![]() Editor’s note: We are starting a new series showcasing very early-stage

Editor’s note: We are starting a new series showcasing very early-stage

startups of interest to banks and other financial institutions considering

Strategic Seed Investing. We have no financial relationship

with the companies mentioned, but we hope to see them at Finovate soon.

—————

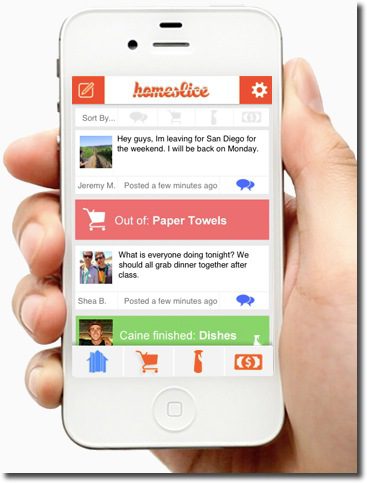

HomeSlice is targeting the 15 million college students currently sharing their lives with one or more roommates. The San Luis Obispo, California, company has created a “micro social network” for a single household where roommates can track chores, supplies, bills due, and payments made. HomeSlice’s “whiteboard function” captures all activity in a social network-like news feed (see inset).

HomeSlice is targeting the 15 million college students currently sharing their lives with one or more roommates. The San Luis Obispo, California, company has created a “micro social network” for a single household where roommates can track chores, supplies, bills due, and payments made. HomeSlice’s “whiteboard function” captures all activity in a social network-like news feed (see inset).

In March, the company reported 6,000 active users across 2,000 households. In total, they’ve tracked 26,000 bills and 80,000 household supply items. The app is currently has no transactional integration so you can’t actually buy items or pay bills, but presumably that is on the way. The startup was recently visiting PayPal’s Venmo unit, a logical partner.

Fundraising: According to its Angel List profile, the company is currently raising a small round. The first investor is MatchFire (23 April 2015 press release), a data supplier to the app.

Why it’s a good strategic bet for financial institutions: Students and young adults are an attractive, albeit difficult, segment to win over. Yet, they are the future, and could be customers for 70+ years. So helping them with early money-management problems could pay huge dividends over time, assuming you are able to upsell profitable financial products. Furthermore, if a “parent view” could be added to the functionality, the app could be appealing to the income-producing part of the family.

Why it’s a good strategic bet for financial institutions: Students and young adults are an attractive, albeit difficult, segment to win over. Yet, they are the future, and could be customers for 70+ years. So helping them with early money-management problems could pay huge dividends over time, assuming you are able to upsell profitable financial products. Furthermore, if a “parent view” could be added to the functionality, the app could be appealing to the income-producing part of the family.

And why it might not work: Young adults, students especially, are generally not big spenders for financial management and/or productivity apps. Nor are they interested, so it won’t be an easy sell.

Finally, remember this is a seed stage opportunity. The HomeSlice app is an MVP (minimal viable product) relying on manual data entry with no financial integration. There is a ways to go before you are sharing with your customers (or board).

")