This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

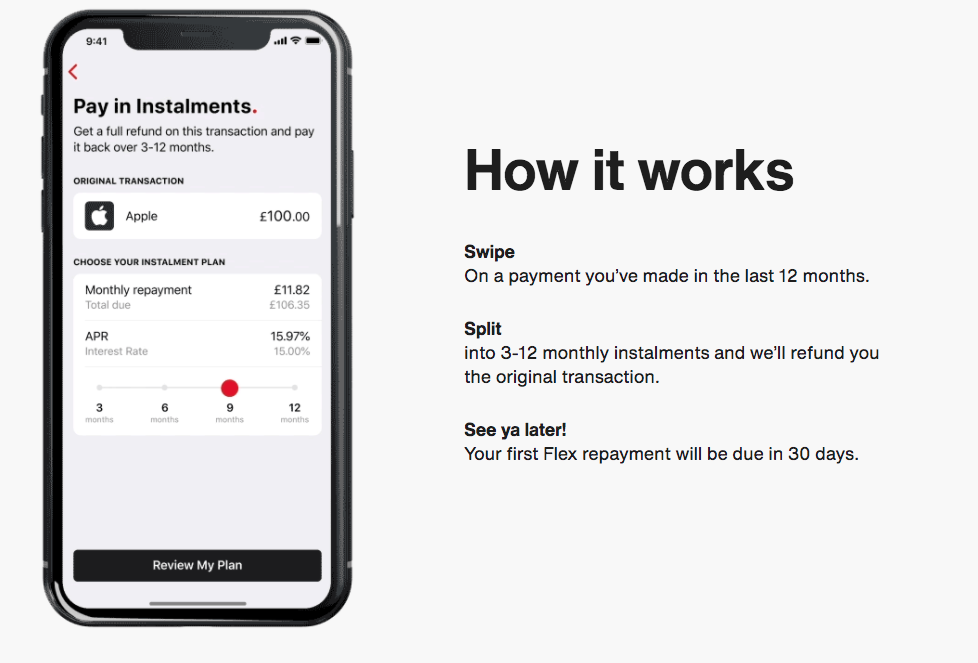

Curve, a U.K.-based payment card technology company, announced its own version of a buy now, pay later (BNPL) product this week.

The company is known for its unique payment solutions, such as its Go Back in Time feature that lets consumers switch payments from one card to another for up to 90 days after the transaction was made. Today, Curve is launching Curve Flex, a tool that builds on Go Back in Time.

Curve Flex allows consumers to convert almost any purchase from the past 12 months into an installment plan, as long as the card they used is linked in the Curve Platform. After the customer makes a purchase, all they need to do is swipe the transaction and select the number of installments. Then, Curve refunds their transaction in full almost instantly.

Unlike most BNPL tools, Curve Flex isn’t limited to specific merchants, cards, or products. It can be used on retail purchases, online orders, household bills, and more. Also unlike many BNPL tools, Curve’s offering charges interest based on the purchase amount and the number of installments.

“Curve is giving customers the unprecedented ability to convert transactions made up to a year ago into free or low-interest installment loans,” said Head of Curve Credit Paul Harrald. “Being able to Go Back in Time and Pay Later is going to forever change how U.K. customers think about managing their personal finances and cashflow.”

Curve Flex, which has been in beta for a year, already has 1,600 users that have opted to pay later on 7,000 transactions worth over $1.4 million (£1 million).

Earlier this week we celebrated the return to in-person events with FinovateFall. Though this year’s event felt a bit different from years past, with vaccination wristbands and social distancing replacing handshakes and hugs, there was an undeniable energy present. While it was wonderful to see many familiar people face-to-face, it was also refreshing to see new ideas and technology presented by the experts themselves.

With three days of demos, panels, keynotes, and networking, there was a lot to take in. Whether you attended in person or digitally, you were able to see some of the newest ideas and technology in banking and finance. And if you weren’t able to attend this time around, here’s a recap of what you saw and what you may have missed.

Overarching themes

Consumers have changed how they choose their bank. This one seems like a theme we’ve been hearing for a couple of years now, but I think it is becoming even more concrete as the move to digital is ever-accelerating. The anecdote I heard multiple times was how consumers used to base their banking relationship on which FI had the closest branch or the most ATMs in their region. Today, with the abundance of neobanks, consumers have a different mindset. They choose their banks based on the brand. Does it appear trustworthy and transparent, or is there too much fine print? Does it offer unique features such as early wage access that speak to the customer’s needs? Does it benefit the community? Does it speak to the unique needs of the customer’s tribe?

Cybersecurity should still be top-of-mind. The cybersecurity and fraud prevention theme is one that has been around since the dawn of fintech. It is also one that isn’t going away any time soon. With the push to digital, fraudsters are finding increased profits. At this week’s event, we saw multiple fintechs looking to stem the flow of cash into criminals’ pockets.

Regtech is rising. The U.S. has been slow to adopt existing regtech tools and create new ones. However, we’ve seen an increase in regulation around consumer data and customer communication. Not only that, but new technologies are also bringing pending regulation around AI, smart contracts, and cryptocurrencies. Fintech is here to fill the dearth of regtech solutions and save financial services companies and fintech alike from legal headaches.

Consumers are ready for self-service. We now live in a world where people no longer want to make a phone call to order a pizza, but would rather do so via an app. On top of this mobile-first preference, consumers also expect things on-demand. For these reasons, the chatbots that were dismissed in years past as a solution-looking-for-a-problem. At this week’s conference, however, we heard that chatbots are now some of the most practical tools FIs can implement to best serve their clients.

My highlight

My favorite session was the Investor All Star panel featuring Alexa Von Tobel, Founder and Managing Partner of Inspired Capital, and Matt Harris, Partner at Bain Capital Ventures. The two discussed the new “creator economy,” a sub sector of the gig economy that represents not just social media influencers, but anyone who monetizes content online.

Harris pointed out that, in general, relatively little money trickles down to creators such as musicians and artists because much of the funds are gobbled up by middlemen such as studios, auction houses, galleries, and publishing companies. However, with the advent of NFTs it is now possible for any artist to directly reap the rewards of their labor using only an NFT Marketplace.

Von Tobel added that banks need to be ready to serve the unique needs of this new workforce, many of which are Gen Z, that wants to ditch traditional jobs to work for themselves.

Hints at what to expect for 2022

We’ll see more no code and low code solutions. At FinovateFall this year, it was obvious that the no code movement is having a moment. It democratizes the internet, making it easy for almost anyone to launch a new tool, product, solution, or even an entire business. Competition in this arena has been slowly heating up for years and next year we can expect it to explode.

There will be more chat bots and AI-enabled help channels. With all of the mentions of self-service technology that pulsed throughout this week’s conference, it became clear that the chatbot movement isn’t just a passing fad. Given this, combined with the difficulty of creating self-service tools that actually meet customers’ needs, we can expect to see more, smarter chat bots and a wider variety of self-service tools.

This was Finovate’s last event for the year. Keep an eye out for updates on our conference roster for next year, including:

SellersFundinglanded $166.5 million in Series A debt and equity funding this week. The company, which provides working capital to ecommerce marketplaces, now has almost $275 million in total debt and equity funding.

The investment was led by Northzone with additional investments from Endeavor Catalyst and Fasanara.

Founded in 2017, SellersFunding offers working capital solutions, payments tools, and analytics to help online marketplace sellers unlock capital, access invoice payments faster, collect payments, manage taxes, and more.

The New York-based company will use the financing to enhance its technology and payments platforms, grow its team, boost sales and marketing efforts, and fuel both domestic and international expansion. SellersFunding plans to gain more clients not only in the U.S. but also in the U.K., Europe, and Australia.

“We are thrilled to complete our capital raise and have Northzone and Endeavor joining our company, and to see the renewed commitment of Fasanara in supporting the expansion of our portfolio,” said SellersFunding CEO Ricardo Pero. “This underscores our dedication to providing world-class financial solutions for our clients and partners and is a testament to the overall growth of the global ecommerce space.”

Today we’re busting out the virtual confetti to announce the winners of the 2021 Finovate Awards, recognizing excellence in fintech across 25 different categories. This is the third annual Finovate Awards competition, which aims to highlight strong work done by the companies who are driving fintech innovation forward and the individuals who are bringing new ideas to life.

We may not get to congratulate the award winners with handshakes this year, but that doesn’t make the accomplishments any less compelling. These companies and individuals have proven that they have what it takes to capture the attention of the fintech world through standout products, services, and overall excellence.

Judges for the awards include media analysts, board members, bankers, fintech founders, and more. Each were given the difficult task of taking a record number of nominations and distilling them down to just a single winner in each category.

Best Alternative Investments Platform: Pipe

Best Back-Office / Core Service Provider: MANTL

Best Consumer Lending Platform: Salary Finance

Best Customer Experience Solution: TMRW by UOB

Best Digital Bank: Oxygen

Best Digital Mortgage Platform: LendingHome

Best Embedded Finance Solution: ApexEdge

Best Enterprise Payments Solution: GoCardless

Best Financial Mobile App: Simplifi by Quicken

Best Fintech Accelerator/Incubator: Financial Solutions Lab

Best Fintech Partnership: T-Mobile and BM Technologies

Best ID Management Solution: IDology

Best Insurtech Solution: FloodFlash

Best Mobile Payments Solution: Simpl

Best RegTech Solution: Featurespace

Best SMB/SME Banking Solution: Ramp

Best Use of AI/ML: Zest AI

Best Wealth Management Solution: Charles Schwab

Excellence in Financial Inclusion: Airtel Money

Excellence in Pandemic Response: Biz2Credit

Excellence in Sustainability: BlocPower

Executive of the Year: Barbara Morgan, FIS

Fintech Woman of the Year: Jo Ann Barefoot

Innovator of the Year: Jon Schlossberg

Top Emerging Tech Company: Synctera

While only one company can win each category, it’s also worth recognizing the quality of all of the finalists who made it to the last stage in the process.

We owe a huge thank you to the panel of judges, followers, and everyone who took the time to submit a nomination. Congratulations to the winners!

Credit and risk underwriting firm TransUnion announced plans today to acquire digital identity solutions company Neustar. The deal is expected to close in the fourth quarter of this year for $3.1 billion.

“The credit information and analytics that TransUnion provides make trust possible between consumers and businesses,” said TransUnion President and CEO Chris Cartwright. “As digital commerce continues to grow globally, TransUnion’s powerful digital identity assets, enhanced by Neustar’s distinctive data and digital resolution capabilities, will enable safer and more personalized online experiences for consumers and businesses.”

With the addition of Neustar’s data and analytics to enable consumers and businesses to transact online with greater confidence, TransUnion expects the purchase will expand its digital identity capabilities.

Specifically, TransUnion’s acquisition is expected to help the company break out of the traditional credit scoring space by leveraging Neustar’s OneID platform, which will help TransUnion unify its digital identity capabilities. This includes TLO data assets and fusion platform, the iovation device reputation network, and the digital marketing capabilities of Tru Optik.

As part of the purchase, TransUnion will acquire Neustar’s employees, data, and products.

We have 70+ demo companies at this year’s FinovateFall event, taking place September 13 through 15 online and in-person in New York City. These demos, combined with a full lineup of keynotes and panel discussions, will bring a wide variety of themes. To get an idea of what’s trending this year, we’re taking a look at the key themes repeated throughout both the demos and the discussions.

For the demos, we’ve distilled the themes into five major categories, as outlined below.

Data

Today’s data discussions transcend the conversations of Big Data that were en vogue in 2015. This year, data is everywhere; it touches everything. Companies will be looking at how they can help gather, clean, and analyze data; how they can place the customer in charge of their own data while allowing the firm to leverage consumer data; and how they can collaborate with others around data. They will also be discussing specific use cases such as receipt data and pulling data from paper documents. At this year’s event, seemingly everything is data-driven.

Fraud prevention & compliance

We can expect to see solutions to prevent financial crime at pretty much every event. Fraud is ubiquitous in financial services because bad actors consistently benefit from it. This fintech sub-sector is continuously evolving as hackers become more and more cunning. And this year, we’ve noticed the addition of more compliance tools to assist with regulations and audits around fraud.

Digital assistant

With the Delta variant in full force, we still have not entered a post-COVID world. Given that our social distancing habits must persist, companies are investing more energy in developing digital assistants. No matter how you may feel about chatbots, they have proven to be a viable way to communicate with clients when in person discussions are no longer an option. And this theme goes beyond chatbots. Digital assistants including AI-powered call centers and automated customer interactions of all types are rising up to help take the burden off of customer service agents during a time when in-branch conversations are not possible.

Customer engagement

Another byproduct of COVID’s aftermath, customer engagement technologies continue to be front-and-center on the minds of banks, fintechs, and (of course) consumers alike. Because so much of our lives currently takes place online, customers now expect an engaging, personalized customer experience.

One of the ways financial firms are tackling this challenge is by creating a gamified user experience. By taking wha typically is viewed as a chore and making it into something fun, customers are more likely to use and return to an app or an online experience.

Another key to customer engagement is, of course, personalization. By leveraging data to center the user experience around the customer’s needs, fintechs and banks can ensure to captivate their existing client base and reign in new ones.

Financial planning and investing

The roboadvisor craze of 2015 has matured, and has left a number of powerful fintechs in its wake. This is thanks to increased popularity combined with enabling technologies of the new decade. Unlike the first wave of roboadvisory tools, today’s offerings tend to take a more holistic and personalized approach. At this year’s event, we’ll see tools that look at consumers’ financial wellness as a whole, not just their retirement savings.

Another difference from early wealthtech tools is that more of today’s offerings are B2B instead of strictly B2C. At FinovateFall 2021, we’ll see tools that help advisors create more value for their clients and products for employers to help their workforce build better financial health.

What’s missing?

Notably absent from this list are two major themes I would have expected to see. The first is Buy Now, Pay Later (BNPL), the payment technology that allows customers to pay for purchases in installments after receiving the product. Companies like Afterpay, Affirm, Klarna, and Sezzle have popularized BNPL, and many retailers and payment companies alike have implemented various versions of this model. Given the seemingly viral nature of BNPL, it’s surprising that only a single demo company, Zeta, offers BNPL technology.

The second missing piece this year is AI, which has been a top trend for years. So how can discussions of such a pervasive theme be so absent? The answer is in the question; AI is so pervasive that it has now become table stakes for every fintech sub-sector. In other words, AI has blended into the background. If firms want to compete and offer worthwhile products and services, they must, at a minimum, be leveraging AI.

FinovateFall won’t just be about the demos. We have an impressive lineup of keynote speakers, panelists, and fireside chats to share a range of perspectives on today’s hottest fintech topics. While you’re at the event, keep an eye out for the following themes:

Cybersecurity & financial crime

Neobanks

ESG

Financial inclusion

Leadership

Automation

Open finance

Wealth management

Digital transformation

Cryptocurrency

Faster payments

Customer experience

We’re so excited to return to New York this year! We’ll see you either online or in person starting September 13 at 8 a.m. Eastern time and continuing through the 15th. Book your tickets here.

Founded in 2015, CipherTrace offers security and fraud monitoring activities for clients’ crypto-related programs. As CipherTrace CEO Dave Jevans states it, the company helps “banks or cryptocurrency exchanges, government regulators or law enforcement to keep the crypto economy safe.”

Mastercard will combine CipherTrace, which offers insights into more than 900 cryptocurrencies, with its own cyber security solutions to provide customers “the same trust and peace of mind that consumers currently experience with more traditional payment methods.”

CipherTrace’s solutions will help Mastercard differentiate its card and payments offerings and help the company’s clients protect their own clients, comply with regulations, and build their own digital asset products. Additionally, Mastercard’s purchase will help the payments company increase its presence with new clients such as fintechs, crypto-wallet providers, and governments.

“Digital assets have the potential to reimagine commerce, from everyday acts like paying and getting paid to transforming economies, making them more inclusive and efficient,” said Mastercard President of Cyber & Intelligence Ajay Bhalla. “With the rapid growth of the digital asset ecosystem comes the need to ensure it is trusted and safe. Our aim is to build upon the complementary capabilities of Mastercard and CipherTrace to do just this.”

Today’s move isn’t Mastercard’s first foray into the crypto realm. The New York-based company already holds partnerships with Uphold, Gemini, and BitPay to create crypto cards; has created tools support CBDCs; and has launched programs to support blockchain technology, NFTs, and stablecoins on its network.

Mortgagetech company Better.com announced today it has acquiredProperty Partner, a U.K.-based property investment company, for an undisclosed amount.

Property Partner is a property crowdfunding investment platform that offers users fractional ownership of rental property homes. The company’s investors can select a diversified portfolio of properties to own and receive monthly rental income from those properties that is paid out as a dividend. Since it was founded in 2014, Property Partner has raised $35.2 million and accumulated $194 million (£140 million) in assets under management from its 9,000 users.

“Combining Property Partner’s unique residential property investment platform with Better’s arsenal of homeownership products and services changes the game for the future of real estate investment,” said Better Founder and CEO Vishal Garg. “We’re turning residential real estate into a liquid asset class and changing how families can grow their wealth. Together, we will lower costs, improve convenience, and deliver huge value to all real estate market participants.”

This marks the second U.K.-based company that Better has acquired this summer. In July, the New York-based company bought Trussle, a digital mortgage brokerage company based in London. Both of these moves hint at Better’s potential plans for international expansion. The company currently offers mortgages in 46 U.S. states and Washington, D.C.

Today’s deal comes ahead of the company’s planned SPAC merger, which is expected to close in the fourth quarter of this year, with Aurora Acquisitions Corporation. The deal will value Better at $7.7 billion.

Founded in 2016, Better offers mortgages for home purchases and refinances, real estate agents, title insurance, and mortgage insurance. The company has funded $30.9 billion in home loans and provided over $7 billion in coverage through its insurance products.

Last month, Better launched a cash offer program that allows a customer to buy a home using cash. Better purchases the home on a customer’s behalf, then finalizes the customer’s mortgage after the deal has closed. The buyer can move in as soon as Better finalizes the purchase, but pays Better prorated daily rent until their mortgage is approved and they buy back the home from Better.

PayPalannounced plans today to acquire Japan-based Paidy, a payments company with a buy now, pay later (BNPL) offering that facilitates transactions for both merchants and consumers. The deal is expected to close for $27 billion (¥300 billion) in the fourth quarter of this year.

PayPal’s purchase will work alongside its existing ecommerce business in Japan, which is the third largest ecommerce market in the world. Paidy will also expand PayPal’s capabilities, relevancy, and distribution in Japan’s domestic payments market.

“Paidy pioneered buy now, pay later solutions tailored to the Japanese market and quickly grew to become the leading service, developing a sizable two-sided platform of consumers and merchants,” said VP and Head of Japan at PayPal, Peter Kenevan. “Combining Paidy’s brand, capabilities, and talented team with PayPal’s expertise, resources, and global scale will create a strong foundation to accelerate our momentum in this strategically important market.”

Paidy was founded in 2008 and enables its six million registered users to make purchases online without the use of a debit or credit card. Instead, Paidy operates on a BNPL model by billing customers for all purchases at the end of each month. Payments can be made via bank transfer or in-person using cash at a convenience store.

This model works not only for ecommerce purchases, but also for brick-and-mortar transactions. The company’s Paidy Link tool was launched earlier this year and allows customers to link digital wallets, including PayPal, to make purchases using the digital wallet but make payment via Paidy. For PayPal, Paidy’s model that circumvents credit and debit card rails is a good thing. It enables PayPal to own the payment flow (and the revenue that comes with it).

“Paidy is just at the beginning of our journey and joining PayPal will accelerate our plans to expand beyond ecommerce and build unique services as the new shopping standard,” said Paidy President and CEO Riku Sugie. “PayPal was a founding partner for Paidy Link and we look forward to working together to create even more value.”

Sugie, along with Paidy Founder and Executive Chairman Russell Cummer, will continue to lead Paidy, which will continue to operate and maintain the brand.

Paidy marks PayPal’s 23rd acquisition, following Honey in 2019 and Curv and Happy Returns in 2021. The purchase of Paidy, with its BNPL capabilities, hints at PayPal’s evolution into becoming more of a holistic shopping platform.

Even though super apps aren’t common in the U.S. or Europe, most everyone in fintech across the globe is familiar with them. Super apps serve as a one-stop shop that allow users to access multiple services from a single place.

In Asia, the hot spot for super apps, users are able to use super apps for everything from ordering groceries to hailing a cab to managing their finances. Apps including WeChat, AliPay, Paytm, and Grab are commonplace across Asia. In fact, WeChat has more than 1.2 billion monthly active users; 78% of people in China between the ages of 16 and 64 are using WeChat.

It is the “super” nature of these apps that makes them so successful; they are a platform and do not just fulfill a single purpose. With a combination of in-house technologies and third party integrations, the apps serve a range of consumer needs. Many super apps began with only a single purpose, accumulated a large number of users, and then began adding new capabilities.

What does it take to become a super app? Starting with a massive user base helps, and providing a range of tools for everyday tasks and activities will help keep those users coming back. Below are 10 common capabilities of successful super apps.

Social

As the popularity of WeChat has proven, social tools are sticky. Building communication, collaboration, and sharing capabilities into an app not only builds a user base, but also creates a community around a brand.

Ecommerce

Shopping is taking place increasingly online, which means that ecommerce purchases are becoming a large part of consumers’ everyday lives.

Food delivery

Everybody needs to eat. And between online grocery orders and takeout meal deliveries, super apps can help users meet this need.

Transportation services

Just as important as having food and online purchases delivered is having the means of getting from one location to another. Included in this category are ride hailing services, car sharing services, and bike or scooter sharing services.

Personal finance

Another one of life’s essentials is managing finances. From budgeting for daily expenses to planning for retirement, banking and finance tools are key components of a super app.

Travel services

Offering travel services, such as travel insurance, concierge services, and rental car discounts, is commonplace for many financial services companies. Super apps offer more robust capabilities, however, such as flight comparison and booking tools, train schedules and ticketing services, and hotel booking capabilities.

Billpay

Paying bills is a regular occurrence for most people, so including utility billpay and a mobile top-up feature will give users yet another reason to log into a super app on a regular basis.

Health services

The healthcare industry is fragmented. So providing health services, such as appointment booking, tele-health calls, records management, general health information, and ask-a-nurse services in a single place provides a lot of value for end users.

Insurance

Similar to the health industry, insurance comes with a lot of moving pieces. Offering a digital lock box with insurance cards, contact information, coverage options, and payment history is a valuable tool that can help keep users organized.

Government and public services

Rounding out the list of life’s necessities in the digital realm are government and public services. Super apps can host social security cards and information, public transportation payment options, and library card information.

Germany-based Rydannounced this week it has received $11.9 million (€10 million) in funding for its technology that allows users to pay for vehicle fuel via their mobile app.

The investment, which marks the first time Ryd has received funding, comes from BP Ventures, the investment arm of British Petroleum. As part of today’s announcement, BP Ventures’ Managing Partner Daniela Proske will join the Ryd board.

Ryd offers a digital payment solution that enables drivers to pay for fuel, electric vehicle charging, and car washes without leaving their vehicle by using the company’s mobile app or with an integration with smart car systems. “This new payment form is much faster, easier, and more comfortable,” said Ryd Founder and Chairman Oliver Goetz, “Ryd is on its way to lead this movement in Europe.”

Goetz called BP “the perfect addition” to the company’s existing network of service stations and added that it completes Ryd’s ecosystem with strategic partners in finance, automotive, and energy sectors.

Ryd plans to use the funding to fuel expansion and deliver digital payment options for BP customers across Europe. The company’s payment technology is currently accepted at 3,000 service stations across seven countries in Europe.

BP will use the strategic relationship to expand its BPme digital fuel payment app into more European countries. The app currently works in the U.K. and the Netherlands. “In-car digital payments are an integral part of the seamless and convenient experience that customers increasingly expect at our retail sites,” said BP SVP of Mobility and Convenience for Europe and Southern Africa Alex Jensen. “Ryd’s technology can help deliver just that, and for an increasing range of services. Our investment and partnership will help BP provide these digital services more widely across Europe, making our customers’ experience easier and more enjoyable.”

The first BP filling stations are expected to go live with Ryd in the fourth quarter of this year.

Insurtech company Blueprint Title recently raised $16 million, bringing its total funding to $24.5 million. Forte Ventures led the Series B round.

Blueprint Title launched in 2017 to tackle title insurance, a type of insurance that protects prospective homeowners from being sued for a claim against the home from before the purchase was finalized. These “clouds” can arise from back taxes, liens, conflicting wills, and other unresolved issues.

The title insurance market in the U.S. is small, however. Blueprint Title CEO Steve Berneman estimates that the market is comprised of four companies with 90% of the market share.

Blueprint Title offers an API that allows customers to search new transaction submissions, pull information about in-process deals, and view real-time updates when there’s a change in title status. Built for secure collaboration, the company’s portal enables document uploads and status updates that keep everyone up-to-date.

Blueprint Title is part of a wave of neoinsurance companies, a term coined by TechCrunch to describe digital-first insurtechs such as Metromile, Roots, and Trov. Blueprint Title’s model is slightly different than these three companies, however, in that it operates on a B2B model instead of marketing directly to consumers. The company’s client base is comprised of real estate investors, lenders, proptech companies, and home builders.

Blueprint Title is currently licensed in 26 states and operating in 19 states.