I’ve mostly just observed the Twitter phenomenon, following a few people and seeing how banks and credit unions are using it (see my previous post for financial institutions on Twitter). However, I’d not fully embraced Twitter either as a publishing device or research source. The 300 or so RSS feeds, emails and news items that cross my desk each day seemed like plenty of intelligence to sift through.

I’ve mostly just observed the Twitter phenomenon, following a few people and seeing how banks and credit unions are using it (see my previous post for financial institutions on Twitter). However, I’d not fully embraced Twitter either as a publishing device or research source. The 300 or so RSS feeds, emails and news items that cross my desk each day seemed like plenty of intelligence to sift through.

But now, I’m reconsidering my priorities after learning about an interesting new alt-payment company BillMyParents from Twitter activity (see notes 1, 2).

How it works: BillMyParents is a new service from IdeaEdge’s Socialwise (press release). The service is primarily designed for kids to shop online. They select what they want, then at checkout, redirect the bill to their parents via an email alert to PC or mobile phone. Parents login and complete the payment process at their convenience using MasterCard, Visa, Discover Card (no American Express; see third screenshot below). Card info can be stored for one-click future approvals.

The company charges a $0.50 transaction fee for each purchase. But like PayPal, the real money will be made when the company pushes purchase transactions through the ACH system.

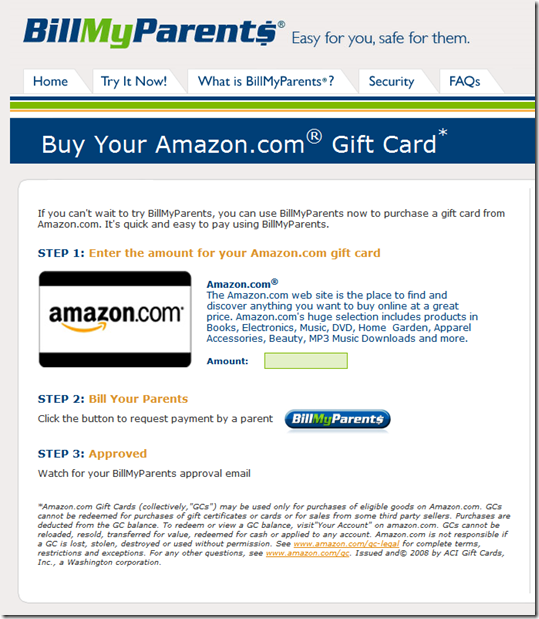

Currently, BillMyParents is selling prepaid gift cards from its site as a proof-of-concept. I tested it yesterday and everything seemed to work as described (see second screenshot below).

The opportunity: The service reminds me of the unmet need that PayPal filled nine years ago. Purchasing at eBay was a major hassle due to the lack of online payment capabilities. Kids have similar problems when trying to buy things online.

The service could also be adapted to other situations where one party does the shopping but wants someone else to authorize payment such as small businesses, nannies, or even spouses. It could also be used for extra security when the shopping is done in a non-secure environment such as public terminal and payment is redirected to a more secure device, such as your mobile phone.

Like any alternative payment, BillMyParents requires the merchant to add the option to its ecommerce platform and consumers to set up accounts. Both of those are time-consuming and face the chicken-and-egg dilemma, i.e., it’s hard to attract merchants without a substantial user base while its difficult to add users without merchants.

Bottom line: This is a winning idea. The massive discretionary purchasing power of teens and pre-teens is a tempting target in this difficult retail environment. And financial institutions, or their payment partners (e.g. Visa, MasterCard), looking to differentiate themselves with the youth market, could jumpstart the program. Or more likely, PayPal and/or Amazon will dive in, either acquiring BillMyParents outright, or building their own version(s).

BillMyParents homepage after setting up an account (26 March 2009)

Note: Split login screen for kids (left) and parents (right)

Proof-of-concept: Gift card purchase (26 March 2009)

Parent’s approval screen (26 March 2009)

Notes:

1. Thanks to Frederic Baud (@fredericbaud) who was the first in my network to Tweet about BillMyParents; and to Glenbrook’s Scott Loftesness (@sjl) who’s retweet is actually what caught my eye.

2. BillMyParents appears to have grabbed its Twitter page name (@billmyparents), but it’s not yet active.

John Cook, a Seattle tech blogger at TechFlash, was apparently the first customer to use the new Starbucks Mobile Card iPhone app to purchase coffee at the Seattle Columbia Center Starbucks. The video was posted at 3 PM yesterday. For more info on the app, see yesterday’s post.

John Cook, a Seattle tech blogger at TechFlash, was apparently the first customer to use the new Starbucks Mobile Card iPhone app to purchase coffee at the Seattle Columbia Center Starbucks. The video was posted at 3 PM yesterday. For more info on the app, see yesterday’s post.