Last week, I attended the BAI Retail Delivery conference in Boston (for more background on the event, see note 1). I enjoyed the show tremendously.

Last week, I attended the BAI Retail Delivery conference in Boston (for more background on the event, see note 1). I enjoyed the show tremendously.

What’s not to like? Famous speakers, new products, several thousand attendees, statistics galore, and a floor filled with new bank tech. For me, the only disappointments were the non-industry keynoters, who are not why I attend, but are something to tell your friends and family about when you get home (note 2).

Like last year, I’ll cut to the chase and hand out my personal awards for the event. I saw only a tiny fraction of the companies, so the list below shows merely my favorites culled from about two dozen company interviews.

The Netbanker awards

- Biggest buzz: Person-to-person payments (we’ll cover it in Online Banking Report soon)

Runner up: Mobile banking and payments - Most likely to make the cover of FastCompany: Cardlytics (will cover next week)

- New solution most likely to be used by 1000 financial institutions: Continuity Engine’s semi-automated, compliance task-management service

Least likely: Microsoft Surface, as cool as it looks, I just don’t see banks deploying it in large numbers - Most audacious business plan: Moneta, winner of this very award last year, but did indeed appear in Boston with a major client win, SunTrust (see Celent’s Jacob Jegher’s not-at-all enthusiastic post on the announcement)

- Best ah-ha moment: When Joe Salesky, Clairmail founder, observed that mobile banking is a 100% solution, meaning it’s for every customer NOT just the half that do online banking

- Biggest surprise: The buzz around person-to-person payments and relative lack of buzz around online PFM

- Most-talked-about vendor without a booth: PayPal which announced partnerships with three large bank tech companies: S1, FIS, and First Data’s STAR unit

- Coolest online feature, not yet available: Credit card available-balance meter displayed directly on the user’s PC desktop, powered by Worklight

- Coolest new GUI feature: Fiserv’s ebill snapshots

- Best demo (I’d not seen before): Dynamic Card Solution’s instant issue of a credit card with my picture on it along with a background image I chose from hundreds available

- Best-attended breakout session (that I attended): Checking 2.0 which analyzed what the product might look like if NSF/OD fee revenues are materially limited

- Best number: From the opening remarks by BAI director, Debbie Bianucci: According to BAI research five years ago, one-third of consumers preferred to deal with their bank remotely; now, two-thirds do

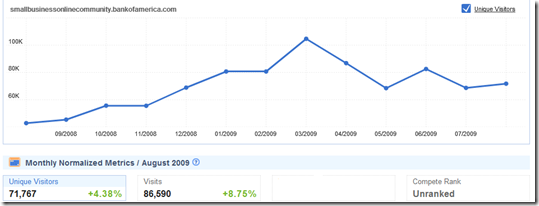

Runner up: Bank of America’s Doug Brown revealed in his presentation that BofA has 3.5 million active mobile banking users (see recent monthly growth below)

- Scariest number: A prediction from Sherief Meleis (Novantas) that new regulation could wipe out 20% to 40% of total checking account revenue

- Missing in action: Security solutions

- Coolest new event technology: Real-time text voting in the Checking 2.0 session

Runner up: Wifi available conference-wide for the first time ever - Most intriguing co-brand opportunity: Getting the bank logo on PayPal messaging (FIS, S1) to payment recipients or during payment sessions (FirstData STAR)

- Product I most wanted to use now: Digital Insight’s (Intuit) FinanceWorks with Turbotax integration

- Best screenshot: Lamping on the iPhone (powered by ClairMail); I call it the “little red number” superimposed over iPhone icons, that tells you how many messages are available (see inset)

Runner up: Worklight’s visualization of its widget running in four environments with essentially the same GUI (see below) - Best party: Geezeo’s blowout at Lucky’s

- Best freebie on the floor: Fresh lemonade from the wonderful people with a booth by the front entrance

- Netbanker spotting: Quote in BofA’s Doug Brown’s Powerpoint regarding BofA threepeat (in the mobile marketplaces)

And I’m always collecting usage stats and other numerical detritus delivered during the presentations. Here are my notes with (source in parenthesis):

- 27% of U.S. households are now mobile only (Doug Brown, BofA)

- New mobile customers at BofA last 3 months: 150,000 (Sep); 210,000 (Aug); 220,000 (July) (Doug Brown, BofA)

- In U.S. and worldwide, text message volume has surpassed voice call volume (Doug Brown, BofA)

- 99% of mobile users view balances, 90% view transaction detail, about $10 billion of funds have been moved via mobile transfers/bill pay; 15 million location-based searches being performed (annual run rate)

- BofA has 35% of all mobile banking users (Doug Brown, citing ComScore numbers in 2009)

- BofA has added 150,000 new checking accounts due to mobile offering

- BofA seeing voice calls decline among mobile users, but online banking usage holding steady

- In pilot, 94% of the users of TurboTax within FinanceWorks chose their host banks to deposit tax refunds (Digital Insight/Intuit)

- More than 50% of iPhone users have used mobile banking in past 30 days (Javelin Strategy)

- 33% of mobile banking users monitor accounts daily, 80% wee

kly (Javelin) - Customer willingness to pay fees for (Novantas):

— Teller transactions 8%

— Bill pay 12%

— Mobile banking 12%

— Paper statement 19%

— ID protection 27% - At ANZ, 65% of its Yodlee-powered PFM (launched Oct 2008) users visit daily; 89% visit weekly (Doug Brown, ANZ; not a typo, there really were two Doug Browns)

- 81% of its PFM users rated the service at least 7 points on 10-point scale (31% rated 9 or 10; 50% rated 7 or 8)

- ANZ’s PFM is a standalone free service that can be used by anyone; so far, 20% are non-ANZ customers; the business case for the service was built on customer acquisition, but they also may charge certain users for certain functions

- Yodlee-powered PFM users spend twice as much time online at the bank than regular users, and only 1.5% leave the bank each year compared to 7% of regular online banking customers

- Worklight case study results:

— 8% to 15% of online customers install widgets within the first year

— 95% of widget users are active

— Customers conducted 15 to 30 sessions/month via widgets

Worklight widgets running on a variety of platforms (4 Nov 2009)

Notes:

1. About BAI Retail Delivery Conference 2009

BAI Retail Delivery is an annual rite of passage for bank tech strategies, delivery system analysts, and product managers. At the peak, in 1999/2000, there were as many as 10,000 people there (attendees + exhibitors) and close to 500 exhibitors stretching perhaps three or four city blocks in each direction through cavernous exhibit halls. It was a little like Times Square but without the highrises. Some exhibitors had massive 10,000 square foot booths filled with hardware. And the show-floor routinely sold out.

Financial institutions brought teams of people to pour over the new machines and software solutions, be inspired at the general sessions where Bill Gates, Roll Perot, Scott Cook, and other tech-industry luminaries showed up to win over the bankers.

Fast-forward a decade. It’s still an awesome event which I highly recommend. I thoroughly enjoyed every conversation I had and most every session I attended. But the event has downsized considerably. This year, you could walk across the exhibit hall in a few minutes. And if you wanted to, you could have spent five minutes with all 180 companies during the show hours. That would have been impossible last year with around 300 exhibitors. But all-in-all, I’d say there was more energy on the floor this year because the attendee per square foot ratio seemed much better.

2. Unfortunately, on Thursday both Al Gore (planned) and Jack Welch (unplanned back problems) phoned in their keynote addresses via sat-link.

![image_thumb[12]](http://www.netbanker.com/WindowsLiveWriter/RIMsNewBlackberryAppWorldIncludesWellsFa_1042C/image_thumb%5B12%5D_2.png)

![image_thumb[2]](http://www.netbanker.com/WindowsLiveWriter/RIMsNewBlackberryAppWorldIncludesWellsFa_1042C/image_thumb%5B2%5D_2.png)