This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

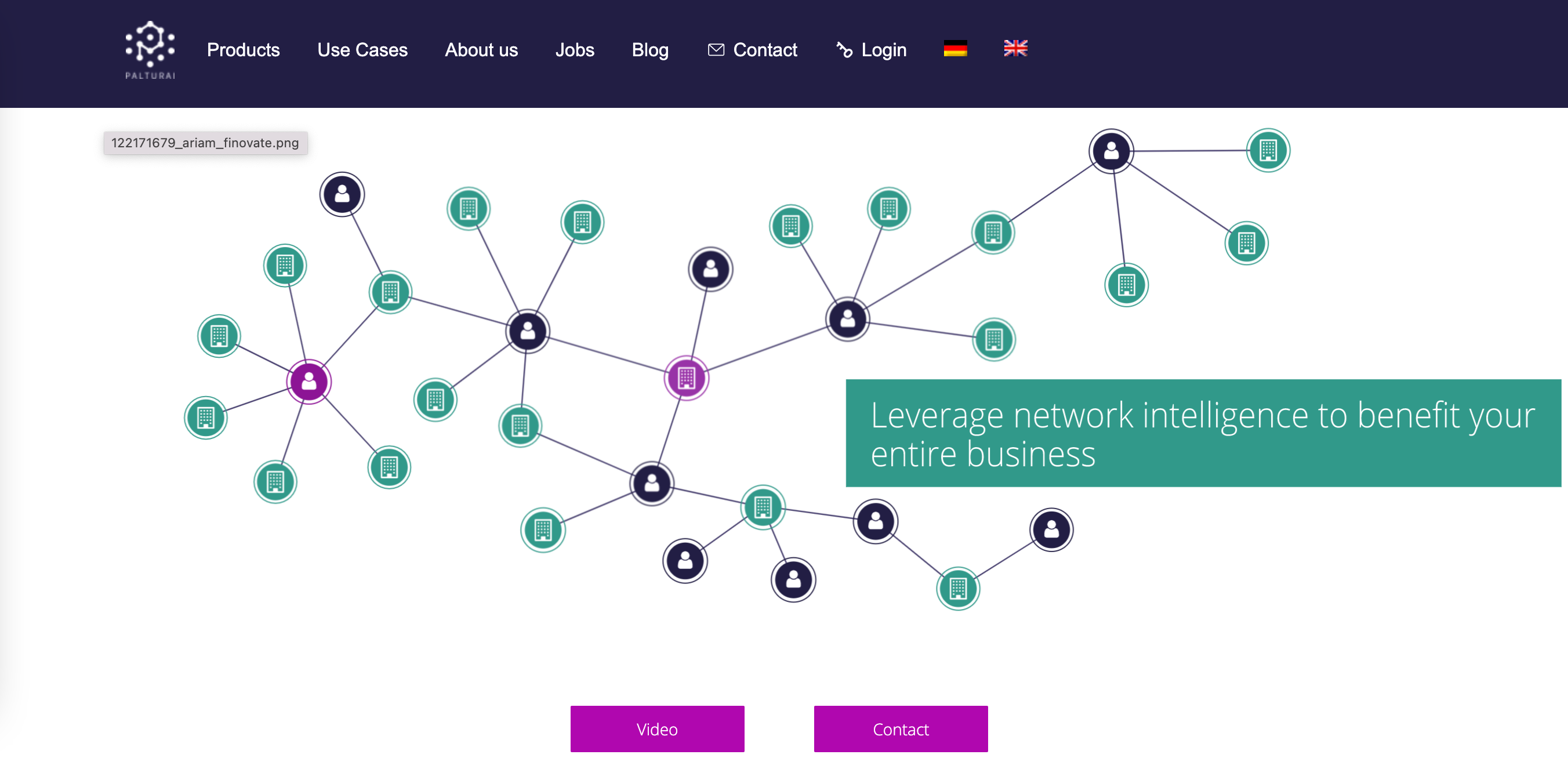

PalturaiBusinessGraph is a leading Knowledge Graph Platform, adding a new dimension of network analytics to businesses. Make more informed decisions and identify hidden opportunities and risks.

Features

Sales & Marketing – discover new leads in business networks

Risk, Fraud & Compliance – identify trouble spots in business ecosystems

Palturai BusinessGraph is pre-loaded with 66M+ companies, 60M+ people and 211M+ relationships. The solution is actively deployed at Tier-1 financial services and public sector institutions.

Presenters

Bernhard Ritz, Regional President, North America Ritz is the Regional President for Palturai in North America. He spent two decades at SAP and held various management roles in Corporate Strategy and Strategic Business Development. LinkedIn

Noel Billingsley, Head of Business Operations, North America Billingsley leads operations for Palturai in North America. A former career banker and serial entrepreneur, he brings unique experience in guiding the introduction of Palturai to the NA market. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

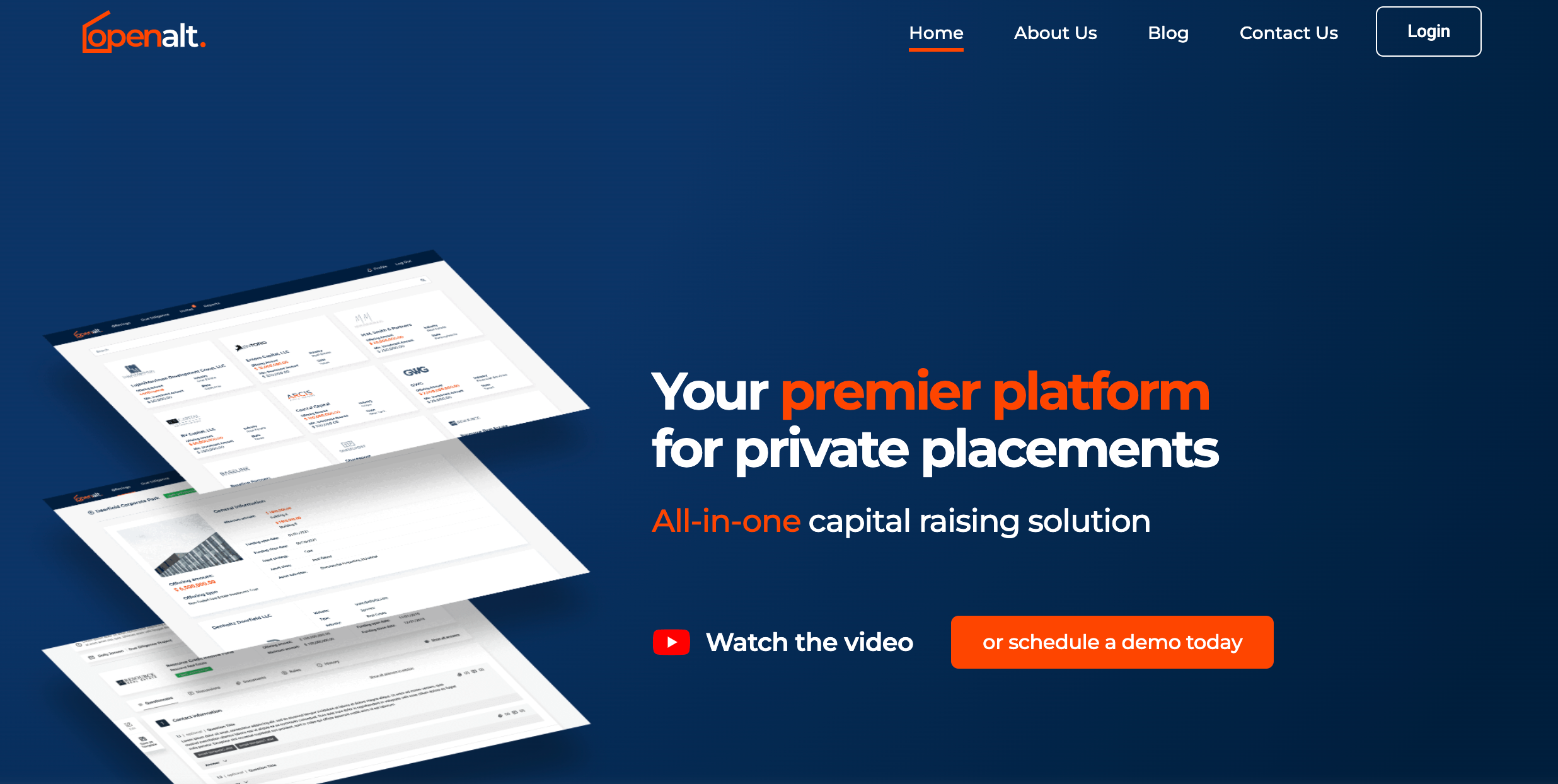

OpenAltoffers a capital raising and custodial platform for private businesses and their investors, including private offerings marketplace, due diligence, transaction processing, and data reconciliation solutions.

Features

Private market investment research and due diligence

Transactional automation

Seamless custodial integration and reporting

Why it’s great

OpenAlt bridges the gap between financial advisors and investable private businesses to allow for better diversification of the investment and retirement portfolios.

Presenters

Nikita Brodskiy, Co-Founder Brodskiy has more than 15 years of experience in the IT industry and FinTech. He holds an M.S. in Management from Stanford Graduate School of Business. LinkedIn

Anton Charnotski, Co-Founder Charnotski is a seasoned software architect, platform builder, and engineering leader. He has extensive experience in the custodial space and holds an IRA Services Professional certification (CISP).

Quarterly funding for Finovate alums topped $365 million in the first three months of 2022. The amount is lower than last year’s Q1 tally, and is more reminiscent of the sums raised by Finovate alums in the first quarters of 2019, 2017, and 2016. The number of alums receiving funding in Q1 of 2022 was also lower than in recent years.

That said, overall fintech investment is as strong as ever. According to research from CB Insights, while overall fintech investment in Q1 of 2022 was lower than in three out of four quarters in 2021, the sum – more than $28 billion – tops Q1 2021 and stands as the largest first quarter for fintech investment on record.

The biggest fundraising of the quarter was the $85 million secured by Personetics in January. Close behind was the $70 million that iProov raised – also in the first month of the year. Given that there were only 11 alums reporting funding in Q1 of 2022, it is understandable that the top ten equity investments for the quarter represent virtually all of the known funds raised by Finovate alums in the first three months of the year.

Here is our detailed alum funding report for Q1 2022.

If you are a Finovate alum that raised money in the first quarter of 2022 and do not see your company listed, please drop us a note at [email protected]. We would love to share the good news! Funding received prior to becoming an alum not included.

Finovate alums Boss Insights and MX are partnering to give SMEs access to real-time financial business data.

The partnership will support faster, more accurate lending and funding for SMEs, as well as enhancing payment services.

A multiple-time Finovate Best of Show winner, MX is headquartered in Lehi, Utah. Boss Insights is based in Toronto, Ontario, Canada.

A partnership between open finance company MX and business data aggregation innovator Boss Insights will make it easier for small and medium-sized businesses to access real-time financial business data. Announced late last week, the collaboration will help banks and other financial institutions better serve their SME customers.

Courtesy of the new partnership, firms will have a 360-degree view of their business customers’ financial health via a single API. The API offers real-time access and integration with accounting, banking, and commerce data from more than 1,000 sources including QuickBooks, Xero, Shopify, Stripe, and Amazon.

“Boss Insights shares MX’s view that finances should be simple, useful, and intuitive,” Boss Insights CEO Keren Moynihan said. “Together, MX and Boss will empower fintechs, private lenders, and financial institutions with a platform to originate, decide, and monitor the business requests of their SMB and commercial business customers. This will help them make faster, more accurate lending, funding, and payment decisions.”

Among Finovate’s newer alums, making its Finovate debut in 2019, Boss Insights leverages big data and AI to accelerate the lending process for SMEs. The company’s Smart Capital product suite offers automated screening, due diligence, and portfolio management, and empowers lenders with real-time insights that lower risk and boost revenue opportunities. Founded in 2017, Boss Insights is headquartered in Toronto, Ontario, Canada.

“The partnership of MX and Boss Insights demonstrates the power and role of connectivity and data in the future of finance,” MX EVP of Partnerships Don Parker said in a statement. “As a leader in Open Finance, MX is committed to expanding our partner ecosystem with reputable partners who align to our overarching mission and stringent data and security standards. Today’s partnership with Boss Insights demonstrates our commitment to Power the Open Finance Economy.”

The newly-announced collaboration with Boss Insights is one of a number of partnerships that Lehi, Utah-based MX has announced in recent weeks. Earlier this month, the company teamed up with omnichannel payments platform Qolo Partners to help fintechs and neobanks scale their businesses faster. In March, MX worked with fellow Finovate alum Fiserv to enable secure consumer financial data access and sharing. That same month, MX announced that it had forged a new data access partnership with the University of Wisconsin Credit Union.

Last month, President Joe Biden signed an executive order on ensuring responsible development of digital assets. The order, which comes at a time of rising interest in digital assets such as cryptocurrencies, seeks to protect consumers, financial stability, national security, and reduce climate risks.

We recently spoke with Peter Torrente, National Leader of KPMG’s Banking and Capital Markets practice, to gain some insight on how the executive order may impact banks and fintechs. With more than 30 years of experience, Torrente primarily works with global financial services companies.

What are the highlights of the executive order?

Peter Torrente: The U.S. has an interest in responsible financial innovation including the continued modernization of public payment systems. This executive order details the country’s first comprehensive government strategy for exploring digital assets. It outlines steps to reduce risks that digital assets could pose to consumers, investors, and businesses. It also addresses other important considerations such as financial stability and financial system integrity; combatting and preventing crime and illicit finance; national security; U.S. leadership in the global financial system and economic competitiveness; financial inclusion and equity; and climate change and pollution. Finally, it also explores a U.S. Central Bank Digital Currency (CBDC) by placing urgency on research and development of a potential digital version of the dollar.

What are the major implications for banks and fintechs?

Torrente: The executive order seeks to ensure that the largest financial regulators, including banking regulators in the United States, make coordinated plans to oversee the blockchain industry. I see this order as a good signal for a comprehensive set of regulations for the digital asset industry. First, the new laws and regulations will require banks and fintech companies involved in the digital asset industry to enhance their governance and control frameworks related to Anti-Money Laundering (AML) / Combating the Financing of Terrorism (CFT) processes. Second, this executive order indicated that the federal government sees digital assets as an important part of the economy and society; it creates opportunities for traditional banks take another look at their digital asset strategy. Lastly, it explores a U.S. CBDC, which would significantly impact domestic and international wire transfer processes. I also see this order as an encouraging signal for banks and fintech companies to push forward with financial innovations associated with the digital asset industry.

Will the executive order benefit end consumers? Or make them worse off? How?

Torrente: Yes, it has the potential to benefit end consumers. First, the initial set of regulations will focus on establishing the baseline rules to protect investors and consumers from fraudulent activities. It can create transparency for end consumers and help them make informed decisions. Second, this executive order promotes building innovative financial platforms. End consumers may benefit from improvements in business performance, efficiency, and enhanced financial inclusion through these innovations. Given digital assets have the potential to increase the speed of payments, it can vastly improve access to financial services, especially for low-income Americans often left out of the traditional banking system. Lastly, new policies and laws for the digital asset industry could potentially help reduce excessive price volatility and improve market stability as cryptocurrency becomes a mainstream financial technology.

Do you envision further regulations around ESG in the future?

Torrente: The pace of proposed rules and regulations related to ESG risk identification, measurement and disclosure has clearly accelerated over recent months. But when we take a step back, these regulatory actions are largely the result of growing interest from a variety of stakeholders – investors, analysts, community groups, and government leaders – who may have been focused on sustainability and ESG for years. There is a widespread desire among stakeholders for enhanced consistency and comparability across ESG targets and metrics. Standardized disclosure requirements are viewed as important to advancing the broader ESG agenda. Stakeholders’ expectations of companies’ ESG strategies, commitments and disclosures are only increasing, which may lead to additional regulatory guidance and focus.

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

Engage People is the only loyalty network that enables program members to pay with points directly at checkout. The global technology provider connects loyalty programs with global payment systems.

Features

It is a convenient, frictionless, and cost efficient tech solution that enables conversion of loyalty points to currency increasing consumer engagement and interaction.

Why it’s great

It offers easy integration with existing platforms and programs.

Presenter

Len Covello, CTO Covello is the Chief Technology Officer (CTO) at Engage People, leading the long-term technology vision of the company. He is responsible for driving continued innovation in the loyalty sector. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

Goalry is a unified “Money Mall” experience that converges personal finance management (PFM) with shopping to help members reach goals in one immersive space.

Features

Everything to achieve goals and comparison shop with a single login

Virtual real estate for embedded tech

Interactive and future-proof design

Why it’s great

Goalry’s platform improves the customer journey by providing a full funnel experience for everything finance and shopping in one virtual, immersive space.

Presenter

Ethan Taub, CEO & Founder Taub has 20 years of executive experience ranging from billion-dollar brands to startups. His mission is to unify a disconnected finance landscape to create efficiencies. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

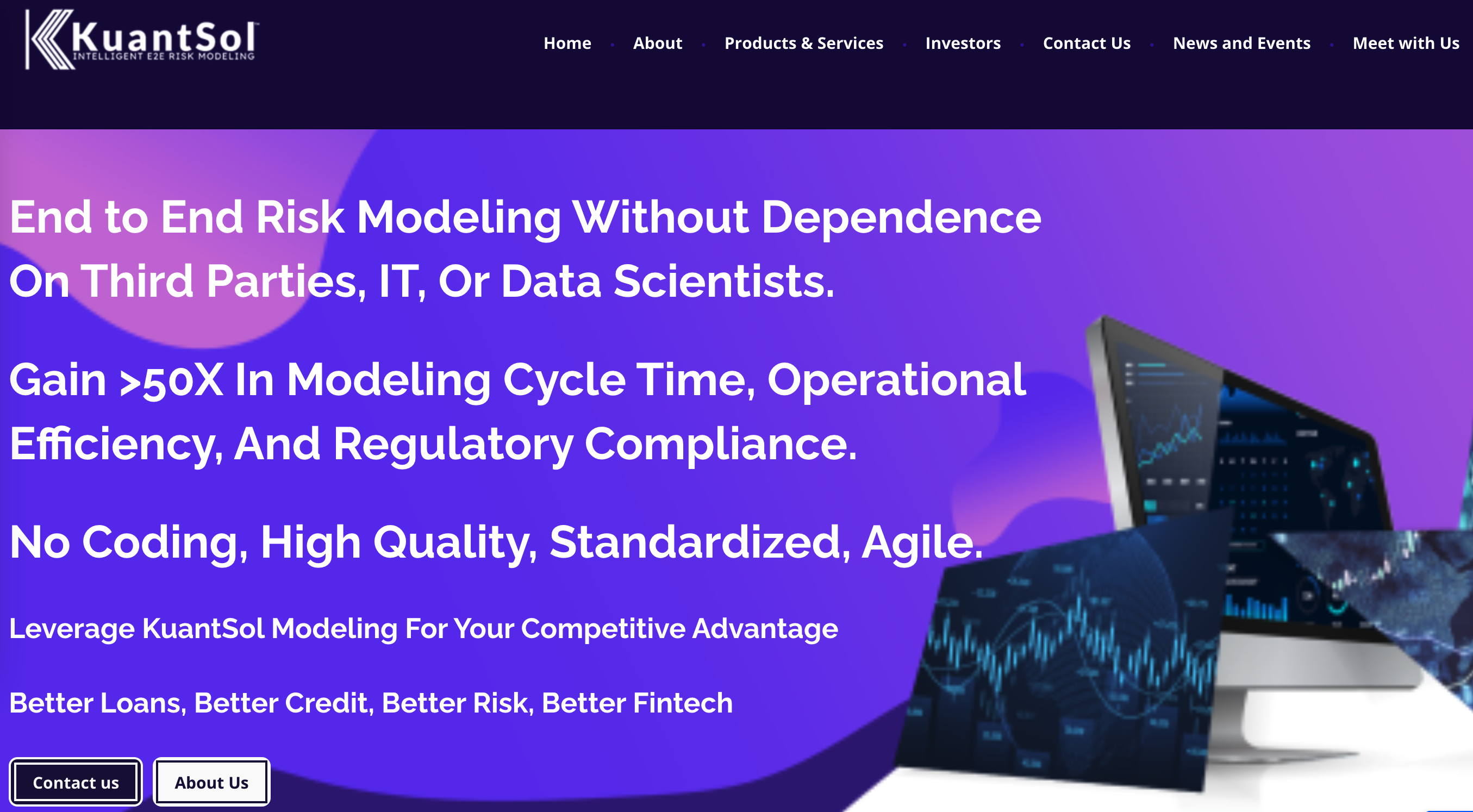

KuantSolEnterprise SaaS democratizes end-to-end modeling for banking, financials, and fintech. KuantSol drives more than 50X gain in operational efficiency, modeling time, quality, and compliance.

Features

Offers E2E modeling, validation, and compliance without dependence on data scientists, IT, and third-parties

Reduces cycle time from months to days

Reduces costs and resource requirements by more than 25X

Why it’s great

The first end-to-end risk modeling technology that is a one-stop shop for all time series and machine learning modeling that shortens cycle time and costs by more than 50X.

Presenters

Alex Shahidi, CEO & Co-Founder Shahidi is the Co-Founder of KuantSo and is a founder or member of five startups with two exits. He is a pioneer in SaaS and cloud technologies, author of papers and patents on data protection, transformation, and infrastructure. LinkedIn

Aytekin Oldac, Co-Founder & Chair of Board Co-Founder of KuantSol, a businessman, and founder of a health services provider, Aytekin is an investor of Code2 and Pyramos software. He has previously served with PwC and IBM Cloud and compliance. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

Spave lets users tap into everyday purchases to increase their savings, give to causes that matter to them, and have control and confidence in their finances. Spave transforms your spending, for good.

Features

We have a patent-pending engine that allows users to choose where they direct their spavings

Access to more than 1.5 million accredited U.S. nonprofits

Partners gain access to user insights

Why it’s great

Spave can help CUs empower their members to save more, give more, and live more by breaking down the barriers that hold them back. Empower your members to transform spending for good.

Presenters

Susan Langer, CEO Three words best describe Langer: Observer. Planner. Connector. Langer is a life-long learner and lover of people. Her 30-year professional journey within financial services, marketing and advertising, international development, and non-profit industries has taught her the value of listening to understand, the significance of appreciating others’ differences, and the extraordinary power of collaboration. LinkedIn

Sarah York, Chief Marketing & Digital Officer York is an active advocate for inclusive entrepreneurship and financial literacy. Her expertise spans data-driven growth, digital technology platforms, as well as global digital strategy. LinkedIn

Christen Wright, Head of Product Wright is a seasoned product leader, leading product for Reseda Group, a CUSO of MSUFCU. He has contributed to experiences at Delta, AT&T, and Best Buy. He was in 100 Black Men of Atlanta in 2020. LinkedIn

The investment includes $115 in debt funding and $60 in equity funding.

Wagestream will use the funds to add to its product lineup and fuel its U.S. expansion.

Earned wage access tool Wagestreamlanded $175 million in combined debt and equity funding today. The Series C round, which brought $115 in debt and $60 in equity, boosts the U.K.-based company to a total of $254 million in total funding.

New investors in the round include Smash Capital, BlackRock Innovation and Growth Trust, and Silicon Valley Bank. Existing investors Northzone, Balderton, QED, LocalGlobe, XYZ, Village Global, and Fair By Design also contributed.

Founded in 2018, Wagestream has offered one million workers access to $4.7 billion in wages that they’ve earned. The company considers one measure of its success as capital raised to liquidity released. Wagestream estimates that, prior to today’s investment, the company’s ratio was 1:55. That is, for every $1 of capital it raised, it released $55 of capital. “We’re aiming for a ratio of 1:100, meaning every $1 of capital raised by Wagestream will unlock $100 of impact for frontline workers,” said Wagestream Co-founders Peter Briffett and Portman Wills.

In addition to making that ratio possible, today’s investment will also power the development of new services, including an insurance offering that automatically adjusts coverage and premium, an app that enrolls users into optimal energy plans, fair credit without the need for a traditional credit score, and an intelligent savings installment plan.

Wagestream will also leverage the investment to expand internationally. Specifically, the company will focus on serving U.S. users. To fuel this move, Wagestream recently opened its U.S. headquarters in Washington, D.C.

Payment-card-as-a-service startup Deserveannounced it can now empower its banks and B2B clients via a new tool, the Commercial Card Platform, that enables customers to add a commercial payment card offering to their product lineup.

“We are extending our digital, cloud-native, mobile-first platform from consumer cards to commercial,” said Deserve CEO and Cofounder Kalpesh Kapadia. “With this, we will enable any financial institution or platform that serves other businesses to embed and issue commercial credit cards. For non-banks, this can be a significant source of revenue and can enhance brand loyalty. Our platform will enable those who serve small and medium-size businesses and corporations to offer true credit combined with sophisticated expense management.”

Formerly known as SelfScore, Deserve has re-imagined traditional credit cards by transforming the application and onboarding processes, as well as the credit card itself by bringing them into the digital-first era. The company enables businesses to provide a white-labeled or co-branded card program made possible via a set of configurable APIs and SDKs.

The new Commercial Credit Card product helps companies, banks, and online lenders offer a white-labeled or co-branded credit card product for their business customers. The full-service card product offering will include underwriting, instant virtual card issuance, digital wallet provisioning, and enterprise controls that will enable management to track, manage, and understand business expenses.

Customers Bank, which is headquartered in Pennsylvania and counts $19.6 billion in assets, will be the first bank on Deserve’s Commercial Card Platform. “Together with Deserve, we are looking forward to offering an exciting and valuable product to our small business customers, combining credit with powerful expense management,” said Customers Bank President and CEO Sam Sidhu.

Founded in 2013, Deserve raised an undisclosed amount of funding from Visa last fall, adding to the company’s $287 million in total funding. Among Deserves investors are Mastercard, Goldman Sachs Asset Management, Sallie Mae, Ally Ventures, Visa, Accel, Pelion Venture Partners, Aspect Ventures, and Mission Holdings.

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

EG3C’s Financial Wellness Center helps credit unions build financial literacy with their members and community through interactive, educational content delivered via website, mobile app, API, or SDK.

Features

Created by a credit union for credit unions

Offers content that can be private-labeled and customized

Provides access to user data and dashboard, and CMS to supplement with your own content

Why it’s great

Creating good educational content is very time consuming. By leveraging EG3C’s Financial Wellness Center, employees can spend more valuable time engaging with members and the community.

Presenters

Ben Maxim, CTO at Reseda Group and VP Digital Strategy & Innovation at MSUFCU Maxim serves in a dual role as Vice President of Digital Strategy and Innovation for MSUFCU and as Chief Technology Officer for MSUFCU’s wholly-owned CUSO Reseda Group and its subsidiary companies. LinkedIn

April Clobes, President & CEO at MSUFCU and CEO of Reseda Group Clobes is President & CEO at MSU Federal Credit Union and CEO of Reseda Group, MSUFCU’s wholly owned CUSO. She has established MSUFCU as a leader in innovation in the CU space. LinkedIn