This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Every company is a fintech company. Or so saidPlaid CEO and Cofounder Zac Perret earlier this year. Today’s news that web browser Opera plans to acquire challenger bank Fjord Bank certainly affirms Perret’s statement.

Terms of the purchase, which is currently subject to regulatory approvals, were not disclosed.

So what will a web browser do with a bank? According to the press release, Opera will use Fjord Bank to “further accelerate its fintech operations in Europe by launching new, disruptive services aimed at improving consumers’ personal finances.”

“Looking at the fintech space in Europe,” said Opera EVP Krystian Kolondra, “we believe it needs more and bigger challengers who should provide people with smarter and empowering solutions for their personal finances.”

Opera, which counts 50 million active browser users, has already made inroads into the fintech space. Earlier this year the Norway-based company acquired banking-as-a-service provider PocoSys. As a result of the move, Opera built on Pocosys’ digital wallet and payment technology and is currently testing a new version of the Pocopay card and app.

“With the support of Opera, we are also excited to launch our first banking services in Lithuania this summer,” said Fjord Bank CEO Veiko Kandla.

Sometimes the story in a funding announcement isn’t necessarily the funding itself, but rather the investors. That’s the case with today’s news of supply chain finance provider Taulia’s $60 million funding round.

The strategic round, which brings Taulia’s total funding to $177 million, was led by China-based Ping An Global Voyager Fund. J.P. Morgan and Prosperity7 Ventures also participated, along with existing investors including Zouk Capital.

With today’s funding, The Wall Street Journal estimates Taulia’s valuation at $400 million.

The strategic relationship tied with this funding round signals international expansion for California-based Taulia, which already has a global customer base. “Ping An, J.P. Morgan and Prosperity7 Ventures bring a wealth of knowledge that we will leverage to further solve liquidity needs of businesses and contribute to economic growth,” said Taulia CEO Cedric Bru.

“Taulia is at the forefront of supply chain finance technology, with a global footprint that spans over two million SME suppliers and a suite of solutions that dramatically improves SMEs’ ability to manage cash,” said Managing Director and COO of the Ping An Global Voyager Fund, Donald Lacey. “We are excited to partner with Cedric and his team to build out their capabilities in China.”

The investment further deepens Taulia’s ties with JP Morgan. The two initiated a relationship earlier this year that aimed to help J.P. Morgan build a trade finance solution for its clients. “We’re committed to bringing the best solutions in the market to our customers and our strategic alliance with Taulia has been well received by clients,” said J.P. Morgan’s Global Head of Trade, Stuart Roberts. “The investment component is another step in our relationship as we look to better serve clients and their supply chains within our Global Trade franchise.”

Founded in 2009, Taulia helps businesses improve their supply chains by providing financing options with flexible payment terms. Their tools help businesses accelerate payments and free up working capital. A network of two million businesses use Taulia’s technology. The company processes over $500 billion every year. Taulia’s clients include Airbus, AstraZeneca, Nissan and Vodafone.

Advanced biometric technologies like facial recognition have their critics. The city of Boston, Massachusetts, just a few weeks ago, became the second community in the world to ban the use of facial recognition technology over concerns of bias against ethnic minorities. And the use of facial recognition in places like China has heightened concerns over the potential privacy-violating aspects of the technology.

Nevertheless, the fact that companies continue to innovate in the biometric authentication space suggests that these issues are more likely to be seen as contemporary challenges rather than permanent obstacles. This is all the more so in a world that is coming more – rather than less – connected, and digital.

Trulioo, a leading global identity verification provider, is one the companies that is helping small businesses take advantage of these technologies. The company announced today that its low-code developer tool, EmbedID, will now feature both facial recognition and document verification functionality. This will enable SMEs to verify new users during the account opening process more efficiently and accurately, and assure that KYC and AML requirements are met.

“Taking a multi-layered approach to identity verification offers businesses the strongest defense against increasingly sophisticated bad actors,” Director of Growth at Trulioo Rutherford Wilson explained. “Adding document verification gives another layer of protection to help reduce risk, especially when combined with reliable identity verification.” Wilson credited the combination of these features for providing businesses with the “increased confidence in knowing the user is tied to a real identity and that they are who they claim to be online.”

Small businesses can use the technology by copying a snippet of code and pasting it on their website. This will automatically generate a stylized registration form that is prewired to Trulioo’s GlobalGateway to provide instant verification of personal identification information. Via the connection to GlobalGateway, small businesses can verify the authenticity of government-issued ID documents and leverage facial recognition technology – equipped with liveness detection – to establish that the individual opening the account is the same person in the photo on the ID document.

“In an age of ongoing digital transformation, it’s essential for SMBs to be able to access the same identity verification solutions used by large organizations to protect their business and scale their company,” Wilson added. He cited cost as the main barrier for most small businesses when it comes to accessing “bank-grade” technology and security. This leaves them more vulnerable to fraudsters than their larger rivals, and makes it more difficult for them to compete.

“We designed EmbedID to help level the playing field to allow for accelerated innovation, customer acquisition, and competition in the marketplace,” Wilson said.

Founded in 2011 and headquartered in Vancouver, British Columbia, Canada, Trulioo has been a Finovate alum since 2014 and most recently demonstrated its technology at our European conference in February. Named to CNBC’s 2020 Disruptor 50 roster in June, Trulioo was featured in our look at Canadian fintech innovators on Canada Day earlier this month.

Two of the biggest stories of 2020 so far – the global public health crisis of COVID-19 and the worldwide resurgence in social justice activism – have had as much impact on the fintech industry as they have the rest of the world.

The mobilization of banks and fintechs to facilitate financing for small businesses, for example, or to offer discounts on their services for essential workers in other industries has been impressive.

And it has been heartening to see companies in the financial technology and services space join with corporations and entrepreneurs in other industries to express their commitment to fighting ethnic discrimination and actively encouraging diversity.

But behind the bright lights of these two, year-defining stories, there have been some pretty impressive fintech-specific headlines that are worth remembering as we dive into the second half of the year. With that in mind, here is our take on the biggest fintech stories from the first half of 2020.

The collapse of Wirecard early this summer was the first major negative headline for the fintech industry this year. What began as an inquiry into a missing $2.1 billion in cash has turned into a major scandal involving the arrest of former Wirecard CEO Markus Braun and talks that the company could become an attractive acquisition target thanks to its relationships with the major card companies.

With Visa’sacquisition of Plaid at the beginning of the year and Mastercard’spurchase of Finicity near 2020’s midway mark, card companies are putting their money where they believe the future of fintech lies: open banking and the leveraging of consumer-permissioned data.

If you had nCino on your bingo card of fintechs most likely to be among the first to go public this year, then you are a luckier soul than most. The news that the Wilmington, North Carolina, Bank Operating System provider is planning an IPO for later this year was a sign that some fintechs still see the public markets as an optimal way to raise capital.

The boost in e-commerce brought on by the COVID-19 pandemic was a major boon for digital payments company Stripe, which raised $600 million this spring, earning a valuation of $36 billion.

Starting as a student loan refinancing company and since expanding its portfolio to include loans, investment products, and debit cards, SoFi made yet another expansion to its product suite with its $1.2 billion acquisition of payments company Galileo.

From the outside, $7.1 billion might be a lot to pay for the ability to help younger consumers better understand and manage their credit. But Intuit’s decision to acquire Credit Karma in the first few months of 2020 may have been an early sign of the sort of consolidation that could await the fintech industry on the other side of COVID-19.

A $500 million Series D round has sent the valuation of U.K.-based fintech Revolutsoaring to more than $5.5 billion. Led by Silicon Valley-based VC firm, TCV, the February investment set an optimistic tone for Q1 VC fintech funding before the reality check of the coronavirus set in.

In acquiring Radius Bank for $185 million early this year, P2P lending pioneer LendingClub became the first U.S. fintech to acquire a licensed bank. Boston, Massachusetts-based Radius Bank is an online bank with $1.4 billion in assets.

By mid-year, the rise of the retail trader a la Robinhood and Dave “Stoolpresidente” Portnoy may have become a bit of a cliche. But that only makes Morgan Stanley’s $13 billion acquisition of ETrade – announced back in February – that much more of a prescient move to diversify its online and self-directed customer base beyond the ultra-rich.

Cryptocurrency exchange platform Binance made a major purchase today, acquiring digital wallet and crypto debit card company Swipe. The deal closed for an undisclosed amount.

The aim of the acquisition is to help push the use of cryptocurrencies into the mainstream by encouraging payments with cryptocurrencies through traditional financial systems such as debit cards.

U.K.-based Swipe provides a cryptocurrency banking account that offers a multi-currency mobile wallet, the ability to buy and sell cryptocurrencies, access to exchanges with instant settlements, and a Visa debit card.

Users can pay with their Visa debit card at all 50 million locations across the globe where traditional Visa debit cards are accepted. The card also offers up to 4% cash back (paid in Bitcoin), doesn’t charge foreign transaction fees, has built-in security features, and more. The debit card is crypto-to-fiat, meaning the user makes a purchase using cryptocurrency while the merchant receives fiat currency in exchange.

“By giving users the ability to convert and spend crypto directly, and have merchants still seamlessly accept fiat, this will make the crypto experience much better for everyone,” said Binance CEO Changpeng Zhao. “Swipe’s exceptional team has made great strides in furthering this mission and has been instrumental in the industry for bridging the gap between commerce and crypto. The Swipe Wallet alone is unique which acts as a digital bank account for its users, providing access to traditional banking services. We are thrilled to work with a team that shares the same core values and looking forward to our larger efforts ahead.”

Swipe CEO Joselito Lizarondo said that the deal “will place Swipe in the position to make cryptocurrencies more accessible for millions of users worldwide.” He added, “We are excited to work with Binance to continue innovating in this crypto-banking space to further build towards mass adoption on our current and future product lines.”

This is the seventh acquisition Malta-based Binance has made since it was founded in 2017. The company has also purchased CoinMarketCap, BxB, DappReview, and WazirX.

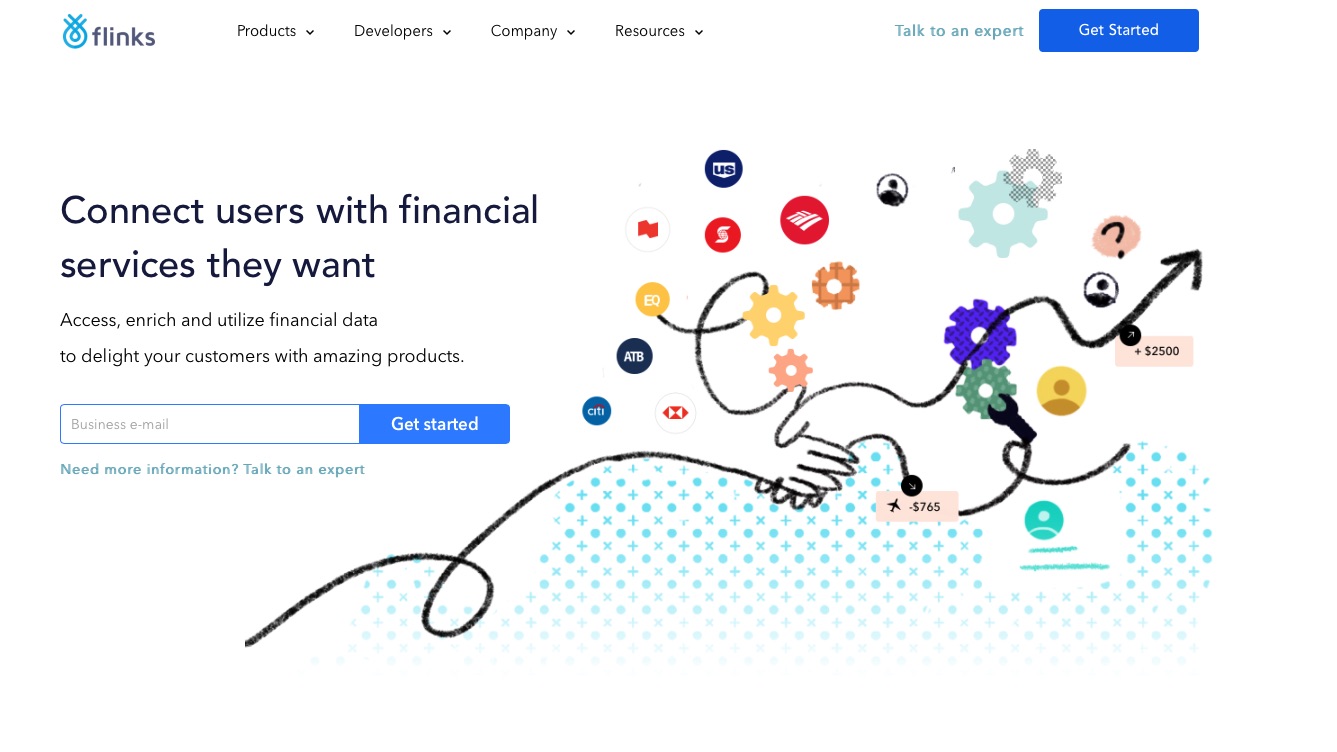

Flinks, a startup based in Montreal, Quebec, Canada, that specializes in data aggregation for financial services, has secured $11 million in Series A funding. The investment was led by NAventures, the VC arm of National Bank of Canada, which also provided $5.2 million in debt financing. Also participating in the round were Intact Ventures, Luge Capital, and Panache Ventures.

Flinks CEO Yves-Gabriel Leboeuf called the investment “timely” adding that the company was “well on track” to meet the goals it has previously set and was now ready to “face new, bigger challenges.” In a Q&A announcement at the company blog, Lebouef explained that, having focused on retail banking up to this moment, the company will look to expand into what he referred to as “wealth data.”

“Flinks will enable connections to data sources in the wealth management space, through a new aggregation service,” Lebouef said. “This is something we’re going to pull off in the near future – in fact, we’re already well into the beta phase.”

Founded in 2016, Flinks helps businesses provide users with the financial services they want. The company’s technology enables companies to connect their customer’s bank accounts, and to leverage data insights to build better, more personalized financial products. Lebouef noted that “roughly 1 in 3 Canadians” have connected their bank accounts with his company, which has processed 300+ million connections.

The investment will help Flinks expand to new markets and take advantage of the opportunities of open banking. Managing Director, Venture Capital, NAventures Philippe Daoust said, “We see great alignment between Flinks’ mission and our own focus on helping our clients manage their finances by providing them with innovative and reliable digital solutions.”

Flinks, which signed its first client in the spring of 2017 and its 100th client a year later, began 2020 by adding Clayton Feick as its new Chief Revenue Officer. Feick is a veteran of Quandl and Thomson Reuters, where he was vice president and global head of sales and business development and global lead, respectively.

Blockchain analysis company Chainalysis is on a mission to promote trust and transparency for cryptocurrencies. Aiding that undertaking today is an additional $13 million in funding to add to its Series B round.

The new investment comes from Ribbit Capital and Sound Ventures and brings Chainalysis’ Series B round to $49 million. The New York-based company’s total funding now stands at almost $67 million.

Chainalysis was founded in 2014 and was recently valued at $266 million, according to Pitchbook. Among its offerings are automated cryptocurrency transaction monitoring software, investigation software for tracing the flow of funds across blockchains, and profiles of cryptocurrency businesses.

As a part of the deal, Chainalysis has gained former Treasury Department official and current Ribbit Capital General Partner Sigal Mandelker as an advisor.

Mandelker and the new funds both play a key role as Chainalysis invests more into the government side of its business. While Chainalysis offers solutions for private sector businesses and financial institutions, the company also works with a handful of U.S. government agencies, including the IRS, the DEA, ICE, and the SEC.

In an interview with blockchain publication The Block, Chainalysis CEO and Co-founder Michael Gronager said, “We extended our Series B in order to meet demand for our services, primarily from government customers. Government agencies understand that visibility into cryptocurrency is important to national security and that crypto crime does not let up during a pandemic. Importantly, this also has long-term benefits to the cryptocurrency industry.”

As transactions move to the digital realm and more countries begin considering CBDCs, Chainalysis is making a smart move in pouring more resources into its government-focused services. Mandelker said she is “excited to work with the Chainalysis team to help develop public-private partnerships, enhance ground-breaking technologies in financial services, and root out illicit networks.”

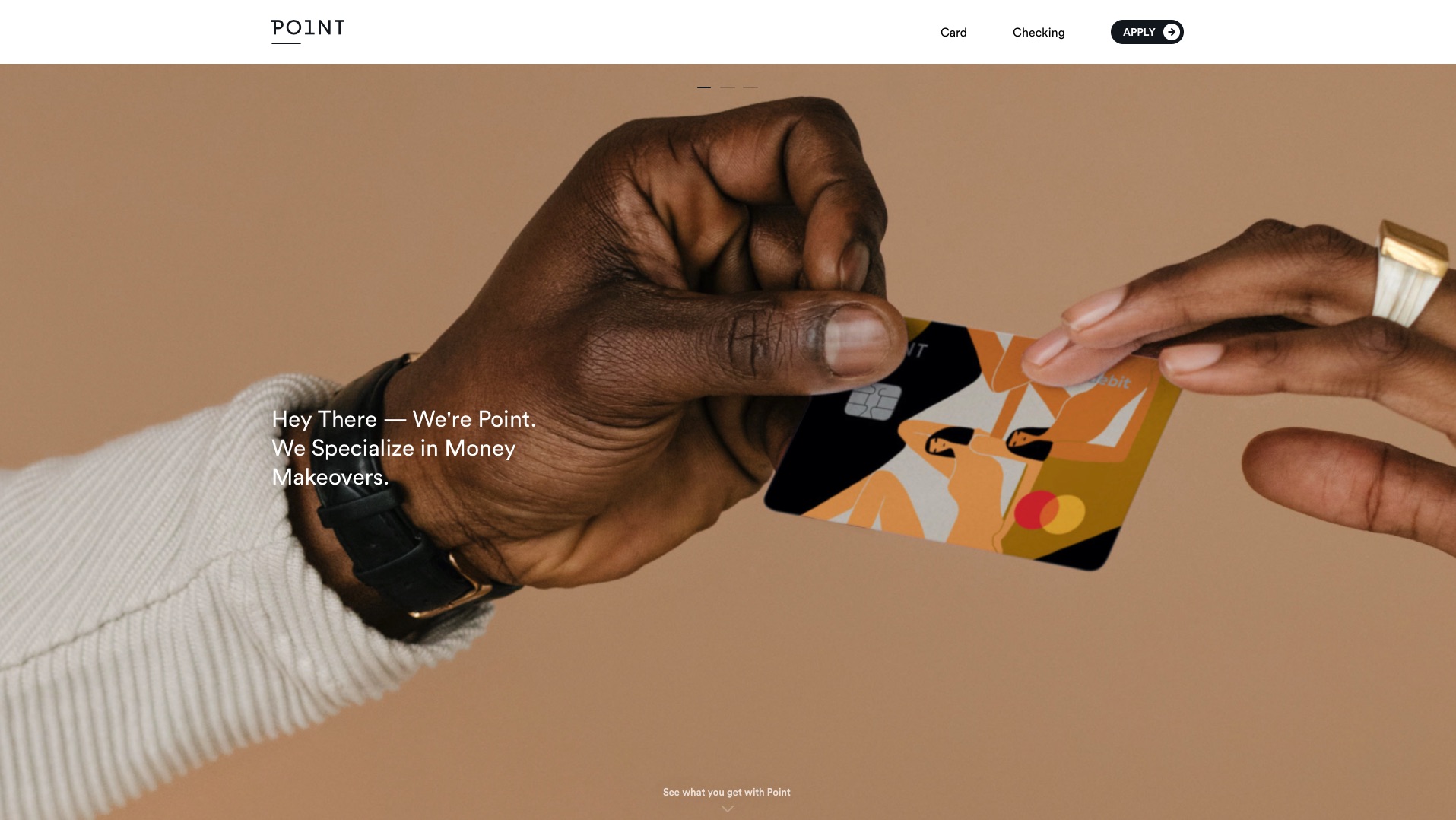

U.S. challenger bank Point, which offers a consumer banking app and pledges to provide a “credit card experience” to debit cardholders, announced that it has raised $10.5 million in Series A funding. The round was led by Valar Ventures, and featured participation from Y Combinator, Kindred Ventures, Finventure Studio and “business angels.” Company CEO and co-founder Patrick Mrozowski said the challenger bank has raised a total of $12.7 million.

The San Francisco, California-based company has been in private beta “for the past year” plans to launch a major new version of its technology later this year, according to reporting in TechCrunch. In addition to its Point Card debit product – available as both a physical and virtual card – the company offers a Point Checking mobile savings account. The account is backed by FDIC-insured, Point partner Radius Bank, and the challenger bank leverages technology from Finovate alum Plaid in order to link accounts on its platform to a third-party bank account. Point does not charge foreign transaction fees for international transactions, and relies on Mastercard’s exchange rate for overseas transactions.

Users of the Point Card earn points when shopping with popular merchants including Airbnb, Uber, and Starbucks where cardholders can pick up 2x, 3x, and 4x in points respectively for each dollar they spend. Seamless integration between the Card and the app ensure a holistic consumer experience with features including purchase notifications, in-app card management, and rewards tracking.

Previous to his co-founding of Point, Mrozowski founded and ran Crumbs, a micro-investing platform for cryptocurrencies and digital assets that was acquired by Metal Pay two years ago.

If you missed the news earlier this week, here’s a recap: Personal Capital agreed to be acquired by Empower Retirement, the second-largest retirement services provider in the United States, for up to $1 billion, composed of $825 million on closing and up to $175 million for planned growth.

According to Forbes, the San Francisco-based fintech is selling for the same price as its valuation in February 2019. The deal is expected to close in the second half of this year.

After a bit of time to digest everything, Personal Capital CEO Jay Shah looked at the decision and what it means for the eleven-year-old company. Shah has been at Personal Capital since the company’s launch in 2009 and will now serve as President of Personal Capital and will also sit on the Executive Team at Empower.

Shah explained that, though many companies have expressed interest over the years in acquiring Personal Capital, none of the opportunities felt right. However, because Empower shares many of Personal Capital’s same “visions and values.”

He went on to describe how, in today’s uncertain world, the buy-out “will ensure extra strength and resources to grow Personal Capital, and bring [clients] more of the great technology and service [they’ve] come to expect. He added that combining the two companies will help Personal Capital support and further develop its features and service offerings.

As for what’s next, Shah said that Personal Capital will continue to operate as it always has. And because the company’s leadership team has committed to stay on for the long-term, the company’s culture will stay in-tact. “I recognize that this announcement feels like a major change, but I also want to assure you that your day-to-day experience with Personal Capital will remain the same,” he added.

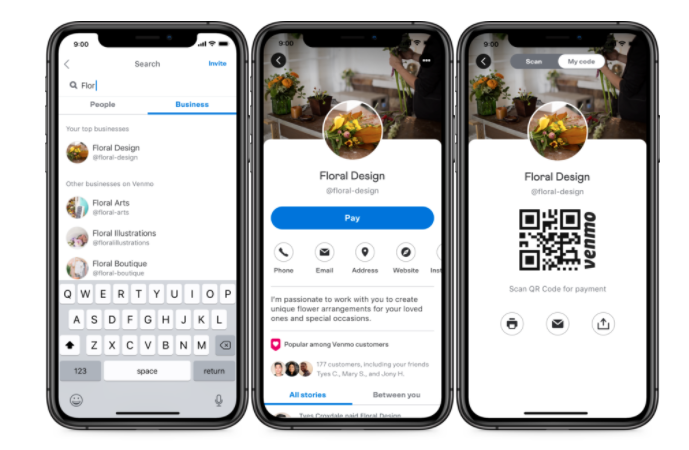

Micro-businesses, such as sole proprietors and gig workers, are an underserved group when it comes to financial management tools.

Seeing this need, and recognizing that more than 75% of small businesses in the U.S. are sole proprietors, Braintree-owned Venmo is releasing a new set of tools to help them connect, market, and grow their business.

“Venmo was designed to be a place where friends and family can send, split and share purchases and experiences. Today, we are introducing a very limited pilot to extend that experience to allow sellers to access the benefits of Venmo’s platform through Business Profiles,” the company announced in a blog post.

Currently in a pilot phase, Business Profiles allow consumers to create a business profile (separate from their personal profile) on Venmo in order to accept payment for goods and services. Business users can also tap into Venmo’s community of 52+ million users to generate interest, referrals, and awareness of their brand.

At launch, Venmo will not charge businesses transaction fees. This is likely because the company recognizes that the micro-businesses it is targeting already use its P2P money transfer service to accept payments for their business. Venmo cautioned that it will eventually charge a per-transaction fee of 1.9% + $0.10, but did not mention when it will begin charging the fees.

Venmo’s Business Profiles launch today to a limited number of iOS users on an invite-only basis and will be available for Android users “in the coming weeks. The company plans to make the new service more widely available “in the coming months.”

Business banking services provider Zeller launched earlier this year to offer businesses in Australia a new way to bank. Heading up the new company is ex-Square duo Ben Pfisterer and Dominic Yap, which just revealed a round of funding Zeller landed earlier this year.

The investment, which closed before the emergence of the coronavirus, totaled $4.4 million (AU$6.3 million). The seed round was led by Square Peg and saw contributions from Apex Capital Partners.

Taking aim at the lack of alternative business banking services in Australia, Zeller seeks to compete with traditional banks by better serving the small business banking market.

“First and foremost [businesses] need to get paid, then they need somewhere to put that money and then need a way to deploy it, to pay their bills and staff and invest further,” Pfisterer told Business Insider Australia. “What we wanted to do was create a solution that did all three for them on one system.”

Specifically, Zeller is targeting the historically underserved category of mid-market businesses, a group Pfisterer estimates at 1.5 million. While the company hasn’t yet launched its services, once it does it will offer payment acceptance technology, business financial management tools, an instant deposit account, and a fee-free debit card.

“You see neobanks popping up everywhere, but they’re all consumer-focused. There’s no sort of neobank focused on all these other business needs. It’s quite complicated but we think we have something completely unique.” said Pfisterer of the Australian market.

Worldwide, there have been a flood of new consumer-focused challenger banks in the past year. However, we’ve seen rising competition in challenger banks working in the businesses banking arena. Among the new entrants are Arival Bank, which was founded in 2018 and recently unveiled its business bank account. Digital payments company Square also announced plans to launch a small business bank next year.

There are two words that help summarize 2020: unpredictability and volatility. It turns out that both of these attributes are bad for a lot of things and that’s especially true for underwriting consumer loans.

Recognizing this issue, U.K.-based credit assessment services company AirelaunchedPulse, a product to help lenders calculate risk in the post-COVID borrowing landscape.

“Lenders have always played catch up when understanding how existing customers perform on commitments elsewhere, and this challenge is exacerbated by the major CRAs’ Emergency Payment Freeze,” said Aire CEO and Founder Aneesh Varma. “In a rapidly changing economic situation, lenders need new tools that can understand the context of the consumer to help them detect emerging risks. Pulse is a quick, convenient and FCA-regulated way for lenders to spot financial change as it happens, providing lenders with a truly holistic view, gathered from the most up-to-date data source available to them: the consumer themselves.”

At its core, Pulse is a scalable communications tool. It enables lenders to collect current information from customers about their changing financial circumstances while maintaining fair and FCA-compliant account handling. The tool enables lenders to reach out to their existing borrowers via SMS and email to conduct an Interactive Virtual Interview (IVI) to gather information regarding disposable income levels and risk of financial difficulty.

It takes consumers an average of three-to-five minutes to complete the IVI, which asks for information such as employment status, current working hours, income level, household bills and expenses, and levels of savings. In order to ensure the information is correct, Aire cross-checks it against its own database of consumer information. After the assessment, Aire sends the lender insight into the consumer’s financial difficulty, affordability, and engagement.

Because of its proactive approach, Pulse offers lenders information about a consumer’s changing financial situation much faster than the traditional method of waiting for historical information from CRAs who identify changes in customer circumstances.

The underwriting and credit scoring space has always been an area of disruption for fintechs. Given that the new reality across the globe has multiple impacts on the economy and unemployment, we can expect to see more existing companies adapt their services to not only help underwriters understand and assess risk but also help consumers access cashflow when they really need it.

Aire was founded in 2014 and has since raised $24 million. Aneesh Varma is CEO.