This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

After the CFPB withdrew its lawsuit over Section 1033 of the Dodd-Frank Act, the bureau stated that it would begin a new, “accelerated” rulemaking process with an Advanced Notice of Proposed Rulemaking (ANPR) within three weeks. That three-week period ended last week, on August 22nd, when the CFPB published its Personal Financial Data Rights Reconsideration, effectively kicking off the new rulemaking process.

Much is riding on how this rule takes shape, not only for banks, but for fintechs and consumers alike. Visa’s recent move to abandon its US open banking initiatives underscores just how high the stakes are. In its latest release, the CFPB asked for comments and data to guide its decisions on four critical issues tied to Section 1033. Below, we’ll walk through each issue and explore the potential impact.

Representatives: who deserves access to the data?

The first of the four issues is defining who can serve as a representative on behalf of the consumer. The question essentially asks who can make a request to access the consumer’s data on their behalf. Today, this includes not only the consumer themselves, but also third-party aggregators and fintechs, as well. If the CFPB decides to narrow this scope, it could potentially block third-party services from accessing consumer data, limiting it to the consumer and the bank itself.

The latter would favor incumbents as it allows them ultimate control. For fintechs, this would create a risky environment. The uncertainty would make it risky to invest and build APIs that could be restricted in the future.

Fee structures: who pays for data access?

The second of the four issues seeks to determine the optimal amount of fees that banks should be able to charge in response to a customer-driven request. As a result, data access may no longer be free for aggregators, which may require them and fintechs to reshape their business models in response.

Charging for data would allow banks to recoup compliance costs for API access, but may receive negative attention from fintechs and consumers. Additionally, fintechs with already thin margins may be forced to look for an exit.

Data security: weighing threats vs. benefits

The third of the four issues the CFPB spotlighted is the threat and cost-benefit analysis for data security associated with complying with Section 1033. If the Bureau requires compliance with tighter security requirements, all stakeholders will feel the repercussions of tighter security expectations.

With tighter compliance, small fintechs that previously had limited compliance requirements may now need to step up to higher standards. This could ultimately lead to consolidation, since large, well-resourced firms would be able to more easily meet compliance.

Data privacy: the cost of protection

The final of the four issues the CFPB spotlighted is the threat landscape surrounding data privacy associated with Section 1033 compliance. The Bureau may set new limits on how fintechs are allowed to monetize consumer data in an effort to maintain their privacy.

With new guardrails on how they are allowed to monetize consumer data, fintechs may face limitations on using data for personalized marketing or other secondary data uses. As a result, innovation may slow down, but consumers may gain more confidence.

Your turn to comment!

The CFPB’s recent call for comments is more than regulatory housekeeping. It is highly consequential and will determine the future of open banking in the US. The Bureau’s questions signal real costs, risks, and opportunities.

It is important to make your voice heard on these issues! In the six days that the comment period opened, only seven comments have been submitted. Send your comments to the CFPB by October 10, 2025 at 11:59 pm EST.

It’s official! The FinovateFall 2025 demo lineup has reached full capacity with 64 innovative technologies selected, bringing together an impressive array of established players and promising newcomers at the New York Marriott Marquis over September 8 through 9.

This year’s complete lineup represents the full spectrum of financial technology innovation. From emerging AI agents to next-generation payment and banking technologies, the 64 selected companies will demonstrate technologies addressing the most pressing challenges in financial services today.

Max Capacity = Max Innovation

For those who haven’t secured their spot yet, this Friday, August 29 is the last chance to save. Book your pass today.

Ant International, Standard Chartered, and Swift have launched a new bank-to-wallet solution linking Swift’s 11,500-institution network with Alipay+’s 1.7 billion digital wallet accounts across 36 providers.

The service offers faster, regulated alternatives to stablecoins, with ISO 20022 backing to ensure interoperability, compliance, and scalability for cross-border payments.

Beyond speed, the initiative aims to boost financial inclusion, giving underbanked consumers access to funds through wallets they already use while allowing banks to stay relevant in wallet-first markets.

Global payments and fintech provider Ant International, international banking group Standard Chartered, and provider of secure financial messaging services Swift are banding together this week to launch a bank-to-wallet payment solution.

The three are leveraging Swift’s network of over 11,500 financial institutions in more than 200 countries and territories, as well as Ant International’s global wallet gateway service Alipay+. The new payment solution will connect Swift’s network to the 1.7 billion user accounts on the 36 global digital wallets in Alipay+’s ecosystem.

“We are very excited to be part of this ground-breaking multilateral collaboration with Swift, banking leaders, and Alipay+ e-wallet partners to facilitate bank-to-wallet transactions on a global scale,” said Ant International General Manager of Global Remittance Jacques Xu. “Ant International will continue to support such cross-sector collaboration with fintech innovations, to build a more connected payment and financial ecosystem for businesses and consumers with ever higher standards of transparency and security, as part of our focus on promoting global interoperability and inclusion.”

The digital wallet can also create an onramp into the traditional financial system. That’s because wallets connected to banks via Swift create a bridge that allows users to build transaction histories, potentially improving access to credit, insurance, and other financial services. Additionally, it has the potential to help unbanked and underbanked consumers because the bank-to-wallet capabilities allow them to receive money directly into a wallet they already use, circumventing the barriers to opening a bank account.

“In a world of fast-moving innovation with a growing number of ways to move value, consumers and businesses expect more choice and optionality in their international payments experience,” said Swift Chief Executive, Asia Pacific, Kevin Wong. “Swift is at the forefront of providing a best-in-class experience with greater flexibility and choice. This collaboration with Ant International and Standard Chartered reflects that strategic commitment to faster, frictionless payments across multiple networks.”

The first transactions on the new payments solution have already been successfully completed between a Standard Chartered Bank customer account and a partner e-wallet.

The launch of the new bank-to-wallet solution comes as stablecoin capabilities gain traction as an alternative for cross-border payments. However, while stablecoins promise fast, low-cost settlement, regulatory uncertainty and fragmentation have limited their adoption at scale. By contrast, today’s initiative shows how banks and fintechs can deliver many of the same benefits through established, regulated rails. Backed by the ISO 20022 messaging standard, the model also ensures interoperability and compliance with global payment systems, giving it a more durable foundation than many of today’s experimental stablecoin frameworks.

This partnership is a great example of how traditional banks and infrastructure services are collaborating with international tech players, moving from competition to interoperability. By linking Swift’s rails with Alipay+’s wallet ecosystem, the bank-to-wallet solution not only brings underbanked consumers into the financial system, but also strengthens cross-border payments. For Standard Chartered, it offers a chance to remain as a central player in markets where digital wallets dominate. The launch is also validating for fintechs that digital wallets have now gone mainstream.

“We are pleased to be the bank of choice to conceptualize, test, and deliver this innovation,” said Standard Chartered Global Head of Transaction Banking Michael Spiegel. “It is testament to the versatility of our banking platform and our strategic relationship with both Swift and Ant International. We will continue to push the boundaries of finance to shape the future of our industry, securely and in compliance with regulatory requirements.”

When it comes to the conversation on cryptocurrencies in financial services, the discussion often starts with stablecoins. And with good reason. The stablecoin market today is estimated to be worth $250 billion. Major financial institutions including JPMorgan, Goldman Sachs, and BlackRock have incorporated stablecoins into transactions and settlement operations. Technology giants like Meta, Apple, and Amazon are exploring the use of stablecoins for payouts. And the recently passed GENIUS Act in the US will establish a regulatory framework for these digital assets.

But there’s another child of the blockchain that is working its way toward the mainstream and that’s tokenization. Darren Carvalho, Co-Founder of MetaWealth, in a recent piece for Finextra, described tokenization as: “the process of digitally representing real-world assets, including stocks, bonds, and real estate, on the blockchain in the form of a token.”

Why is this a big deal? As Carvalho explained, tokenization promises to bring greater efficiency and inclusion to traditional financial markets. This includes making a wide range of financial assets accessible to a broader range of potential investors thanks to its exceptional ability to enable fractional investments. The deployment of smart contracts that automate compliance processes is another use case for tokenization that has excited advocates of the technology.

To discuss all this and more, we caught up with Carvalho’s colleague, fellow MetaWealth Co-Founder and CEO, Amr Adawi (pictured). In this interview, Adawi shared his insights about the growing role of tokenization of real-world assets (RWA) in financial services and how a new generation of companies is helping individual investors leverage tokenization to build their wealth.

You recently announced a distribution of more than one million USD in yield income to token holders. Why is this milestone important and what does it say about the outlook for tokenized assets?

Amr Adawi: Distributing over $1 million in yield income to MetaWealth token holders is a significant milestone—not only for our platform, but also as a true validation of tokenization as a transformative technology in the real estate industry. MetaWealth demonstrates that tokenization has moved beyond the hype and now delivers real financial outcomes for everyday investors. Essentially, we have met the promise of tokenization: democratizing access to traditionally high-barrier investments.

It is also worth highlighting the underlying structure of the yield income distributed to investors. MetaWealth is passing on real rental income generated from the income-producing properties listed on its platform, demonstrating that tokenized assets can deliver both accessibility and returns without having to compromise on compliance, transparency, or limit investor protections.

Let’s step back a bit. What are tokenized assets? Why are they becoming more important?

Adawi: We use the term “tokenized assets” to refer to any asset—from real estate and cars to bonds and stocks—that are represented as digital tokens on the blockchain. Each token corresponds to a share of ownership or interest in the underlying asset, enabling secure, transparent, and fractionalized ownership of the asset.

We’re seeing such deep interest in tokenized assets, especially from financial institutions, because of their ability to remove long-standing barriers in traditional finance. Take real estate investing, for example; the industry has been limited by high entry costs, complex legal structures, and illiquidity. Tokenization has completely removed these barriers to entry by lowering the minimum investment, increasing transparency and enabling more flexible trading of assets through digital ownership.

How does MetaWealth fit in? What problem does MetaWealth solve?

Adawi: MetaWealth is an investment platform that is purposefully designed to enable global investors to access institutional-grade and income-generating real estate through tokenization.

We partner directly with Europe’s leading property developers, bringing investment opportunities to any retail or corporate investors that were previously reserved for large institutions. Our platform complies with all relevant legislation, recently achieving the EU’s VASP licence and now pursuing MiCa registration. Using our fully-licensed platform, investors can buy into premium properties with as little as $100 and receive yield directly through our platform.

MetaWealth’s approach to real estate investment is also advantageous for property developers, opening up their projects to a broader capital base, unlocking new revenue streams and greater liquidity through the power of tokenization.

Who are MetaWealth’s primary customers? How do you reach them?

Adawi: Our platform serves both retail investors and institutions, with over 50k investors signed up across 23 countries in Europe and Canada. MetaWealth’s support for fractionalized real estate investments on-chain, and within an investment platform that offers transparent performance reports and adheres to high regulatory standards, is particularly appealing to institutional investors.

Investors typically find us through their own research on small-ticket real estate investments, with our direct investment opportunities in properties across Greece, Italy, Spain, and Romania making us stand out from competing platforms.

What in your background gave you the confidence to tackle this challenge?

Adawi: I think it’s important to highlight the scale of this challenge; real estate is a $180 trillion market, and has proven resistant to digitization so far. The root of my confidence that we can tackle this challenge is a deep belief that financial inclusion typically wins in the long term; challengers in cross-border payments, stock investments, banking, and more have been able to capture market share. More specifically, I’m confident we can build a reputable, user-friendly and efficient tokenized investment platform due to my years of experience building across both Web2 and Web3 ecosystems.

Before co-founding MetaWealth, I spent over eight years working at leading startups and organizations including Wealthsimple, the Chan Zuckerberg Initiative, Drop, and Meta. I also co-founded 1lens, an AR company leveraging computer vision to create immersive, real-world experiences. This career trajectory, and the invaluable knowledge I picked up along the way, allowed me to design and deploy platforms used by millions—platforms that demanded both robust infrastructure and user-first design at scale.

All of the above experiences have enabled me to do what I care about the most: solving real problems with technology that expands access and opportunity. It is a simple fact that real estate remains one of the most powerful pathways for wealth creation and yet it is still inaccessible for many. We’re democratizing this key asset class, bringing benefits to every stakeholder in the property value chain in the process.

Can you tell us about an implementation or deployment of your technology that you think is especially noteworthy?

Adawi: MetaWealth’s most impactful deployment of our technology has to be our real-time yield distribution to global investors who hold tokenized real estate investment on the MetaWealth platform. Surpassing $1 million in distributed yield, directly delivered to users’s wallets via blockchain, validates our entire business model—merging asset-backed performance with digital ownership infrastructure. Further noteworthy implementations include funding developments in Athens, Rome, and other European cities, increasing supply of housing while bringing returns to our users.

There’s growing interest in and awareness of stablecoins. Do you think interest in tokenized assets will catch up? What could drive faster embrace of tokenization?

Adawi: Stablecoins have seen accelerated adoption because they offer a clear and undeniable utility, serving as a powerful alternative to frictionless money movement. Essentially, stablecoins have proven their worth by being stable, liquid, and solving a global pain point transferring value across borders, unhindered by borders or time constraints.

Conversely, tokenized assets are more complex in nature, although we are already seeing more real-world use cases that deliver measurable returns. The drivers of tokenization adoption will be performance and transparency. When people can buy a tokenized share of a property, receive verified rental income and track ownership on-chain, the technology becomes more concrete.

Although the technology clearly works, better UX, credible regulation, and consistent yield will accelerate tokenized assets’ credibility as an investment vehicle among retail and institutional investors. Moreover, broader education about tokenized assets as well as integrations with mainstream fintech apps and further regulation will bolster investor confidence.

What can we expect to hear from MetaWealth in the months to come?

Adawi: Following the recent approval of our VASP license early this year, which allows MetaWealth to expand its offerings in the tokenized real estate market, including introducing a compliant secondary market for its real-world assets and real estate tokens, we are now focused on our upcoming MiCAR submission. This will enable MetaWealth to operate with regulatory clarity across the EU, unlocking passporting rights, enhancing trust, and institutional access and many other benefits that will enable us to scale.

Outside of MiCAR, we are continuing to expand our presence across Europe. A majority of our $50+ million in tokenized assets remain under development, with assets in Spain and Italy recently reaching 100% in commitments. Over the months to come, we will list new real estate assets on the MetaWealth platform, spanning a range of European markets.

Global payouts orchestration platform PayQuicker announced that it now offers Same-Day ACH for US payees. The expansion of the company’s real-time payout capabilities will be made available to select users across the firm’s key verticals including the gig economy, affiliate marketing, direct selling, and other industries where fast, secure payments are required.

“Timely compensation plays a critical role in driving payee engagement and ultimately business success,” PayQuicker VP of Partners and Relationships Kevin Zeman said. “With Same-Day ACH, we’re equipping our partners with a powerful advantage, enabling them to deliver faster, more reliable payments that drive loyalty, and meet the unique financial needs of payees across the globe.”

In its statement, PayQuicker highlighted the value of Same-Day ACH for a wide variety of industries, including clinical trials, where there is a direct correlation between fast and reliable compensation for trial participants and their retention and engagement. According to a report from Linear Clinical Research, participants in clinical trials can be forced to wait up to four business days for bank transfers. Same-Day ACH, in contrast, enables organizations to settle payments for trial participants within the same day, boosting both efficiency and participant satisfaction.

Same-Day ACH adds to PayQuicker’s suite of payments solutions, which include instant payments to cards and digital wallets. The company’s single API connects to multiple banks and payment rails, optimizing transactions for speed, cost-effectiveness, or both. The technology supports instant, hourly, and daily payouts, as well as on-demand earned wage access. Available as a white-label offering, PayQuicker’s technology enables payees to leverage branded debit cards, customizable portals, and mobile apps to help ensure that organizations are able to keep their brands top of mind.

Founded in 2007 and headquartered in Rochester, New York, PayQuicker made its Finovate debut at FinovateFall 2022. At the conference, the company demonstrated Payouts OS, PayQuicker’s in-market, payouts payment orchestration platform which determines and facilitates the fastest, most cost-effective payment routing across 210+ countries and in 80+ currencies.

Earlier this year, PayQuicker announced that it was expanding its instant payout and local currency solution for clinical trials across the UK and EU. The ability to provide real-time digital payouts in local currencies has enabled clinical trial organizations and trial sponsors to quickly and securely compensate trial participants while remaining compliant with local regulations and laws.

Thinking about attending FinovateFall next month, September 8 through 10, in New York? Register by Friday, August 29 and take advantage of big savings on the price of your ticket.

Pipe is partnering with Airwallex to expand its global reach, leveraging Airwallex’s infrastructure for same-day and next-day payouts to SMBs in need of fast working capital.

Airwallex’s global network supports local collections in 60+ countries and transfers in 21+ countries, which will help Pipe deliver seamless, localized financial services as it scales.

Pipe is already live in the UK and Canada with Airwallex, and is preparing to launch in Australia by year’s end.

Global trading platform for recurring revenue streams Pipe has selected global commercial payments and financial platform Airwallex to help Pipe grow globally.

The partnership enables Pipe to tap into Airwallex’s tools for delivering same-day and next-day payouts to small businesses that rely on accessing working capital quickly. Combining Airwallex’s extensive international coverage with Pipe’s local payment rails will help Pipe scale its platform globally while ensuring its clients enjoy seamless, localized financial experiences.

Pipe was founded in 2019 to provide businesses with access to working capital and financial tools. The company helps business owners who want to have the option of launching in multiple markets, saving them the hassle of selecting different partners and infrastructure providers.

“Our goal at Pipe is to enable software platforms that are serving SMBs to unlock revenue potential through embedded financial tools—no matter where they operate,” said Pipe CEO Luke Voiles. “With its broad global coverage and deep product capabilities, Airwallex gave us the support to launch in our first international market in weeks, not months. That speed and scale are critical for us as we look to expand our global footprint.”

Airwallex provides alternative accounts to help businesses manage their funds, access capital, control their spending, and embed financial services. The company helps businesses collect funds like a local in 60+ countries and make local transfers in 21+ countries. Founded in 2015, the Melbourne, Australia-founded company now processes $200 billion each year.

Pipe has already demonstrated momentum in its partnership with Airwallex, launching in the UK in late 2024 and entering Canada earlier this year. The California-based company is set to expand further, with plans to go live in Australia before the end of this year and a vision to enter markets across Europe and Asia Pacific in 2026.

“Pipe is bringing innovative embedded financial solutions to global markets with remarkable speed, and we’re proud to help power that momentum,” said Airwallex CRO Kai Wu. “Our global payments infrastructure was built to help leading businesses like Pipe reach new heights, expand access to new markets and verticals, and help them better serve their customers around the world.”

Today’s partnership is a testament to the fact that embedded financial services and offering global payments infrastructure are no longer optional but essential, especially for firms that want to scale. For Pipe’s business customers, this could make the difference between competing locally and thriving globally.

Budapest, Hungary-based digital banking solutions company Finshape has completed its acquisition of loyalty platform Realtime-XLS.

The acquisition will enhance Finshape’s expertise in customer loyalty with the addition of 60 new specialists, as well as expand the firm’s reach geographically.

Finshape made its Finovate debut at FinovateEurope 2023 in London.

Digital banking solutions provider Finshapehas completed its acquisition of loyalty platform Realtime-XLS. Finshape bought the company from the Collinson Group and it represents Finshape’s first acquisition of a global product company. Terms of the transaction were not disclosed.

There’s a lot to like in the move. The acquisition will boost Finshape’s expertise in the field of customer loyalty, giving the company 60 new specialists. The deal will also enable Finshape to extend its geographic reach courtesy of new offices in France and Singapore, and bolster its relationships with major banks in the UAE, Australia, Indonesia, and Singapore. In total, Finshape will consist of nearly 600 professionals supporting millions of end users across 100 banks around the world.

“This acquisition is a strategic milestone on our mission to transform the way banks serve their customers by unlocking the full potential of people and technology,” Finshape CEO Petr Koutný said.

Integrating the Realtime-XLS solution will give Finshape’s Digital Bank Operating System (DBOS) advanced loyalty capabilities, enabling banks to reward customer behavior, boost customer engagement, and generate additional revenue via cross-sell and up-sell opportunities. This will increase customer lifetime value, help banks secure a larger share of wallet, and make growth more sustainable.

“The loyalty solution will now form an integral part of our growing, customer-centric digital banking portfolio,” Koutný added. “Seamlessly integrated into our DBOS platform, it enhances the value we deliver by enabling banks to offer hyper-personalized experiences and build deeper, more meaningful relationships with their customers.”

Headquartered in Budapest, Hungary, Finshape won Best of Show for its demo at FinovateEurope 2022. At the event, the company showed how its platform combines digital banking and deep personalization capabilities to help financial institutions boost digital engagement, loyalty, and sales—especially among their micro- and small business customers. The company was formed in 2021 when Czech Banking Software Company (BSC) merged with Hungary’s W.UP (a three-time Finovate Best of Show winner).

Jenő Nieder, Deputy CEO at PortfoLion Capital Partners, the majority owner of Finshape that helped finance the merger between BSC and W.UP, praised the transaction as “perfectly aligned with the buy-and-build strategy” conceived when Finshape was founded. “This transaction not only incorporates a new loyalty platform but also adds new capabilities and true global coverage to an already strong company,” Nieder said.

A look at the companies demoing at FinovateFall in New York on September 8 – 10. Register today using this link and save 20%.

Conductiv

Conductiv helps lenders find more good loans, approve them faster, and grow portfolios safely using AI and permissioned data orchestration.

Features

Prevents fraud

Identifies charge offs before they happen

Finds new good loans hidden within existing loan applications

Who’s it for?

Banks and credit unions that make retail, SMB, and commercial loans.

Dimply

Dimply is an intuitive AI experience engine for builders in financial services to create, own, and evolve customer experiences, turning any data into personalized experiences, ready to embed instantly.

Features

Allow teams closest to customers to own the experience

Bring APIs in real-time to orchestrate data

Deliver personalized journeys inside existing apps and sites

Who’s it for?

Banks, credit unions, insurers, pension providers, wealth managers, and other financial services providers.

ID-Pal

ID-Pal’s ID-Detect is an additional layer of verification applied to every submission that accurately detects the most common type of AI document fraud, like synthetic IDs and portrait swaps.

Features

Confirms presence of physical, real ID vs. deepfake

Detects AI-manipulated IDs instantly and removes risk of fraud

Delivers seamless onboarding of real users and reduces false-positives

Who’s it for?

Credit unions, community banks, payment providers, wealth management firms, fund admins, merchant acquirers, and financial service providers.

Kaaj AI

Kaaj AI agents turn messy small business loan packages into clear, holistic risk assessments in just three minutes, helping lenders close ten times more loans.

Features

Delivers an end-to-end small business loan assessment in three minutes

Provides holistic credit and fraud risk insights with ready-to-review credit memos

Offers AI agents for loan officers, sales, and credit teams that unlock ten times more loans

Who’s it for?

Banks, credit unions, and small business lenders.

Payfinia

Payfinia’s composable QR payment service, built with Matera, allows FIs to deliver secure, instant QR code payments across FedNow, RTP, ACH, and digital asset platforms.

Features

Delivers instant, secure bank-to-bank payments via QR codes

Works across FedNow, RTP, ACH, or digital assets

Ensures safe, real-time transactions with native fraud controls

Who’s it for?

Credit unions, community banks, digital banking platform providers, and fintechs.

Scamnetic

Scamnetic offers cutting-edge, globally patented AI solutions that detect, prevent, and stop scams in real time, protecting identities and communications everywhere.

Features

KnowScam 2.0: Provides real-time scam detection across multiple channels

IDEveryone™: Delivers instant identity verification to prevent impersonation

Enhanced AI: Uses deepfake detection with actionable insights

Who’s it for?

Banks, credit unions, payment providers, fintechs, SMBs, and individuals.

Vertice AI

Vertice AI empowers community FIs with predictive analytics that transform data into actionable insights, driving smarter, measurable growth.

Features

Delivers AI-powered insights for precise customer targeting, boosting acquisition and cross-selling

Provides automated, personalized campaigns that maximize engagement

Chime is partnering with Workday to integrate Chime Workplace into Workday Wellness, expanding access to financial wellness tools through employers’ existing HR systems.

Chime Workplace helps employees manage money, save, and build credit, while giving employers insights into overall financial health and benefit usage.

The move positions Chime beyond consumer banking, signaling its push into the employer-driven financial wellness space.

Chime announced its latest move to build up Chime Workplace, the financial wellness suite it launched in March of this year. The company has partnered with HR solutions company Workday, becoming a Workday Wellness partner for financial benefits.

Chime will integrate Workday Wellness into Chime Workplace to bring financial wellness into its employee benefits suite. Chime Workplace offers employers a single platform with financial wellness tools and an aggregated view of employee financial health. The platform helps employees manage their money, track their savings, build their credit, and more.

Workday was founded in 2005 to provide HR tools as a service to businesses across industries. Today, in addition to offering a wide range of HR tools, the company also offers AI tools such as agents, financial tools such as payroll and financial management, legal tools such as contract intelligence, supply chain management solutions, and more.

Under the partnership, organizations using Workday can turn on benefits for their employees using Chime Workplace directly through Workday Wellness in their existing HR systems. Workday’s Workday Wellness solution offers its clients insights into which benefits their employees want and use, helping them to improve their programs and add appropriate new offerings, all in the Chime Workplace dashboard. Chime Workplace will be available via the Employer Benefits Selection Portal for Workday customers.

“Employees today are increasingly looking to their employers for competitive financial wellness benefits,” said Workday General Manager, HCM, Workforce Management and Payroll Cristina Goldt. “Our partnership with Chime makes it easy for Workday customers to provide their workforce with financial wellness tools directly through Workday Wellness. This ultimately helps them manage money, build credit, and save—fostering a more financially confident and resilient workforce.”

The integration is Chime’s latest move to differentiate itself as a competitor in the challenger banking field. The company was founded in 2012 and formed Chime Enterprise in 2024 after acquiring employee rewards and loyalty platform Salt Labs. Chime has more than 8.7 million members. By embedding its workplace tools into HR platforms like Workday, the company is positioning itself not just as a consumer bank alternative, but as a partner in the employee benefits ecosystem. This shift may indicate that Chime intends to grow beyond direct-to-consumer banking and capture a larger share of the employer-driven financial wellness market.

A new partnership between Donor-Advised Fund (DAF) provider Endaoment and philanthropic advisory firm Active Cause will help creatives, athletes, entertainers, and influencers make charitable donations in cash, stock, crypto, and other assets.

A DAF works like a charitable investment account, enabling investors to make tax-deductible contributions and to recommend charitable grant outlays from the fund, while the assets grow in value over time.

Founded in 2020, Endaoment made its Finovate debut at FinovateSpring 2024 in San Francisco. Robbie Heeger is President and CEO.

Next-generation Donor-Advised Fund (DAF) provider Endaoment has teamed up with philanthropic advisory firm Active Cause. The partnership combines Endaoment’s DAF infrastructure with Active Cause’s experience in serving the philanthropic needs of athletes, creatives, entertainers, and other influencers. Active Cause clients will be able to leverage the Endaoment platform to set up their own personalized DAFs where they can make charitable donations in cash, stock, crypto, as well as other assets.

“Active Cause is leading a cultural shift in philanthropy by centering creatives, athletes, and entertainers,” Endaoment President and CEO Robbie Heeger said. “We’re proud to provide the technology and infrastructure that allows their members to give seamlessly and confidently, while tracking their impact in real time.”

A DAF is a financial vehicle that acts like a charitable investment account. Contributions to DAFs are irrevocable to the sponsoring 501(c)(3) organization, which gains legal control over the funds. And while funds cannot be withdrawn for personal use, contributors—donors—still retain advisory rights over how the funds are invested and ultimately distributed.

DAFs provide donors with immediate tax benefits, enabling them to deduct the full amount of the contribution from their tax bill. The invested assets appreciate and grow tax-free over time and donors can recommend grants from the fund to qualified charities as they deem appropriate.

The partnership will embed charitable giving options directly into Active Cause’s membership platform, empowering influencers to support the causes that matter most to them. In addition to providing streamlined, simplified philanthropic service and tax advantages for creatives with often high-but-unpredictable income streams, the personal DAFs also offer a degree of privacy to help keep charitable donations out of the headlines.

“Our partnership with Endaoment gives members access to a modern platform that makes giving easier, faster, and more transparent,” Active Cause Co-Founder and CEO Yonis said in a video statement posted on LinkedIn.

Active Cause has more than 20 athletes, artists, and creators who have launched funds through the company and granted more than $10 million to community organizations as of 2025. The company provides philanthropic strategy and impact monitoring on key metrics like tax savings and fund growth. Working with Active Cause streamlines philanthropic processes, cutting administrative time by up to 50%, and lowering administrative costs to as low as 1.5% for DAFs greater than $10 million.

Founded in 2020 and headquartered in San Francisco, California, Endaoment made its Finovate debut at FinovateSpring 2024. Earlier this year, the company launched its Farcaster mini-app that helps users “convert emotional resonance into immediate impact.” The app enables users to find and donate to causes directly within their social feed and to share giving opportunities with those in their network. Donations can be made in USD, USDC, or ETH.

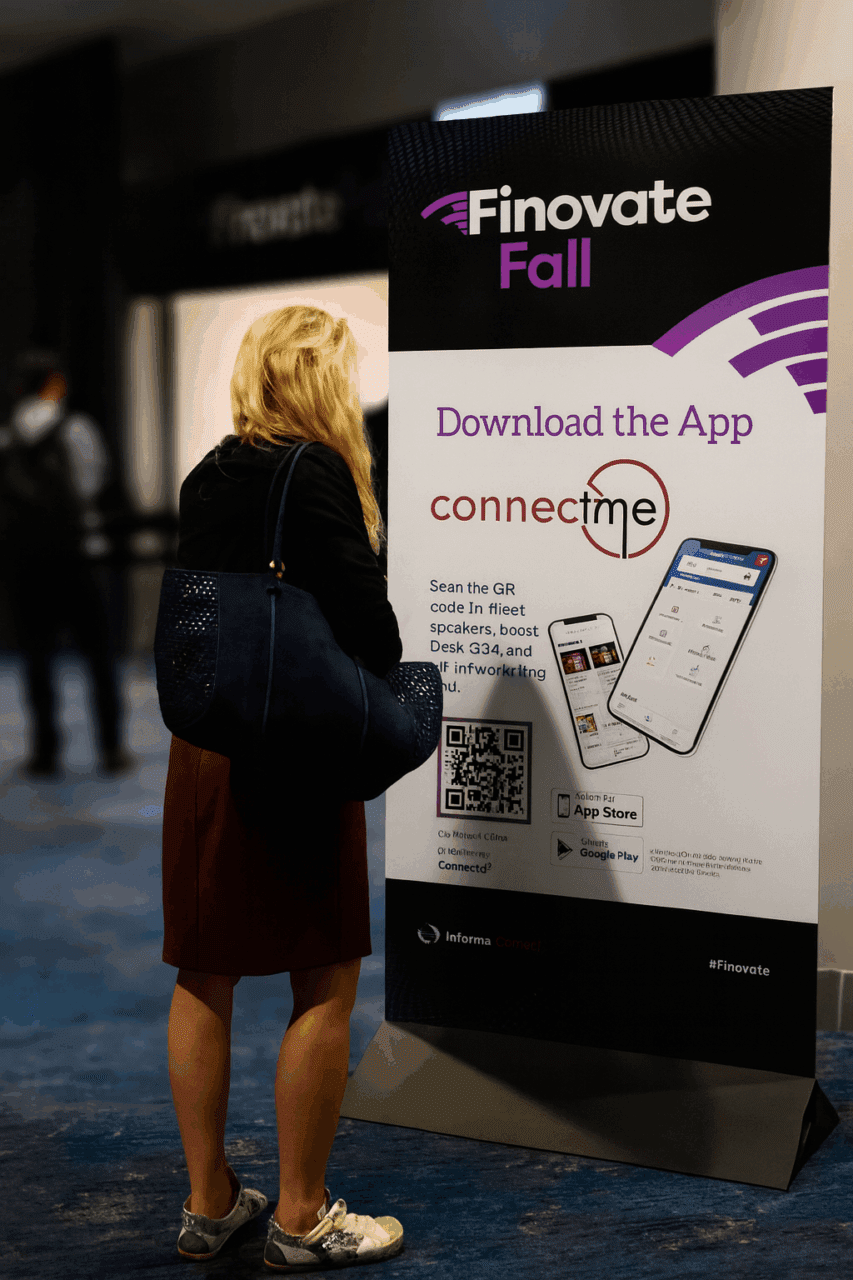

FinovateFall is just around the corner (taking place September 8 through 10 in New York), and we can’t wait to welcome fintech leaders, bank executives, investors, and analysts back to our flagship show. With discussion sessions, networking opportunities, and 60+ demos packed into three days, it’s important to have the right tools at your fingertips to help you navigate the event. That’s where the ConnectMe event app comes in.

You can think of the app as your personal conference assistant. It gives you everything you need to maximize your time at FinovateFall, starting today and continuing after the event.

Plan Ahead

With the app, you can browse the full agenda, bookmark the sessions and demos that matter most to you, and build a personalized agenda to manage your on-site schedule. Whether you want to see the latest fintech demo on stage or catch a discussion on open banking, you’ll know exactly where you need to be and when.

Connect with the Right People

Networking has always been a cornerstone at Finovate, and the app makes it even easier. Use the attendee directory to see who else will be in the room, send messages, and set up meetings in advance. The app features an AI-powered matchmaking feature that highlights the people and companies most relevant to you, making it easy for you to make the high-impact connections you’re looking for.

Stay in the Loop

From last-minute speaker updates to location details, the app keeps you informed in real-time so you don’t miss a thing. You can also engage in live polls and Q&A during sessions, making the event more interactive and getting your voice heard.

Keep the Conversation Going

Your FinovateFall experience doesn’t end when the conference does. The app remains open after the event, giving you continued access to contacts, content, and discussions. Whether you missed a meeting or wanted to follow up with a contact you met on the networking floor, the app makes it easy to keep building relationships and follow up on new opportunities.

To download the FinovateFall ConnectMe app, keep an eye on your email inbox for a link and a code to get in. Be sure to set up your details within the app ahead of the show in order to hit the ground running. Whether this is your first Finovate or your fifteenth, the app is the best way to ensure you can maximize your event experience.

The fallout from JP Morgan’s plan to charge companies for access to client bank account data continues as—according to a report from Bloomberg—Visa has announced that it is shuttering its open banking unit.

We’ve got a lot to say about the fight for open banking next month at FinovateFall. For now, be sure to check in to Finovate’s Fintech Rundown for all the latest fintech news!

AI-powered credit intelligence company martini.ailaunches its Financial Autonomy Ladder, a framework for measuring an institutions evolution from manual to autonomous decision-making systems.

MeridianLinkexpands its partnership with Jack Henry, which will resell the suite of Meridian Link One platform solutions, including MeridianLink Mortgage and MeridianLink Consumer.

First Northern Credit Union selectsAppli to modernize member lending experience.

Small business solutions

Expensifyannounces upgrades to its Expensify Travel offering including central billing, event management, and employee itineraries.