This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

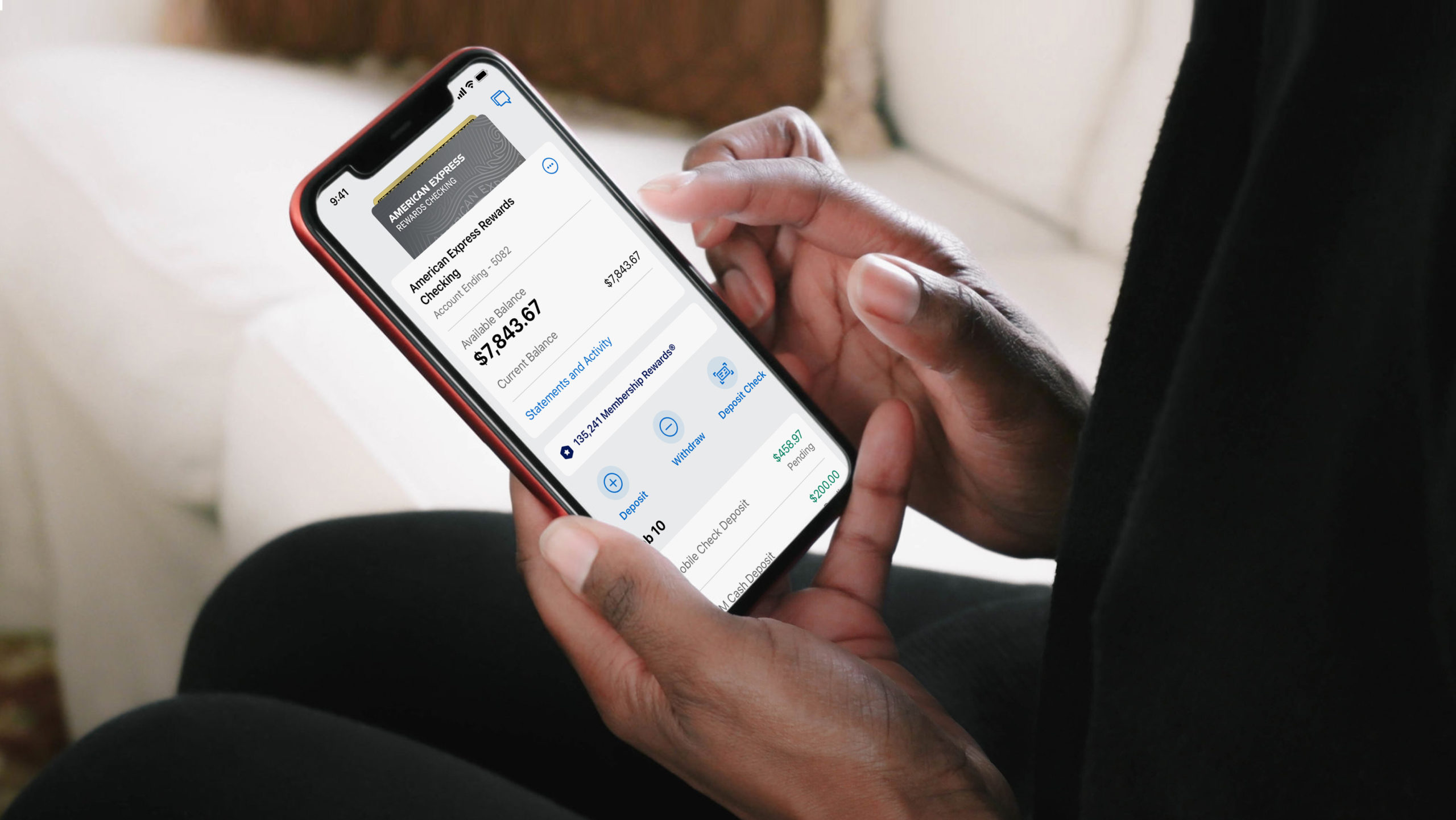

American Express is launching a new, digital checking account called Amex Rewards Checking

The Amex Rewards Checking account will offer a 0.50% high-yield APY on account balances, along with other membership rewards

The new checking account is only open to primary American Express credit cardholders and is limited to individual users.

Financial services giant American Express is expanding its horizons into the crowded world of digital checking. The company is launchingAmex Rewards Checking, an all-digital consumer checking account, for eligible U.S. card members.

As an incumbent player, American Express has multiple advantages over the many smaller digital challenger upstarts that have launched in the past two years. That’s because not only does the New York-based firm have credibility and a pre-existing large customer base, it also comes with a reputation for its rewards and perks.

“Our Members want more banking products and services from us,” said American Express Executive Vice President and General Manager of Consumer Banking Eva Reda. “And they want more from their checking account, without giving up the benefits that are important to them. That’s why we built Amex Rewards Checking to deliver more value for Members with the powerful and trusted backing of American Express. It’s digital checking without compromises.”

The checking account product will be a draw to Millennial and Gen Z users, who look for banking products with incentives and rewards. In fact, according to a study from Amex, 35% of consumers rank rewards and offers at the top when considering opening a new account. Given this, Amex packed competitive features into its new checking account. Accountholders can:

Earn 0.50% high-yield APY on their account balance, which is 10x higher than the national rate

Gain one Membership Rewards point for every $2 spent on eligible debit card purchases. Users can redeem these points for deposits into their Amex checking account

Pay no monthly maintenance fees or minimum balance fees

Receive purchase protection for accidental damage or theft on eligible purchases

Access Amex’s customer care providers 24/7 via phone or chat

Receive fraud protection and monitoring

Make fee-free ATM withdrawals at 37,000 MoneyPass ATM locations

The new Rewards Checking account is only open to primary American Express credit cardholders who have had their account for more than three months. Currently, the new checking account is limited to individuals and cannot accommodate joint accounts.

The new Amex Rewards Checking is American Express’ first checking account for retail customers. The financial services giant has offered small business checking for a little over a year now. The company acquiredKabbage in 2020 for $850 million and leveraged the purchase to launch a small business checking offering in 2021. That said, it’s worth noting that Amex’s new debit card is not available to its small business checking customers.

American Express, which presented at our developers conference in 2015, is listed on the New York Stock Exchange under the ticker AXP. The company saw $36 billion in revenue in 2020 and has a market capitalization of $149 billion. Stephen Squeri is CEO.

Canadian fintech TickSmith is ringing in the new year with $20 million in Series A funding. The company will use the additional capital to support marketing of its Data Web Store, a B2B SaaS platform that enables organizations and institutions to generate new revenue streams based on their data.

“Data monetization is no longer limited to large enterprises,” TickSmith CEO Francis Wenzel said. “Selling data should be as simple as selling products in an e-commerce store, and data sellers of all sizes can now benefit from the same tools that power the largest, most robust data marketplaces in the world.”

The Series A was led by Investissement Québec, and featured participation from Fonds de solidarité FTQ, CME Ventures, Databricks Ventures, Anges Québec, Anges Québec Capital, and Illuminate Financial Management. The investment gives the company a total capital of $26.8 million, according to Crunchbase.

Founded in 2012, headquartered in Montreal, Québec, and making its Finovate debut two years later at FinovateFall 2014, TickSmith offers a platform that gives firms the technology they need to prepare, manage, package, and monetize data via private marketplaces. With customers in industries ranging from financial institutions and data providers to exchanges and brokerages, TickSmith helps organizations take advantage of a new world of data types – including alternative data and unstructured data.

The company’s technology also empowers them to enhance and refine existing data, enabling them to offer granular, micro-data services. This, as TickSmith Head of Product Nicolas Doyen, explained in a recent blog post, is allowing data providers to “(offer) more control to the ultimate consumers of their information services.” He added that this “modern approach to the data buying process” not only gives more control to the end-user, but also can help reduce the costs of data by “circumventing the data packaging approach used by traditional data suppliers.”

TickSmith ended 2021 with a collaboration with international cryptocurrency and digital asset technology company BlockFills. Earlier this month, TickSmith announced that IPOhub will use TickSmith’s Data Web Store platform to distribute and securely commercialize SME data from more than 3,000 companies and more than 100 different sources. A pan European investment information platform headquartered in Estonia and founded in 2017, IPOhub is also collaborating with TickSmith and market data specialist EOSE to help take IPOhub data on growth company IPOs to market.

“TickSmith’s technology is making it easy for us to offer our customers a personalized e-commerce data shopping experience with our very own data web store that showcases IPO and European SME data,” IPOhub CEO Silver Laus explained. “Their platform provides an end-to-end data monetization experience and helps us open up an entirely new channel to deliver data to our customers in just a few clicks.”

FinovateFall Best of Show winner SpyCloud has launched its latest solution to combat online fraud. The SpyCloud Identity Risk Engine, unveiled this week, analyzes billions of data recaptured from the dark web to help businesses and financial institutions make faster, more accurate, real-time fraud mitigation decisions.

What’s unique about SpyCloud’s approach to fighting fraud is the company’s focus on identifying credentials that have been exposed during data breaches and are actively being traded in the criminal underground. These exposed credentials are sold to fraudsters on the black market or used by the hackers themselves to steal confidential information, access secure systems, or commit fraud. Because many of these sources of stolen credentials cannot be readily accessed by automated software tools or web crawlers, SpyCloud uses a combination of technical innovation and human intelligence to find and recapture data from online criminal communities. The company also gives businesses and financial institutions access to the kind of authentication systems that will help defend them against cyberattacks that leverage stolen credentials such as account takeover (ATO), identity fraud, and new account fraud.

With the release of its SpyCloud Identity Risk Engine, SpyCloud gives businesses in financial and ecommerce services actionable, predictive fraud risk assessments based on breach data and stolen credentials that have been recaptured from the dark web. The technology combats difficult-to-detect challenges including data harvested by malware and the use of synthetic identities. SpyCloud Identity Risk Engine also gives businesses insight into which customers have the highest risk of account takeover due to risk factors such as exposed credentials or weak password protocols.

Businesses place the Identity Risk Engine at their most critical points of potential fraud (i.e., at account opening, login, transactions, etc.). From there, all that is required is an API query using an email address or phone number. SpyCloud then scans billions of recaptured data points to deliver a risk score that enables businesses to make more accurate fraud decisions. SpyCloud has recaptured more than 145 billion breached assets, more than 30 billion email addresses, and more than 25 billion total passwords. The company’s technology collects 50+ breach sources every week.

Winner of Built In Austin’s Best Places to Work for a second year in a row, SpyCloud was founded in 2016 and made its Finovate debut one year later. The company was featured in Fast Company’s inaugural Next Big Things in Tech roster last fall and, in October, SpyCloud announced a partnership with Houston, Texas-based identity and access management solution provider Identity Automation to help schools fight ransomware threats.

“Preventing ransomware is possible by negating the top attack vector: credentials that have been exposed in data breaches,” SpyCloud SVP of Business Development Cassio Mello explained. “This service gives schools early identification of compromised accounts, enabling them to take action quickly and prevent cyber attacks that leverage recently-breached identity data.”

SpyCloud has raised $58.5 million in funding from investors including Centana Growth Partners, Microsoft’s Venture Fund M12, March Capital, and Silverton Partners. Ted Ross is co-founder and CEO.

With its acquisition of financial analysis as a service company FlashSpread, digital mortgage platform BeSmartee’s ability to deliver a complete, digital lending experience just got that much more complete.

“We are excited to welcome FlashSpread and Ariel Trybuch to the BeSmartee family,” CEO and co-founder of BeSmartee Tim Nguyen said in a statement. “This is an acquisition that not only brings new clients, technologies, and talents to BeSmartee, but one that also sparks further innovation into all lending verticals, including mortgages, consumer, and commercial.”

Founded in 2017 and headquartered in Glendale, California, FlashSpread specializes in instant tax spreading for commercial lenders and fintechs. The company’s proprietary algorithms enable lenders to convert scanned tax returns into customized and comprehensive financial reports with the click of a button. The technology brings significant efficiencies to the commercial loan process – from origination to servicing – and empowers lenders to make accurate, data-driven credit decisions quickly.

Via its acquisition of FlashSpread, BeSmartee will be able to accelerate its growth strategy, prioritizing increased automation as it expands into the commercial lending space. FlashSpread is integrated with some of the largest loan origination systems in the commercial lending industry, with more than 100 financial institutions relying on its technology to automate manual processes. Post-acquisition, FlashSpread will continue independently to serve customers as a “BeSmartee Company” with FlashSpread founder and CEO Ariel Trybuch taking on the role of General Manager.

“This partnership will provide the resources necessary to support the hyper-growth FlashSpread is currently experiencing, as well as allow us to provide our customers with an even higher level of customer support, rapidly introduce new features and functionality, and expand our ever-growing library of supported document types,” Trybuch said. The company will continue growing its document library to support a broader range of financial statements, as well as launch a no-code reporting module to offer instant custom reports, and unveil an ongoing credit monitoring tool.

BeSmartee’s acquisition announcement comes just days after the company reported a partnership with Freddie Mac. The Huntington Beach-based fintech will integrate Freddie Mac’s automated underwriting system, Loan Product Advisor, improving workflows for lenders by automating risk assessment, and both asset and income data review. The integration will also improve lenders’ ability to make smart business decisions, leveraging actionable insights from Loan Product Advisor’s rich data visualization features.

Visa-owned open banking platform Tink has finalized its purchase of FinTecSystems. The acquisition, which was initiated prior to Visa purchasing Tink, was first announced in May of last year. The integration of the two companies combines Tink’s open banking platform and FinTecSystems’ product suite to offer a more complete solution when partnering for open banking technology.

Additionally, FinTecSystems brings Tink new customers including N26, DKB, Santander, Solarisbank, and Check24. The Germany-based open banking firm will help Sweden-based Tink build on its growth strategy and expand into the DACH region, where FinTecSystems is currently powering over 150 banks and fintechs.

“Germany is a key market for Tink, and we are excited to have acquired an innovative leader with a strong reputation for the quality of its bank connectivity and payments services,” said Tink Co-founder and CEO Daniel Kjellén. “We have followed FinTecSystems for many years and are impressed by what they have achieved. Through this acquisition, we are taking a big step into the DACH region, and we look forward to supporting the FinTecSystems’ team to further accelerate their growth.”

FinTecSystems was founded in 2014 and facilitates data analytics, digital account checks, account aggregation, and open banking payments. The company connects to more than 99% of the banks in the DACH region, and in Germany specifically, three in every four online credit decisions involve FinTecSystems’ technology.

FinTecSystems’ 78 employees have joined Tink’s team, which now sits at almost 600 employees. FinTecSystems will continue to function as an independent, regulated company in Germany.

Today’s deal comes two years after Tink landed $103 million (€85 million) in a funding round that boosted its total raised to $308 million. The acquisition also comes after Tink itself was bought out by Visa in June of 2021 for $2.1 billion (€1.8 billion).

Tink, whose open banking platform is used by more than 10,000 developers, was founded in 2012 and currently serves 18 markets from its 13 offices. The company is a two-time Finovate Best of Show Award winner, and most recently demoed at FinovateEurope 2019.

FinovateEurope 2022 is right around the corner. If you are an innovative fintech company with new technology to show, then there’s no better time than now and no better forum than FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22 to March 23, visit our FinovateEurope hub today!

One month after introducing its next generation development application platform, OutSystems has announced that it is entering a strategic partnership with fellow Finovate alum ieDigital. The alliance will enable ieDigital’s financial services company partners – ranging from bank to mortgage lenders – to access a suite of pre-built, low-code applications that support a variety of operations including originations, self-servicing, retention, and collections.

The goal of the new relationship is to give financial service providers new resources that will help accelerate growth, become more cost-efficient, and better manage risk. The partnership also allows for additional functionalities to be added as part of broader, future digital transformation efforts. One example of this would be enabling companies to analyze data collected during the completion of online applications for a new financial product or service.

“By pioneering the low-code market and having a vision to transform how enterprise software is delivered,” ieDigital Commercial Director Garry Larner said, “the OutSystems platform perfectly complements our existing product-offering. We look forward to working alongside them to continue delivering market-leading financial technology that makes a real impact to all that use it.”

ieDigital noted that the partnership will leverage and further build upon the Interact Application Suite, an approach ieDigital used in a previous collaboration with Cambridge & Counties Bank to help the firm combat financial crime. The result was a more streamlined customer onboarding process, enhanced automation for both middle and back office workers, and better capacity and knowledge to support the development of applications going forward – including an option for Cambridge & Counties Bank to build its own in-house development capability.

Founded in 1984 and headquartered in London, U.K., ieDigital demonstrated its Money Fitness solution at FinovateFall 2018. The technology helps credit unions effectively compete with the wave of competition from “digital-first” providers with a forward-looking personalized service that credit union members can use to better manage their day-to-day finances, make better financial decisions, and improve their overall financial health.

More recently, ieDigital launched its customer retention solution Interact Switch, which is designed to help mortgage lenders retain customers at product offer maturity. The technology enables mortgage lenders to function more efficiently by cutting down on paper-based, mortgage representative, and third-party costs. Also this fall, ieDigital announced a partnership with Darlington Building Society and a collaboration with DF Capital to help the savings and commercial lending bank to launch a new digital interactive channel for its savings customers.

An alum of our developers conference, FinDEVr NewYork 2017, Boston, Massachusetts OutSystems specializes in cloud-native, low-code app development. More than 14 million people currently use OutSystems’s platform to build solutions such as mobile apps and consumer websites, as well as extensions of core systems from Microsoft and Salesforce. The latest platform edition from the company, code named Project Neo, marries the productivity benefits of visual, model-based development with state-of-the-art container- and Kubernetes-based cloud architecture. The technology is hosted on Amazon Web Services to make it easy for any company to build customized, cloud-based apps that scale globally and can be continuously updated.

“Developers should be the artisans of innovation in their organization, but they are mired in complexity that stifles their ability to innovative and differentiate,” OutSystems CEO Paulo Rosado said. “Instead of using their talents to fix, change, and maintain code and aging systems, you can give them industry-leading tools that unleash their creativity on your business, and achieve massive competitive advantage.”

Even though our annual European conference has moved from February to March, FinovateEurope will always be synonymous with wintertime for many of us. So with the coldest season swiftly approaching, now seems as good a time as any to check in on the latest from some of our most recent FinovateEurope alums.

Paris, France-based Thread recently earned recognition at Catapult: Kickstarter 2021 Fall Edition. As one of the event’s five winners, the company is now eligible for up to $56,360 in subsidies. Thread made its FinovateEurope debut earlier this year, demonstrating its technology that makes complex and critical investment workflows more efficient and collaborative. In doing so, Thread aims to help investors make better investment decisions and reap “consistently higher performance.”

“With the acceleration of digital transformation worldwide, many companies have struggled to personalize their customer journeys online,” Surfly CEO Nicholas Piel said in a statement. “Surfly’s Co-browsing has helped ensure that insurers globally do not lose their personal touch with customers.”

Earlier this month we shared news that Strands had teamed up with carbon tracking company Doconomy. The partnership will enable the Barcelona, Spain-based fintech to offer climate impact and insight-driven engagement tools to their customers. Last month, Strands announced that digital financial solution provider Comviva will use Strands’ smart PFM solution to help its bank and financial services clients offer their customers a better digital banking and payments experience.

FinovateEurope 2021 Best of Show winner Quantum Metric was one of our more recent guests as part of our Finovate Webinar series. In partnership with BMO, the company led a webinar on How BMO is reimagining the Commercial Banking digital client experience using real-time analytics. Available for free on-demand for a limited time, the webinar panelists discuss the importance of quantifying the long-term impact of negative user experiences and how to establish a customer-centric mindset via Continuous Product Design (CPD).

Picking up a variety of fintech awards this year, white-label digital banking solution provider Meniga is another company that is leading the way in helping its customers understand and manage their climate impact – as citizens, consumers, and investors. Meniga, which demonstrated its Carbon Insight solution at FinovateEurope this year, announced that its transaction-based carbon footprint calculator had earned independent assurance from global accounting and professional services company EY.

ITSCREDIT was one of five Portuguese fintechs chosen to participate in a program to help provide Portuguese technology companies with the tools they need in order to “gain a foothold in (their) respective U.S. tech ecosystems” and help drive expansion. The landing pad program, Portugal Tech NYC, is sponsored by AICEP Portugal Global and SOSA, and will also feature the participation of Finovate alums ebankIT and LOQR.

ITSCREDIT demonstrated its Genie Advisor at FinovateEurope this year. The technology predicts customers’ financial conditions and provides insights to banking and finance professionals on how to best support customers that may be facing financial challenges.

To start the week, multiple-time Finovate Best of Show winner iProov announced that its partnership with Eurostar, the high speed passenger rail service that links the U.K. with mainland Europe, was now live. Eurostar has launched a trial of a new contactless fast-track service, SmartCheck, at London Pancras International. The service lets passengers use their mobile devices to secure ticket verification and U.K. exit check before they travel. Ticket holders of Eurostar’s Business Premier and Carte Blanche programs will be able to use their iPhones to complete a biometric face scan, which uses iProov’s Geniune Presence Technology, for identity verification that is linked to the traveler’s e-ticket.

“The days of rooting around in your bag for your passport or hoping that your phone battery doesn’t run out before you show your e-ticket at the gate are over,” iProof founder and CEO Andrew Bud said, “(SmartCheck) is effortless and convenient while also delivering the reassurance and security that travelers expect.”

Speaking of companies that have won more than a few Finovate Best of Show trophies, Digital Customer Service innovator Glia has been on an epic partner-making pace since its FinovateEurope appearance earlier this year. Customer engagement solution provider Engageware, Connecticut-based Liberty Bank ($7 billion in assets), digital banking solution provider Apiture, and Conversational AI specialist Posh Technologies are just a few of the companies Glia has collaborated with this fall. In November, the company earned a top 250 spot in the Deloitte’s Technology Fast 500 for North America.

Stockholm, Sweden-based Dreams, which demoed the savings module of its financial wellbeing platform at FinovateEurope this year, earned recognition at the Banking Tech Awards hosted by Fintech Futures. The company was named “Best Digital Banking Solution Provider.” Learn more about the Best of Show-winning company in our interview with Dreams CCO Lucia Hegenbartova, who sat down with Finovate VP Greg Palmer for an episode of the Finovate podcast over the summer.

CoCoNet Group, a digital banking services provider based in Germany, recently. announced a successful collaboration with Raiffeisen Group. The Swiss banking group leveraged technology from CoCoNet to launch a multibanking solution with integrated cash management and a secure EBICS interface to streamline online banking for corporate customers. CoCoNet made its FinovateEurope debut this March, demonstrating its MULTIVERSA Corporate Customer Onboarding solution.

The company formerly known as Nordic API Gateway has enabled more than 40 financial institutions, and a number of businesses, to integrate financial data and offer A2A (account-to-account payments) via a simple API. Founded in 2017, the company had raised $15 million (€13.5 million) in funding to date.

“For the past decade, we have worked to build Aiia into a leading and quality-driven open banking platform, which has onboarded hundreds of banks and fintechs onto safe and secure open banking rails,” Aiia founder and CEO Rune Mai said. “We have worked closely alongside banks, customers, and local authorities to ensure that our APIs show the true effect of open banking. We’re excited to become a part of Mastercard and progress our journey of empowering people to bring their financial data and accounts into play – safely and transparently.”

FinovateEurope 2022 is right around the corner. If you are an innovative fintech company with new technology to show, then the time is now and the forum is FinovateEurope. To learn more about how to demo your latest innovation at FinovateEurope 2022 in London, March 22-23, visit our FinovateEurope hub today!

Cryptocurrency exchange platform Coinbaseacquired Israel-based security company Unbound Security today. Terms of the deal, which Coinbase calls the next phase of its security journey, were not disclosed. Coinbase expects the deal to close in the coming months.

Unbound specializes in cryptographic security technologies, including secure multi-party computation (MPC), an emerging subfield of cryptography that allows parties to jointly compute a function over their inputs while protecting their data. Essentially, MPC enables crypto assets to be stored, transferred, and deployed more securely, easily and flexibly.

Today’s deal will give Coinbase access to cryptographic security experts, including Unbound Co-founders Guy Peer and Yehuda Lindell, who is considered a world leader in MPC. Coinbase will also gain a presence in Israel and plans to establish a tech center in the country. The company states that this global reach will “add an additional powerful prong” to its global talent acquisition strategy.

“We’ve long recognized Israel as a hot bed of strong technology and cryptography talent, and are excited to continue to grow our team with some of the best and brightest minds in these fields,” the company said in its blog post announcement. “The Unbound Security team will form the nucleus of this new research facility, which we plan to grow over time.”

The purchase of Unbound marks Coinbase’s twentieth acquisition since the company was founded in 2012. Coinbase has acquired six companies this year alone, including financial software company BRD, voice AI startup Agra, crypto wallet API provider Zabo, financial infrastructure company Skew, and blockchain security firm Bison Trails.

Coinbase, which demoed at FinovateSpring 2014, went public earlier this year and now trades on the NASDAQ under the ticker COIN. The company has a current market capitalization of $67 billion. Earlier this fall the company announced plans to launch its own NFT marketplace, Coinbase NFT, to help users mint, purchase, showcase, and discover NFTs.

Analytics and decision management technology company FICOlaunched a loan origination tool called FICO Originations Solution that automates the entire customer journey leveraging the FICO platform.

The cloud-based tool leverages FICO’s enterprise intelligence network to streamline and personalize loan originations. The new tool helps financial services providers do two key things. First, it helps remove friction from the customer experience. Second, it empowers loan originators by helping them make more precise origination decisions and better manage risk, ultimately helping them grow more profitable portfolios.

This enhanced decision-making is thanks in part to FICO’s data library that offers lenders access to 130+ global data sources. The ever-increasing data source helps firms make faster and better customer decisions.

The FICO Originations Solution starts with a completely digital onboarding experience. The tool considers an organization’s goals, including the types of borrowers they want to attract, their ideal conversion rate, and profitability goals. FICO offers simulation capabilities to test the user experience to determine if decreased friction results in increased fraud or if changing an application question increases the conversion rate.

FICO Originations Solutions’ customers have access to FICO’s suite of tools that includes interactive messages, fraud prevention capabilities, and pricing optimization.

“Financial services providers today need data-hungry, analytics-ready, agile, extensible systems in order to compete in a digital-first economy,” said FICO VP and Head of Product Management Tim Van Tassel. “FICO Originations Solution, Powered by FICO Platform provides the digital and analytic sophistication that enables financial institutions to offer the safety, convenience, and personalization that customers look for during the account opening process through their chosen channel, while closely managing customer-level risk.”

FICO was founded in 1956 and is headquartered in California. The company is best known for the consumer FICO score that is calculated based on information in credit reports maintained by Experian, Equifax, and TransUnion. The company also offers fraud and compliance as well as debt collection and recovery solutions.

Sometimes at Finovate, the first time is the charm.

Detroit, Michigan-based fintech Autobooks, which helps small businesses send digital invoices and accept online payments via their financial institution partner, took home Best of Show honors in its Finovate debut in September. The company, co-founded by Steve Robert (CEO) and Aaron Schmid (CIO), impressed our audiences with its embedded solution that gives small businesses an e-commerce platform that is fully integrated into their current digital banking system.

Autobooks shared the stage with partner TD Bank, which offers Autobooks’ suite of tools as part of its TD Online Banking solution. TD Bank Head of Corporate Products and Services Jo Jagadish noted that the partnership has “increased relationship depth with our SMBs by 26%” and represented what Jagadish referred to as a complete reimagining of the bank’s small business checking experience.

“Small businesses are an enormous and diverse group with one thing in common,” Robert explained, “how they get paid is in a state of transition. Financial institutions must invest in digital-first experiences to meet SMBs where they, and their customers, are.” One advantage Autobooks provides is the fact that its technology is embedded into the customer’s existing banking channels, helping financial institutions build and fortify their relationships with their small and micro-business customers.

In the weeks since Autobooks’ Best of Show winning demo at FinovateFall, the company has announced a partnership with Central Trust Bank. Headquartered in Jefferson City, Missouri, the $20 billion state-chartered trust company will embed Autobooks’ technology into its digital banking platform. In addition to giving the bank’s business customers the ability to send digital invoices and accept online payments, the integration will also provide cash flow management, accounting, and financial reporting tools.

“We’re dedicated to providing innovative solutions to our customers, and the tools to make banking as easy as possible,” Central Trust Bank SVP of Commercial Banking Services Arlene Vogel said. “We believe partnering with Autobooks will allow for business customers to optimize payments for their business, ultimately helping their business succeed.”

Central Trust Bank has more than 250 locations in 78 communities in Missouri, Kansas, Illinois, Oklahoma, Tennessee, North Carolina, Colorado, and Iowa. The bank was founded in 1902.

Also last month, Autobooks announced that it had expanded its partnership with TD Bank to add invoicing to TD Bank’s TD Business Simple Checking offering. The bank’s business customers will now be able to accept credit card and electronic payments that settle directly into their TD account. This will enhance cash flow and liquidity, and will make it that much easier for small and micro-businesses to get paid faster. The collaboration marks TD Bank as one of the first major financial institutions to offer integrated invoicing as part of its digital banking solution.

“Probably the greatest pain point for small businesses is actually getting paid for the services they provide,” Jagadish said. “The new tool will make things easier, faster, and enable our small business customers to get paid, almost immediately in most instances, when the process previously could take up to a week or longer.”

Previous to co-founding Autobooks, both Robert and Schmid were executives with another Finovate alum, Billhighway. Robert served as Chief Information Officer, while Schmid was Chief Product Officer. The company was acquired by BluePay in 2016.

From a collaboration with Visa to a partnership with Q2, new Finovate alum Veem, which made its Finovate debut last September at FinovateFall, continues to offer the kind of solutions to help make business payments easy, efficient, and affordable.

In fact, within one month of the company’s first-ever demo on the Finovate stage – a presentation of Veem’s Partner Connect product – the San Francisco, California-based company inked two major deals with some of the most innovative companies in financial services and digital banking.

Veem’s partnership with Visa, announced in the first half of October, will give the company’s 400,000+ customers access to a new SMB Visa card program, as well as digital money movement capabilities courtesy of Visa’s real-time push payments platform, Visa Direct. The agreement will enable Veem customers to generate and issue virtual Visa payment cards that can be used to cover business costs ranging from payments to suppliers to more general business expenses. The virtual card program, along with Veem’s spend management tools, also provides reconciliation and other financial benefits to help customers further digitize and streamline their operations. Access to Visa Direct will give Veem’s U.S. clients the ability to send money directly to both bank accounts and eligible Visa cards in more than 160 currencies.

“Visa is renowned for having broad network acceptance both domestically and internationally,” Veem CEO Marwan Forzley said. “Our collaboration helps Veem expand digital payment options for our customers, as we continue to build the next generation global solution for businesses.”

Veem also last month announced that it was teaming up with digital banking innovator Q2. The partnership is geared toward taking the friction out of the accounts payable/accounts receivable process for SMEs by making Veem’s AP/AR automation platform available to the 450+ financial institutions and 1.5 million businesses on Q2’s digital banking platform.

“This partnership with Veem gives our Financial institutions the ability to deliver Veem’s modern payment services to SMB customers with agility and reliability,” Q2 Innovation Studio Managing Director Johnny Ola said. “Businesses are looking for embedded solutions that act as a one-stop-shop to conduct all their day-to-day transactions. With our integration with Veem, we are excited to give our financial institution customers the option to offer small businesses innovative technology solutions.”

The two collaborations were only part of a very busy autumn for Veem, which was founded n 2014. Also last month, the company appointed Jeff Revoy as Chief Growth Officer and Travis Green as Vice President of Product Management. Revoy brings 20 years of CEO, President, and C-level experience at a number of public and VC-backed firms. Previous to his joining Veem, Revoy was Chief Operating Officer for SpaceIQ, a real estate workplace management software company he founded in 2016 that was acquired by WeWork in the summer of 2019.

In September, Veem secured $31 million in strategic funding in a round led by Truist Ventures. The company said in a statement that the capital will help it develop a robust channel partner program to broaden the company’s geographic footprint. The investment takes the company’s total equity funding to just over $100 million.

“This funding round marks an important milestone for the company, putting us in an ideal position to build out our channel partner program and prepare for Veem’s next stage of global growth,” Forzley said when the investment was announced. “Our channel partner network serves as our vehicle to better commercialize our product offering and further expand upon our market development efforts.”

As Veem’s FinovateFall debut showed, the development of its channel partner program has already borne fruit. At the conference, Veem’s Revoy and Connor Grilo demonstrated a new minimal code integration – Partner Connect – that enables banks to offer their clients an all-in-one, global payments platform designed for small and mid-sized businesses that keeps the bank’s branding at the forefront. The solution is integrated with the major accounting platforms so that, with a couple of clicks, users can reconcile what they are sending out from or receiving in Veem with their accounting software.

“There’s no back and forth, there’s no trying to keep two separate systems,” Revoy said from the Finovate stage. “All of this is automated and designed in a way so that, as a business owner, it can be fast, it can save you time, hopefully it will save you money, and will save you a lot of headaches, because everything is tied together.”

Peer-to-peer lending platform and digital bank Zopalanded $304 million (£220 million) this week. The investment marks Zopa’s largest round to-date, and brings the U.K.-based company’s total funding to $792 million.

According to TechCrunch, today’s funding, which follows a $28 million investment received earlier this year, gives Zopa a post-money valuation of $1 billion (£750 million).

Softbank Vision Fund 2 led the round, which saw contributions from existing investors including Silverstripe, Northzone and Augmentum. Zopa anticipates the cash will help bring its banking tools to more U.K. consumers.

Zopa is on track to hit profitability by early next year. If it does, it will be one of the fastest digital banks in the U.K. to do so. Additionally, if Zopa continues on this path of success, the company is likely to IPO at the end of next year.

Founded in 2004, Zopa debuted its peer-to-peer lending platform at FinovateSpring 2008. The company has since evolved as a player in the challenger banking space. Zopa’s differentiator from competitors, however, is that it is not a fully-fleged bank. The company does not offer a checking account or payment card. Instead, it focuses on savings, loans, and credit-building tools.

Zopa received its banking license in June of 2020. Since transitioning from its flagship peer-to-peer lending model, Zopa has reached $931 million (£675 million) in customer deposits for its savings accounts, has issued 150,000 credit cards, and is now a top 10 credit card issuer in the U.K. based on new customers.

The company’s lending products have also seen success. So far this year, Zopa has disbursed over $8.3 billion (£6 billion) in loans. The company lends over $138 million (£100 million) each year in car loans.

Zopa has formed two recent partnerships that centralize on helping users build and access credit. Its partnership with ClearScore helps provide a pre-approved credit card to Zopa customers who have been declined credit, and its integration with CreditLadder enables renters to build credit by reporting their rental payments.

As for what’s next, Zopa says it is “focused on building a sustainable, profitable business model” that benefits both customers and shareholders.