize in providing financial services to seniors and those who are caring for them.

Many of these plans from the Harris campaign will require the approval of a Congress that could easily remain split between the two parties. While that may limit the scope of even the successful initiatives, it would provide the kind of balance (or, if you prefer, gridlock) that has often accompanied strong economies. And that, in itself, would be a good thing not a bad thing for fintech and financial services.

Should more financial advisers be treated as fiduciaries? Even for one-time financial recommendations like a 401(k) rollover?

The Washington Post recently published an article looking at the battle over the needs of recent retirees on one side and what critics have called “lucrative broker commissions” on the other. At issue is an effort by the Biden administration to force brokers to act as fiduciaries, which means that they must place client needs above all else, including their own paychecks. The administration is especially concerned about what happens when millions of Americans retire or roll over their retirement savings in favor of tax-advantaged accounts such as IRAs. This is a huge market; the federal government estimates that these transactions are valued at more than $770 billion in 2022.

In many, if not most instances, these transfers from 401(k)s and similar products into IRAs is unremarkable. But the administration is looking closely at some transfers, in which investors’ retirement money is invested in instruments such as annuities. Annuity products, in which retirees give funds to an insurance company that provides them with a fixed, annual payout, not only often have costly restrictions – such as big penalties for early withdrawals and caps on returns – but also can be more lucrative products for insurance agents to sell compared to other investments. This – from the Biden administration’s perspective, and that of some consumer advocates – creates a conflict of interest that can lead to savers being steered toward investments that are not optimal for them.

As such, Biden’s Department of Labor extended fiduciary duties under the Employee Retirement Income Security Act to cover one-time recommendations issued to retirement investors. This puts a number of activities traditionally not covered by the fiduciary rule, including those rollovers noted above, under the rule. The policy was finalized in April and was set to take effect next month.

For their part, critics of the administration’s policy see the attempt to change regulations as a “costly, illegal federal mandate.” In an unsigned statement (ahem!) one of the organizations that sued to stop the Biden’s administration, the American Council of Life Insurers, warned that new fiduciary requirements could “deprive millions of consumers of access to much needed retirement financial guidance and protected lifetime income products.”

So far, the courts – and Congress – have agreed with the critics. Congress made initial moves toward invalidating the new rules in July, with a congressional committee passing a resolution to overturn the rule. Additionally, two federal judges have separately blocked the Biden administration from implementing the rule in September. And industry groups, sensing a major change to their business model, have geared up to persuade politicians that an expansion of the fiduciary rule “would be potentially devastating for the insurance industry,” according to one such group, the Federation of Americans for Consumer Choice.

Indeed, impact would be felt. Morningstar reported that investors in annuities could save more than $32 billion over the next ten years – with insurance agents enduring major restrictions in their commissions.

Could an extension of fiduciary responsibility become as significant a campaign topic as the debate over taxing tips? It’s hard to say. But I’ll be on the lookout to see whether or not the Trump or Harris campaigns decide there’s advantage to be had by backing fewer regulations – or retiree rights – when it comes to the role of fiduciary responsibility.

Interested in wealthtech? Check out our feature on the six key ways fintechs drive innovation in wealth management.And be sure to read our primer on wealthtech at FinovateFall next month, Client Centricity and the Rise of Alternative Assets.

This morning CrowdStrike CEO George Kurtz reported that 97% of the Windows sensors knocked out during CrowdStrike’s botched software update a little over a week ago are back online. That’s great news for those companies still reeling from one of the biggest IT outages in history.

When it comes to cybersecurity companies, CrowdStrike is widely considered to be a belle of the ball. Here’s wealth manager Josh Brown, a shareholder in the company since 2020, bringing the roses less than a year ago:

You can talk as much about cloud and mobile and social and machine learning and distributed computing and generative AI as you’d like, if you can’t secure your data and provide safe access to users, you have nothing. Literally ….

Spending on top-of-the-line security solutions has now been enshrined into securities law, in addition to all the other reasons to take this stuff seriously, such as not getting sued into the stone age by your customers or forced to make Bitcoin ransom payments to international cyber terrorists ….

As a business manager, you would cut IT spending on literally anything else first. A small handful of publicly traded companies have what I consider to be a massive runway ahead of them. CrowdStrike is aiming to become the Salesforce of the industry.

To recap: Friday morning, July 19, a bug in a CrowdStrike software update resulted in major IT outages that grounded flights and brought chaos to banks and other businesses around the world.

“CrowdStrike is actively working with customers impacted by a defect found in a single content update for Windows hosts,” CrowdStrike’s Kurtz wrote on the social media platform X the morning afterward. “Mac and Linux hosts are not impacted. This is not a security incident or cyberattack. The issue has been identified, isolated, and a fix has been deployed.”

As we learn more about exactly what happened, is there a particular insight here for banks, fintechs and financial services companies? At a time of heightened concern over third-party risk in our industry, the CrowdStrike outage is yet another reminder of the importance of not only choosing technology partners carefully, but also of ensuring resiliency in the event of an issue with a partner.

The latter is especially pertinent here. Many of the challenges and controversies with regard to third-party risk management in financial services involve the latter, vetting issue, primarily. A signature example is the case of Synapse, the fintech whose allegedly improper handling of customer funds led to more than 200,000 users losing access to their money and numerous disputes with banking partners. CrowdStrike is being accused of no such malfeasance and will, in all likelihood, remain a major player in the cybersecurity industry, with its reputation scratched perhaps but probably not scarred.

That leaves us with resiliency. In banking, the definition of resiliency has expanded significantly in recent years. From the failures of the banking crisis to the strains of the COVID-19 pandemic and accompanying economic slowdown a little over a decade later, banks have dealt with major challenges to both financial and operational resiliency.

The CrowdStrike outage represented a different type of disruption, and one that may be less amenable to the solutions that have ensured bank resiliency in the past (i.e., leadership, talent, and technology). Given many of the common complaints when technology disappoints, it’s worth wondering if we should look at ourselves, not just our institutions, for greater “resiliency.”