This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

“We are clearly aligned in our mission to improve global banking and transaction settlement services that unlock the borderless banking and global economic opportunities for all,” Managing Director for Buckzy in EMEA Adrian Brown said. “Combining Buckzy’s network with M2P’s API platform delivers an outstanding customer experience and competitive advantage for customers.”

Buckzy’s network enables real-time, cross border payments around the world. The company’s technology gives both businesses and financial institutions the ability to expand their offerings via white-label solutions on a secure platform. Moreover, Buckzy’s ecosystem also empowers these organizations to make collections and receive payments in local currency. Headquartered in Toronto, Ontario, Canada and founded in 2018, Buckzy demonstrated its solution one year later at FinovateFall. At the conference, Buckzy Global CMO Lindsay Mulligan showed how the company’s technology powered instant, on-the-go digital wallet transfers and top ups, as well as multi-currency transfers and instant email money transfers with just a few clicks and without transaction fees.

Business Head of M2P Solutions for MENA, Vaanathi Mohanakrishnan, underscored the importance to the company of opening up these regional opportunities. “A lot of M2P’s strategy hinges on enabling fintechs to deliver solutions leveraging our infrastructure and partner network,” Mohanakrishnan explained. “We are excited to be partnering with Buckzy to deliver frictionless cross border payment experiences to customers in the MENA region.”

Delivering real-time cross-border payments to 47 countries, Buckzy Payments was recently named to the CIX Top 20 Early roster of innovative Canadian technology companies. With offices in the U.S. and India, as well as Toronto, the company has raised $3 million in funding from investors including Dash40 Ventures, Mistral Venture Partners, and Revel Partners.

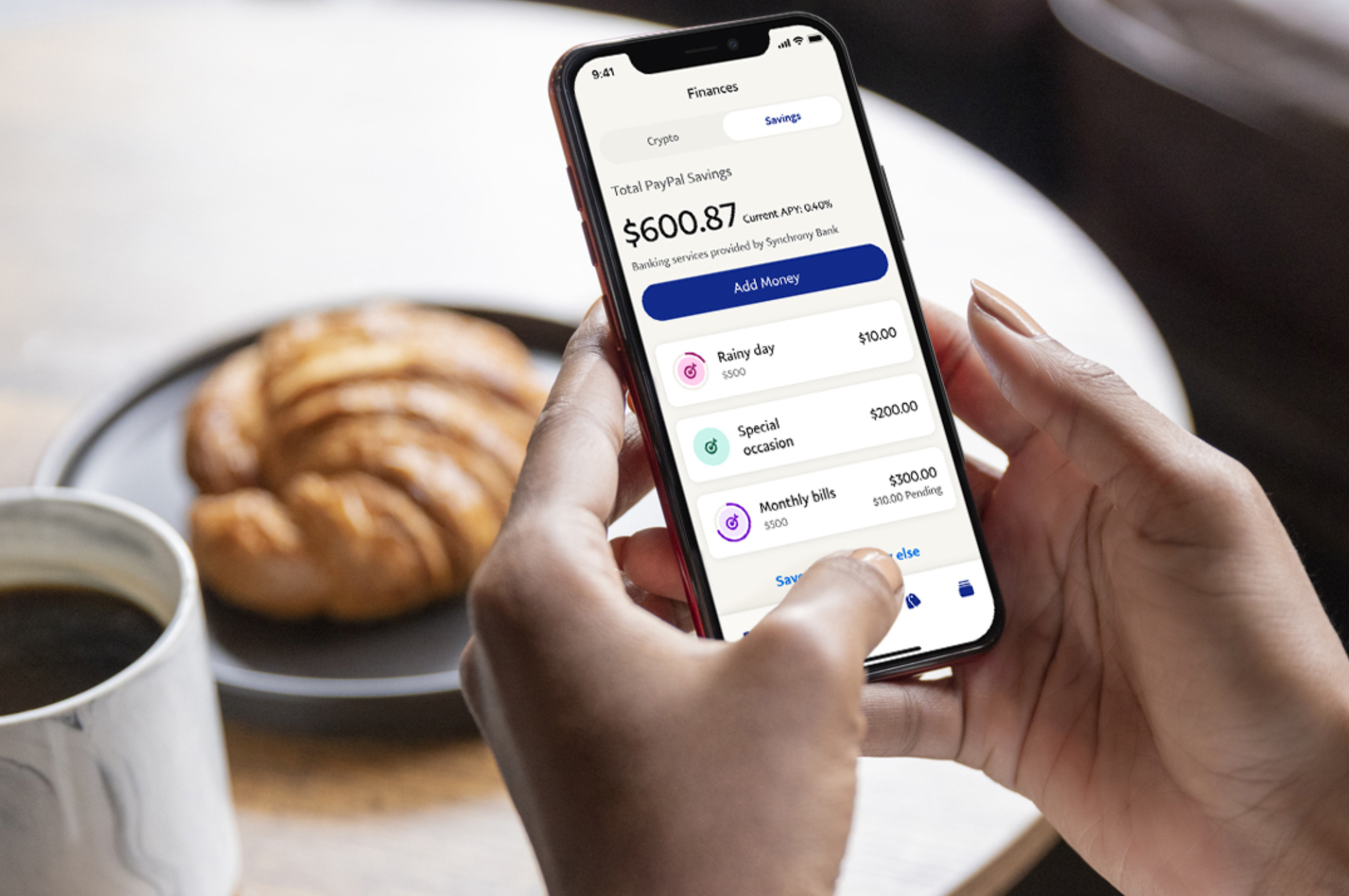

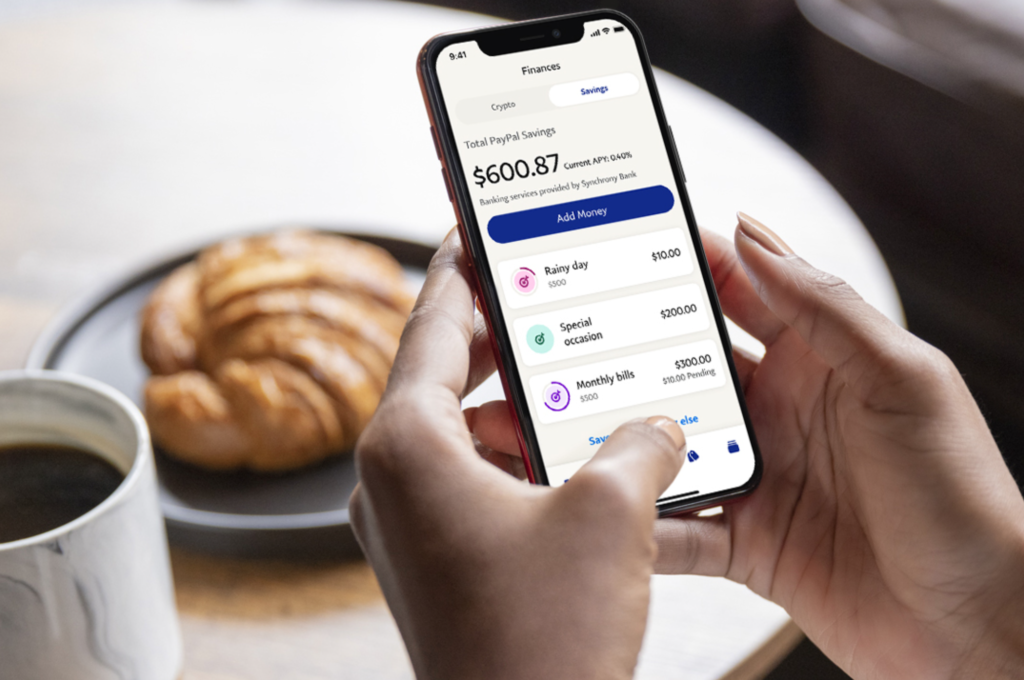

The company is adding a handful of features that bring it into “super app” territory, competing with the likes of WeChat, Alipay, and Paytm. PayPal’s app already offers a peer-to-peer payment tool, a mobile wallet, and a charity donation feature.

The new release, however, will offer more features and new banking capabilities. Here’s a rundown of what to expect:

PayPal Savings, a new, high-yield savings account provided in partnership with Synchrony Bank that pays 0.40% APY

In-app shopping tools that allow customers to discover and earn loyalty rewards

Billpay management tools that help users track, view, and pay their bills

A new Direct Deposit feature that fronts users their paycheck up to two days early

Rewards capabilities

Gift card management

Credit access

Buy Now, Pay Later services

Crypto purchasing, holding, and selling abilities

The app will show users a personalized dashboard of their account; a wallet tab to manage payments and direct deposits; a finance tab to access savings and crypto accounts; a payments tab that enables users to send and receive money, make a donation, and manage billpay; and a messaging feature built around peer-to-peer payments.

“We’re excited to introduce the first version of the new PayPal app, a one-stop destination for our customers to take charge of their everyday financial lives, with new features like access to high yield savings, in-app shopping tools for customers to find deals and earn cash back rewards, early access Direct Deposit, and bill pay,” said PayPal CEO Dan Schulman. “Our new app offers customers a simplified, secure and personalized experience that builds on our platform of trust and security and removes the complexity of having to manage multiple financial or shopping apps, remember different passwords and track loyalty rewards.”

What’s next for PayPal’s Super App? The company will add investment tools, offline QR code payments, and new shopping and deals capabilities.

PayPal is currently the closest thing the U.S. has to a super app. However, the new app is still missing some key elements that Asia’s successful super apps have, including food delivery, transportation, travel, health, insurance, government, and public services.

Financial planning software company RightCapital unveiled new dynamic retirement spending strategies on its platform this week. The new offering gives investors the ability to better plan their finances once their working days are done.

“The industry has been using a rather simple retirement expense approach in the financial planning process for many years,” RightCapital CEO Shuang Chen said. “The ability to offer multiple options for retirement spending within our comprehensive planning tool is a significant step forward.”

Traditionally, financial planners have relied on an inflation-adjusted retirement spending model which focuses on a single input – the rising cost of living – to anticipate an increase in retirement spending each year. One criticism of this approach is that it does not account for changes in an individual’s portfolio that might significantly affect how much they are able to spend in retirement. RightCapital’s new offering factors in changes in portfolio value, reducing retirement spending projections when the portfolio loses value and giving investors the option to spend more in retirement should their portfolio significantly increase in value. The two dynamic strategies – referred to as guardrail and floor and ceiling – enable retirement spending to adjust in sync with portfolio performance and investment strategy parameters rather than being limited to tracking the rate of inflation.

Dynamic strategies such as those now available on the RightCapital platform more accurately reflect how individuals respond to changes in their investments in the real world. As Michael Kitces, Chief Financial Planning Nerd for Kitces.com and Head of Planning Strategy for Buckingham Wealth Partners explained, “as advisors, we cannot eliminate the uncertainty of markets themselves, but tools like RightCapital’s dynamic spending can help eliminate the uncertainty for clients of what they’d have to do in response to those market events, facilitating better client conversations about how to keep their retirement on track.”

Other features of RightCapital’s dynamic retirement spending strategies include the ability to customize spending levels by age, anticipating a higher level of spending early in the investor’s retirement life and tapering off as the investor ages. The strategies can also incorporate changes in healthcare expenditures over the course of the investor’s retirement, as well.

Founded in 2015 and headquartered in Shelton, Connecticut, RightCapital demonstrated its technology most recently at FinovateSpring in 2019. At the conference, the RightCapital team demonstrated the company’s API/Enterprise solution, which gives financial advisors the ability to offer their clients access to custom applications ranging from PFM to account aggregation to secure document sharing. In June, RightCapital announced that it would “enhance (its) integration” with partner Riskalyze, a specialist in risk alignment and portfolio analytics. Also that month, RightCapital and a coalition of fintechs including fellow Finovate alum Bettermentlaunched the RIA Tech Suite to provide financial advisors with services and tools to automate back-office operations.

From the partnership between Best of Show winners MX and Dwolla that will enhance and automate account verification to the news of a strategic partnership between roboadvisor Bambu and Moven, collaborations between Finovate alums are filling the fintech headlines to start the week.

With MX and Dwolla, the partnership extends instant account verification coverage to 4,000+ institutions, making it easier for MX customers to connect securely to any deposit account. The integration also enables account verification through micro-deposits, which makes it possible for MX to offer verification for “nearly 100 percent” of deposit accounts in the U.S.

Enabling better access to micro-deposits by improving the verification experience is a key component of the integration. MX co-founder and CTO Brandon Dewitt underscored the importance of these deposits and the role they play in financial inclusion and serving the underbanked. “Micro-deposits have gotten a bad reputation in the industry, but the truth is for some of the population who bank with community credit unions or mid-sized institutions, it comes down to either using a micro-deposit or not having the ability to connect them to their accounts,” Dewitt said.

MX most recently demonstrated its technology on the Finovate stage two years ago at FinovateFall. The Lehi, Utah-based company won Best of Show for a live demo of its MX Enabled platform that helps financial institutions add to their offerings via connections with fintechs through MX’s API ecosystem. Earlier this month, MX launched a new suite of financial insights APIs and embeddable user interfaces to enable companies to pursue opportunities in open finance.

Dwolla won Best of Show in its Finovate debut in 2011 at FinovateSpring. The company announced just last week that it had raised $21 million in funding in a round led by Foundry Group that will help it continue to innovate in the B2B payments space.

“Partnering with MX will automate the verification experience and make it that much easier to verify a bank account,” Dwolla President and COO Dave Glaser said. “Together with Dwolla, MX has configured a new solution to ensure that millions of payments occur smoothly and easily each day. We couldn’t be more excited about this partnership and the impact it will have on millions of Americans.”

Giving average retail banking customers the kind of support typically available only to high net worth individuals is part of the motive behind the strategic partnership announced early this week between roboadvisor technology solution company Bambu and financial wellness technology platform Moven.

“Adding Bambu’s capabilities to Moven’s mobile-centric experience is well in-line with the needs of banks and fintechs to provide consumers with personalized, automatic investing to their product offerings,” Moven Chief Revenue Officer Bryan Clagett said. He noted that traditional banks still have a major impact and influence on their customers and, as such, they can and should do more – beyond banking – to enable their customers to better manage the entirety of their financial lives.

The new offering is designed to empower bank customers by allowing them to manage and plan their finances and investments more holistically. The goal is to provide customers with the equivalent of a digital CFO to help them better understand their spending patterns in order to increase savings and better manage their investments. This is a critical aspect of the new solution, which moves beyond simple robo-investing to give customers a more comprehensive view – and greater control – over their finances.

“We look forward to working closely with Moven as wealth and digital banking become more seamlessly connected,” Bambu co-founder and CEO Ned Phillips said. “Moven’s long history in digital banking and Bambu’s intelligent wealth APIs will provide a perfect platform for any financial institution focused on digital banking and wealth.”

Singapore-based Bambu made its most recent Finovate appearance last year at FinovateEurope in Berlin where the company demonstrated its BambuGo white label financial roboadvisor platform. Earlier this month, Bambu announced that it had acquired investment management technology company Tradesocio.

Making its Finovate debut more than eight years ago, Moven famously pivoted from a direct-to-consumer/neobank model to a focus on “smart banking and financial wellness” a little over a year ago. The company has teamed up since with fellow Finovate alums Q2 and Digital Onboarding, as well as with intelligent billpay company Blip Labs and digital asset manager NYDIG, to help them better engage their customers with actionable insights to enhance financial health.

Lendsmart, which took home Best of Show honors in its FinovateFall debut last year, announced a new partnership with Freddie Mac this week. The digital lending platform has integrated with Freddie Mac Loan Product Advisor, the firm’s automated underwriting system, to improve the loan origination process for both lenders and borrowers by reducing processing time.

“Lendsmart’s software predicts the credit and underwriting conditions required in the loan origination process by pinning them to a borrower’s data in real-time rather than making the borrower wait 45 days to get an email from the underwriter,” Lendsmart founder and CEO AK Patel explained. “We’re also shaving off weeks in the letter of explanation process.”

Headquartered in New York City, Lendsmart combines an AI-powered digital lending platform with a home buying marketplace to save lenders time, help them increase productivity, and grow their profits while providing both the lender and the homebuyer with a “next-generation digital experience,” in the words of Lendsmart COO Philip Gem George.

Lendsmart’s platform centralizes and unifies all parties in the mortgage process while automating manual tasks to ensure accuracy, reduce risk, and keep costs low. George noted during the demo of Lendsmart’s technology at FinovateFall that the automation ensured that homebuyers are only asked for information that cannot be readily accessed from the documentation. This further accelerates the process and relieves some of the burden typically felt by homebuyers during the origination process.

And as Freddie Mac VP of Business Partner Integration Kevin Kauffman added, technology like that available from Lendsmart helps financial institutions keep up with the expectations of their increasingly digital-first customers. “Today’s lenders and borrowers expect a seamless digital process that isn’t burdened with administrative tasks or excessive timelines,” Kauffman said. “Partnering with Lendsmart allows Freddie Mac to provide the latest technology that satisfies out mutual clients’ needs.”

Founded in 2019, Lendsmart was among the many fintechs that helped facilitate PPP funding during the COVID-19 pandemic, partnering with Griffin Technologies to offer banks and credit unions an end-to-end solution to enable them to process more loan applications while identifying and pursuing qualified small business leads. “With financial institutions struggling to manage the high number of applications and small businesses in need of immediate funds,” Patel said when the partnership was announced last spring. “We saw an opportunity to speed up and simplify the mostly manual process by using our existing technology.”

Lendsmart began the year raising an undisclosed amount of pre-seed funding from INV Fintech. In addition to its New York headquarters, the company also has an office in India.

Connectivity and financial data enhancement innovator MXlaunched a new suite of financial insights APIs and embeddable user interfaces this week. The APIs will enable developers to quickly and securely bring MX-powered financial data into their solutions, helping companies pursue their open finance initiatives. MX also noted in their announcement that their offering will help firms accelerate time-to-market for financial wellness products – with personalized smart recommendations and insights built into the company’s app or website.

The API integrations and widgets now available enable companies to enjoy the benefits of MX-powered financial data without requiring them to build their own front-end solution. The embedded nature of the offering allows developers to add widgets to mobile banking and shopping apps, for example, without having to make major changes to the overall app or user experience.

“MX APIs and widgets make it easy for any company to embed financial insights and wellness tools into their current products and services,” MX Chief Product Officer Brett Allred said. “We’re making data-driven financial wellness tools more available and scalable than ever before by giving developers an easier and more secure way to connect financial data and help build products that power new money experiences for customers.”

Founded in 2010 and headquartered in Lehi, Utah, MX began the year with a $300 million Series C funding round that gave the company a valuation of $1.9 billion. Since then, the multiple-time Finovate Best of Show winner has forged partnerships with banks and credit unions including Libro Credit Union, First Hawaiian Bank, and AbbyBank. MX also this year has teamed up with Viva First to help the digital bank promote financial wellness in the Latino community. In April, MX collaborated with Moov to bring faster account verification to fintechs.

MX currently connects more than 16,000 financial institutions and fintechs with its data connectivity network. The company powers 85% of digital banking providers, as well as thousands of banks, credit unions, and fintechs, reaching more than 200 million financial services customers. Ryan Caldwell is co-founder and Chief Executive Officer.

In its biggest investment round to date, U.K.-based Open Finance platform Moneyhub has secured $18 million in funding to support its expansion into new markets. The round was led by Sir Peter Wood, founder of Direct Line and Esure, via his new investment vehicle, SPWOne.

“It is incredibly rewarding to be able to deliver results to both investors and clients in this truly transformational landscape,” Moneyhub CEO Samantha Seaton said. “It is a fantastic vote of confidence from Sir Peter and his team, who are renowned for foreseeing game-changing growth opportunities – and a ringing endorsement of our team and our strategy for applying new technology where the rules of engagement have been turned upside down.”

A Finovate alum for more than four years, Moneyhub demoed the SmartAsset feature of its solution at FinovateEurope 2017. At the event, the company showed how SmartAsset’s AI-driven, intelligent messaging functionality helps users better manage their finances. In the years since, Moneyhub has grown into a leading open finance and data intelligence platform that offers both API and white label solutions to help businesses leverage personalization to enhance the customer experience. In the U.K., Moneyhub currently provides customer-permissioned financial data access to more than 200 financial services providers via 584 connections with an additional 3,500 connections in Europe.

Moneyhub’s funding announcement comes on the heels of a new partnership with Triodos Bank, a sustainable bank that supports working toward positive social, environmental, and cultural change. Founded in 1980, Triodos Bank serves more than 700,000 banking customers in the U.K., Germany, Spain, the Netherlands, and Belgium. The bank has lent more than £8 billion to support projects around the world that are dedicated toward “benefitting the people and (the) planet.” Triodos Bank also co-founded the Global Alliance for Banking on Values (GABV), a 63-bank network designed to promote sustainable banking.

“We are pleased that our customers will now be able to integrate their everyday banking with Moneyhub’s app and enjoy the many benefits of Open Banking, such as helping them to easily track spending and set budgets to help manage money,” Triodos Bank U.K. head of retail banking Gareth Griffiths said.

In addition to its partnership with Triodos Bank, Moneyhub teamed up with mortgage market insights and intelligence firm Hometrack, shared branch banking innovator OneBanks, and adtech specialist Zedosh this summer; partnered with financial health platform Level Financial Technology and charitable fundraising app Kynder this spring; and began the year collaborating with professional services company Aon and ESG investment platform The Big Exchange.

Along with the fanfare surrounding so-called meme stocks and the “power of the individual trader” last year, there was a dark side. Investing and trading platforms that had embraced gamification were being accused of not fully preparing their customers for the dangers involved in stock trading – especially in volatile, illiquid stocks. Critics demanded that these platforms spend more time – and money, if necessary – educating their customers for their own benefit as well as for the good of the investing and trading industry, which has recovered impressively since the dot.com bust 20 years ago.

This is the spirit in which we take the news that Stash, a New York-based, mobile-first investment platform that made its Finovate debut in 2017, has acquired financial literacy platform PayGrade. The terms of the deal were not disclosed, but the acquisition marks Stash’s first acquisition and its biggest fintech news headline since a whopping $125 million Series G fundraising back in February.

Brandon Kreig, CEO and co-founder of Stash said that the acquisition was an example of the company’s mission to “empower everyday Americans to invest for the future.” He noted that personal finance education is not emphasized in American schools – with 43 out of 50 states not requiring coursework in personal financial management – and that an overwhelming number of American adults – as much as 80% – live “paycheck to paycheck.”

“With PayGrade,” Kreig explained, “Stash will provide teachers, parents, and children with interactive tools to learn effective money management skills that will last a lifetime.”

Stash enables users to begin investing on its platform with as little as $1 a month. The company’s “Stash Beginner” program allows investing – including fractional share investing – as well as banking, portfolio recommendations, savings strategies, and a Stock-Back card that helps users earn stock every time they use the card for shopping. Stash also offers Growth and Plus plans that add features such as portfolios for children, premium research, and enhanced bonuses for using the Stash Stock-Back card.

Purchasing PayGrade is not the only way that Stash will support the cause of financial literacy this year. Stash’s acquisition news arrived just a few days before the company announced that it was partnering with the Suh Family Foundation and the Big Yard Foundation to launch a financial literacy program over the summer. Dubbed the Stash101 Summer School, the program will be conducted in partnership with Portland Public Schools and will give 160 middle school students an introduction to vital money management and wealth building.

“From investing and banking to education and retirement planning, we believe everyone has the power to achieve greater financial freedom—one step at a time.” Krieg said. “We’re thrilled to deepen our commitment to childhood education through Stash101 and this special summer school program in Portland with the Suhs and Big Yard. It’s going to be a tremendous four weeks for the kids.”

Stash101 is part of the Portland Interscholastic League Trajectory Math Program, which provides additional learning resources for historically underserved students. The course will include a simulated economy experience in which the students will complete tasks like renting desks, while earning a salary and learning about the difference between savings and credit. The classes will be held between July 6 and July 27 at a pair of schools in the Portland School system.

A pair of Finovate alums have announced plans to “tie the knot” this week. Intelligent Identity solution provider Ping Identity has agreed to acquire fraud and bot detection and mitigation specialist SecuredTouch. Terms of the transaction were not immediately available.

By leveraging a variety of enabling technologies – including machine learning, AI, behavioral biometrics, and deep learning – SecuredTouch’s technology empowers fraud and risk teams to identify suspicious and potentially malicious behavior across all digital entities. The acquisition will integrate SecuredTouch with Ping Identity’s PingOne Cloud Platform, giving business customers the ability to better understand and prevent malicious activity. Customers will have the option of using SecuredTouch as a standalone solution or as part of the PingOne platform.

Ping Identity founder and CEO Andre Durand said that the acquisition “accelerates” the company’s mission to provide cloud-based identity and anti-fraud solutions to businesses to help them fight a wide range of cyberthreats ranging from emulators to account takeover.

“Identity isn’t just about knowing who your customers are, it’s about knowing when someone is pretending to be a customer,” Durand explained. “As companies undergo massive digital transformation initiatives, the need for seamless, frictionless, and secure identity solutions to confidently understand both those situations is imperative.”

Ping Identity made its Finovate debut at our first European fintech conference in 2012. In the years since, the Denver, Colorado-based company has become the identity management solution provider of choice for 60% of the Fortune 100 and forged partnerships with technology companies like Microsoft and Amazon. Most recently, Ping Identity collaborated with ProofID to enhance identity security for Tesco Bank, the banking division of Tesco, the largest supermarket retail chain in the U.K.

Headquartered in Ramat Gan, Israel, SecuredTouch demonstrated its behavioral biometrics technology at FinovateFall 2018. The company’s solution analyzes more than 100 different behavioral behaviors – from scroll velocity to touch pressure – to create a unique user profile that benefits from continuous verification. Winner of Best Product at the Loyalty Security Association Lion’s Den event this spring, SecuredTouch earned a patent for its continuous use authentication in 2019.

“This is a defining moment for our industry as identity security and fraud come together,” SecuredTouch CEO Alasdair Rambaud said of this week’s acquisition news. “Ping Identity’s enterprise proven and robust platform provides the perfect foundation for SecuredTouch’s advanced fraud detection capabilities.”

From the rise of digital commerce to the growth of the gig economy to the challenge of a global pandemic, digital identity technology has been one of the bigger beneficiaries of a number of trends sweeping societies around the world. Add to this a new emphasis on financial inclusion and social equity, and you have a recipe for opportunity for many innovators in the digital identity space.

The latest company to take advantage of the current moment is OCR Labs, which made its Finovate debut at our developers conference, FinDEVr Silicon Valley, in 2016. The company, headquartered in Sydney, Australia and founded by Matthew Adams and Daniel Aiello, returned to the Finovate stage the following summer, earning a Best of Show award for a demo of its ID verification solution.

OCR Labs combines five different technologies – ID document OCR, document fraud assessment, liveness detection, video fraud assessment, and face matching – in a single, end-to-end digital identity experience. The company’s technology has been deployed in a wide range of verticals – from financial services and e-commerce to telecommunications and real estate – to provide AML and KYC-compliant digital ID verification and customer onboarding.

This week OCR Labs announced that it had raised $15 million (EUR 12.5 million) in Series A funding. The round was led Oyak Group of Turkey and will enable the company to expand into markets into Turkey, the U.K., and throughout Europe. OCR Lab currently maintains an international headquarters in London.

“No one wants to spend hours trying to prove who they are, whether it’s for a job or for a bank account, and we also want to know we’re protected against identity theft and fraud,” OCR Labs co-founder Daniel Aiello said. “Digital ID verification has a key role to play, but this year we’ve also seen the limitations if hybrid models are used. People are a barrier and a risk, but fully automated technology can have a huge impact on many industries and privacy. OCR Labs is built to be secure, frictionless and fast, and capable of recognizing ID documents the world over.”

Enjoying triple-digit growth since its launch, OCR Labs has partnered with Reed Screening to help businesses verifying candidate identities during the COVID crisis ahead of a potential in-person COVID check mandate later this month. There is some pressure to allow businesses to continue remote COVID checking, an idea with which OCR Labs understandably sympathizes.

“The need for digital verification is growing exponentially,” Aiello said. “This past year we’ve seen more demand from new sectors as they try to navigate the pandemic and an inability to operate in-person. We believe it has accelerated what needed to happen.”

On the consumption side of personal finance, managing credit is one of the most important aspects of financial wellness. And for more than a decade, Credit Sesame has been among the more innovative companies in this space. From its origins as a hub for financial planning tools, insights into credit scoring, and advice on smart borrowing, Credit Sesame has grown into a leader in the financial wellness industry with new solutions like its Sesame Cash debit account, which topped one million customers less than a year after emerging from its beta launch.

“With Sesame Cash and features like real-time cash back rewards and rewards for improving their credit score,” Credit Sesame GM and Head of Global Banking Miro Pavletic explained when the solution was introduced last September, “we are helping customers put more money back in their pocket than any other digital banking service. Whether you’re looking to buy groceries or debating where to grab takeout, we can connect you with the brands you love and give you cash back instantly,” Pavletic said.

The $51 million in new funding the company raised this week is a testament both to the journey Credit Sesame has been on since its launch in 2010, as well as the potential the firm has to continue to play a leading role in helping millions of consumers better understand and manage their finances.

“Creating access to better credit and finance is critical for financial prosperity for consumers in our country, and it’s enlightening to see major banks and the federal government also taking action,” Credit Sesame CEO Adrian Nazari said. “The impacts of the past year have only made those needs greater, and through our recent acquisition and fundraising, we are proud to be expanding our platform offerings and leading the charge in opening more doors to financial inclusion and wellness for all.”

The company sees its current mission as closing the “credit chasm,” which it believes limits economic opportunities for more than 44 million “credit invisible” Americans. Part of this effort includes Credit Sesame’s decision to acquire Zingo, a transaction that was completed recently. A fintech company headquartered in Portland, Oregon, Zingo helps renters improve their credit scores via timely rent payments. With almost 80% of its 15 million members renting, rather than owning, a home, Credit Sesame expects the acquisition to represent a “significant growth opportunity for the company” while enhancing “financial inclusion for its customers.” Credit Sesame anticipates integrating Zingo’s rent reporting technology into its financial wellness platform over the summer.

Looking out over the balance of 2021, Credit Sesame appears to be taking a page from Zingo’s book by launching a new feature that will enable consumers to use their cash to help them improve their credit rating. Requiring no credit check, the new solution will allow Credit Sesame customers to leverage their cash and credit together to help build a strong financial foundation and create a path toward better financial health.

How are banks and fintechs leveraging the lessons learned during the global health crisis to provide consumers and businesses with financial products that do an even better job than before of addressing their needs? And when it comes to innovation in technology and financial services, is disruption or collaboration dictating the pace of change?

To talk about these and other issues, we caught up with Andrea Zand, co-founder and Chief Operating Officer of FISPAN. Headquartered in Vancouver, British Columbia, Canada, FISPAN made its Finovate debut in 2017, demonstrating its cloud-based platform that leverages APIs to enable banks to deliver new business banking solutions to their corporate customers.

How are the banks you work with doing now – a little over one year after the onset of the pandemic?

Andrea Zand: Open-banking infrastructure and data sharing are helping banks and governments around the world better respond to the recovery post-pandemic. We are starting to see evidence that governments are beginning to use open banking data to help inform their pandemic responses and help small businesses. The banks we work with are feeling positive about the recovery going into 2021.

In what ways should banks expect customer behavior to change and how should they respond?

Zand: We’ve already seen that the pandemic has sped up innovation in financial services. Customers are getting more and more comfortable doing their personal banking online, and business banking customers are also turning to digital banking platforms as an alternative to in-person branch visits. Banks are struggling to keep up with this rapid shift in the types of online service offerings their clients are demanding.

Because of this, banks are looking to deploy innovations that will have an immediate impact on the client experience. This is where we see a huge opportunity with embedded banking. By embedding the banking experience inside the platforms that business customers use to run their businesses (such as ERPs or accounting software), banks are able to easily provide their business clients with a more automated and streamlined treasury management process. The banks that are ahead of the curve and partnering with fintechs like us are beginning to better understand how their customers use their products in context, allowing them to innovate smarter and faster.

Technology has moved too fast for the banks to build those capabilities themselves. The best way for B2B banks to manage the impact of rapidly evolving customer expectations is to partner with agile, innovative fintech services.

Connecting with their clients as much as possible and understanding their needs will be essential in driving the agenda for the new capabilities the banks should be focusing on. Leveraging tech and automation will manage and rise to customer expectations while still allowing for more face time during this transition period to explore and understand customers’ needs and wants.

What are some of the other challenges that banks will encounter as the recovery picks up steam – and how will FISPAN help them?

Zand: Banks will continue to be challenged by continually changing customer expectations. They will also be challenged by the need to adapt to an open exchange of data that will happen as a result of the many new fintech upstarts that are creating new business models and finding ways to better meet these changing client demands.

FISPAN helps by collaborating with FIs to understand what will make their customers happier by joining forces across all levels of the product discovery and implementation phases. Getting in front of the customers and understanding their day-to-day ERP and accounting struggles is a large part of how we meet and overcome the challenges that have risen due to the digital shift during our global pandemic. More specifically, we enable banks to extend their service offering to their business clients by embedding commercial banking applications within the organization’s ERP or accounting software.

For those institutions that engaged in digital transformations, how do they make sure those efforts truly pay off?

Zand: Continue to be open to new ways of thinking and working with new partners. In partnering, serving, or investing in innovation by way of technology upstarts, financial institutions are able to position themselves for future growth and adaptation through real-time, easy access to products, services, data, and channels. Delivering a product or service that truly resonates with their customers and meets them where they are with the current challenges they face in a rapidly growing digital market.

What does collaboration between banks and fintechs look like in a post-COVID world?

Zand: Collaboration between banks, fintech, and other providers is becoming more important as the payments landscape is becoming more complex. Banks that are open to partnering have a competitive advantage because they can provide better services at scale. Not to mention that some banks are at risk of getting disintermediated by nonbank providers for some of these types of solutions. The time that bank partners spend helping integrate their banking services into different platforms is markedly less than the time it would take for the bank to develop it themselves. That same time investment from the bank also leads to countless saved hours for their business clients, increasing their value as a business bank.

What has been your biggest professional takeaway from 2020?

Zand: If 2020 taught me anything, it was to always remain flexible and open-minded. One of the big plans we had was to go to some in-person events and start to talk face to face with end-users and really understand what kinds of pain points they were experiencing with their treasury management process. All of our events were either canceled or transferred to digital. We were still able to get the information we needed from customer interviews and case studies, but it just goes to show that sometimes your best-laid plans aren’t going to be in the cards and you need to pivot quickly.

What are you looking forward to most in 2021? Where do you see the greatest opportunities?

Zand: Besides being able to see our bank clients and end-users face to face, in 2021 I am looking forward to watching banks, payments providers, and fintech companies launching services and solutions that can help small businesses across the country emerge from 2020. I think the greatest opportunity for economic recovery and success post-pandemic lies in banks being better able to serve their small business clients.