This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

We are all familiar with the challenge businesses have when it comes to new customers. On the one hand, there is an urge to onboard as many new customers as possible. On the other hand, great care must be taken to block bad actors or, in the case of the lending business, to avoid borrowers who are unlikely to repay their loans.

To help companies manage this tug-of-war, innovators in the credit scoring space have developed new strategies for determining credit-worthiness. These new approaches have moved beyond traditional credit scoring to help lenders reach reliable borrowers who may have thin credit histories – or even no significant, traditional credit history at all.

VantageScore is one such innovator. This year at FinovateFall, we caught up with Rikard Bandebo, VantageScore Executive Vice President and Chief Product Officer to talk about the company’s approach to credit scoring, how it differs from traditional credit scoring methods, and how fintechs can leverage VantageScore’s technology discover more “newly lendable” customers.

On making credit scoring more accurate and more inclusive

We went back to the drawing board in a way to look at what we could do to make these models much more accurate and inclusive. In doing so we started looking at ways we could look at the data on the credit file. We began using what’s called trended data and found, in doing so, we were able to improve the accuracy of the model significantly. It’s probably one of the most accurate, if not the most accurate, generic model that’s been widely adopted.

Secondly, we also found that by using this type of data we got much more consistent scores for consumers over time. There’s nothing quite as frustrating for consumers and lenders (than) when their scores go up and down a lot over time. So this provides a much smoother transition throughout a consumer’s history.

And the third piece is that we were able to massively improve our inclusion with this latest model. We score about 37 million more consumers than traditional generic models that are out there – out of which more than 10 million are above 620.

On transitioning to VantageScore from other credit scoring providers.

First and foremost, we are a very transparent credit scoring company. We provide a lot of transparency into how our models work (and) what impacts different activities have on our models. We also have built out great support services around migration and also around governance. We do a lot to make it as easy as possible for both fintechs and lenders to make a transition.

On VantageScore’s reputation in the capital markets and among ratings agencies.

We recently had FTI Consulting conduct a study where they went out and interviewed and tried to understand what the appetite was like in the broader market, what they were looking for. One of the common feedbacks they found was that, like other markets, they’re looking for more competition, and they’re looking for the best models that they can use to understand the impact of different types of consumers on risk.

We’ve actually seen a big uptake in VantageScore being used in general, and we’re seeing now a growing appetite in the securitization markets. We’ve seen some very large lenders transition to now offering their securities based on VantageScore.

Tampere, Finland-based ReceiptHero is on a mission to make meaningful interactions from every day transactions.

The company’s platform combines digital receipts with loyalty programs and benefits to give merchants new ways to engage with their customers. Consumers benefit from an integrated solution that relieves the burden of paper and email receipts, as well as the hassle multiple loyalty cards and apps.

We caught up with Chris Moore, Chief Operating Officer with ReceiptHero, to talk about how far the company has come since its Finovate debut in 2020, and the role ReceiptHero plays in the emerging data economy. We also talked about the company’s recently announced partnership with Ingenico.

You made your Finovate debut at FinovateEurope 2020 in Berlin, Germany. What was that experience like?

Chris Moore: Wow, that feels like a decade ago! Back then we were a very small team and had just released our Nordea bank integration. We had also started to systematically onboard our first batch of Finnish merchants to the platform. The feedback we got from the demo was fantastic; it really felt like we were solving a global problem and not just something we had been talking about here in Finland. You could argue pitching at FinovateEurope was the catalyst to where we are today.

Later that year you secured two million dollars in seed funding. What did that investment say about your company at the time and how did you put the capital to work?

Moore: The seed funding also solidified we were fighting a problem big enough. We picked some great Nordic investors and they’ve provided more than just capital since the investment. Essentially, the funding was to grow the platform and increase our sales efforts in the Nordics, but also to (expand) into other markets, such as Switzerland and the U.K. and put capital towards our POS integrations which are a key part of getting the receipt data flowing from the retailers.

Last fall ReceiptHero partnered with Mastercard and Visa. How did these partnerships come about and what was accomplished through them?

Moore: These partnerships came quicker than we expected. To partner with both Visa and Mastercard at the seed stage was a huge milestone for us. But we also knew that tackling the digital receipt problem would only happen if we had global partners such as the two major card schemes. The partnership with both Visa and Mastercard allows us to move into new markets in Europe with less dependence on local payment providers and therefore fewer integrations before being able to launch our solution. So it was a really big win with regards to scaling the platform and providing confidence at the highest level to support our objective of removing paper receipts as the main method of proof of purchase. I don’t think these partnerships would of been possible without our great development team building out a PCI DSS compliant platform, emphasizing our commitment to safeguarding cardholder data and providing the best possible receipt platform on the market today.

Speaking of Visa, you’ve recently strengthened your relationship with the company. How so?

Moore: Visa has seen increased client requests and interest in digital receipting over the last 18 months and, for a while, they have been trying to find a European partner who can enable such a solution. Building on the technical partnership from 2021, this new agreement puts us in the shop window as an approved partner for Visa’s clients and partners. We are already seeing the benefits of being involved in Visa’s Fintech Partner Connect program and we hope we can announce something soon off the back of this strengthened relationship.

You have talked about the idea of the data economy. In what way is ReceiptHero a part of this data economy – and what role does it play within it?

Moore: We are surrounded by data in our daily lives, most of it is unstructured and in hard to reach places. Receipts printed on paper are just that: unstructured and, as a customer, it’s hard to apply that purchase data to good use. Part of my opening remarks at FinovateEurope was that we are showered by amazing digital payment innovations and sadly the post purchase experience has mainly been left to stay in the analog world. Purchase data is core to building a strong data economy, as this data has so far been siloed and in a format that is hard to receive in real-time. It’s not really been leveraged or valued as it should be. ReceiptHero is breaking down those silos and enabling a world where a consumer can have this data instantly in their banking app or in an approved service where the data is used to better the customer experience.

Part of our unique role in fighting for digital, structured receipts is that we have a fiduciary duty to the data that flows through our platform to use it in a way that benefits all ecosystem stakeholders. We have no ulterior motive here; we are not a bank, a large retailer nor the cash register or payment provider enabling the sale. This allows us to act with the best interest of all stakeholders and help everyone to better utilize this new found digital data for the cardholder and the merchant.

ReceiptHero also plays a role in the trend toward sustainability and responsible consumption. How important has this been to you and to your customers?

Moore: For large retailers that print hundreds of thousands of receipts a day, what happens when you turn off all the receipt printers in your stores nationwide and only send customer receipts via digital channels? What are the impacts to your business from a cost perspective – but also the environmental repercussions? Simply put, less trees get turned into wood and then into paper, which then would have found their short existence as thermal receipts that sadly cannot be recycled due to the harmful chemicals on the paper. Take that scenario and then multiply it across thousands of retailers right across Europe (and, at some point, globally). That becomes a significant change in our fight for sustainability and better digital experiences.

What can you tell us about the fintech industry in Finland that those outside of the country – and the region – might be surprised to hear?

Moore: Well, I have personally been in Finland for 10 years now and I’ve seen the fintech space grow year over year. Sweden has always been a few steps ahead with regard to fintech unicorns, but Finland has now quickly caught up. We have a great ecosystem here where banks seek to innovate and look for fintechs to speed up those embedded features. Now we have unicorn successes such as Enfuce and AlphaSense in Europe. I also think the VC space is heating up with regards to fintech funding, with lots of appetite for investments in young ambitious fintech companies.

You introduced a loyalty rewards solution this summer. Why this move now – and how has the early reception to the new feature been?

Moore: Distributing digital receipts in real-time is the very foundation of what can be built with this data. What we wanted to prove is what happens in adjacent segments when you get this data and wrap a lightweight loyalty solution around it. We’ve started to onboard our SME merchants onto the rewards program, and so far it looks like we’re able to provide even more value to the merchant and the cardholder. For larger retailers where they might already use a loyalty platform, we can enable real-time card-linked receipt data to give them better visibility over repeat spend, lifetime loyalty, and average basket size.

You’ve also announced that you will be joining Ingenico’s new PPaaS platform. What can you tell us about this partnership?

Moore: We’ve announced this week that we’ve signed a partnership with Ingenico, one of the world’s largest payment terminal providers and now part of the Worldline group. PPaaS is Ingenico’s new payment platform that enables a “one-to-many” integration for us, so we can enable our digital receipt solution for thousands of acquirers, another partnership that supports us to scale across Europe. What’s exciting about this partnership is that we can onboard cardholders from the payment terminal, allowing another entry point to receive digital receipts for customers.

What else can we expect to hear from ReceiptHero over the balance of 2022 and into 2023?

Moore: Well, we’ve got some important retailers coming to the platform over the next six months so we’re really excited to announce those in due course. These are retailers that operate across multiple markets and more signs of us expanding further into Europe. There will be some bank partnership news too, but I wont give anymore away on that just yet!

What is venture capital doing to help promote fintech innovators who come from underrepresented groups and communities?

We caught up with Elizabeth McCluskey, Director of The Discovery Fund at CMFG Ventures, to talk about her work in supporting underrepresented entrepreneurs that are building solutions to drive financial inclusion.

We discussed her own extensive experience in financial services, working in both investment banking and wealth management before moving to venture capital. We also learned why she believes it is important to invest in female founders and founders from communities that are underserved by traditional financial institutions.

Why did you decide to transition from investment banking and wealth management to venture capital? What do you enjoy about working at a venture capital firm?

ElizabethMcCluskey: Investment banking is transactional. I enjoyed being part of transformational deals for companies but missed being there for the long-term impact. When I pivoted to wealth management, I was able to develop more longevity in client relationships, but the investments were focused on public equities with which I had minimal connection. These experiences led me to find the ideal balance in venture capital. Now I can build more intimate relationships with portfolio companies and invest in people and ideas that are meaningful and important to me. It brings joy and satisfaction to support their long-term growth and success.

Tell me more about your current role at CMFG Ventures and the Discovery Fund.

McCluskey:CMFG Ventures is the venture capital arm of CUNA Mutual Group. CMFG Ventures invests in fintechs to help financial institutions grow and provide a brighter financial future for all. The firm adds value to fintechs by leveraging its well-established network of over 6,000 financial institutions and suite of complimentary technology solutions. Since 2016, CMFG Ventures has invested in nearly 50 fintech companies and its Discovery Fund has invested in 14 additional early-stage companies led by BIPOC, LGBTQ+, and women founders.

I am the director of the Discovery Fund. The Discovery Fund was created to support underrepresented entrepreneurs who are building solutions for financial inclusion. We plan to invest $15 million over the next three years in early-stage fintech companies. Through my role, I’m able to see the full scope of venture capital investing, including but not limited to:

Sourcing deals and meeting entrepreneurs

Conducting due diligence

Negotiating the terms of the deal

Providing long-term support for entrepreneurs’ journeys by helping them scale, network, and find the resources they need to continue to succeed.

Why is it important to invest in diverse founders, especially women-led businesses? And what qualities you look for when investing in these companies?

McCluskey: Women entrepreneurs receive less than 3% of venture capital funding. This staggering number demands that we take a step back and focus on supporting diverse founders, especially women-led businesses, to improve equity in the venture capital space. This is not just the right thing to do – it’s good business. A 2018 BCG study concluded that women-founded businesses yielded two times as much revenue per dollar invested as those founded by men.

Women and diverse founders who have been historically underserved by traditional financial services are working hard to create the financial inclusion they wish they had. We are investing in entrepreneurs like them who are deeply connected to the problems they’re solving. Empowering underrepresented leaders is already creating new opportunities for liquidity management, wealth management, credit access, asset protection, and more.

Can you share more about the women-led businesses that CMFG Ventures invests in and supports? How are they helping make the financial services industry more inclusive?

McCluskey: CMFG Ventures has made investments in multiple women-led companies, such as The Beans, Climb, Caribou, and Frich to help the financial services industry become more inclusive.

The Beans simplifies the path to financial balance through evidence-based design and cutting-edge technology, so consumers stress less about money and focus on what they love.

Climb is a student lending and payments platform intended to make career education more affordable and accessible.

Caribou enables financial advisers to engage their clients in healthcare planning to support life transitions and build stronger financial futures.

Frich makes money social. It helps Gen Z develop better financial habits leveraging the power of community and benchmarking.

These female-driven fintechs are transforming the financial services space and improving the financial lives of everyday Americans.

What advice do you typically share with women founders? What about those looking to break into the VC space?

McCluskey: I would give the same advice to women founders as I do with men: always ask for feedback, especially to better understand why someone is telling them “no”. Founders who send updates over time allow me to track their progress, including growth and consistency of their business plans. In several cases, I’ve ended up investing in companies that I passed on in earlier rounds. And even if someone says “no” to doing business together, they can still be a valuable ally. Attempt to stay in touch and leverage their networks. People are often willing to share their connections and provide valuable guidance.

As for those looking to break into the VC space, I believe it is slowly becoming more inclusive and representative, yet it is still a very network-based profession. Similar to my advice for entrepreneurs, start with one person you know (or cold outreach via alumni networks, common interest groups, etc.). From there, ask every person you talk to for an introduction to at least one other person. Focus on growing your network with the goal of building genuine relationships, not necessarily getting a job right away. This is a long-term investment in your career.

We’re more than halfway through the 2022, what do you predict for the rest of the year?

McCluskey: After record levels of investments in 2021, we all knew things had to cool off. However, I believe the pace at which this has happened surprised VCs and entrepreneurs alike.

In fact, startup funding has fallen by 23% over the last 3 months, bringing us back to 2019 levels. For many, it probably feels like the sky is falling, but there is still a significant amount of money in circulation. Venture capitalists today, and by extension founders, are more focused on “real” metrics versus vanity metrics when deciding which companies to fund. The companies that will do well in the second half of the year will have measurable revenues, not just wait lists, and will be managing costs and runway to drive profitability, not endless cash burn.

Launched in 2019, Piermont Bank aims to blend the best of modern banking and agile fintech. Piermont Bank’s peer banking approach provides customers with technology-enabled, human-delivered solutions, opting for dedicated bankers over “1-800 numbers or chatbots.”

Last month, Piermont Bank celebrated three years of innovation. The woman-founded and entrepreneur-led financial institution currently has more than $420 million in total assets, and offers an end-to-end, digital banking-as-a-service platform with more than 40 fintech clients already onboard. More than 50% of Piermont’s loans since inception have been made to low- and moderate-income communities, as well as women- and minority-owned businesses.

The genesis of building Piermont was actually really simple. A lot of entrepreneurs would tell you they had this grand vision. For me, it was actually just very two practical reasons. The first was seeing the impact and the speed of impact that fintechs were making on consumer banking … The second reason was: I’ve been in banking for 26, 27 years. (And I’ve seen) the same pain points repeatedly from both the customer (side) as well as internally as an operator … So basically I said, “Okay if I could start with a blank slate, how would I build this? How would I build a fully digital-native, totally tech-enabled bank to do commercial banking faster and more efficiently?

On the evolution of financial services in recent years

My industry, historically, doesn’t change. It doesn’t go that fast. These days, I say that if the CEO is still working off their three-year strategic plan, if it’s in their third year, the board should fire that person. I mean, are you still even relevant in terms of your products (or) the way that you’re delivering these products? So I think the biggest change is just the speed, the speed of change, the speed of innovation.

I was taught and it’s still true banking is a risk management business. So it’s a little bit counter-intuitive if you think about it, this so-called “innovation.” But you absolutely can innovate in a risk management business.

On the advancement of women into leadership roles in financial services

I find myself able to make the biggest impact in the day-to-day: hiring based truly on skill sets and meritocracy, being gender-blind, age-blind … I know that sounds weird but, as an executive, as somebody who is doing the hiring, as somebody who’s doing the promotion, if I can just say, is this person the best person for the job? That’s more than half the game. I know that doesn’t sound very inspiring or trailblazing, but it is actually the day-to-day that makes a huge difference. Empower women, give them the job opportunity, give them the opportunity to rise to the occasion. That’s how we get there.

If there were a Challenger Bank Hall of Fame, then rest assured that Anne Boden, who founded U.K.-based Starling Bank in 2014 and is the challenger bank’s CEO, would be prominently featured therein. As we learned in our conversation with Ms. Boden, her inspiration for founding the U.K.’s first digital bank was driven by both the opportunities presented by new technologies as well as a banking industry that was still significantly shell-shocked from the Great Financial Crisis of 2007 and 2008.

Headquartered in London, Starling Bank now has more than three million accounts and four different account types. Voted Britain’s “Best Current Account” five years in a row, Starling Bank maintains offices in Cardiff and Southampton, as well as London, and still has zero brick-and-mortar branches. Starling Bank secured its banking license from the Bank of England in 2016, launched its first mobile personal current account in 2017, and introduced the country’s first digital business bank account in 2018.

On the decision to launch a fully-digital challenger bank

(T)he banking sector, back in 2014, was still looking backwards. They were still looking at the financial crisis, trying to repair their balance sheets, trying to repair their financials, and they weren’t really looking forward about what they could do to improve customer experience or customer satisfaction. I went around the world, talking to big banks and talking to technology companies and asking what they were doing. I came to the decision in 2014: wouldn’t it be great to start a new bank? Wouldn’t it be great to have a new bank with all new technology, a different way of engaging with customers, being fair to customers? And here we are in 2022 and things have gone from strength to strength.

On the challenge and opportunity of digital transformation in financial services

Organizations have become far more fixated on minimizing the risk of change. “Let’s do small projects around the core. Let’s not change the core. Let’s make big decisions at the senior level. Don’t empower people.” But in order for big banks to be more successful and compete with the new startups such as Starling, they have to have new technology, but above all a culture of being prepared to change. I am trying to empower people – the CTOs, the CIOs – to knock on the door of the CEO and say: “We can be better. We can embark upon technology projects. And we can compete with the new guys.”

On the present and future of Starling Bank

In the U.K. we’re very, very successful. We’ve built a whole new technology stack. We have a new banking license, three million customers, (and) we have something like eight percent of market share in business banking. That is huge. We’ve done in three years what some banks have done in 300. But that’s because we have this remarkable technology stack which we call Engine, and we have lots of banks around the world asking us if they can use Engine. We don’t plan to get a banking license in the States, but banks in the States will be able to use our Engine technology. So we’re going to be software-as-a-service, based on Engine, so lots of businesses around the world can have a bit of the Starling magic.

The world of banking is ever-evolving, and NCR has been part of this evolution since it was founded in 1881.

To get some insight from a firm that has had a front-row seat to industry changes– and to get a glimpse of what’s next– we spoke with NCR Chief Product Officer Erica Pilon. She has spent more than 20 years in the fintech industry, having also spent time at FIS managing three unique digital banking platforms.

What products and technology are resonating with NCR’s 600+ institution clients?

Erica Pilon: Our clients are really responding to data enhancements, crypto, and self-service support. Consumers today expect all interactions to be hyper-personalized, which is impossible without real-time, reliable data. At NCR we are helping financial institutions personalize banking experiences for customers at scale through enriched data and analytics. For example, we recently announced that Allegacy Federal Credit Union has partnered with us and Google Cloud for our data warehousing and analytics solution to make data actionable, unlock predictive insights, and drive innovation and financial health.

Another service resonating with our clients is the ability to offer buy/sell/hold of bitcoin within digital banking as it drives opportunities to build relationships, increase data insights, and generate revenue. Our clients have also shown increased interest in and excitement around enhanced self-service offerings, such as the Kasisto intelligent digital assistant, which provides human-like digital customer support.

What trends are making the largest impact in fintech in the coming year?

Pilon: Community financial institutions no longer only compete with the institution down the block but also with nontraditional threats like neobanks, big techs, and fintech providers. There is a new sense of urgency for financial institutions to provide modern, convenient experiences with robust, innovative products and services to retain customer loyalty, trust, and market share.

Open banking is a massive trend that is transforming the fintech space; it’s creating an opportunity for banking as a service and giving smaller fintech players the ability to try and steal market share from traditional institutions. To compete, banks and credit unions must work with partners that will help them stay open while continuing to leverage the significant trust advantage they have with customers and members. This is another reason why personalizing the experience within digital channels is so important; it helps community financial institutions retain their differentiator and compete with emerging threats.

How is NCR preparing itself for web3?

Pilon: We recently acquired LibertyX, a leading cryptocurrency software provider, which lays the groundwork for us to deliver a complete digital currency solution to our customers. This includes the ability to buy and sell cryptocurrency, conduct cross-border remittance, and accept digital currency payments across digital and physical channels.

NCR remains committed to delivering the agile software platform and services necessary for institutions to power flexible, efficient, and modern banking experiences across all customer touchpoints. Our platform is designed to help our clients quickly innovate and deliver new offerings to keep pace with emerging preferences and trends.

Howhas the recent consumer-first narrative changed how NCR develops its banking products?

Pilon: NCR continues to prioritize consumer-first, mobile-first experiences in our technology solutions. Now, in a world with so much optionality, banks and credit unions must be able to offer a wide range of choices for how consumers can conduct their banking. This means robust self-service capabilities with strong support options like video chat, as well as sophisticated physical footprints.

The consumer-first narrative is another reason NCR is so focused on data; banking interactions today must be personalized, or customers will quickly go elsewhere. This doesn’t just mean knowing basic details like names and birthdays, it also means being able to provide meaningful advice and guidance related to things like financial health and wellness.

How has NCR evolved to serve bank clients in today’s digital-first era?

Pilon: We firmly believe that digital-first doesn’t mean digital-only, but rather digital everywhere. This is where NCR is uniquely differentiated in the market; we have the ability to offer sophisticated digital solutions for both physical and digital touchpoints, enhancing the customer experience and increasing efficiencies. For example, we can facilitate the ordering ahead of cash or coin for small businesses or starting an account opening process online and then finishing it in the branch. NCR bridges the gap between physical and digital touchpoints.

The pandemic only emphasized what NCR and our clients have known all along: the future is digital, and it’s time to adapt. NCR remains dedicated to providing the flexible, innovative, and efficient technology needed to power excellent banking experiences and strengthen credit unions and community banks’ competitive positions.

In a digital world, there’s no way around digital identity. The topic touches all corners of fintech and ecommerce, and while it can create a stumbling block, leveraging consumer identity data can also hold great opportunity.

We recently spoke with Experian’s Kathleen Peters for her thoughts on digital identity and how financial services companies can use consumer data to their advantage.

Peters started her career as an engineer at Motorola and later moved into voice and messaging encryption technology. Eventually, she began working in Experian’s global fraud and identity business and now serves as the company’s Chief Innovation Officer.

The fintech industry has always struggled with digital identity. Why is digital identity so difficult to get right?

Kathleen Peters: A consumer’s identity is personal; every interaction and transaction requires their identity. Consumers expect a seamless and frictionless experience, but also rely on organizations to protect their information. The balance is crucial and challenging.

As an industry, fintech is known for creating compelling and personalized online journeys. But that experience can suffer if the fraud-prevention routines are perceived as burdensome by consumers.

Every year, Experian conducts a survey of consumers and business leaders, asking them about sentiments, trends, and other matters around fraud and identity. Year after year, the number-one consumer concern is online security. When transacting online, people want to know that their information is safe and secure. In striking a balance with consumers to instill trust, industry players need to show some sign of security that reinforces privacy.

Putting this balance into practice, if a consumer or business is performing a large online transaction, they want to see added layers of identity verification. Conversely, if they are performing a simple online purchase, industry players should not over-index with heavy-duty identity resolution (e.g., facial recognition, passcode) on low-risk, low-dollar transactions. In short, we need the right fraud‑prevention treatment for the right transaction; it is not a one-size-fits-all exercise.

It is important to know a customer’s identity for compliance reasons, but are there business use cases for this as well?

Peters: When it comes to KYC (Know Your Customer) compliance, you want to verify that you are dealing with a real person (not a made-up entity) and ensure that you are not dealing with criminals or people on watch lists. This is a basic compliance check and mitigates the risk presented by increasingly resourceful “bad actors” who have become very sophisticated in how they find and exploit vulnerabilities.

For commercial entities, especially small businesses, you want to know that they are a real business. You want to know that the principals involved in the business (the owners, board members) are not criminals or people on watch lists, or that the company itself is not somehow engaged in things that you do not want to deal with. In this sense, KYC applies to consumers and businesses alike in terms of a compliance check. There is a different level of compliance for consumers versus businesses, but the KYC concepts remain similar.

With KYC, businesses can check the box that indicates that “I am compliant.” That does not necessarily grow a bank, fintech, or online merchant’s topline revenues. Compliance is certainly a core element of identity, but so is identifying a potentially fraudulent transaction. For example, recognizing synthetic identity scams can prevent an organization from losing hundreds, if not thousands, of dollars in fraud losses.

When the concept of personalization was introduced in fintech, there was a lot of discussion of privacy concerns and fears that consumers would perceive banks’ efforts as “creepy.” Does this still exist today?

Peters: Our annual Global Identity and Fraud Report shows that people hold banks in high regard. They possess an especially strong degree of trust from consumers. Yet, unknown fintechs that may reach consumers through a banner ad or other similar means may not yet possess that same amount of trust. Building trust with consumers is critical, especially for fintechs, and it starts with transparency and reinforcing the value exchange.

What is the best way for banks and fintechs to build trust among their consumers?

Peters: Banks and fintechs need a layered approach to identity resolution that accommodates the balance between fraud detection and the online experience to build consumer trust early in their relationship. Establishing that trust should be a top priority and involves having visible means of security, being transparent about why you are collecting certain types of data, and delivering value for that data exchange (e.g., personalized offers, speed). And that value needs to be immediate and a tangible benefit, not a down-the-road promotion or assurance.

According to our Global Identity and Fraud Report, consumers are willing to give more data if they trust the entity and feel as though they are receiving value.

Once the value exchange is established, those feelings of trust and recognition lead to increased brand loyalty, a holy grail for banks and fintechs.

Given this, what are ways banks and fintechs can leverage consumer data combined with an increase in their trust to better connect with consumers?

Peters: Building relationships with consumers comes down to recognizing them, protecting their information and offering a personalized experience. Consumers want to feel confident that their online accounts are secure, and that they don’t need to jump through hoops to access the resources they need.

It comes down to identifying and understanding consumers and their needs. The best way to do that is with a lot of data. It serves as a vast resource to look at the multitude of behaviors historically and predict the next likely behaviors and intent. Predictive modeling like this can be hard to do, especially if you do not have a lot of historical data. However, with aggregated data, scores, and solutions from a provider like Experian, it can be a very powerful way to drive engagement.

For instance, if a consumer is in-market for a new credit card, banks and fintechs may want to engage their consumers with a personalized offer or increase dollar-value transactions—both ways to build trust.

As Pride Month draws to a close, we wanted to take a look at the impact that banks and other financial services companies have on LGBTQ+ communities.

The issues that face LGBTQ+ communities when it comes to financial services are as varied as these communities themselves are. They range from simply allowing cardholders to determine how they will be identified on their own bank cards, to healthcare-related savings and investment planning, to learning which financial institutions respect LGBTQ+ individuals and their values – as well as those institutions who work against them.

We caught up with Chris Luton, Director of Customer Care with Oakland, California-based Beneficial State Bank, to talk about the relationship between banks – especially community banks – and LGBTQ+ communities. We also discuss Beneficial State Bank’s efforts in this regard – as a “values-based bank” – as well as the bank’s own development as a community financial institution in the age of digitization.

Tell us about Beneficial State Bank. What makes you unique in your community?

Chris Luton: Beneficial State Bank is a for-profit, mission-driven bank whose owners are institutions governed in the public interest. Instead of working to maximize shareholder profits, we work to maximize prosperity for our communities and our clients, while maintaining strong business performance and serving as a model for ethical banking.

The bank was founded to serve a triple bottom line of environmental sustainability, social equity, and prosperity. The intention was to prove that this banking model could be sustainable, and influence the banking system to substantially change its practices.

All of these qualities differentiate us from most banks. For instance, we invest in and work with community organizations that are often turned away by traditional banks. We offer socially-conscious individuals, small businesses, and nonprofits the unique opportunity to put their money toward causes they believe in.

What does it mean to be a values-based bank?

Luton: This means prioritizing our values just as much as our profits, which is captured in our triple bottom line of environmental sustainability, social equity, and prosperity.

In practice, this means that our values guide our investment decisions. All of Beneficial State Bank’s investments are mission-aligned, and we aim for at least 75% of that lending to go toward the highest-impact organizations and initiatives. We then work to ensure that the rest never goes toward projects or organizations that cause harm.

For example, we invest in environmental sustainability, affordable housing, social justice, and health and well-being. Meanwhile, we never invest in fossil fuels, payday lenders, private prisons, or weapons manufacturers.

What can banks do to better serve and support the LGBTQ+ community?

Luton: Right now, some of the nation’s biggest banks fund anti-LGBTQIA+ policies through political donations. If the millions put toward these discriminatory policies were instead invested in organizations that protect and uplift the LGBTQIA+ community, banks could make huge progress in a more positive direction. For better or worse, money is hugely influential, especially in our political process. Banks could better serve the LGBTQIA+ community by leveraging this power for good.

Banks should also consider how their policies and practices impact their LGBTQIA+ customers and employees. At Beneficial State Bank, we strive to create a welcoming and inclusive customer experience — for example, we make it as easy as we can for clients to change their name and gender on any official communications.

Ultimately, it’s important that banks try to see the big picture on this issue by looking beyond performative celebrations during Pride Month. Members and allies of the LGBTQIA+ community are looking for more than just a rainbow logo or special blog post, and the community’s needs don’t suddenly end once Pride month is over. Support for the LGBTQIA+ community should last all year long. Companies should also look at their overall impact to see if it’s consistent with their messaging. For instance, they might claim to support the LGBTQIA+ community while funding discriminatory politicians or having discriminatory internal policies.

What changes do banks need to make internally to better support their LGBTQ+ employees?

Luton: It starts with building a welcoming and inclusive environment where employees feel safe and empowered to be themselves. We make an effort to hold space for connection among our LGBTQIA+ employees and their allies, and host Pride celebrations every year. Benefits and policies should also be inclusive. For instance, we make sure employees can add domestic partners and their children to their insurance plans, regardless of marital status.

How can banks help consumers make better banking choices that are aligned with their values?

Luton: The first step is transparency. Consumers can’t make better banking choices if they don’t know where their money is going. Unfortunately, a lot of banks aren’t transparent about where their money goes. Banks need to be honest about their investments so consumers can learn, engage, and make banking choices that are more aligned with their values.

Values-based institutions like Beneficial State Bank are upfront about our investments. For example, our goal is always for at least 75% of our commercial loan dollars to go to mission-aligned businesses – i.e., those working on issues like affordable housing or renewable energy. We also never lend in non-mission-aligned sectors, such as fossil fuel extraction, private prisons, or weapons manufacturing.

Mighty Deposits is a great resource for discovering how your bank is using your money, and what better options might be out there. Beyond the banking sector, Data for Progress has also released the latest version of its Pride Corporate Accountability Project, which looks at how many Pride sponsors and Fortune 500 companies are funding anti-LGBTQ+ campaigns.

Digital transformation is a big topic in banking. How has this trend impacted Beneficial State Bank?

Luton: A big milestone in our own digital transformation was the PPP lending process in 2020. We did a substantial amount of lending that required all hands on deck. This actually gave us confidence in bringing up a new platform quickly and effectively. Since then, we’ve improved our digital and online functions, increased efficiency and speed, and lowered our cost of delivery.

The bank also recently closed on an equity investment of $218 million from the U.S. Treasury’s Emergency Capital Investment Program (ECIP), which will support expanded lending to small businesses, and low- and moderate-income consumers. Our first priority is investing in the bank’s capacity so we can better serve our customers. This will include technological capacities like automation and infrastructure.

Where do you hope to see Beneficial State Bank in the next three to five years?

Luton: With this recent investment from the U.S. Treasury, we see the next few years as a time of growth and an opportunity to demonstrate the power of values-based banking. We see ourselves continuing our work with marginalized customers and communities on a larger scale, expanding our investments in people and organizations making positive change in the world, and influencing other banks to do the same.

Our ultimate vision is an economy that restores our planet and extends prosperity to all people. We can achieve this vision if more banks decide that doing good and doing well are not mutually exclusive.

Innovation and regulation are the ying and yang of financial technology in many respects. To this end, we caught up with Justin Beals, co-founder and CEO of Strike Graph, to talk about the relationship between fintech innovation and fintech regulation, and why compliance is something that successful fintechs are taking seriously.

Founded in 2020 and headquartered in Seattle, Washington, Strike Graph specializes in helping companies secure critical security compliance certifications. These are the certifications that can both impact revenue and reduce the time to close, as well as demonstrate the maturity of an organization.

Why banks and financial services companies need a compliance partner.

The challenge (for banks) is that the standards that you’re trying to meet can be complex. It’s important to not only have technology, but (also) a provider of that technology with intelligence about how to meet the standard so that you don’t essentially spin your wheels trying to do things that don’t necessarily make you more secure and don’t necessarily impact compliance.

So when revenue is on the line – and that’s what the challenge is here – being unable to represent a security posture that meets certain standards (means) you might not get that partnership, you might not get that contract … You really need to do it efficiently and effectively and be able to maintain it for a long period of time.

On the role an effective compliance partner can play to help financial services companies

I think one of the secrets about compliance practices is that if there’s some aspect of your business that isn’t applicable to the standard, you’re actually not required to be assessed to it. And so what’s really important is to customize your security posture according to the types of risk that your business is meeting in the marketplace, and then respond to those risks. Then, (you are) able to talk to the assessor and say, “hey, look, you know we don’t necessarily have this particular risk. It’s not something we solve for and therefore it’s not something we need to be assessed for.” That way you get through the compliance process as efficiently as possible.

On Strike Graph’s approach to helping financial services companies meet compliance obligations

The secret sauce at Strike Graph is that we have a very intelligent SaaS platform that helps our customers customize that particular security posture based upon the risks that are impacting their business.

This is impacting any B2B company that’s sharing data. And that’s really how we describe our marketplace. And, of course, fintech handles some of the most precious transactions and pieces of data, and they have a long history of things like PCI DSS where compliance is really important. So they really do understand the value of having a good compliance practice.

The fintech industry talks a lot about bank-fintech and fintech-bank relationships. Everyone in this industry will proudly declare how essential these partnerships are for everyone in the value chain. However, the recent introduction of crypto and decentralized finance (DeFi) is complicating things. How can a traditional financial (TradFi*) institution like a bank align itself with a DeFi startup or get involved in crypto?

For insight, we spoke with Sila CEO and Founder Shamir Karkal. Karkal co-founded Simple, one of the first digital banks, in 2009 and sold the company to BBVA in 2017. The following year, Karkal founded Sila, a company that offers banking, digital wallet, and ACH payments APIs to help companies integrate with the U.S. banking system and blockchain quickly, securely, and in compliance.

In our conversation, Karkal highlights the intersection between TradFi and DeFi and examines ways the two can work together while still regarding necessary compliance measures.

What are some ways you are currently seeing crypto businesses and TradFi organizations interacting?

Shamir Karkal: Unquestionably, crypto is becoming part of life. It is becoming part of everyday finance. We had a massive crypto boom in 2021 and now we are experiencing a crypto bust. But public markets and fintechs have performed equally as bad – or worse – than crypto. Over the last few years, traditional finance has been waking up to the crypto space. They take it seriously now.

During mid-to-late 2020, most TradFi organizations thought of crypto as a passing fad, a new dotcom boom. Today, there is no more dismissal of it. The top levels of large banks understand that crypto is here to stay – that it is an important part of the future of finance. Clearly, how this future will look in detail is still to be seen. Some TradFi organizations have embraced crypto whole-heartedly, such as Cross River bank and Silvergate bank, but there are also others still on the fence.

Crypto has scaled dramatically in 2021, which – ironically, some might say – has made crypto businesses appreciate traditional finance a lot more. They are not fans, not by a long shot. But, for example, they understand that compliance is not optional, and that one needs to comply with the law in one’s jurisdiction. As crypto businesses matured, reality has set in partially because when you‘re big, ignoring the law is not an option. In fact, crypto businesses often have a better understanding of regulations than fintechs. Because most answers are subject to change in the world of crypto, participants need to understand and follow very closely how things evolve.

Some of the largest TradFi organizations such as JPMorgan went as far as launching their own stablecoin (JPMcoin). All are going to have similar projects. In my view, big banks have no ability to compete head-to-head with anybody in the crypto space. However, they are perfectly positioned to provide services to the winners in the crypto space– to the big exchanges, the big processors. All of those firms need all the services that traditional finance provides. Providing financial services to crypto winners is where the money is to be made. The foundation of the future of finance is still the financial services that today are supporting any other businesses.

What types of partnerships do you expect to see in the future?

Karkal: To partner is in the interest of both crypto and traditional financial institutions. Crypto businesses are using traditional finance to broaden and speed up adoption of crypto services. True, a lot of people want to get into crypto. Still, everyone who does today has money in a bank account or a debit card. Even if your business is all about crypto, you need to create the bridge to allow people to move money from here to there.

When it comes to regulation, what do banks need to look for when partnering with crypto startups?

Karkal: In technology or crypto, it is often said that you need to look for teams who move fast and break things. That is not true in banking. Banks need to look for projects that have good teams, are well funded, and where teams have an understanding of the compliance issues they will face. Because you can only develop a plan to deal with problems after they are recognized. One key question to ask is, “Do you have an opinion from an experienced lawyer?”

My advice is to look for real teams with real people that are serious about a long-term relationship. Beware! There are plenty of scams out there. Don’t support people who are only interested in making a quick buck, or the next ponzi coin (a real thing).

Crypto is also fraught with fraud. There are many, many different types of fraud: fraudulent businesses, payments fraud, ACH fraud, etc. Banks have been combatting these issues longer than crypto businesses. They stand to know more about them and can help. The key is to identify crypto businesses that built out the necessary capabilities, and that get advice from the good lawyers in the space. That’s a good litmus test.

How can banks position themselves as good partners for crypto companies?

Karkal: The key is to figure out which products and services the bank is willing to offer. That sounds basic, but a bank has to ask itself if it is willing to service a crypto company. Is it ready to be their corporate bank? To do payment processing? To be a custodian for their funds, or their customers’ funds? After figuring out what a bank is willing to do, the second step is to go do it with some startups. Some banks act as if they want to partner with crypto businesses, but then their compliance processes are so onerous, it just won’t work. They end up standing in their own way. My advice is: if you’re serious, go do it with a couple of crypto companies first before making a big marketing push. If you’re successful, word will spread through Discord or Telegram channels. And, suddenly, you’ll find other projects and companies that will be coming to you.

Here is the rap. The question is really, “Can you get to the point of opening an account?” Remember: crypto businesses do not have the profile of traditional customers. It might come as a Delaware subsidiary of a company registered in the Cayman Islands with senior people sitting all over the world. As a highly regulated bank, what is your process for this setup? You need to figure out your compliance piece to make such a setup work.

I know of crypto businesses that are public companies abroad, are serious players, and yet have trouble opening corporate bank accounts in the U.S. As a bank, you need to understand that there is one thing crypto businesses don’t have: patience. They won’t wait 12 months while a bank’s internal committee rejects their application for the 13th time because they have a subsidiary in the British Virgin Islands that’s on a black list somewhere. You as a bank need to figure out this and related processes first, before your sales people are soliciting crypto businesses.

*TradFi refers to traditional financial institutions as well as fintechs.

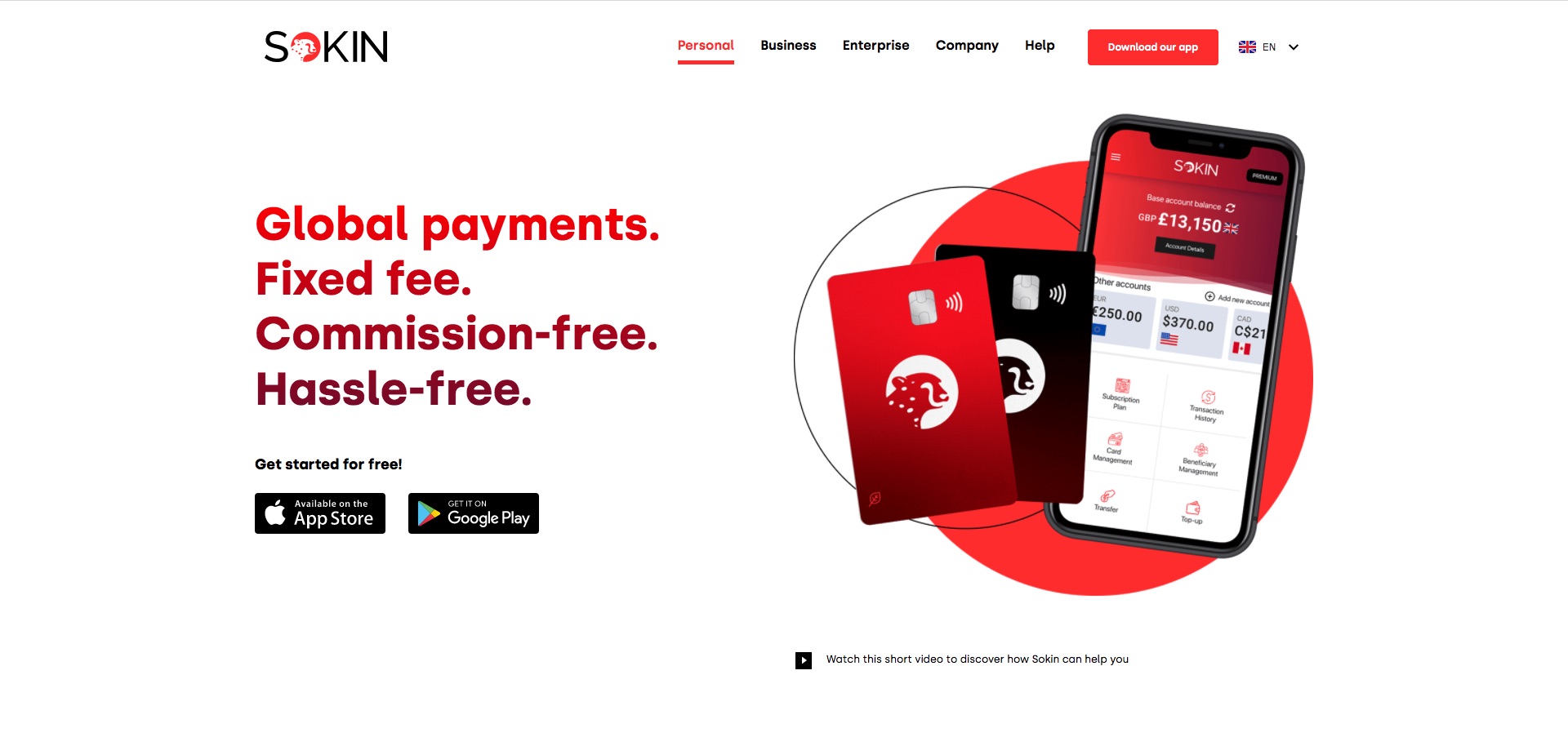

We recently caught up with Vivienne Hsu, Chief Communications and Marketing Officer with Sokin, a U.K.-based, global financial service provider and payments company. Originally slated for our Women’s History Month commemoration, our conversation includes both Hsu’s thoughts on “the State of Women in Fintech” and gender diversity in the industry, as well as her insights on Sokin, its contributions to fintech innovation, and what we can expect from the company in the future.

Joining Sokin in 2021, Hsu was previously co-founder and Partner at Anabasis Partners, an international marketing and communications advisory firm. Before that, Hsu spent more than seven years as an executive with Cognito, a London-based PR, marketing, and communications agency.

Can you tell us a little about Sokin and its place in the fintech industry?

Hsu: Sokin is a global payments fintech that is the first to offer a consumer subscription model for unlimited transfers for a fixed fee. We believe in straightforward, transparent currency exchange and money transfers and allowing as many people and businesses to have access to the global payments ecosystem. We are ethically conscious and focused on the positive impact we can have as a business, putting financial inclusivity and eco-friendly innovation centrally to our purpose while working to democratize and simplify the global payments process.

How long have you worked at Sokin? What do you enjoy most about being a part of its leadership team?

Hsu: I’ve been with Sokin since January 2021 and enjoy being part of a very fast-paced business that is constantly growing, innovating, and evolving. I’m surrounded by hard-working and exceptionally talented people where I continue to learn so much. The leadership team is experienced, grounded, and strategic, but also fun which makes being part of it such a privilege.

What are the biggest responsibilities you have as CCMO? Are there any accomplishments as Sokin’s CCMO that you are most proud of?

Hsu: The biggest responsibilities I have as CCMO is to build the Sokin brand and keep our name front-of-mind within the global payments and innovation industry. We have an incredible story to tell – one that really holds people at its heart – and great products and services to get out to market with.

I’m immensely proud of the team we have built and how quickly we have managed to scale the Sokin brand globally. We’ve nurtured our flourishing sports club partnerships very effectively and continue to enter new markets at pace with an extremely exciting proposition.

How has the pandemic impacted the work you do as CCMO?

Hsu: The global pandemic changed how we work, but not what we need to do to deliver it. If anything, the change in working environment has forced us to innovate and collaborate in new and diverse ways. For example, as a global organization with a workforce across the world, we do not let time zones or geographies hold back progress.

Being able to build a good team culture and the creative spark is the only area which has been harder to achieve as our people are not always together. But overall, it’s not negatively impacted my role or the work we do at Sokin.

How would you characterize the “State of Women in Fintech and Financial Services” in 2022?

Hsu: The industry has improved, but there is still a lot of work to do. When I started out, it was not uncommon for only one or two women to have a seat in the boardroom. This, of course, has changed due to a shift in workplace attitudes and, as a result, we are seeing more women than ever moving up the ladder. However, this must only be seen as the beginning. It’s still not an equal men-to-women ratio, but it’s getting better.

Evidently, more attention and emphasis have been placed on supporting women in the finance industry over the years. I have seen more female leaders and experts working in finance and fintech compared to 10 years ago. It’s wonderful to see the glass ceiling starting to crack and I hope it grows in momentum.

What do you think the industry is doing right in terms of promoting gender diversity? What do we need to do better?

Hsu: I think fintech and financial services are having the conversation and pushing the agenda for gender diversity, which is really the first step. We need to get to a point where equality is part of a natural and organic system, not a forced issue as it is now – much like a box to tick.

I hope in the coming years we will not have to talk about gender diversity in the same way we do now, but instead it becomes something that’s actioned without question.

What can you do in your role as CCMO to help advance gender diversity?

Hsu: I think I can help in my role as a CCMO – and also as a senior female leader – by setting a good example, supporting, and mentoring others and driving a strong DE&I team and agenda at Sokin. Being part of a progressive and innovative company helps immensely, but also we have a culture where everyone’s opinion matters and can be shared which really can drive quick and necessary change.

It’s also about giving women the opportunities they need to succeed. The best way to create a rope ladder for other people to climb is to include them in your own journey. I’ve been exceedingly lucky to work with lots of incredible people over the years who did just that. By doing so, they pulled the best out of me which I did not see in myself. Before I knew it, I was involved in activities which, to me, seemed impossible, but those around me saw things differently. I will always be grateful for this, and I hope I can support the talent of today in the same way.

It may sound simple, but by doing so you naturally open opportunities and further responsibilities for those in your team. Providing an accessible platform to learn is fundamental in supporting others through their professional careers, especially in fast-paced industries such as fintech in which there are an plenty of chances opening every day. It’s about giving people both the confidence and, most importantly, access to pursue them.

Sokin is involved in multiple new initiatives. What excites you most about the direction of the company right now?

Hsu: I’m most excited about how the company is innovating and the way we are building our ecosystem and partnerships. It’s unlike any other organization I have worked! Sokin is at the forefront of several innovations such as taking payments into the metaverse and web 3.0, alongside what we can do with our existing and new partners.

Having only launched our Global Currency Account in August 2021, Sokin has rapidly expanded into 32 territories, and welcomed more than 120,000 Sokin customers with a further 175,000 currently on the global waiting list. At the end of 2021, we had transferred over $100 million around the world, delivered a multilingual app with five accessible languages, doubled the size of Sokin’s global workforce, partnered with five top-class football clubs including our first NFL team, and launched our exclusive sponsorship community, Sokin – Money Goals. To achieve this in a matter of months is astounding.

In short, we are leveling up global payments with the ambition to become the provider of choice for global transfers and currency exchange around the world. And I wholeheartedly believe we can and we will achieve this.

Zilvinas Bareisis is Head of Retail Banking at Celent. Based in London, Bareisis specializes in consumer and card-based payments, as well as identity and authentication. He is especially interested in payments innovation, and what he calls “the perfect storm” of competitive, regulatory, and technology developments that are shaping the present and future of consumer payments.

Embracing the open ecosystem is a really big topic right now – from open banking to embedded finance. How do you innovate around products and how do you differentiate yourself? Banks are starting to talk about their purpose, how they embrace different communities they may be serving, and how they tailor their products to those communities. Even things like crypto (are important). Twelve months ago I didn’t think retail banks should be interested in crypto, and here we are talking about that now.

On the role of enabling technologies in financial services

You really need to have the right set of technology tools – and those tools are diversifying. It’s easier now to have composable building blocks that might be coming from different parties, platforms like low code and no code that do not require much IT capability so that business users can start developing applications and, of course, the cloud. A lot of our clients are looking into how to migrate to the cloud and how fast.

On the promise and potential of embedded finance

At the heart of embedded finance is the idea that customers are out there, doing their own things and, as they do those things, they realize that there might be a need for a financial services product, which is something they can acquire right there and then. The idea itself is not new; you and I have probably bought car insurance at the same time we bought our car at the dealership. What’s changing is that there are nice, big, sophisticated digital experiences, first of all, and it’s easier now for financial services to plug into those experiences because now the technology is catching up.

Check out the rest of our conversation with Zilvinas Bareisis from FinovateEurope 2022 on what’s next in the “new normal” in fintech and financial services.