This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

The company, which made its Finovate debut in 2011, said that the acquisition will help make its technology available to an even wider range of corporate customers worldwide. The deal is the latest evolution of a relationship between Kantox and BNP Paribas that extends back more than three years.

“We have been serving clients together since 2019 when our technology partnership started,” Kantox CEO and co-founder Philippe Gelis said. “During those three years, we spent a lot of time together in the field, getting the opportunity to understand that together we were stronger and able to bring more value to clients.” Gelis called the union “the best of both worlds, the leading software company in the currency management automation category and the leading bank in Europe.”

Kantox offers a single, API-driven, plug-and-play solution that helps companies optimize their FX workflow. Kantox’s technology gives businesses the ability to automate their currency risk management, build better hedging strategies, and lower costs. With its Currency Management Automation, Kantox enables corporate treasurers to deal effectively with challenges ranging from an over-reliance on manual processes to a fragmented FX workflow due to the absence of end-to-end solutions.

Kantox’s technology will be put to work for the Global Markets business of BNP Paribas’ CIB division, and the business centers of the Commercial, Personal, and Banking Services (CPBS) division. Both small businesses and large corporates will be the target markets for Kantox’s currency automation risk management offering.

Among the premier banks in the European Union, BNP Paribas is active in 65 countries and has almost 190,000 employees. The company’s Chief Operating Officer, Head of BNP Paribas CIB, Yann Gérardin called the acquisition another example of the institution’s readiness to “establish long-term partnerships with fintechs in ever-increasing range of areas.”

Kantox made its Finovate debut in 2013 at FinovateEurope. Within ten years, the company surpassed $15 billion in total corporate foreign exchange transactions. Kantox began this year with news that it was partnering with virtual IBAN and corporate account provider Monneo. This spring, Kantox teamed up with London-based fintech Revving to launch an integrated and embedded finance and working capital solution. Kantox raised more than $43 million in funding prior to the this week’s acquisition according to Crunchbase.

“The valuation underscores investors’ confidence in Airwallex’s core business value and fundamentals,” Airwallex CEO and co-founder Jack Zhang said. He added that the market environment going forward remained “challenging in the foreseeable future,” but said the investment would help fuel the company’s objectives with regards to growth, product expansion, and talent acquisition. “By strengthening the breadth of our global reach and product offering, we can better empower our customers to unlock new market opportunities,” Zhang said.

The investment takes Airwallex’s total capital to $900 million. Participating in this week’s funding were existing investors Square Peg, Salesforce Ventures, Sequoia Capital China, Lone Pine Capital, Hermitage Capital, 1835i Ventures, and Tencent. Other investors included Australian superannuation fund, HostPlus, and a pension fund based in North America.

Airwallex’s payments and banking platform helps businesses accept payments, move money around the world, and enhance their financial operations. The company also offers a business account that features global accounts, borderless cards, transfers and foreign exchange, payment links, business expense reconciliation, and integration with accounting platform Xero. Founded in 2015 and headquartered in Melbourne, Australia, Airwallex has enjoyed revenue growth of 184% in the past year and is currently processing nearly $50 billion in annualized transactions.

Named Startup of the Year in the U.S. FinTech Awards and FinTech of the Year at the Asia FinTech Awards, Airwallex announced in August that it was committing an additional HK$2.25 million ($286,650 USD) into its Hong Kong SMEs Initiative. Launched in April, the effort is designed to help small businesses recover from the economic fallout from the COVID pandemic. This latest commitment brings Airwallex’s total support of the initiative to HK$4.5 million ($573,300 USD).

Enthusiasm for cryptocurrencies has settled down from its peak a year ago. But innovation in the space continues undaunted. Today we learned that one of the pioneering companies in digital assets, Coinbase, has forged a strategic partnership with Google Cloud. The partnership calls for Coinbase to use Google Cloud as its strategic cloud provider for developing advanced exchange and data services. Google Cloud’s platform will enable Coinbase to process blockchain data at scale, and boost the international reach of its services courtesy of Google Cloud’s fiber optic network. Coinbase will also benefit from Google Cloud’s secure infrastructure and the company’s data and analytics capabilities.

“We are excited Google Cloud has selected Coinbase to help bring Web3 to a new set of users and provide powerful solutions to developers,” Coinbase CEO and co-founder Brian Armstrong said. “With more than 100 million verified users and 14,500 institutional clients, Coinbase has spent more than a decade building industry-leading products on top of blockchain technology. We could not ask for a better partner to help execute our vision of building a trusted bridge into the Web3 ecosystem.”

The partnership also means that Google Cloud will enable select customers to pay for its cloud services with designated cryptocurrencies. The functionality will be powered by Coinbase Commerce, which provides a decentralized way for merchants around the world to accept cryptocurrency payments. Further, Web3 developers will be able to access Google’s BigQuery crypto public datasets – powered by Coinbase Cloud Nodes – across leading blockchains. This will enable developers to operate Web3-based systems without requiring expensive and unwieldy infrastructure.

Google Cloud CEO Thomas Kurian said the partnership would help make it easier and faster for developers to build Web3. Kurian highlighted the “scalability, reliability, security, and data services available via Google Cloud” which he said would enable developers to “focus on innovation in the Web3 space.” Google also announced that it will use Coinbase Prime for institutional crypto services such as secure custody and reporting.

Coinbase’s partnership news with Google Cloud comes as the cryptocurrency innovator announces that it has secured regulatory approval from the Monetary Authority of Singapore (MAS). The company received its In-Principle Approval (IPA) as a Major Payments Institution license holder, which will enable Coinbase to offer regulated Digital Payment Token products and services in Singapore. It’s worth noting that Coinbase is no stranger to the country. The company introduced the island nation as its technology hub last year. And over the past three years, Coinbase’s venture capital arm, Coinbase Ventures, has invested in more than 15 Singapore-based Web3 startups.

“Today’s announcement underlines our commitment to Singapore as a regional hub that allows us to unlock new capabilities for Singapore-based institutional and corporate clients in the future,” Coinbase’s Nana Murugesan wrote on the company blog this week. “Gaining this in-principle approval from MAS is an important step, as we plan to launch our full suite of retail, institutional, and ecosystem products.”

Coinbase made its Finovate debut in 2014 at FinovateSpring in San Francisco, California. Founded in 2012, the company now enables more than 100 million people and businesses to buy, sell, and manage cryptocurrencies. Coinbase has a quarterly trading volume of $217 billion, and $96 billion in assets on its platform. With partners in more than 100 countries, and 4,900+ employees, Coinbase is a publicly-traded company on the NASDAQ exchange under the ticker COIN and has a market capitalization of $16 billion.

2022 marks the fourth year in a row in which Finovate alums have raised $1 billion or more in equity funding in the third quarter. The number of alums reporting investments in Q3 this year was lower than in previous years, and much of the quarter’s lofty fundraising total comes from a single, sizable investment of $800 million in Klarna.

Also continuing a trend we’ve seen for the past few years is the relatively strong performance of August compared to other months in the third quarter. While more capital was invested our alums in July (again, credit to Klarna), August featured more alums receiving funding than any other month in Q3 this year.

Previous Quarterly Comparisons

Q3 2021: More than $1.1 billion raised by 14 alums

Q3 2020: More than $1.2 billion raised by 14 alums

Q3 2019: More than $1 billion raised by 21 alums

Q3 2018: More than $400 million raised by 19 alums

Q3 2017: More than $1 billion raised by 31 alums

Top Equity Investments for Q3 2022

The top equity investment of the quarter for Finovate alums this year was Klarna’s $800 million fundraising in July. In fact, at nearly 80% of the quarter’s total alum funding haul, Klarna’s investment was significantly larger than combined amount of the other six known alum investments in Q3.

While impressive in this context, the capital infusion did come with a reduction in Klarna’s valuation. According to Reuters, the Swedish e-commerce and payments innovator was valued at $6.7 billion in its July transaction, an 85% drop from its 2021 valuation of $46 billion.

Here is our detailed alum funding report for Q3 2022.

If you are a Finovate alum that raised money in the third quarter of 2022 and do not see your company listed, please drop us a note at [email protected]. We would love to share the good news! Funding received prior to becoming an alum not included.

Financial solutions provider Finastra announced a strategic collaboration with digital trade finance network Contour.

Finastra also announced a partnership with India’s Kotak Mahindra Bank, bringing its Unified Corporate Portal solution to support the institution’s corporate banking portal Kotak FYN.

Formed via a merger between Misys and D+H in 2017, Finastra also recently announced the appointment of Chief People Officer Helen Cook.

Financial solutions company Finastra recently announced a pair of partnerships. The U.K.-based firm, which launched its open platform for innovation FusionFabric.cloud in 2017, has entered a strategic collaboration with digital trade finance network Contour. The collaboration will integrate Finastra’s Fusion Trade Innovation technology with Contour’s platform, boosting access to trade finance and streamlining back-office workflow.

The collaboration helps financial institutions take advantage of the multi-trillion dollar global trade business that both corporate customers and consumer depend upon every day. The partnership between Finastra and Contour will give financial institutions a network that supports collaborative workflows between trading parties. The new integration facilitates digital adoption, lowers costs and reliance on paper, and reduces risk.

“Our partnership with Finastra is an important step forward in breaking down barriers to adoption and increasing access to trade finance,” Contour CEO Carl Wegner said. “By integrating Finastra’s Fusion Trade Innovation, financial institutions and corporates will have access to an end-to-end ecosystem of services that will enable them to transact seamlessly and securely.”

Finastra also announced a partnership with India’s Kotak Mahindra Bank, specifically supporting the firm’s new integrated corporate banking portal, Kotak FYN. The bank will rely on Finastra’s Unified Corporate Portal solution, expanding a partnership with Finastra that extends back to October of 2021. The new enterprise portal will enable bank customers to conduct trade services. By the final quarter of the year, the portal will also offer account services, payments, and collections.

“Working together with Finastra, the Unified Corporate Portal will allow us to make the Kotak FYN portal even more revolutionary,” Kotak Mahindra Bank President for Global Transaction Banking Shekhar Bhandari said. “We can provide intuitive, easy-to-use access to many products and user journeys through a single platform, reducing complexity and friction for our customers and providing a truly differentiated user experience.”

The Bank’s Unified Corporate Portal will leverage Finastra’s Corporate Channels framework. This will empower banks to offer their corporate clients a seamless experience for account services, payments, trade, supply chain finance, and lending. The portal will enable banks to unify data across portals and back office systems to give users a single view of transactions, positions, and balances. Finastra noted that the integration will support self-service operation and boost efficiency.

Finastra’s partnership news comes in the wake of a new C-suite hire: the appointment of Helen Cook as the company’s Chief People Officer. Announced late last week, Cook comes to Finastra from Natwest Group, where she worked as Chief Human Resources Officer. At Finastra, Cook will be tasked with helping the company fulfill its goal to be “the most inclusive and diverse employer in the fintech industry,” according to a statement.

“Finastra’s vision is built on collaboration, and its commitment to become a truly inclusive workplace and enhance the skills of its workforce,” Cook said. “I’m thrilled to support in growing and developing the company’s global talent.”

Finastra was formed in 2017 as a merger between Finovate alum Misys and D+H. The company’s technology is used by more than 8,600 institutions, including 90 of the top 100 banks in the world. Simon Paris is CEO.

The ESG (Environmental, Social, and Governance) movement may be drawing snickers from some corners of the investing world. But in places like Singapore, the drive to build a more sustainable, equitable, and accountable world for investors and users of financial services, is picking up steam.

This week, the Monetary Authority of Singapore announced the launch of its ESG Hub. The Hub is dedicated to supporting collaboration between fintechs, financial institutions, and other industry participants. With 15 ESG fintechs and organizations already on board, the new hub will serve as an anchor for a variety of sustainability initiatives including the Point Carbon Zero Program and KPMG’s ESG Business Foundry.

The Hub will also facilitate MAS’ Project Greenprint, a set of initiatives launched in 2020 to help the financial industry obtain “quality, consistent, and granular data” on sustainability. The project includes a common disclosure portal to simplify the ESG disclosure process; a data orchestrator to aggregate sustainability data from multiple sources such as ESG data providers, utilities providers, and others; a ESG registry to record and manage ESG certifications; and a marketplace to help green technology providers in Singapore connect with investors, venture capital firms, and financial institutions to foster partnerships and innovations in green technology.

“The establishment of the ESG Impact Hub is a critical milestone in Project Greenprint’s journey to build a vibrant and robust ecosystem in Singapore, underpinned by technology and data,” MAS Chief Sustainability Officer Darian McBain said. “This physical Hub will augment MAS’ plans to launch a digital Greenprint Marketplace next year to catalyze the growth of the region’s online ESG community; and will serve as the launchpad for public-private partnerships that support Asia’s just and sustainable transition to a low carbon economy.”

MAS’ ESG hub will look to build Singapore’s ESG ecosystem in three ways: helping corporations and financial institutions meet their ESG needs via the “discovery, scaling, and deployment” of new green technical solutions; partnering with knowledge leaders, investors, and financial institutions to organize and launch ESG accelerator programs, workshops and other initiatives; and supporting ESG stakeholders by directing the community’s “programs and solutions toward “material, quantifiable impacts.”

As of October 4, the members of MAS’ ESG Impact Hub include:

Acre Resources

CDP

Climate Impact X

Circulate Capital

Eachmile Technologies

Equilibriuim AI

GDST (Global Dialogue on Seafood Traceability)

Grow Asia

KPMG

MUFG BAnk

STACS

Stonehaven

Terrascope

The Nature Conservancy

World Wide Generation (WWG)

Elsewhere in the Singapore fintech ecosystem, customer intelligence and risk assessment firm Bizbaz recently secured $4 million in seed funding. The round was led by HSBC Asset Management, and featured participation from Vynn Capital and SOSV.

Bizbaz offers banks, fintechs, and other businesses the ability to leverage data to acquire new, unbanked and underbanked customers, reduce risk and cost-associated risk, and create revenues from upselling new financial products to existing customers. Founded in 2019, the Singapore-based company offers a range of financial intelligence solutions including alternative credit scoring, fraud detection, eKYC, and product aggregation and recommendation systems.

Bizbaz does business in Indonesia, the Philippines, Malaysia, Vietnam, Bangladesh, Thailand, Africa, and Latin America, as well as its home market of Singapore. The company notes that more than seven out of ten Southeast Asia’s 680 million population are unbanked and have no credit history. At the same time, Bizbaz recognizes that mobile phone penetration rates of 69% give the startup the opportunity to leverage social data, along with financial data, to develop risk profiles for thin or no-file individuals.

“Most financial institutions and financial technology companies still use outdated financial history based credit risk systems,” Bizbaz CEO Hayk Hakobyan said. “Our solutions analyze all financial and non-financial data, which have meaningful impact on risk assessment for loans, insurance and other financial services.”

Bizbaz includes insurtechs eBaoTech and Aktivo, Philippine credit bureau CIBI, and digital identity and programmable communications firm Telesign among its partners. This spring, the company announced a collaboration with Australia-based Advanced Human Imaging Limited.

HSBC Asset Management is the investment division of U.K.-based HSBC Group. The firm’s investment in Bizbaz comes a little over a year after launching a new venture capital investment strategy designed to gi give customers more exposure to innovative fintechs. The Greater Bay Area in China was among the markets highlighted when the fund was announced late last summer.

Here is our look at fintech innovation around the world.

Neutronpay, a Vietnamese fintech that leverages Bitcoin’s Lightning Network to enable consumers and businesses to send and receive payments, secured $2.25 million in seed funding.

Singapore AI and Big Data company Advance.AI announced a partnership with Visa to enhance credit decisioning for un- and underbanked communities in Southeast Asia.

Sub-Saharan Africa

Nigeria-based proptech Spleet raised $2.6 million in a round led by MaC Venture Capital.

From Open Banking to Embedded Finance, there are more ways than ever for financial institutions and financial services providers to embrace digital technology and bring better, more personalized, and easier to use financial products to market.

One company that is playing a role in helping businesses make the most of the latest innovations in financial technology is ASA. The company, headquartered in Utah and making its Finovate debut last year at FinovateFall, facilitates collaborations between financial institutions and fintechs. An embedded solution, ASA’s technology helps community banks and credit unions offer their customers the same quality of innovative digital services offered by their larger rivals.

We caught up with Lisa Gold Schier, Chief Strategy Officer with ASA, to talk about the opportunity of collaborative banking, how to make bank/fintech partnerships work, and what financial institutions are focused on right now.

Tell me about your time in the industry and your new role at ASA. Why did you make the switch from banking to fintech?

Lisa Gold Schier: I started my financial services career with a bank, then worked with banks and fintechs. However, I had never worked directly for a fintech. Prior to joining ASA, I served as a leader at the American Bankers Association (ABA), where I led product evaluation and served as a strategic advisor to bankers, technology providers, and consultants across areas such as technology trends, digital transformation, and the customer experience. I helped establish and spearhead the only industry committee focused on guiding strategic direction for industry innovation with an emphasis on bank/technology partnerships and core processor engagement.

I evaluated hundreds of fintech solutions during my years at ABA. When I discovered ASA, I knew it was something unique. I realized ASA’s technology and framework changes and improves how financial institutions, fintechs, and customers access technology and work together. By joining the team, I help financial institutions and fintechs meet the needs of their account holders. I am now Chief Strategy Officer at ASA, driving the strategy of collaborative banking and creating a clear path to innovation, scale, and customer financial empowerment through embedded fintech.

Who is ASA and what is collaborative banking? What makes it different than Open Banking or Banking as a Service?

Schier: While OpenBanking and Banking as a Service each have their place in the market, challenges exist with each. Banking as a Service requires fintechs to jump through regulatory hoops and open banking puts banks and fintechs against each other in competition for customers’ finances. Collaborative banking, on the other hand, is a model that allows financial institutions and fintechs to work together, sharing revenue and business opportunities. Collaborative banking takes the spirit of open banking and mitigates the pitfalls, allowing institutions and fintechs to partner in a mutually beneficial way by removing the regulatory risk traditionally associated with partnerships.

ASA, the pioneer of collaborative banking, is an embedded fintech solution that connects financial institutions with customer-facing fintechs in a secure, compliant, and easy to implement marketplace, powering growth and opportunity for all. Account holders select and instantly download the apps that meet their individual needs, and link their accounts without giving the fintech access to any personal information. With ASA and collaborative banking, financial institutions are the hub of financial choice, maintaining the account holder relationship and providing financial empowerment through individualized choice.

Lisa Gold Schier introducing ASA’s demo at FinovateFall 2022 in New York.

What challenges have traditionally made bank/fintech partnerships difficult, and how is the ASA model helping to overcome them?

Schier: There are many challenges, some of the largest include developing an innovation strategy and the team to implement and follow through, researching and vetting all the fintechs and determining which ones will solve the majority of customers’ needs, contracts, core integrations, and balancing innovation with liability and risk. These roadblocks can be especially challenging for community institutions, who lack the large tech budgets of regional and national players.

ASA addresses these issues by acting as a single integration point between financial institutions and fintechs, either through the institution’s core, online provider, or data aggregator. Fintechs never interface with institution’s core, and ASA normalizes, tokenizes, and anonymizes customer PII data, ensuring fintechs can’t access personal accountholder data.

By solving the one-to-one integration pain point, ASA is enabling personalization at scale by allowing customers to choose and download the niche apps they crave without diluting the relationship with the bank or credit union. ASA creates a trusted closed network between financial institutions and fintechs, making partnerships easier, more affordable, and more secure than ever before.

How do you mentor and support women in the industry?

Schier: I strongly believe in having diverse views around the table, and part of doing so means proactively seeking out those different perspectives. This often looks like creating networks, whether within my organization or within the industry, and then supporting each other. It’s important to foster relationships with junior and senior women and share advice and insights.

I also support women through social media and speaking opportunities, looking at and creating diversity in promotional and advertising materials. It’s disappointing to see panels and conference sessions that lack diversity. So, when I am working with conference coordinators, I make it a priority to seek diverse representation, which includes recommending industry leaders and women that may not be tied in with the conference circuit. This also includes working with and supporting diverse communities. Since so many have supported me, I want to continue to give back to the industry.

What is top of mind for financial institutions and fintechs now and over the next 12 months?

Schier: To quote Ron Shevlin, our industry is at a hard fork in the road, and it’s critical for banks and credit unions to move toward the collaborative future of banking. Doing so will enable them to keep up with all of the new technology apps, grow business, and remain relevant. Financial institutions and fintechs that embrace embedded fintech and lean into secure consumer choice, providing consumers with more authority over who has access to their data and under what circumstances, will gain a strong competitive advantage. Moving forward, financial institutions and fintechs should prepare to embrace self-sovereign identities more fully, enabling consumer ownership of their data in new, innovative ways.

Customers increasingly need easier, quicker access to a range of financial education and wellness resources, especially given current market volatility. Those financial institutions that proactively offer more choice, providing customers with simpler, more secure, wider access to the tools needed to develop their financial health and education, will be well positioned to promote financial empowerment and equity.

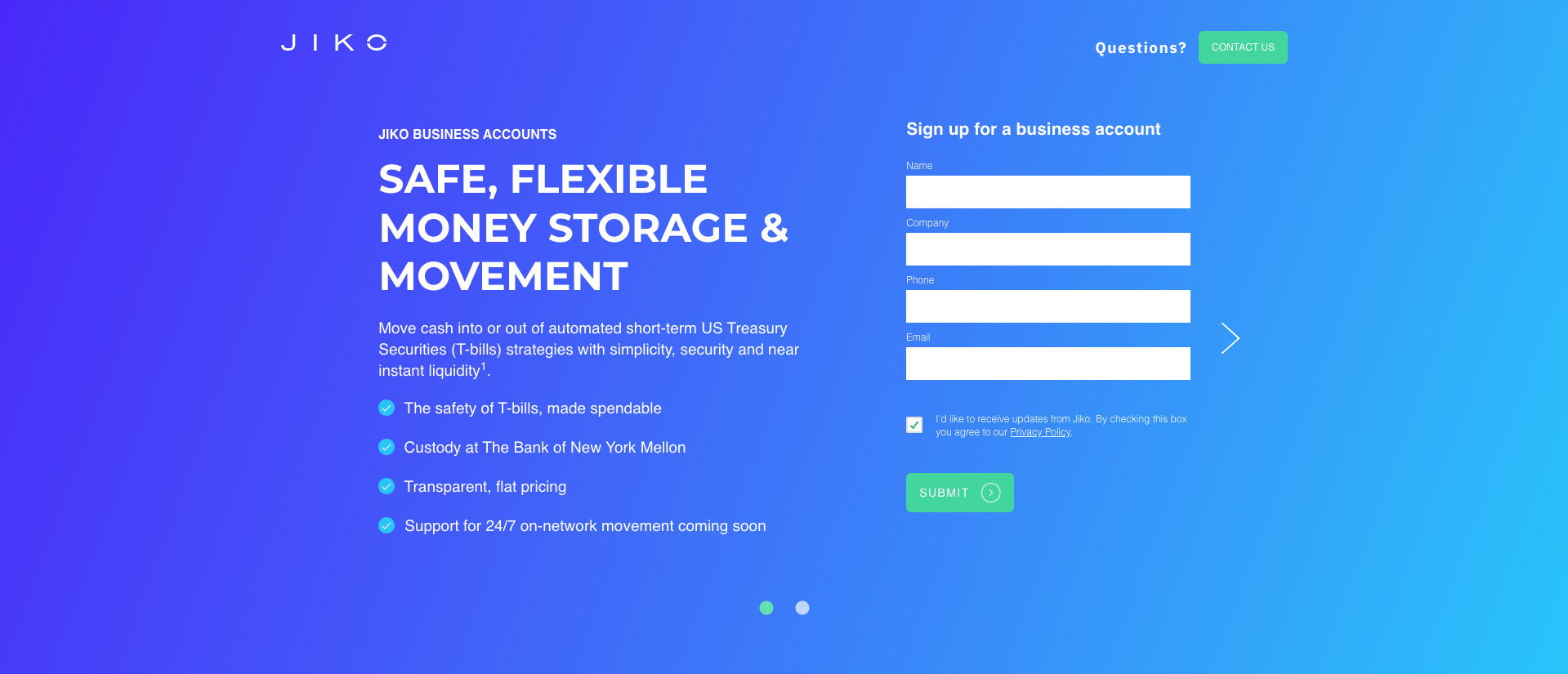

Cash management innovator Jiko raised $40 million in Series B funding today.

The company’s technology enables businesses of all sizes to store their cash in higher yielding “spendable T-bills.”

Jiko also announced the launch of its Jiko Money Storage solution, which will soon enable 34/7 money movement on the Jiko Network.

Among the more interesting fintechs innovating in the cash management space, Jikoraised $40 million in Series B funding today. Jiko enables companies of all sizes to move cash into and out of short-term U.S. Treasury bills (known as T-bills).

Jiko “spendable T-bills” provide transparent pricing and near instant liquidity, blending the safety and yield of T-bills with the flexibility of cash. The Oakland, California-based fintech leverages its status as a broker-dealer, as well as its technology stack and bank charter, to operate more cost-efficiently than other cash storage options.

“Today’s CEOs, CFOs, and corporate treasurers must be increasingly nimble in the face of factors such as inflation, supply chain disruption, and geopolitical conflict, while still managing their company’s risk exposure – making it paramount that cash deliver yield through safe and secure strategies,” CEO and co-founder of Jiko Stephane Lintner said.

“That need is at the heart of why we created Jiko, and with this additional funding, we look forward to continuing our work to transform how money can be moved and stored – exemplified by our milestone launch of Jiko Money Storage.”

Jiko Money Storage, also announced today, enables businesses to store cash securely in the form of T-bills with on-demand liquidity at leading custody bank BNY Mellon. Jiko will soon make the holdings movable 24/7 on the Jiko network.

The company’s Series B round was led by Red River West. Trousdale Ventures, Owen Van Natta, Temaris & Associates, La Maison Partners, BPI France, Airbus Ventures, Anthem Ventures, Upfront Ventures, and Radicle Impact also participated. The investment adds to the $47.7 million the company has raised to date via its Series A and seed funding rounds.

“It’s rare to come across a fintech team quite as ambitious as Jiko’s,” Airbus Ventures Partner Claas Kohl said. “Jiko’s network presents uncompromised safety combined with the efficiency of a modern tech stack and is equipped to soon support multi-currency financial activity.” Former U.S. Treasury Secretary and Jiko advisor Larry Summers said, “In today’s macro environment, cash should be put to work – not sit idly in bank accounts. I don’t endorse any products or platforms, but I am excited by the innovation that Stephane and his team are delivering for money storage and look forward to continuing to advise them.”

AML surveillance technology specialist Hawk AI forged a strategic partnership with digital onboarding and business KYC solutions provider Know Your Customer.

The partnership will give businesses an integrated anti-fraud solution that will help them avoid the problem of siloed compliance technologies.

Munich, Germany-based Hawk AI made its Finovate debut in May, demoing its technology at FinovateSpring in San Francisco, California.

Hawk AI, an anti-money laundering surveillance technology company for banks and fintechs, announced a strategic partnership with Know Your Customer this week. The alliance will combine Know Your Customer’s digital onboarding and business KYC solutions with Hawk AI’s transaction monitoring technology. The new offering will give businesses an integrated anti-fraud solution to enhance their defense against financial crime.

“There is a wave of technological innovation taking place in RegTech,” Hawk AI CTO and co-founder Wolfgang Berner said, “from cloud native infrastructure enabling scalability, real-time native processing in a performant, safe and secure way, to fully explained AI and machine learning that augment traditional AML approaches and ensure efficient and effective crimefighting.”

Berner also underscored the challenge of fraud prevention solutions that are not well integrated. “Cutting-edge technology is not enough if information remains siloed,” he said. Berner noted that Know Your Customer shared Hawk AI’s “vision of modular solutions that foster a more holistic approach to fighting financial crime.”

Hawk AI’s Steve Liú, General Manager North America

Processing billions of transactions in more than 60 countries every year, Hawk AI’s technology leverages explainable AI and cloud technology to detect financial crime while keeping false positives low. The company reported that reducing false positives can help AML compliance officers save up to 70% of their workday, enabling them to focus on more complex compliance challenges.

Hawk AI made its Finovate debut earlier this year at FinovateSpring 2022 in San Francisco. Headquartered in Germany, and founded in 2018, the company demoed its AML Surveillance Suite. The technology blends AI with traditional, rule-based strategies to monitor financial transactions in real-time and help financial institutions and fintechs better detect suspected cases of fraud, financial crime, and money laundering. This method helps identify minor, easily missed anomalies that can be overlooked by traditional rule-based approaches alone.

Hawk AI includes financial services consultancy Capco, and KYC and customer onboarding specialist Ondato – as well as fellow Finovate alums like Visa, Mambu, and Diebold Nixdorf – among its partners. A member of the RegTech 100, Hawk AI has raised $10 million in funding from investors including BlackFin Capital Partners and Picus Capital. Co-founder Tobias Schweiger is CEO.

Crypto friendly banking platform Juno has raised $18 million. The Series A round was led by ParaFi Capital ‘s Growth Fund. The fundraising included a sizable number of investors including Greycroft, Antler Global, Hashed, Jump Crypto, Mithril, 6th Man Ventures, Abstract Ventures,, and Uncorrelated Fund.

As part of the investment, Juno announced the launch of a new loyalty token, Juno coin (JCOIN). The program acts similarly to credit card rewards points schemes, and tokens will only be distributed to verified account holders. Juno users can earn JCOIN by spending crypto with their Juno debit card or by taking their paychecks in cryptocurrencies such as bitcoin, Ethereum or USDC. The company says that more than 75,000 customers in the U.S. take and invest at least a portion of their salary in cryptocurrency every month on its platform.

Juno offers cryptocurrency checking accounts that enable individuals to earn, invest, and spend in crypto. The checking accounts are free to open, and both crypto deposits and withdrawals are free, as well. The accounts are FDIC insured, courtesy of a sponsorship by Evolve Bank & Trust. Note that the USD holdings in the account, not the crypto holdings, are covered.

A merchant and developer-first payments orchestration platform, Elements was credited for its ability to “take the complexity out of crypto payments,” by Circle Chief Product Officer Nikhil Chandhok. The Elements acquisition will help make it easier for merchants to integrate their current PSP relationships with Circle’s crypto payments solutions. “Providing well-designed payment products that can facilitate seamless, efficient, frictionless and delightful customer experiences are key to empowering merchants to take advantage of these next-gen payment solutions,” Chandhok said.

An issuer of both USD Coin (USDC) and Euro Coin (EUROC), Circle enables companies around the world to leverage digital currencies and public blockchains to facilitate payments, commerce, and financial technology. Founded in 2013, the Boston, Massachusetts-based company recently announced partnerships with GIANT Protocol to facilitate tokenized mobile data and with non-profit Mara Foundation to help developers in Africa build DApps and blockchain solutions.

There are big changes at the top for New York Digital Investment Group – more popularly known as NYDIG. The cryptocurrency investment company began the week with news that both CEO Robert Gutmann and President Yan Zhao were stepping down from their positions. Replacing them will be Tejas Shah, who will become NYDIG’s new CEO, and Nate Conrad, who was promoted to President.

Shah was formerly NYDIG’s Global Head of Institutional Finance. Conrad was previously NYDIG’s Global Head of Payments. Both Shah and Conrad joined NYDIG in 2020. In their new roles, both executives will be tasked with boosting investment in the company’s mining franchise and accelerating bitcoin adoption via solutions like the Lightning Network, which facilitates payment by bitcoin.

Speaking of investment, NYDIG’s C-suite personnel news came at the same time that reporters uncovered an SEC filing revealed that NYDIG had raised $720 million for its institutional digital asset fund. According to the filing, 59 investors participated with an average investment of $12 million.

Founded in 2017, NYDIG is among the industry’s biggest custodians of cryptocurrencies. The company holds more than $1 billion in digital assets for its customers.

As more card issuers authorize cardholders to transact in cryptocurrencies, it becomes increasingly important to make sure that card issuers are up-to-date and compliant with the regulations that govern digital assets. This week, we learned that Mastercard had launched a new solution, Crypto Secure, designed to enable issuers to determine the risk profile of crypto exchanges and other crypto providers, before specifying which purchases of cryptocurrency should be approved.

The new offering will enable issuers to accurately identify the crypto exchanges from which their cardholders are buying crypto, measure transaction approvals and declines, review their exposure to crypto risk at a portfolio level, and compare themselves to a peer group of financial institutions.

“Crypto Secure will provide card issuers with a platform that allows them access to insights which will improve the safety of crypto purchases,” President of Mastercard Cyber and Intelligence Ajay Bhalla said.

Crypto Secure is powered by CipherTrace, a cryptocurrency intelligence company Mastercard acquired just over a year ago. CipherTrace’s data analytics and algorithms provide insight into more than 900 cryptocurrencies, helping companies bring better security to their crypto-related operations. The Menlo Park, California-based company was founded in 2015.

We mentioned the Lightning Network earlier in our look at the goals of the new leadership team at NYDIG. Just recently, a company based in Vancouver, Canada, and Ho Chi Minh City, Vietnam, announced that it has secured $2.25 million in seed funding for its technology that brings the benefits of bitcoin’s Lightning Network to the payments rails of southeast Asia.

Hivemind Ventures led the round for Neutronpay, which disclosed the investment last week despite raising the money in June. Participating in the investment were Republic Cavalry, Ride Wave, Studio, Iterative, Fulgar Ventures, along with individual investors. Among these individual investors is Lisa Shields, founder and CEO of Finovate alum FISPAN.

The company has already put the new capital to work, adding talent with an eye toward boosting its capacity to develop enterprise APIs, soon, a consumer mobile app. ‘”Laying the infrastructure for Lightning across South East Asia would make it very easy for locals to better transact with each other and for the rest of the world to transact in the region – whether while on vacation or for doing business,” Neutronpay founder and CEO Albert Buu said.

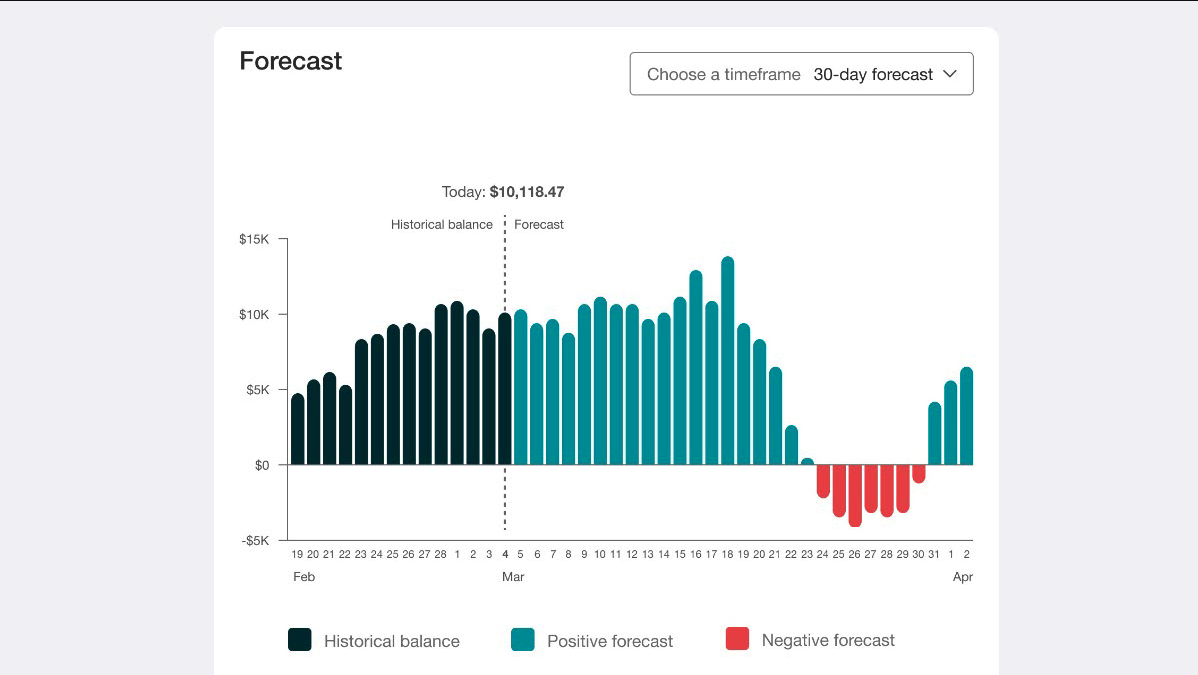

U.S. Bank introduced a new tool to give small business owners the ability to see a 90-day forecast of their cash flow.

The new offering is the latest innovation from U.S. Bank’s Business Essential suite of banking and payments solutions.

U.S. Bank made its Finovate debut last year at FinovateFall 2021. At the conference, the bank demoed its Cards-as-a-Service (CaaS) technology.

U.S. Bank unveiled a new solution to enable small business owners to see a 90-day forecast of their cash flow. The tool allows users to leverage external data from their clients along with their own U.S. Bank accounts to provide more comprehensive insights. The offering is designed to address what U.S. Bank Chief Digital Officer Irv Henderson called “a top concern for today’s business owners.”

“Giving our clients the ability to forecast their cash flow outlook, including, in the future, the capability to consider various scenarios, will provide them with vital information to make smart decisions for today and the future,” Henderson said.

U.S. Bank’s new cash flow tool gives users a 90-day historical view along with its forecast of account balances up to 90 days ahead. The bank plans to introduce additional functionality to enable users to build “what if” scenarios and observe the impact of those scenarios on future cash flow.

The tool is currently available to clients of U.S. Bank from their online dashboard. Part of U.S. Bank’s Business Essentials suite of banking and payments solutions, the cash flow tool is the bank’s latest effort to “bring together digital capabilities and the power of data” to provide small businesses with actionable insights, according to Henderson.

U.S. Bank made its Finovate debut a year ago at our all-digital FinovateFall 2021 conference. At the event, the Minneapolis, Minnesota-based bank demonstrated its Card-as-a-Service (CaaS) technology that enables companies to extend corporate credit digitally. With the touch of a button, virtual cards -with precise spend limits, tokenization, and encryption – can be pushed to users’ mobile wallets in real time. The Card-as-a-Service solution also gives businesses the ability, via API integration, to build custom virtual payment experiences in their ecosystem.

The parent company of U.S. Bank National Association, U.S. Bancorp serves millions of customers through a range of businesses including consumer and business banking, payment services, corporate and commercial banking, wealth management, and investment services. The institution has $591 billion in assets as of June 2022.

A financial institution serving area creatives, Nashville, Tennessee-based Studio Bank has partnered with Corserv.

The credit card issuing program provider will enable Studio Bank to launch a comprehensive credit card program featuring virtual cards, automated credit decisioning, and more.

Founded in 2018, Studio Bank is the first newly chartered de novo bank to launch in Nashville in more than a decade.

“We are excited to launch this next level of innovation,” Studio Bank Chief Experience Officer April Britt said. “Our clients have a unique set of credit card and payment needs as business owners, leaders, and creatives. We have been able to partner with Corserv to create a program to provide an enhanced credit card user experience with all the conveniences of the modern economy.”

A digital financial institution, Studio Bank is designed to bring banking services to Nashville area creatives. And by “creatives,” Studio Bank looks to serve a variety of creative communities: from musicians and code writers to entrepreneurs, social activists, and even parents working to build better lives for their families. Founded in 2018, Studio Bank was the first newly chartered de novo bank to launch in Nashville in more than 10 years. Reaching profitability in its second year of operation, Studio Bank has assets of more than $750 million as of the end of Q2 2022.

Studio Bank’s partnership with Corserv comes less than a month after the bank announced raising $38 million in new funding. The fresh capital includes $18 million in equity issued this spring as well as $20 million in unsecured notes issued from Studio Financial Holdings, a new holding company also announced last month. “As I have always said from the founding of Studio Bank, we offer the sophistication and capability of a large, regional bank coupled with the customer service of the very best community bank we could create,” Studio Bank CEO and President Aaron Dorn said when the funding was announced. “Our growth and expansion into key communities in Middle Tennessee show we are fulfilling that promise.”

Atlanta, Georgia-based Corserv offers a turnkey credit card issuing program that gives financial institutions the ability to offer branded credit cards to consumers, businesses, and commercial customers. The company’s program includes features such as virtual card support for ePayables, automated credit-decisioning, sales and servicing portals, transparent reporting, and hosted and secure PCI compliant software.

“Our program is designed to enable banks, like Studio Bank, to own their credit card financials without the need to add expertise, infrastructure, or staff,” Corserv CEO Jerry Craft said. “We look forward to providing Studio Bank with the tools to serve their unique customer base with innovative payment solutions for their evolving needs.”

This year, Corserv has partnered with regional financial institutions such as Massachusetts-based BayCoast Bank, Madison-based correspondent bank Bankers’ Bank, and The Bank of Missouri (TBOM). In August, the company received Visa Ready Certification for its Payment Cards as a Service APIs (PCaaSA) issuer processor program.