This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

VersaBank is getting in on the digital currency game. The Canada-based bank announced plans to launch VCAD, its own cryptocurrency backed one-to-one by the bank’s Canadian dollar bank deposits.

Key to the launch is a partnership with Stablecorp, a joint venture between crypto asset manager 3iQ and blockchain development company Mavennet. Stablecorp will aid in the commercial launch of VCAD.

VersaBank plans to manage the digital issuance process using VersaVault. The issuance tool is a digital bank vault designed by Versabank subsidiary DRT Cyber to secure digital assets.

“VCAD provides consumers with not only the security afforded by an underlying deposit with a Canadian chartered bank but also the comfort of knowing that each VCAD issued or redeemed will always have one-to-one value with the Canadian dollar,” said Stablecorp CEO Jean Desgagne. “With such clear benefits, we are highly confident in the demand for VCAD as digital currencies increasingly become part of mainstream financial transactions.”

According to CoinTelegraph, VCAD is not the only stablecoin pegged to the Canadian dollar. Other Canadian dollar stablecoins available include Coinsquare’s eCAD and TrustToken’s TrueCAD token.

VersaBank aims to make VCAD publicly available “in the coming months.” In the future, VersaBank and Stablecorp plan to launch VUS and VEuro, which will be U.S. dollar and Euro versions, respectively, of the VersaBank digital currency.

Digital mortgage software provider BeSmartee has secured a strategic growth investment from Boston-based venture and growth stage investment firm M33 Growth. Terms of the deal were not disclosed. In a statement, the company said the capital will help accelerate growth of the Huntington Beach, California-based fintech, as well as power further product innovation.

Calling 2020 a “pivotal year for the mortgage industry,” BeSmartee CEO and co-founder Tim Nguyen underscored the value of a platform like BeSmartee’s in “driv(ing) higher volumes for and ROI to” customers. “We believe that M33’s investment and knowledge will help us to bring our product to more customers and continue to build out our capabilities,” he said.

BeSmartee enables banks, credit unions, and non-bank lenders to deliver a complete digital mortgage experience for their customers. The company offers a white-labeled, mortgage POS that helps lenders go to market faster (zero to POS in 30 days) and better compete with tech-savvy fintechs and marketplace banks. BeSmartee’s technology has been particularly helpful to bank and non-bank lenders alike during the COVID crisis, as lenders have moved “with greater urgency” to embrace digital mortgage options. BeSmartee has referred to this demand for POS platforms as “exponential.”

A Finovate alum since 2017, BeSmartee began this year teaming up with NOVA Home Loans, a Tucson, Arizona-based mortgage banker. Earlier this month, the company announced that it had achieved a 100% customer retention rate in 2020, a 91% customer conversion rate, and growth of 50% in its customer base. “We deepened our integrations with LOS partners, pricing engines, and document providers, along with numerous other integrations to deliver a better experience to our customer base,” BeSmartee Operations Manager Rick Johnston said. “The suite of new tools rapidly increased the rate of loan officer adoption and, in turn, skyrocketed lender ROI.”

Apex Clearing Holdings, a digital clearing and custody engine, announced formal plans to publicly list on the New York Stock Exchange under the ticker “APX.”

The Texas-based company is eschewing the traditional IPO route to a public launch, and instead pursuing the listing via a merger with Northern Star Investment Corporation, a special purpose acquisition company (SPAC). The deal values Apex at $4.7 billion.

Apex is the sixth fintech to use a SPAC to go public in the past few months, joining SoFi, BankMobile, Payoneer, MoneyLion, and OppFi.

“We are in the first inning of the digital revolution in financial services, and our merger with Northern Star will provide Apex with the resources and flexibility to accelerate our growth, scale our platform, and expand our offerings and market share alongside our clients,” said Apex Clearing CEO William Capuzzi.

Capuzzi, along with Apex President Tricia Rothschild, will continue to serve the company in their current roles. Northern Star Chairwoman and CEO Joanna Coles will join the combined company’s Board of Directors.

Apex was founded in 2012 and helps online brokerages, traditional wealth managers, wealthtechs, professional traders, and consumer brands with account opening and funding, execution of trades, digital asset movements, trade settlement, and the safekeeping of customer assets.

Apex has provided custody for $14 billion in new assets year-to-date and currently serves 200+ clients representing more than 13 million customer accounts. The company has already recorded impressive growth so far this year, seeing 3.2 million customer accounts and more than one million new crypto accounts opened in the past two months.

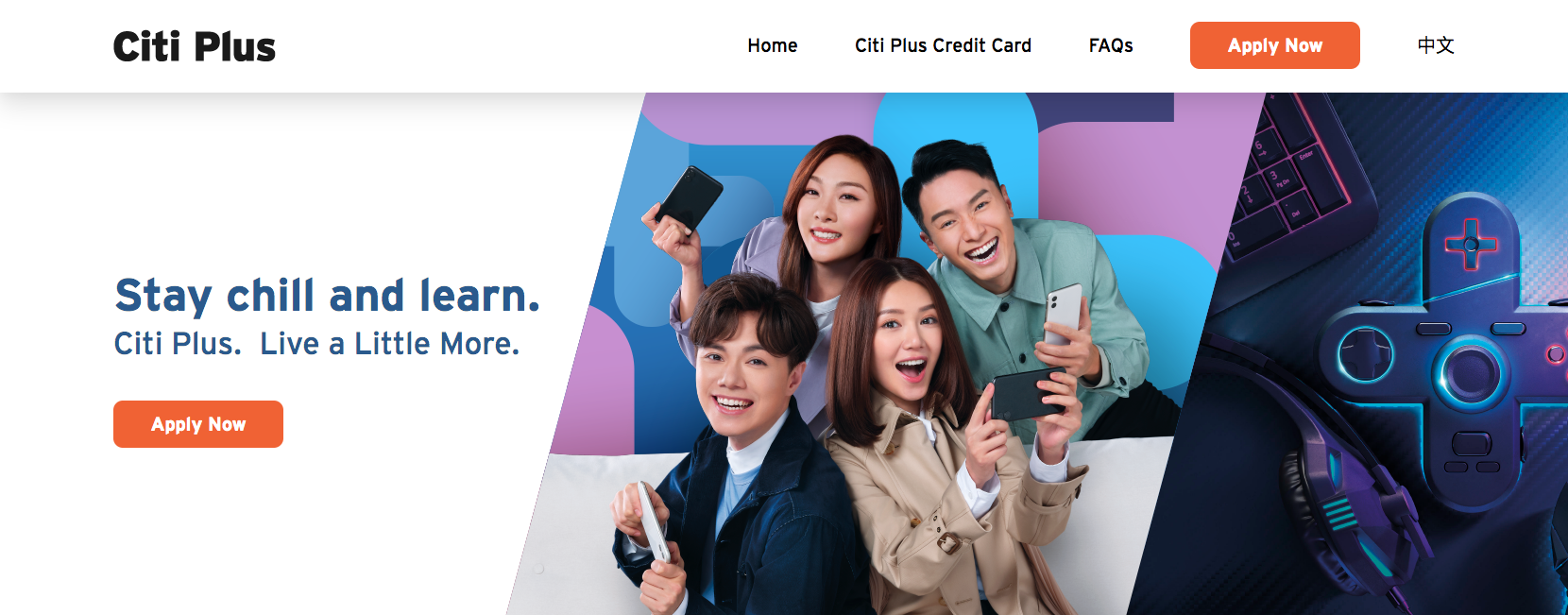

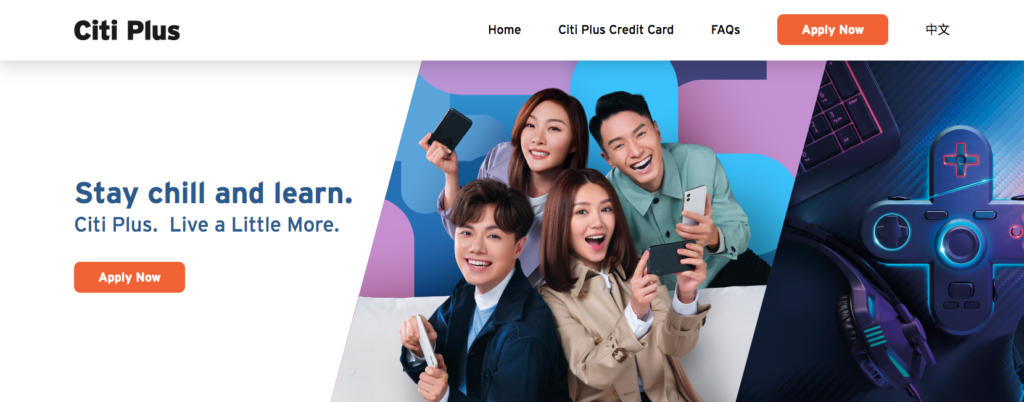

After piloting the product last year, Citibank Hong Kong formally unveiledCiti Plus, its mobile-first bank designed for digital natives.

The new offering aims to help users “level up” their banking experience by providing financial education, personalized wealth management tips, and easy access to a range of investment products.

“Citibank Hong Kong has shown strong determination in the development of digital banking in recent years. Citi Plus is our latest initiative to bring digital natives a banking experience they admire,” said Citibank Hong Kong Consumer Business Manager Lawrence Lam. “Millennials were invited to participate in research and the co-creation process, through which we could better address target clients’ pain points, and help them grow their wealth via the new service.”

The platform’s gamified user experience encourages users to build their wealth by accomplishing fun tasks. The Citi Interest Booster, for example, enables users to earn higher interest rate of up to 1.8% on their savings by completing what Citi calls “missions.” These missions include tasks such as maintaining a certain balance, funding accounts, investing, exchanging currency, and spending with their Citi Plus card.

In addition to the gamification element, Citi Plus will offer savings goals, debit and credit cards with built-in rewards, easy money transfer capabilities, and a low threshold investment platform. The investment opportunities include access to stocks, money market funds, and mutual funds from Aberdeen Standard Investments, Allianz Global Investors and Franklin Templeton.

In the first three weeks after the pilot launched, Citi received 5,000 registrants interested in Citi Plus, which is open to Hong Kong residents only.

The millennial-friendly user interface and marketing, combined with features such as low-threshold investing, financial education tools, and high interest savings accounts, help Citi compete with the increasing number of challenger banks and neobanks that are enticing young users. Unlike this group of digital banks, Citi has a slight upper hand. That’s because the bank not only has a robust existing user base from which to draw new clients, it also has an established reputation and inherent consumer trust.

In a round co-led by Abdiel Capital and Tiger Global, low code application development platform OutSystems has raised $150 million in new capital. The funding gives the company a valuation of $9.5 billion, and will help fuel investment in its R&D and go-to-market strategies.

In a statement, OutSystems CEO and founder Paulo Rosado highlighted the challenges businesses face when it comes to keeping pace with innovation in an increasingly digital and software-run world. “Developers are a scarce resource in business today, and the complexities of traditional software development exacerbate the challenges most organizations face when tackling their digital transformation agenda,” Rosado said.

“By fundamentally changing the way software is built, OutSystems makes it possible for every organization to compete, innovate and grow with the developers they already have,” Rosado explained. “We’re focused on helping customers succeed with their most challenging digital transformation initiatives, and today’s announcement is an acknowledgment of our progress on that journey.”

OutSystems gives businesses the ability to deploy and manage critical applications at speed – from enhancing the customer experience to streamlining and automating processes to modernizing legacy systems. OutSystems leverages a visually-based, model-driven development approach to enable institutions to build differentiation into their solution, maximize the development talent on hand, and accelerate the process of concept iteration to uncover new viable ideas.

“OutSystems matched our vision for reusable architecture, robust application lifecycle management, and a visual approach that would allow developers to focus more on delivering business value instead of coding,” Shepherd and Wedderburn Head of Technology Steve Dalgleish said. “It has given us the speed and agility to deliver effective process and technology solutions – both internally and for our clients – including complex, large scale, high-profile projects.”

An alum of our developers conference, OutSystems presented “Low-Code: The Next Evolution in App Dev Platforms (Oh, and 5xFaster)” at FinDEVrNewYork in 2017. In their presentation, the company showed how it helped take a European retail bank, BPI, through a major digital transformation including solutions for mobile banking, internet banking, branch, and contact center.

With headquarters in Boston, Massachusetts and Lisbon, Portugal, OutSystems has customers in 87 countries around the world and partnerships with 350 corporations including AWS, Deloitte, and fellow Finovate alum Infosys.

Have you fallen into debt and can’t get up? Fortunately, there’s a new fintech on the scene that has dedicated itself to helping Americans build credit and savings – and get out of debt.

SeedFi, launched in private beta in 2019, announced today that it has raised $15 million in new equity – along with $50 million in debt financing. The Series A round was led by Andreessen Horowitz. Flourish, Core Innovation Capital, and Quiet Capital also participated.

“Our goal is to address the root cause of the problem and leave our customers better off than we found them,” SeedFi CEO and co-founder Jim McGinley explained, “so we’ve structured all of our products to generate savings and build credit.”

SeedFi COO and co-founder Eric Burton explained the savings/debt dilemma for many Americans in a conversation with Crunchbase News. He noted that the lack of savings in the event of an emergency is often the pre-existing condition that can lead to serious debt problems, which in turn, make it more difficult to save. “The insight we’ve learned is to combine savings with credit to address the immediate need for credit in a way that will leave them better off and down the path to a better financial future,” Burton said.

The San Francisco, California-based company plans to put the new capital to use growing its customer base and – with its bank partners – bringing products to market across the country. SeedFi also plans to add to its product offerings, which currently include two solutions: Credit Builder and Borrow and Grow.

“SeedFi is creating a suite of plans to address borrowers at various financial points in their lives,” Andreessen Horowitz General Partner Angela Strange wrote on the company’s blog earlier today. “Customers can start by saving as little as $10 a paycheck through SeedFi’s Credit Builder Plan, which enables them to build credit while they save. For those in need of money, SeedFi’s Borrow and Grow Plan gives customers the cash they need now and sets them up to save for the future.”

Many financial commentators are boasting about the high savings rates many Americans are achieving due to limited spending opportunities during the COVID crisis. Our “K-shaped” economic recovery means that many people are surviving – or even thriving – financially during the pandemic. But there are a significant number of Americans for whom COVID-19 has meant major financial hardship – including loss of income and an increase in consumer debt. For those Americans, fintechs like SeedFi are increasingly part of the solution.

Opera, one of the top internet browsers, announced a suite of in-browser cashback and payment tools for ecommerce. The release of the tools coincides with the launch of Dify, Opera’s new digital wallet.

Dify is a standalone mobile app that will enable users to open a Dify checking account and make purchases using a free, virtual Mastercard debit card. The account also features a special shopping mode, which protects users’ data while they shop by disabling third party extensions.

“Every day millions of people shop online and make their payments using Opera browsers,” said Opera EVP Browsers & EEA Fintech Krystian Kolondra. “Opera has a track record of growing audiences and then improving their experiences to make them more engaging. We think this is one of the highest-potential areas: With Dify, we are making the browser and a superior wallet work better, together, to improve users’ shopping experience and also make it financially rewarding.”

At launch, the main incentive to opening a Dify account is the cashback feature. Shoppers will receive cash back for purchases made on Opera’s partner websites accessed through its browser and will receive additional cashback on purchases made using their virtual Dify Mastercard.

Opera has a larger vision for Dify’s future, however. The company plans to enable more wallet services like savings management, credit products, investment opportunities, and instant cashback.

Dify is currently available to users in Spain in beta. Opera says it plans to expand to more European markets in the future.

Today’s launch follows a recent expansion of online shopping. According to research from J.P. Morgan, last year ecommerce activity reached $863 billion (€717 billion). The bank’s reports indicate that many countries in Europe will continue to have double-digit growth this year.

Australia-based financial comparison website Mozo has agreed to be acquired by British Media company Future PLC.

Future anticipates the purchase will fuel its global growth by creating a new revenue stream, adding a new financial services content arm in Australia, and growing Mozo’s market share.

Founded in 2008, Mozo is a B2C site that helps consumers compare offers on home loans, credit cards, and personal loans, as well as compare banking and insurance products. In total, the company compares more than 1,800 products from over 200 banking, insurance, and energy providers.

Monzo is also known for its personal finance resources. The company offers financial calculators and creates content to help guide readers through financial decisions and build their awareness of the finance world.

“We’re delighted to be adding Mozo to the Future family,” said Future CEO Zillah Byng-Thorne. “We are seeing the increasing convergence of content and price comparison and this acquisition supports our global growth ambition in this area.”

Mozo has raised $1.4 million (£1 million) via one round of funding. The company’s team of 45 employees works out of Sydney, Australia.

Cryptocurrencies have dominated the fintech headlines this week- from Mastercardagreeing to allow merchants to accept payments in cryptocurrencies to BNY Mellon’s announcement that it will begin custody of cryptocurrencies.

Today, after bitcoin reached an all-time high of over $48,000, marketing services company Kasasaunveiled plans to help its bank and credit union clients provide bitcoin wallets to their consumers.

The new capabilities will be powered by a partnership with New York Digital Investment Group (NYDIG), a technology and financial services firm dedicated to Bitcoin. The collaboration will help Kasasa’s bank clients stay ahead of the rapidly growing bitcoin adoption.

“Clearly, Bitcoin is here to stay, and consumers are demanding that Bitcoin offerings be made through their trusted financial institutions,” said Kasasa CIO John Waupsh. “With this new partnership, we’re looking across the product and services that Kasasa currently offers, as well as future product and service ideas. With NYDIG we can evaluate new offerings such as a buy-sell-hold wallet while also incorporating Bitcoin into our core rewards business.”

This partnership will be a major selling point for Kasasa, especially as consumer interest in cryptocurrencies rise. According to NYDIG, more than 22% of U.S. adults over the age of 18 own Bitcoin today.

This interest, combined with the creation of formal regulation like the OCC’s recent ruling that banks may use stablecoins for payment facilitation, is bringing cyrptocurrencies into the forefront of banks’ agendas. With today’s partnership, Kasasa is better positioned to help small financial institutions compete with larger players when it comes to cryptocurrencies.

An integration between two of Intuit’s top acquisitions, consumer financial technology platform Credit Karma and TurboTax tax management software, will help put the former’s new U.S. checking account – Credit Karma Money Spend – in the hands of more consumers.

The integration will provide a seamless process for getting refunds to eligible taxpayers when they file their taxes with TurboTax – and then turn those taxpayers into Credit Karma checking accountholders. Filers on TurboTax will have the ability to open a Credit Karma Money Spend account and have their refund sent directly to that new checking account. Users then can access the full Credit Karma Money experience – for example, setting up direct deposit and adding debit cards to their digital wallets – from within TurboTax. The checking account’s Instant Karma feature also encourages users to make payments with their Credit Karma Money Spend accounts by offering monetary rewards for actions like on-time credit card bill payments and automating direct deposits.

“We believe consumers should have a checking account that helps them make financial progress, which is why we created Credit Karma Money Spend,” Credit Karma founder and CEO Kenneth Lin explained. “We’re starting 2021 off by leveraging our relationship with Intuit to bring Credit Karma Money to millions of tax filers this tax season.” Lin referred to tax refunds as “the biggest paychecks” many Americans receive, and added that getting taxpayers the refunds they are owed and helping them put that money to work “(maximizing) their day-to-day spending and billpay” is a critical role the new integration will play.

Acquired by Intuit in a deal just completed in December, Credit Karma is among Finovate’s earliest alums, demonstrating its consumer credit score monitoring platform back in 2008. Now with more than 110 million members in the United States, Canada, and the U.K., Credit Karma offers a wide range of financial wellness solutions for individuals including identity monitoring, credit cards and loan shopping, insurance, high-yield savings accounts and, most recently, its new checking accounts backed by bank partner MVB Bank.

The integration news comes in the wake of a flurry of recent criticism that Credit Karma’s credit scores varied from what users were expecting when engaging with credit card companies or prospective lenders. The differences have since been explained – Credit Karma uses a credit score model, VantageScore 3.0, that not only examines factors other than those traditionally considered for FICO scores, but also can weigh like factors differently. But the issue may reflect a growing trend of popular annoyance with some of the ways fintechs are able to provide the services they do. This “Robinhood Syndrome” is a challenge that is only likely to grow as more customers – with varied expectations and financial sophistication – continue to migrate to fintech platforms.

Data analytics firm Moody’s announced plans to acquire data insights company Cortera this week. Terms of the deal, which is expected to close in the first quarter of this year, are undisclosed.

Moody’s anticipates the purchase will enhance its risk assessment capabilities. The move will also significantly extend Moody’s coverage in the SME market– the segment that serves as Cortera’s focus.

“Cortera plays an important role in helping businesses understand each other,” said President of Moody’s Analytics Stephen Tulenko. “Our customers will be able to leverage Cortera’s extensive information on small businesses with Moody’s proprietary analytic tools to make better decisions.”

Cortera was founded in 1993 and provides credit data and workflow solutions on North America-based public and private organizations. The Florida-based company maintains a database of credit information on more than 36 million businesses across the continent.

Cortera sources this data from thousands of resources and scrubs it using AI. As a result, the company is able to provide analytics, reports, and monitoring services to help inform businesses’ decisions.

Specifically, the acquisition will augment Moody’s Orbis database of private company information and enhance its KYC, commercial lending, and supply chain solutions.

Moody’s was founded in 1900 and provides data, analytical solutions, and insights to help businesses identify opportunities and manage risk. The company employs more than 11,000 people across 40+ countries. Headquartered in New York City, Moody’s is publicly traded on the NYSE under the ticker MCO. The company has a market capitalization of $52 billion.

Klarna is taking its Buy Now, Pay Later (BNPL) platform to a logical next step. The Sweden-based company announced today it will launch a bank account offering in Germany.

This move makes Klarna the first BNPL firm to make such a move. The company will now compete with the growing roster of digital banks in Germany, including N26 and Tomorrow.

Users will receive a Visa debit card, which is available in two colors, and will have tools on the app to track, manage, budget, and analyze their spending habits. Klarna will also reimburse users for two global ATM transactions per month.

“Our focus is to provide a superior shopping experience to our consumers at the intersection of retail and banking,” said Klarna CEO Sebastian Siemiatkowski. “And we know that there’s still massive room for improvement to the way many people bank and save their money today. Users are demanding more seamless, intuitive and transparent services to meet their daily needs, but many banks still do not cater for this.”

As Siemiatkowski points out, Klarna banking will be useful for “bundling shopping and banking in one app.” However, it is difficult to see the extra value a Klarna bank account will bring to users who aren’t big on shopping. N26 touts an integration with Transferwise for easy and inexpensive foreign money transfers and Tomorrow differentiates itself with a positive approach to sustainability and social causes. Klarna, in contrast, makes shopping a more embedded experience. This isn’t necessarily a positive attribute for one’s finances.

To counteract this “spend, spend, spend” mentality, Klarna said it has plans to add savings goals to the banking app, a feature that is already available in Sweden.

A pilot of Klarna’s bank account will initially be available to the company’s “most loyal” users and will roll out to all Germany-based users “in the coming months.”