This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Join Finovate VP and host of the Finovate Podcast Greg Palmer as he wraps up 2023 and gets us ready for 2024 with a quartet of conversations about the latest trends in fintech and financial services.

From life stories about women and men who became fintech converts, founders, and innovators later in their professional careers to discussions on enabling technologies like Generative AI, the Finovate Podcast is a great place to hear some of the smartest voices in our business talk about what matters most.

Podcast host Greg Palmer sits down with Barry Kirby and Dave Buerger of Union Credit, winners of the “Best Emerging Technology” category of the 2023 Finovate Awards. EP 197.

Greg Palmer interviews Dhairya Dholiya, Vice President of Growth & Innovation at Celtic Bank, on his transition from innovator to banker. EP 196.

Greg Palmer talks with tech founder, venture investor, and Head of Innovation for Better, Nneka Ukpai, on the lessons learned from a recovering lawyer turned innovator. EP 195.

Host Greg Palmer and Experian VP of Strategy, Global ID and Fraud David Britton discuss Generative AI and fraud – why it’s so scary and what you can do about it. EP 194.

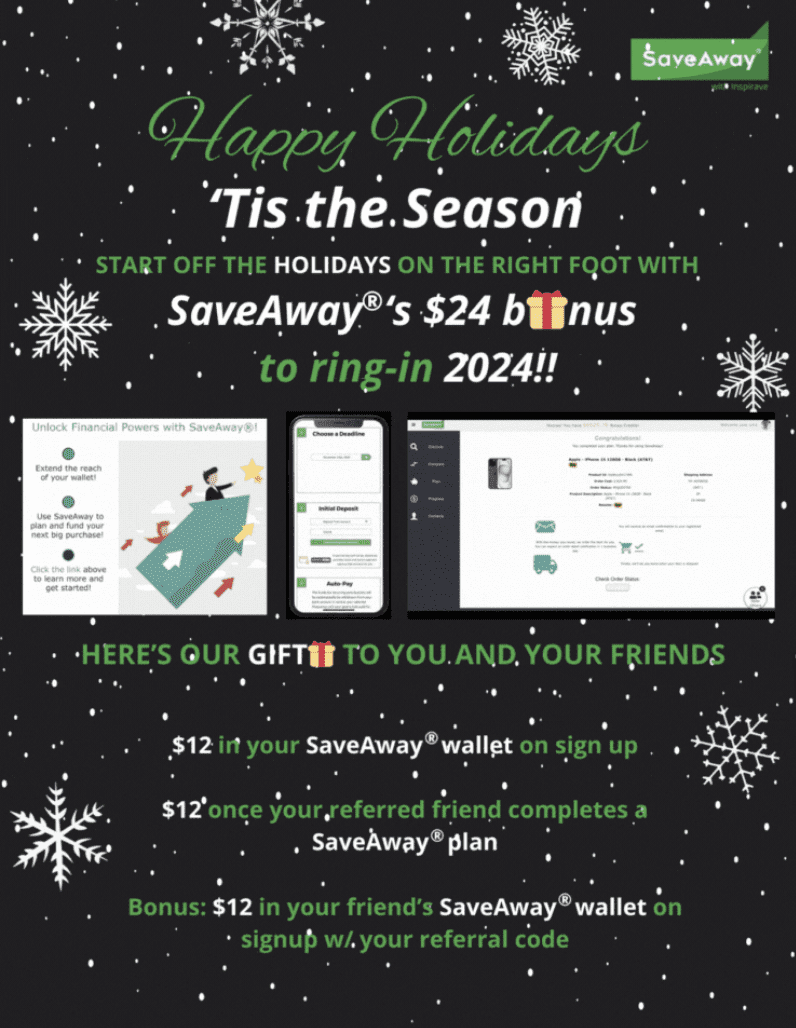

SaveAway is celebrating the season with its “$24 to Ring in ’24 program. The new offering, timed for the New Year, will put $12 in the SaveAway wallet of new sign ups and another $12 for any referral who signs up and completes a SaveAway plan. That’s $24 for new users who bring along a referral now through January 2024.

In an email, CEO and founder Om Kundu explained the thinking behind the “$24 to Ring in ’24” plan. “The $24 to ring in 2024 initiative is a recognition for those joining the remarkable company of our pioneering users and partners who have seen the merits of SaveAway first-hand,” Kundu said.

“SaveAway is social by design, as well as its proprietary engineering – $24 to Ring in ’24 is the celebratory spirit to recognize, and make the opportunity for our users to refer other SaveAway users that much more rewarding.”

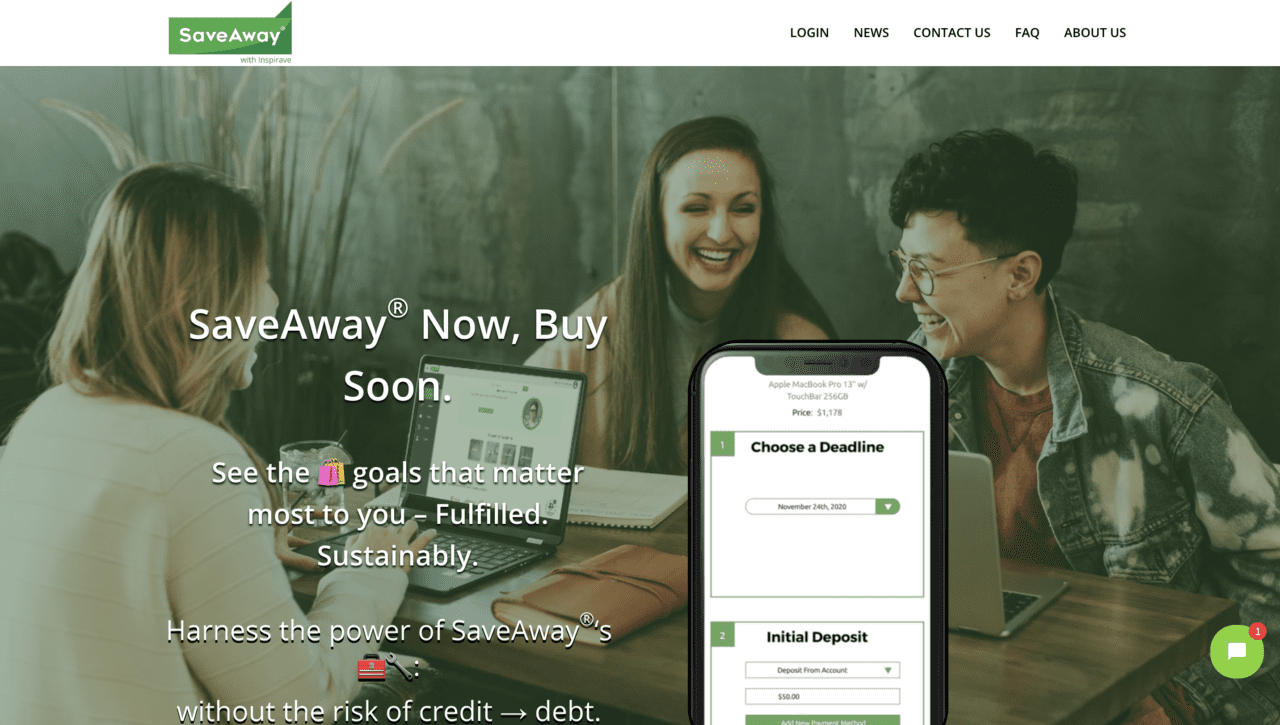

The company’s “SaveAway Now, Buy Soon” approach offers a departure from the world of Buy Now, Pay Later. The social saving and retail e-commerce platform enables consumers to buy important purchases responsibly, without having to rely on credit.

In this way, the solution combines intelligent financial planning with a sustainable path-to-purchase. The platform’s social gifting functionality enables members of the user’s trusted social network of friends and family to both support sensible spending as well as help users make purchases that they cannot afford on their own.

Users have praised the ease with which they can invite friends and family to participate in the spending process – voting on options and gifting toward the eventual purchase. The SaveAway platform also lets users see the progress they are making toward their purchase goal based on their personalized savings plan.

SaveAway made its Finovate debut at FinovateFall 2016. Earlier this year, Kundu facilitated the Fintech and E-Commerce Meetup at the SXSW conference, and the Retail Transformation+Evolution at the NRF Big Show Table Talk. Also this year, NYCEDC tapped SaveAway as a recipient of its Founder Fellowship. The fellowship offers resources for technology entrepreneurs from historically underrepresented backgrounds.

SaveAway will begin 2024 as a presenter at VentureCrushFGX having been selected to the 14th cohort of the VentureCrushFG Pod. Run by the Tech Group at legal firm Lowenstein Sandler, VentureCrush offers programs and events for startup founders and investors. The Wall Street Journal ranked Lowenstein Sandler as one of the top five most active law firms in the U.S. in terms of the number of VC/PE deals completed.

With a spot Bitcoin ETF expected in 2024, crypto investors, traders, and enthusiasts are likely feeling as optimistic about digital assets as they have in awhile.

As the trauma of Sam Bankman-Fried and FTX fades further into the background, the digital asset community has been able to refocus its energies on a number of positive developments in the space – from the surging price of crypto assets like bitcoin to the increasing interest in cryptocurrencies from major financial institutions.

So with the year drawing to a close, here are a few recent crypto- and blockchain-oriented headlines that you might have missed.

Coindesk’s reporting is based on a published memo from the SEC’s Office of Market Supervision, Division of Trading and Markets. The memo notes the subject of the meeting as “Meeting with BlackRock re: iShares Bitcoin Trust”, lists the meeting participants, and indicates that the conversation “concerned The NASDAQ Stock Market’s proposed rule change to list and trade shares of the iShares Bitcoin Trust under NASDAQ Rule 5711(d).”

What does this mean for a Bitcoin ETF in 2024? Rule 5711(d) refers to a variety of specific criteria required for listing and trading shares on the Nasdaq exchange. But especially noteworthy are aspects of this rule has to do with market integrity and protections against potentially fraudulent activity. We’ve covered the “surveillance-sharing” issue before in 5 Tales from the Crypto, so it is no surprise to find that the SEC is still looking to dot “i’s” and cross “t’s” as we move closer to a potential new ETF product for crypto investors and traders.

Saylor on Bitcoin: “Biggest Wall Street Development in 30 Years”

Michael Saylor, former CEO and current Executive Chairman of MicroStrategy, was interviewed on Bloomberg TV earlier this week. Asked about the potential of a Bitcoin ETF in 2024, Saylor said that the launch of a Bitcoin ETF next year could be “the biggest Wall Street development in 30 years.” He went on to say that he thought that the launch of an institutionally supported Bitcoin ETF could ignite a major bull market in crypto assets as a new surge in demand confronts current (inadequate) supply.

In his comments Saylor compared the emergence of a Bitcoin ETF to the launch of the S&P 500 ETF, popularly known as the SPY, more than 30 years ago.

Headquartered in Tysons Corner, Virginia, and founded in 1989, MicroStrategy is a long-time Finovate alum. The company made its Finovate debut in 2013 at FinovateSpring in San Francisco. MicroStrategy is a public company, trading on the Nasdaq under the ticker MSTR. The firm has a market capitalization of $8 billion.

Blockchain-based micropayments company raises seed funding

Swiss-fintech Centi, which offers blockchain-based micropayment solutions, announced the completion of a seed funding round this week. The amount of the investment was not disclosed. The round was led by Archblock and Bloomhaus Ventures, with current shareholders and founders also participating. The company will use the funds to help fuel global expansion.

Centi leverages blockchain technology to address two significant challenges in the payments industry: the inefficiency of micropayments and the issue of financial inclusion. Centi responds to these problems with its proprietary stablecoin technology that facilitates transactions as small as a cent. This creates new opportunities in digital content monetization for merchants, creatives, and others.

The Swiss firm also offers a direct-to-consumer stablecoin that can be purchased with fiat currency. This technology supports financial inclusion by giving unbanked consumers a pathway to digital payments.

“We founded Centi driven by the potential of blockchain for micropayments and financial inclusion,” Centi co-founder Bernhard Müller said. “The name ‘Centi’ itself, derived from our capability to process transactions as small as one cent, encapsulates this focus.”

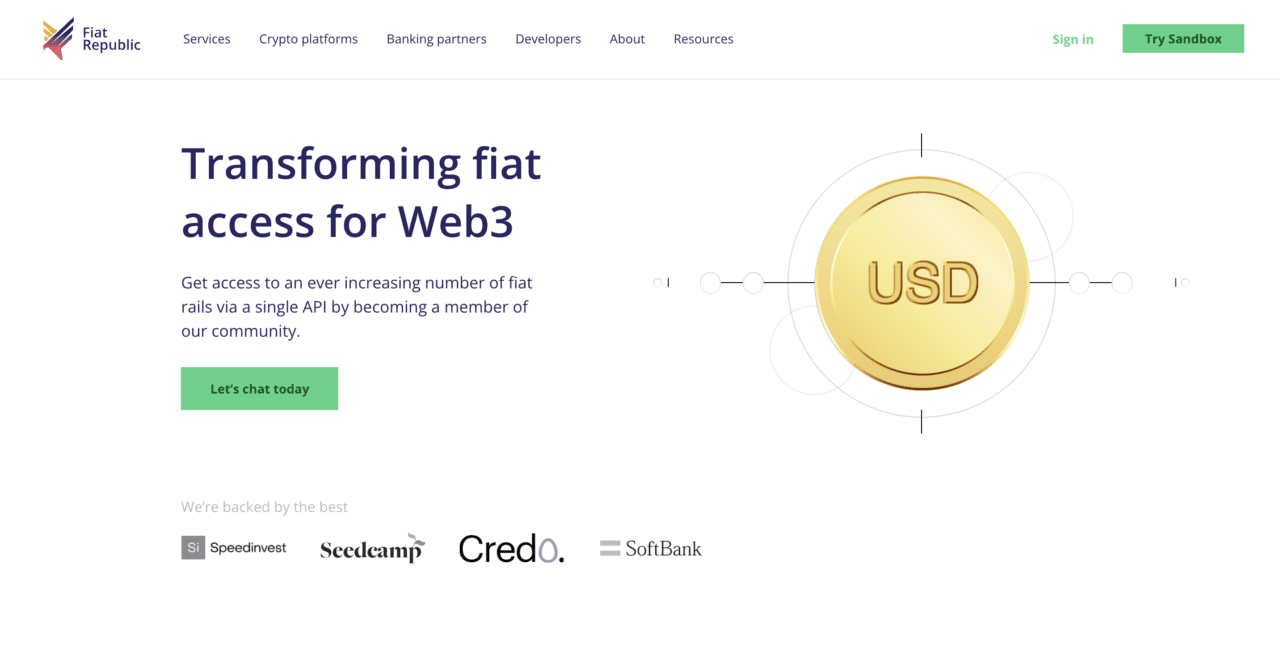

Connecting crypto and banking pays for Fiat Republic

Europe continues to be the source of crypto funding news this week as Fiat Republicannounced a seed extension round of $7 million (€6.4 million). The investors include first-timers Kraken Ventures, Fabric Ventures, Arca, and Inovo Ventures. Existing investors Speedinvest, Credo Ventures, and Seedcamp also participated in the funding. Fiat Republic will use the capital to support growth and expansion, as well as make strategic hires and fortify banking partnerships.

London-based Fiat Republic helps crypto platforms connect with crypto-friendly banks. The company’s platform allows crypto firms to create accounts in multiple currencies and access local payment rails and FX via a single API.

Fiat Republic’s funding announcement comes as the company reports that it has been granted a full electronic money institution (EMI) license by the Netherlands’ De Nederlandsche Bank (DNB). This license will enable Fiat Republic to offer regulated financial services throughout the European Economic Area (EEA). These services include the ability to offer payment services and issue e-money to EEA crypto platforms courtesy of its API. The Dutch license is the second earned by the company; Fiat Republic has held an EMI license in the U.K. for more than a year.

Fiat Republic CEO and co-founder Adam Bialy said that the addition of the Dutch license was a major step for the two-and-a-half year old startup. “Passporting from the reputable and credible jurisdiction of the Netherlands not only boosts our legitimacy in the traditional finance world, but also highlights our commitment to high compliance standards, security, and close collaboration with regulators.”

Crypto Comeback? Looking back and leaping forward

There’s a lot for crypto investors, traders, and observers to be excited about as 2024 draws near: renewed bullishness in assets like Bitcoin and Ethereum, continued interest in crypto from institutional players and financial services incumbents … But before we go, here are a few last looks at crypto in 2023.

Payment provider Ping Payments has forged a partnership with open banking technology company Neonomics.

Via the partnership, Neonomics will manage end-user consents and account-to-account payments for Ping Payments.

Neonomics made its Finovate debut at FinovateEurope 2020 in Berlin. The company is headquartered in Oslo, Norway.

Ping Payments has announced a partnership with open banking technology company Neonomics. The Swedish payment provider will leverage its new relationship with Neonomics to enhance its account-to-account payment capabilities, identity verification, and compliance operations.

“Reach, market insight, and technical viability were paramount in our selection of a partner for expanding our services,” Ping Payments CEO Petter Sehlin said. “Neonomics has consistently demonstrated high quality throughout our relationship, and we are excited to expand our offering outside of Sweden across the Nordics with Neonomics.”

Courtesy of the partnership, Neonomics will manage end-user consents and account-to-account (A2A) payments for Ping Payments. Additionally, the partnership will feature open banking powered identity verification, a significant value-add when combined with account-to-account payment functionality. A specialist in providing payment solutions for platforms, SaaS companies, and marketplaces, Ping Payments will gain from Neonomics connections to Nordic-area banks, leveraging the company’s open banking API platform to reach FIs in Norway, Denmark, and Finland.

Neonomics founder and CEO Christoffer Andvig spoke to this aspect of the partnership in his comments. Andvig said, “With our advanced account verification solutions designed to mitigate risks and safeguard transactions, we will together strengthen payment and compliance processes across all customer touchpoints – bringing a future where transactions are inherently secure and seamless for all participants in the Nordic markets.”

Neonomics made its Finovate debut at FinovateEurope 2020 in Berlin, Germany. At the conference, the company demoed its technology that enables users to trigger instant payments and transfers from their bank, directly from an app or website.

Neonomics’ partnership news with Ping Payments comes just weeks after the company announced another collaboration, this time with Carbon Centrum. The goal of this partnership is to leverage open banking to help reduce carbon emissions. Also this year, Neononics announced that it was working with BetterNow to use open banking to enhance digital fundraising.

Both Ping Payments and Neonomics were founded in 2017. Ping Payments is based in Örebro, Sweden. Neonomics is based in Oslo, Norway.

Looking to demo your latest fintech innovation? Apply now to demo at FinovateEurope in London, February 27 and 28, 2024. Visit our FinovateEurope hub for more information.

Agency execution specialist Liquidnet has turned to investment technology company bondIT to give new tools to traders on its Fixed Income electronic trading platform. Liquidnet will leverage bondIT’s Scorable Credit Analytics to help traders better anticipate market trends. The technology will also help them mitigate credit risk and make more informed decisions quicker.

“With this integration, our goal is to give access to crucial information to investment firms of all sizes,” Liquidnet Global Head of Fixed Income Product and Partnership Programs Nicholas Stephan explained. “Our members will have seamless access to a wide range of credit data giving them an extra edge ahead of making their trading decisions.”

Scorable Credit Analytics leverages data science, Explainable AI, and machine learning to help fixed income investors anticipate changes in credit ratings and spreads. The solution predicts downgrade and upgrade probability for 3,000+ rated corporate and financial issuers worldwide. Using insights such as these, traders can spot investment opportunities earlier and outperform peers. Courtesy of explainable AI, Scorable ensures transparency and allows users to understand the reasons behind the predictions. The integration will benefit Liquidnet’s 700+ member firms that access the platform’s primary and secondary market trading protocols for corporate bonds.

“Bonds are back, but so is risk,” bondIT Head of Global Client Business Dr. David Curtis said. “Technology becomes an ever more important ally in this dynamic financial landscape. The synergy between bondIT’s AI-driven Scorable Credit Analytics and Liquidnet’s platform empowers traders with actionable insights, enabling them to stay ahead in today’s volatile markets.”

Founded in 1999, Liquidnet is an institutional trading network headquartered in New York. More than 1,000 institutional investors in 49 markets across six continents use Liquidnet’s technology. Interdealer broker TP ICAP acquired the company in 2021 for $700 million.

Note that Liquidnet is not the first company this year to deploy bondIT’s Scorable solution. Wealth management solution provider First Rate announced a strategic partnership with bondIT in June. The Arlington, Texas-based firm integrated Scorable Credit Analytics into its own AI-driven reporting tool.

bondIT made its Finovate debut at FinovateFall in 2016. In the years since, the Israel-based fintech has grown into a 50+ person team, and partnered with some of the world’s leading asset managers, banks, and technology firms. In addition to Scorable Credit Analytics, bondIT offers two other solutions: Frontier and Embedded. Frontier provides data-driven, personalized, fixed income portfolio management. Embedded is bondIT’s end-to-end, integrated portfolio construction, research, and trading solution.

Finovate alums raised more than $1.2 billion in equity funding in 2023. The total funding for the year reflects the continued slowdown in fintech funding that began in 2022.

In the fourth quarter of 2023, eleven Finovate alums raised more than $307 million in equity funding. Note, however, that this sum does not include the equity portion of the investment secured by SumUp, for example. The quarterly total also does not include the investment received by Icon Solutions, the amount of which was undisclosed.

Previous Quarterly Comparisons

Q4 2022: More than $380 million raised by 15 alums

Q4 2021: More than $1.2 billion raised by seven alums

Q4 2020: More than $472 million raised by 17 alums

Q4 2019: More than $876 million raised by 21 alums

Q4 2018: More than $800 million raised by 19 alums

Nevertheless, the fourth quarter alumni fundraising total approximates that of both last year’s Q4 and the final quarter of 2020.

Top Quarterly Equity Investments

Adlumin: $70 million

Paysend: $65 million

Scalable Capital: $64.7 million

Three investments in the fourth quarter of 2023 stood out among the others: Adlumin, Paysend, and Scalable Capital all announced fundraisings of more than $60 million in Q4. Also noteworthy was the $40 million raised by Stash in October.

Combined, the top three quarterly equity investments from our alums represent more than 65% of the total alum funding haul for Q4 2023.

Here is our detailed alum funding report for Q4 2023.

If you are a Finovate alum that raised money in the fourth quarter of 2023, and do not see your company listed, please drop us a note at [email protected]. We would love to share the good news! Funding received prior to becoming an alum not included.

Digital conversations platform Eltropy announced a partnership with Magnifi Financial.

The two companies will work to build and launch Generative AI-based solutions for employees, customers, and members of community financial institutions.

Eltropy most recently demoed its technology at FinovateFall 2022 in New York.

Digital conversations platform Eltropy and Magnifi Financial are working together to launch Generative AI solutions to enhance employee training and improve the customer/member experience. Eltropy’s Generative AI tools are powered by large language models (LLMs) that are specifically designed for community financial institutions (CFIs). These tools have enabled CFIs to bring new efficiency to their operations and greater personalization to the products and services they offer. Speaking about the partnership in a statement, Magnifi Financial SVP for IT and Digital Brad Shafton highlighted the fact that Eltropy’s technology is especially geared toward the needs of community financial institutions.

“What sets Eltropy apart is not just their technology but also their dedication to understanding the credit union industry and their commitment to community financial institutions like ours,” Shafton said. “They continue to evolve, and that’s why we consider them a long-term partner, including for AI.”

Magnifi will deploy Eltropy’s technology in a number of ways, including enhancing the firm’s mortgage and lending operations. Additionally, Eltropy’s ChatGRT-style Employee Assistants enable customer-facing financial services workers – from contact center agents to tellers – to access vetted, verified customer data. The technology also automates tasks like e-mail response generation, using natural conversational language.

To this end, Eltropy co-founder and CEO Ashish Garg said that solutions based on Generative AI have the potential to provide credit unions and community banks with new “innovative ways to thrive.” Garg added, “Eltrophy’s generative AI tools are empowering forward-thinking CFIs to achieve this by accelerating and enhancing employee knowledge training, improving the member experience and ultimately fueling growth.”

Eltropy made its most recent Finovate appearance last year at FinovateFall 2022. The company’s partnership with Magnifi Financial follows news of a collaboration with fellow Finovate alum Jack Henry from earlier this month, and an integration with Fiserv’s full-service account processing platform Portico in November. In August, Eltropy teamed up with yet another Finovate alum, Alkami, to enhance digital conversations for financial institutions.

Headquartered in Milpitas, California, Eltropy has raised $25 million in funding. The company includes K1 Investment Management and Curql among its investors.

Payments solutions company Allied Payment Network has partnered with MY CREDIT UNION of Bloomington, Minnesota.

The partnership will integrate Allied’s payment technology with the credit union’s Ultracs digital banking platform.

Headquartered in Fort Wayne, Indiana, Allied Payment Network made its Finovate debut in 2013.

Payments solutions provider Allied Payment Network will integrate its technology with MY CREDIT UNION’s Ultracs digital banking platform courtesy of a new partnership.

“Financial institutions like MY CREDIT UNION serve a critical role in their communities,” Allied Payment Network CEO Geoff Knapp said. “Their members aren’t just numbers; they’re neighbors and friends. They are allies for their community and we’re proud to be an ally for them.”

Headquartered in Bloomington, Minnesota, MY CREDIT UNION specializes in providing its members with financial wellness and banking solutions that “educate, empower, and engage.” Founded in 1957, MY CREDIT UNION has $380 million in assets, and serves its members via four branches as well as online.

MY CREDIT UNION President Greg Worthen credited Allied Payment Network for being a “community-focused organization.” He noted that this factor, among others, is what helped seal the deal. “With the combination of two, state-of-the-art platforms like Ultracs and Allied,” he said, “we’re confident we’ll be able to give our members the superior mobile-first experience they expect.”

Fort Wayne, Indiana-based Allied Payment Network made its Finovate debut in 2013 at FinovateSpring. Since then, the company has grown into a major paytech leader with 500 bank and credit union customers. Allied Payment Network offers a real-time, open-network payments model, and features a broad range of online and mobile solutions. These products and services include online billpay, P2P fund transfer, PicturePay, BizPay, PortalPay, A2A fund transfer, and Vault, a digital document storage solution.

In 2022, the company processed $3.6 billion in payment volume. This year, Allied Payment Network has forged partnerships with fellow Finovate alum Q2 in May, First Farmers Bank & Trust and Central Payments in June, Washington-based Commencement Bank and South Carolina-based United Community in September, and marketing firm Murphy & Company in October. The company also made a pair of C-suite hires in 2023. Allied began the year adding Kathi Klawitter as Chief Operating Officer. In July, the company introduced new Chief Information Security Officer James Dixon.

Allied Payment Network has raised more than $8 million in funding. The company includes Plymouth Growth among its investors.

Enabling technologies continue to fuel innovation in fintech and financial services. But what are regulatory bodies doing to ensure safety for consumers and fair competition for businesses?

Here are some of the areas where regulators could make themselves felt by the fintech industry in 2024.

AI: From the EU’s AI Act to Executive Orders in the U.S.

Whether its the boardrooms of Silicon Valley or the halls of Congress, the call for regulating AI technology is only getting louder. As we enter 2024, the focus on AI-based regulations in the U.S. will come from the Executive Order signed by President Biden in October. This order, called the Executive Order on the Safe, Secure, and Trustworthy Development and Use of Artificial Intelligence, builds on the administration’s Blueprint for an AI Bill of Rights from last year. The order lists eight guiding principles for the responsible development and use of AI – including the importance of U.S. leadership in this field as well as both support for American workers and protections for American consumers.

The order also set out a series of regulatory requirements that range from establishing AI safety and security standards to the importance of fostering innovation to concerns about human rights and equity. In their review of the executive order, Foley & Lardner analysts Millendorf, Allen, Moore, Barrett, and Zhang note that while it could set the stage for “potentially rigorous regulation,” the order also makes it clear that “the administration is not shy about their desire to promote competition.”

Meanwhile in Europe, we soon will have the chance to see the implementation of the European Union’s enactment of the AI Act. Unlike policy in the U.S., the EU’s AI Act is set to become law early next year. The AI Act comes two years after the EU first proposed a regulatory framework for AI and will mandate new restrictions on the use of the technology. This will include greater transparency on how data is used. The Act also categorizes AI technologies in terms of risk, recognizing everything from “unacceptable risk” systems that involve cognitive behavioral manipulation or social scoring, to limited risk systems such as image generating or manipulating technologies.

There has been some criticism of the EU’s AI Act – for example, French President Emmanuel Macron expressed concern that the legislation could stifle innovation. But with final details hammered out this week, a new comprehensive framework for regulating artificial intelligence will be among the first big technology headlines of the new year.

Buy Now, Pay Later, Regulate Someday?

According to research from Lafferty, the international Buy Now, Pay Later market will top $532 billion in 2024. And observers of the Buy Now, Pay Later phenomenon – supporters and critics – have known for some time that tougher regulations were coming to the industry. The only question was when.

Is the answer, “next year”? In the U.S., the Consumer Financial Protection Bureau (CFPB) has been studying the BNPL industry since at least late 2021. As such, the CFPB has recognized a number of key benefits BNPL provides relative to traditional credit products, especially with regard to the absence of interest payments, ease of access, and simple repayment structure. At the same time, the agency has also acknowledged a number of potential issues: discrete consumer harms, data harvesting, and overextension.

At this point, much of the CFPB’s impact on BNPL has been minimal. And while some observers believe that regulation is inevitable, few see signs of any specific imminent changes to law or policy with regard to BNPL in the U.S. There has some concern at the state level, with state attorneys general voicing consumer protection warnings. But at this point, “study and recommend” seems to be the approach the agency is taking toward BNPL for the immediate future.

Unsurprisingly, the EU is significantly farther down the path toward regulating BNPL than the U.S. is. In September, policymakers revised their Consumer Credit Directive (CCD) which updated rules for consumer credit and roped in Buy Now Pay Later products for the first time. With regards to BNPL, the revised directive specifies the circumstances under which a given BNPL service falls under the CCD. It also mandates that those BNPL services that are within the scope of the CCD be “subject to license requirements and certain regulations regarding responsible lending.” The new stipulations in the CCD must be implemented into member state national law by the fall of 2025.

Will the Regulators Curtail Crypto’s Comeback?

The price of Bitcoin is up more than 148% year-to-date. Ethereum is up more than 90%. Even the lowly Dogecoin has gained more than 35% from the start of the year through mid-December. After a slow start, 2023 is turning out to be a great year for cryptocurrency asset prices.

So will the regulators show up to take away the punch bowl?

Once again, the EU is the first mover when it comes to major regulation of enabling technologies in fintech. Next year, the EU will implement the Markets in Crypto Assets regulation – also known as MiCA or MiCAR. The first instance of a regulatory body establishing a comprehensive set of regulations for cryptocurrencies, MiCA was established in June. The regulations set new rules for stablecoins, including e-money tokens; require authorization for certain types of services provided by companies deemed crypto-asset-service providers; and introduce new rules to prevent market abuse via unlawful disclosure, insider trading or other activities “that are likely to lead to disruption or manipulation of crypto-assets.”

In the U.S., 2023 seemed like the year when regulators were doing everything they could to make life miserable for the cryptocurrency business. But 2024 could bring better news for the industry in the form of rule changes like the one recently made by the Financial Account Standards Board (FASB). This rule change allows institutions to represent their crypto holdings at fair value beginning late in 2024. Under current accounting rules, cryptocurrencies suffer from something called impairment.

This occurs because of the imbalance between how cryptocurrencies are recorded when they lose value as opposed to when they regain value. According to one observer, TradeStation Head of Brokerage Solutions Anthony Rousseau, this change gives corporate treasurers a potential way to include cryptocurrencies like Bitcoin to their balance sheets as a reserve asset. And as we’ve seen with the emergence of crypto ETFs in 2023, institutional adoption of crypto is one of the key leading indicators for potentially greater adoption of crypto throughout society.

ERM announced that it will integrate its ESG screening engine, ESG Fusion, with data from SESAMm.

The integration will enable ESG Fusion to screen an additional 20 billion documents and four million sources for ESG-related adverse events.

Headquartered in France, SESAMm won Best of Show in its Finovate debut at FinovateEurope 2022.

Sustainability advisory firm ERM announced a data partnership with Finovate Best of Show winner SESAMm. ERM will integrate data from SESAMm into its ESG screening engine, ESG Fusion. The result will boost the number of documents ESG Fusion screens for ESG-related adverse events by more than 20 billion and increase the number of sources by more than four million. The integration will also add to the engine’s coverage of languages, bringing ESG Fusion’s language coverage total to more than 100.

“A recurring challenge we see in the market is the capability to feed a state-of-the-art ESG methodology with extensive amounts of up-to-date raw data at pace and scale,” ESG Fusion Product Lead Marcel Leistenschneider explained. “Any informed ESG assessment must be built on as large a data foundation as possible. With this new partnership, we can confidently say that ‘if there is evidence on a company’s ESG performance out there, we will find it.”

ESG Fusion leverages AI to consume large amounts of unstructured data. Via a robust screening and analysis process, the engine transforms the data into an ESG Fusion report that is both intuitive and insightful. To ensure accountability, each report undergoes a review by an ERM expert before being distributed to customers. The new data capabilities from ERM’s partnership with SESAMm will enable ESG Fusion to reproduce “high-quality, outside-in-reports at scale on almost any company worldwide,” according to M&A Advisory Services Global Lead Andrew Radcliff.

In addition to ESG-related adverse events and controversies, ESG Fusion also provides assessments of industry-inherent risk of any given company. The technology also offers an assessment of the company’s management performance with regards to ESG issues, particularly disclosures.

Founded in 2014 and headquartered in Paris, France, SESAMm made its Finovate debut at FinovateEurope 2022 in London. At the conference, the company won Best of Show for its demo of TextReveal, an alternative data platform that leverages SESAMm’s Natural Language Processing powered engine to provide daily sentiment and ESG data mapped to public and private companies.

Earlier this year, SESAMm announced a partnership with Compass Financial Technologies to build a thematic index for cryptocurrencies. In July, the company announced that it was integrating Generative AI into its platform to enhance ESG risk mitigation. SESAMm has raised $54.5 million (€50.5 million) in funding, most recently securing $37.7 million (€35 million) as part of an overall $45.8 million (€42.5 million) Series B round. Sylvain Forté is co-founder and CEO.

Looking to demo your latest fintech innovation? Applications are now being accepted for demoing companies at FinovateEurope in London, February 27 and 28, 2024. Visit our FinovateEurope hub for more!

“Fired up and ready to go” is not just for political campaigns any more. According to a new survey from Ernst & Young, that sentiment aptly describes the attitude of a growing number of leaders in financial services when it comes to their eagerness to deploy artificial intelligence (AI), particularly generative AI (GenAI).

How eager? According to Ernst & Young’s 2023 Financial Services GenAI Survey, “nearly all (99%) of the financial services leaders surveyed reported that their organizations were deploying artificial intelligence (AI) in some manner. All respondents said they are either already using, or planning to use, generative AI (GenAI) specifically within their organization.”

Given the popularity of AI and GenAI, overwhelmingly positive responses like these may not be surprising. The FOMO in this field is reminiscent of the dot-com gold rush of more than two decades ago. After all, are many of the companies appending “ai” to their names that much different from their predecessors who donned “.com” back in 1999? Today’s eagerness has a similarly fearlessness. In the EY survey, expressions of anxiety and skepticism about the potential impact of GenAI on their business were few at just over one in five. For what it’s worth, insurers were the most nervous; bankers the least.

Other color pops in the EY Survey included “feeling supportive and optimistic about using AI in their organization” (55%), seeing GenAI “as an overall benefit to financial services within 5 to 10 years” (77%), and believing AI will improve the customer and client experience (87%).

The survey did reveals discontents. And within these discontents are potential opportunities for fintechs, especially those involved in the “picks and shovels” of the AI gold rush. Respondents to the tune of 40% reported that there was a lack of proper data infrastructure for successful deployment of AI solutions. And with regards to technology infrastructure, the survey noted that 35% of respondents believed there were still significant barriers. EY Americas Financial Services Organization Advanced Analytics Leader Sameer Gupta spoke to this problem, noting that while “generative AI holds the potential to revolutionize a broad array of business functions … with each new wave of AI and analytic innovation, it becomes increasingly clear how important it is to have a tech stack with a solid foundation.” Gupta added that it is critical for legacy data and technology to be “unimpeachable” before introducing AI.

Another challenge is talent. The mainstream conversation on AI still orbits concerns about AI-induced job losses. But the real job challenge with regards to AI right now is finding enough people qualified to implement AI-based solutions. “Our data showed that 44% of leaders cited access to skilled resources as a barrier to AI implementation,” EY Americas Financial Services Accounts Managing Partner Michael Fox said, “but there’s only so many already skilled professionals in existence.”

Fortunately, leaders seem to be embracing an AI-enabled future, making it that much more likely that these challenges will be met and overcome. In our own informal surveys with financial professionals, we have learned that buy-in from leadership is seen as key – for everything from DEI initiatives to digital transformation. And it is no surprise that EY has a role to play in making sure this is clear to its financial institution partners. “We like to take an ‘innovation intelligence’ approach to putting artificial intelligence to work,” EY Americas Financial Services Innovation Leader David Kadio-Morokro explained. “Planning, education, and an agile test and learn strategy for implementation are imperative for those looking to make the most of AI’s potential benefits.”

Conducted in August, the 2023 Financial Services GenAI Survey queried 300 financial professionals at the level of Executive or Managing Director or higher. All respondents worked at financial institutions with more than $2 billion in revenue. Organizations in banking, capital markets, insurance, wealth management, and asset management were surveyed, with 100 responses per sector collected.

SumUp has raised $306 million (€285 million) in combined equity and debt funding.

The round was led by Sixth Street Growth. Bain Capital Tech Opportunities, Fin Capital, and Liquidity Capital also participated in the investment.

The funding round does not change SumUp’s valuation which, as of June 2022, stood at $8.5 billion (€8 billion).

London-based fintech SumUp has secured $306 million (€285 million) in growth funding. The round was led by Sixth Street Growth and featured participation from Bain Capital Tech Opportunities, Fin Capital, and Liquidity Capital. The company will use the funding, which includes a combination of equity and debt, to support international expansion.

The round reportedly does not change the company’s most recent June 2022 valuation of $8.5 billion (€8 billion). It follows SumUp’s announcement of a $100 million credit facility from Victory Park Capital earlier this year.

In a statement, SumUp CFO Hermione McKee credited the merchants on the company’s platform – more than four million strong – for the company’s growth. “(It) is a direct result of the success of the traders we serve and would not be possible without the unwavering trust and support of the investor community,” McKee said. “This funding gives us additional firepower to pursue growth opportunities and accelerate products that empower small businesses.”

Founded in 2012, SumUp provides businesses of all sizes with affordable payment products and financial services. The company won Best of Show in its Finovate debut at FinovateEurope in 2013, and has since grown into a major payment solutions and point of sale systems provider active in 36 markets around the world. These markets include Australia, where SumUp launched in August.

More recently, the company introducedTap to Pay on iPhone for SumUp customers in both the U.K. and the Netherlands. This enables SumUp merchants to accept all types of contactless payments using only an iPhone and the SumUp iOS app. No additional hardware is required. SumUp sees the offering as ideal for new and smaller merchants looking to potentially scale their businesses and broaden payment options for customers. SumUp Senior Strategic Growth Manager Giovanni Barbieri underscored the technology’s ability to support financial inclusion. “I am especially pleased with the exceptional functionality of the product and the fact (that) it lowers barriers to entry, with the potential to fuel entrepreneurship.”

This spring, SumUp launched its multi-product subscription offering, SumUp One. The new solution amalgamates the company’s product suite in a single, unified solution for merchants. SumUp One initially launched in Italy and the U.K.