This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

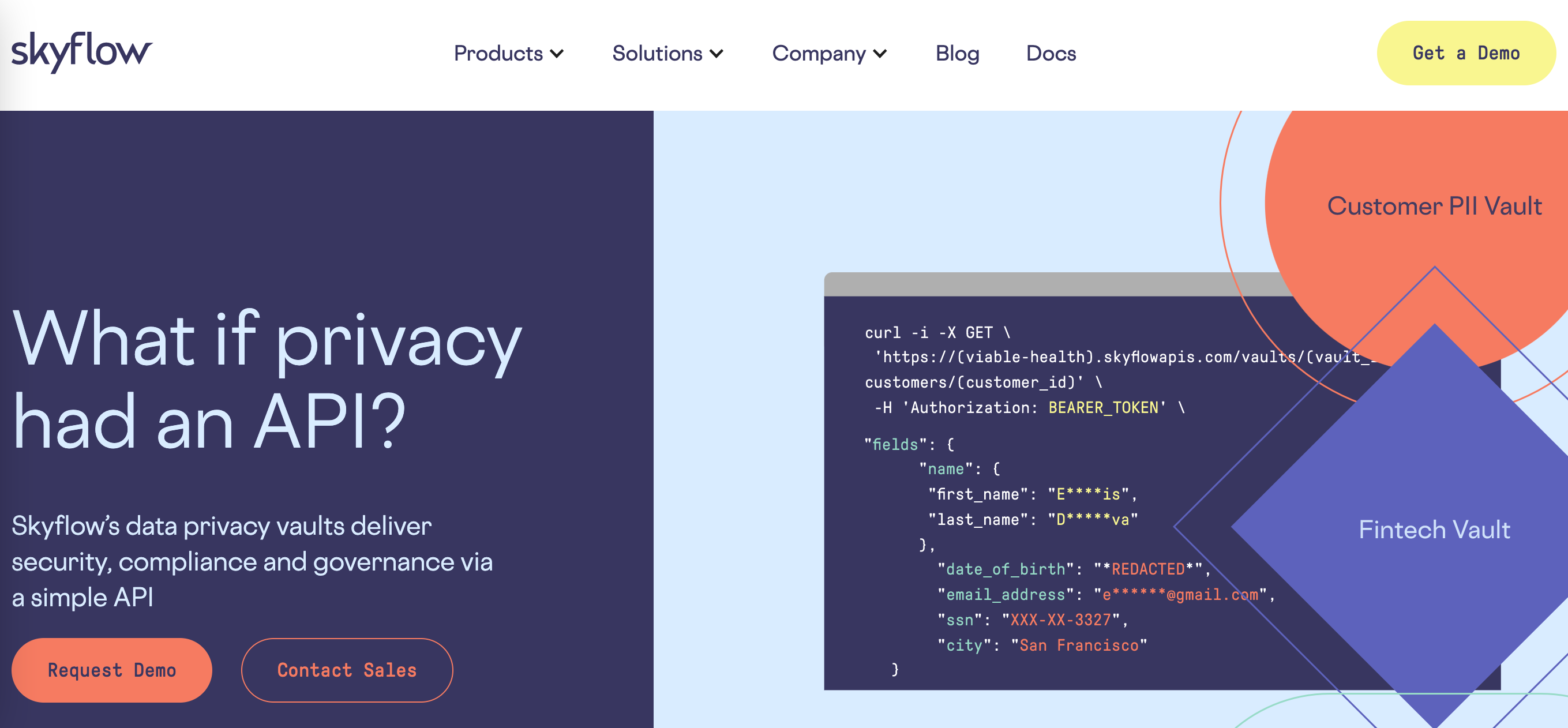

Goalry is a unified “Money Mall” experience that converges personal finance management (PFM) with shopping to help members reach goals in one immersive space.

Features

Everything to achieve goals and comparison shop with a single login

Virtual real estate for embedded tech

Interactive and future-proof design

Why it’s great

Goalry’s platform improves the customer journey by providing a full funnel experience for everything finance and shopping in one virtual, immersive space.

Presenter

Ethan Taub, CEO & Founder Taub has 20 years of executive experience ranging from billion-dollar brands to startups. His mission is to unify a disconnected finance landscape to create efficiencies. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

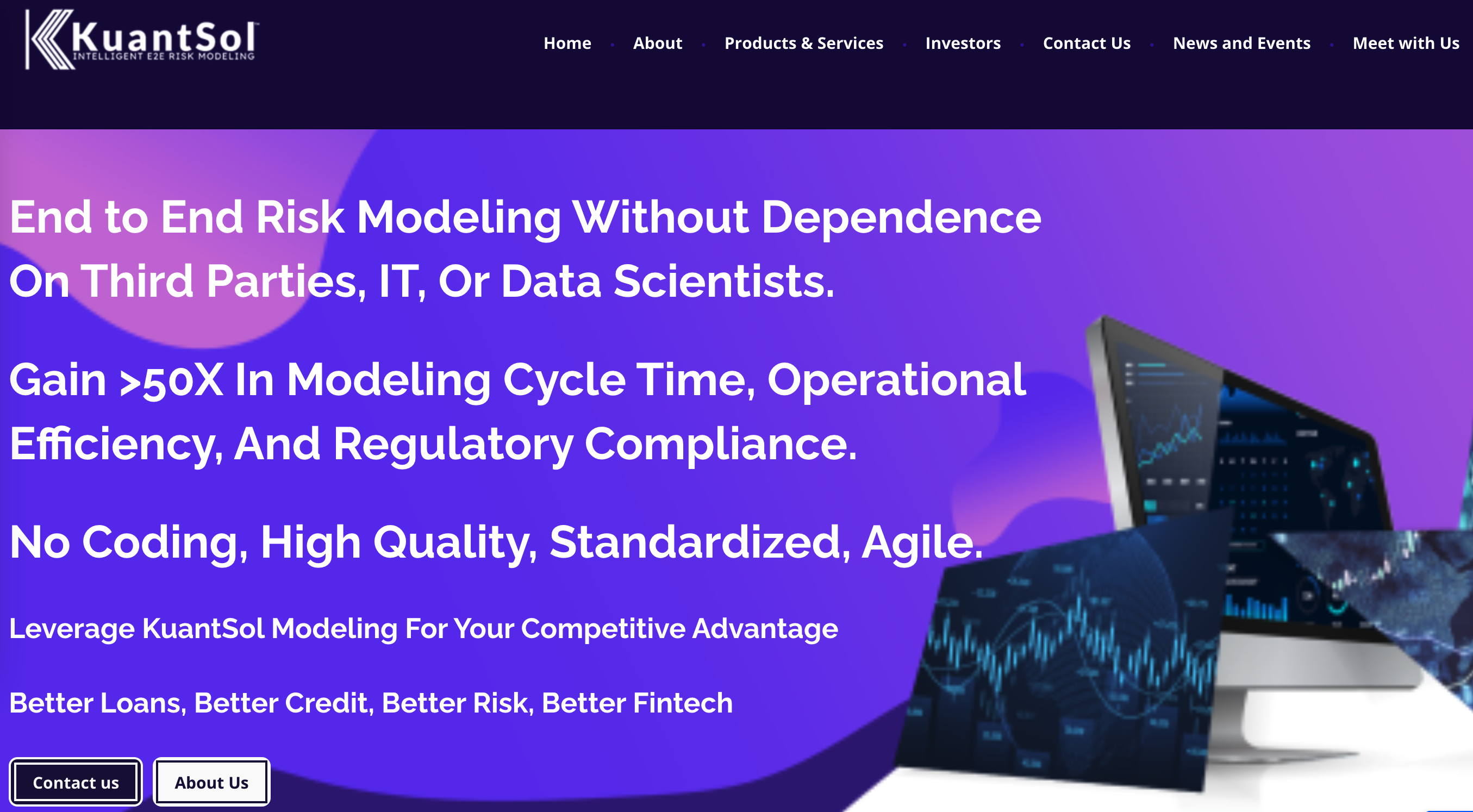

KuantSolEnterprise SaaS democratizes end-to-end modeling for banking, financials, and fintech. KuantSol drives more than 50X gain in operational efficiency, modeling time, quality, and compliance.

Features

Offers E2E modeling, validation, and compliance without dependence on data scientists, IT, and third-parties

Reduces cycle time from months to days

Reduces costs and resource requirements by more than 25X

Why it’s great

The first end-to-end risk modeling technology that is a one-stop shop for all time series and machine learning modeling that shortens cycle time and costs by more than 50X.

Presenters

Alex Shahidi, CEO & Co-Founder Shahidi is the Co-Founder of KuantSo and is a founder or member of five startups with two exits. He is a pioneer in SaaS and cloud technologies, author of papers and patents on data protection, transformation, and infrastructure. LinkedIn

Aytekin Oldac, Co-Founder & Chair of Board Co-Founder of KuantSol, a businessman, and founder of a health services provider, Aytekin is an investor of Code2 and Pyramos software. He has previously served with PwC and IBM Cloud and compliance. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

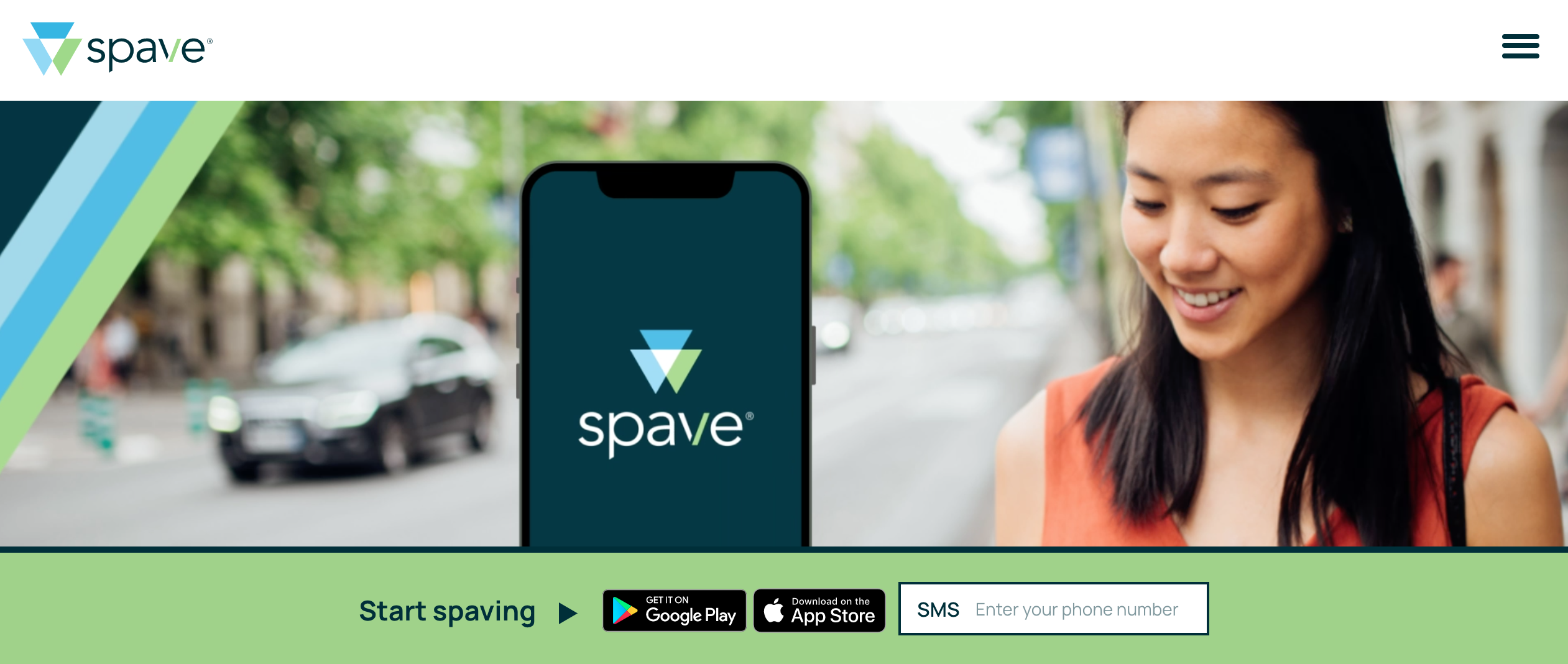

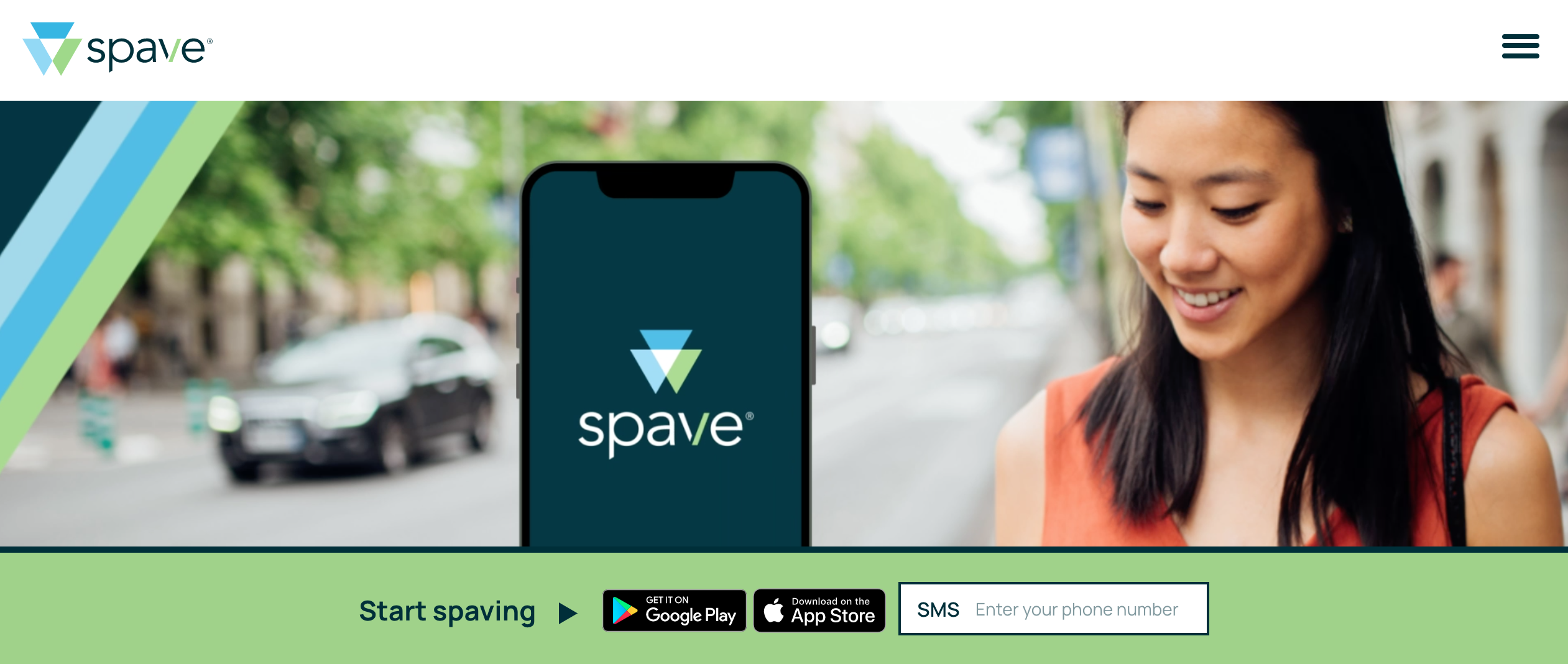

Spave lets users tap into everyday purchases to increase their savings, give to causes that matter to them, and have control and confidence in their finances. Spave transforms your spending, for good.

Features

We have a patent-pending engine that allows users to choose where they direct their spavings

Access to more than 1.5 million accredited U.S. nonprofits

Partners gain access to user insights

Why it’s great

Spave can help CUs empower their members to save more, give more, and live more by breaking down the barriers that hold them back. Empower your members to transform spending for good.

Presenters

Susan Langer, CEO Three words best describe Langer: Observer. Planner. Connector. Langer is a life-long learner and lover of people. Her 30-year professional journey within financial services, marketing and advertising, international development, and non-profit industries has taught her the value of listening to understand, the significance of appreciating others’ differences, and the extraordinary power of collaboration. LinkedIn

Sarah York, Chief Marketing & Digital Officer York is an active advocate for inclusive entrepreneurship and financial literacy. Her expertise spans data-driven growth, digital technology platforms, as well as global digital strategy. LinkedIn

Christen Wright, Head of Product Wright is a seasoned product leader, leading product for Reseda Group, a CUSO of MSUFCU. He has contributed to experiences at Delta, AT&T, and Best Buy. He was in 100 Black Men of Atlanta in 2020. LinkedIn

The investment includes $115 in debt funding and $60 in equity funding.

Wagestream will use the funds to add to its product lineup and fuel its U.S. expansion.

Earned wage access tool Wagestreamlanded $175 million in combined debt and equity funding today. The Series C round, which brought $115 in debt and $60 in equity, boosts the U.K.-based company to a total of $254 million in total funding.

New investors in the round include Smash Capital, BlackRock Innovation and Growth Trust, and Silicon Valley Bank. Existing investors Northzone, Balderton, QED, LocalGlobe, XYZ, Village Global, and Fair By Design also contributed.

Founded in 2018, Wagestream has offered one million workers access to $4.7 billion in wages that they’ve earned. The company considers one measure of its success as capital raised to liquidity released. Wagestream estimates that, prior to today’s investment, the company’s ratio was 1:55. That is, for every $1 of capital it raised, it released $55 of capital. “We’re aiming for a ratio of 1:100, meaning every $1 of capital raised by Wagestream will unlock $100 of impact for frontline workers,” said Wagestream Co-founders Peter Briffett and Portman Wills.

In addition to making that ratio possible, today’s investment will also power the development of new services, including an insurance offering that automatically adjusts coverage and premium, an app that enrolls users into optimal energy plans, fair credit without the need for a traditional credit score, and an intelligent savings installment plan.

Wagestream will also leverage the investment to expand internationally. Specifically, the company will focus on serving U.S. users. To fuel this move, Wagestream recently opened its U.S. headquarters in Washington, D.C.

Payment-card-as-a-service startup Deserveannounced it can now empower its banks and B2B clients via a new tool, the Commercial Card Platform, that enables customers to add a commercial payment card offering to their product lineup.

“We are extending our digital, cloud-native, mobile-first platform from consumer cards to commercial,” said Deserve CEO and Cofounder Kalpesh Kapadia. “With this, we will enable any financial institution or platform that serves other businesses to embed and issue commercial credit cards. For non-banks, this can be a significant source of revenue and can enhance brand loyalty. Our platform will enable those who serve small and medium-size businesses and corporations to offer true credit combined with sophisticated expense management.”

Formerly known as SelfScore, Deserve has re-imagined traditional credit cards by transforming the application and onboarding processes, as well as the credit card itself by bringing them into the digital-first era. The company enables businesses to provide a white-labeled or co-branded card program made possible via a set of configurable APIs and SDKs.

The new Commercial Credit Card product helps companies, banks, and online lenders offer a white-labeled or co-branded credit card product for their business customers. The full-service card product offering will include underwriting, instant virtual card issuance, digital wallet provisioning, and enterprise controls that will enable management to track, manage, and understand business expenses.

Customers Bank, which is headquartered in Pennsylvania and counts $19.6 billion in assets, will be the first bank on Deserve’s Commercial Card Platform. “Together with Deserve, we are looking forward to offering an exciting and valuable product to our small business customers, combining credit with powerful expense management,” said Customers Bank President and CEO Sam Sidhu.

Founded in 2013, Deserve raised an undisclosed amount of funding from Visa last fall, adding to the company’s $287 million in total funding. Among Deserves investors are Mastercard, Goldman Sachs Asset Management, Sallie Mae, Ally Ventures, Visa, Accel, Pelion Venture Partners, Aspect Ventures, and Mission Holdings.

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

EG3C’s Financial Wellness Center helps credit unions build financial literacy with their members and community through interactive, educational content delivered via website, mobile app, API, or SDK.

Features

Created by a credit union for credit unions

Offers content that can be private-labeled and customized

Provides access to user data and dashboard, and CMS to supplement with your own content

Why it’s great

Creating good educational content is very time consuming. By leveraging EG3C’s Financial Wellness Center, employees can spend more valuable time engaging with members and the community.

Presenters

Ben Maxim, CTO at Reseda Group and VP Digital Strategy & Innovation at MSUFCU Maxim serves in a dual role as Vice President of Digital Strategy and Innovation for MSUFCU and as Chief Technology Officer for MSUFCU’s wholly-owned CUSO Reseda Group and its subsidiary companies. LinkedIn

April Clobes, President & CEO at MSUFCU and CEO of Reseda Group Clobes is President & CEO at MSU Federal Credit Union and CEO of Reseda Group, MSUFCU’s wholly owned CUSO. She has established MSUFCU as a leader in innovation in the CU space. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

ToroAlerts‘ fintech app removes emotions from trading by bringing Wall Street technology to Main Street with accuracy and precision using ML and AI with predictive analytics.

Features

Risk management tool for crypto

Easy tool for alternate investment

Crowd-sourced verified intelligence

Why it’s great

The performance from our fully automated algorithmic trading software is unforgettable. Our 2021 portfolio returns include:

Cannabis – 147%

Crypto – 876%

Options – 120% (YTD)

S&P500 – 47% (5yr avg)

Presenters

Rohit Srivastava, Chief Visionary Officer A math and quantitative analysis geek combined with advanced technological experience with an in-depth knowledge of investments and trading has led Srivastava to innovate and build “Smart Frequency Trading.” LinkedIn

Josh Kincaid, CMO Kincaid is the Chief Marketing Officer at ToroAlerts. In his spare time, he produces a cannabis business podcast called The Talking Hedge and hosts “Interviewing CEOs” for Seeking Alpha. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

Buddy’s industry-transforming Insurance Gateway is the simplest way for software companies to manage and sell insurance products to customers.

Features

Offers a single, forward-compatible gateway connection allows customers to source, connect, transact, fulfill, and analyze any type of insurance

Ability to add or swap insurance products without writing new code

Why it’s great

A simpler, faster connection enables businesses to better match their customers and users with the right insurance products, increasing conversion rates. Let Buddy handle all the insurance-y stuff.

Presenter

Charles Merritt, CEO & Co-Founder Buddy Co-Founder+CEO Charles Merritt is an experienced marketer, strategist, and innovator. He held leadership roles in online travel, fintech, and consulting before launching insurtech Buddy in 2018. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

Prelim is a no-code platform to automate the customer experience for banking. The company’s commercial real estate application is the first in the market to automate commercial lending at the point-of-sale.

Features

Reduce loan manufacturing turn-times by using the latest APIs to verify data at the point-of-sale

Offer a first-class customer experience

Decrease loan manufacturing costs

Why it’s great

Commercial real estate lending automation using Prelim’s platform and APIs is the future of lending.

Presenters

Heang Chan, CEO Heang Chan is the Co-Founder and Chief Executive Officer of Prelim. LinkedIn

Sam Kim, Head of Banking Platform Sam Kim is the Head of Banking Platform at Prelim. LinkedIn

Many systems for managing the document life-cycle process could be more efficient.

Banks and financial technology (fintech) companies commonly use document life-cycle management solutions to make their back-office functions run more smoothly. To take full advantage of these systems, organizations must be able to transform documents into a format they can work with.

However, this crucial first step in the process remains cumbersome for many organizations. Even after documents are in the system, organizations need to be able to do more than view them. “The key to managing back-office tasks more efficiently is capturing and extracting data from documents without bogging employees down with manual processes,” said Tracy Schlabach, Director of Marketing at Accusoft. The ability to work with documents and their data can help organizations realize the full efficiency of a comprehensive document management solution.

Identity expert SailPoint is making waves this week. The Texas-based company has agreed to be acquired by private equity firm Thoma Bravo.

The all-cash deal, which values SailPoint at $6.9 million, will take the company private. SailPoint debuted on the New York Stock Exchange under the ticker SAIL in 2017. As part of the transaction, SailPoint stockholders will receive $65.25 per share, which represents a premium of 48% to the company’s 90-day volume-weighted average price.

SailPoint cited multiple benefits of the new arrangement. As a private firm, the company will have increased flexibility and resources to provide identity security solutions. Additionally, SailPoint can now tap into Thoma Bravo’s operating capabilities, capital support, and software expertise. “The transaction will also allow us to pursue our long-term growth trajectory with greater flexibility and effectiveness to support our customers, expand our markets, and accelerate innovation in identity security with the backing of a strong financial partner with deep sector expertise,” said SailPoint Founder and CEO Mark McClain.

The deal comes at a time of increased interest in cybersecurity. Because many employees are still working at home after the pandemic, fraudulent attackers are taking advantage of increased security vulnerabilities. Additionally, experts have warned of potential cyber threats arising from the Russia-Ukraine war.

“SailPoint is ideally positioned to capitalize on the large and growing demand from modern enterprises for robust identity security solutions that secure their business and reduce risk,” said Thoma Bravo Managing Partner Seth Boro. “Their market-leading identity security platform provides the autonomous and intelligent approach that the market requires today, especially among larger enterprises and as hybrid working becomes more common.”

The transaction is expected to close in the second half of 2022.

Solarisbank Launches Women’s Network to Fight Fintech’s Gender Gap

As part of an effort to close the gender gap in the fintech industry, Berlin, Germany-based banking-as-a-service platform Solarisbank has launched a new “women’s network” called Futura. Part of the company’s holistic Nature, People, Business (NPB) framework, Futura is currently organizing events such as discussion panels and training sessions for women looking to enter the fintech industry.

Futura also has a “heal thyself” component. The company has overhauled its recruitment process to be more inclusive, changing language and encouraging recruitment agencies to reach out to more female applicants. Solarisbank has pledged to reach at least 30% female representation by 2024.

“At Solarisbank, we decided to take a deliberate stand to improve gender equity in our industry,” Futura initiator and VP of Onboarding and Integration, Alex Gessner said. “We launched Futura to make fintech more inclusive for everyone – women, men, and non-binary people. It’s encouraging to see so much support for our initiative, and the market response to our first activities has shown the need for such a network.”

German fintech Express Group raises €25m in Series A funding

Express Group, a Hamburg, Germany-based startup dedicated to making tax preparation easier for working and middle class families, has secured $27 million (€25 million) in Series A funding. The investment round was led by Insight Partners and Project A Ventures. The funds will be used to help grow Express Group’s business internationally as well as to fuel future product launches.

ExpressSteur, the initial product from Express Group, leverages AI to enable accounting companies, tax consultants, and lawyers to process tax cases in minutes. The solution brings machine learning and automation to a process that is typically manually-dominated, making the tax preparation process easier, faster, and more accurate. The product helped the company grow to a Gross Merchandise Value (GMV) run rate of more than $49 million (€45 million) in less than 12 months.

Express Group was founded in 2019 by Maximilian Lambsdorff, Dennis Konrad, Konstantin Loebner, Mehdi Afridi, and Andreas Santoro.

New partnership marries recurring payments and subscription management

Dutch payment processor Mollie has announced a collaboration with U.S.-based subscription management platform Recharge that will offer an end-to-end, one-stop solution for managing recurring payments and subscriptions. The partnership will make it easy for users to leverage Recharge’s APIs to integrate recurring payments into Magento, WooCommerce, or other standalone webshop. The integration will also support deploying and managing subscriptions, as well as offer a retention suite to automatically retry payments in the event of failure, an enhanced self-serve customer experience with personalized transactional notifications, and real-time insights into revenues, customers, and subscriptions.

“We’re really excited to be able to offer merchants the opportunity to implement fully powered subscriptions with Recharge easily,” Mollie CCO Ken Serdons said. “Seamless effortless payments brought to recurring ecommerce means an increase in lifetime value and average order value, and at a time of unprecedented ecommerce growth and ambition, we’re able to meet and surpass customer expectations.”

Headquartered in Amsterdam, Mollie is one of Europe’s fastest-growing payment service providers (PSPs). Founded in 2004, the company this year has forged partnerships with WooCommerce and carmaker Mazda. Mollie launched its SaaS payment platform in March.

Recharge was founded in 2014 by Oisin O’Connor (CEO) and Mike Flynn (CTO). Today, the company powers subscriptions for more than 15,000 merchants serving 50 million subscribers, and has processed more than $10 billion in transactions. In May of last year, the Santa Monica, California-based firm secured a Series B investment of $277 million in growth capital, giving the company a valuation of $2.1 billion.

Here is our look at fintech innovation around the world.