This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

FIS launches Smart Basket, a checkout solution that uses real-time, item-level intelligence to optimize payment methods, rewards, and savings for each purchase.

The platform blends FIS’ payments, loyalty, and spend technologies to give shoppers granular payment choices, including HSAs, and help merchants reduce costs while boosting loyalty.

The launch positions FIS in the agentic AI payments race, turning checkout into a proactive decision engine that anticipates consumer needs and personalizes outcomes.

Fintech giant FIS announced its latest planned launch, Smart Basket, this week. The new tool aims to enhance the payment experience at checkout with real-time, item-level adjudication.

The new transaction gateway analyzes an individual’s shopping behavior and applies optimal rewards and payment methods at checkout. The proactive, automated approach helps shoppers save money and earn rewards while increasing brand loyalty for the merchant.

The solution combines FIS’ real-time payments gateway, its loyalty platform, and its filtered spend technologies to differentiate its payment network. Notably, Smart Basket will allow shoppers to select which payment method to use for each individual item they are purchasing. In addition to using traditional debit, credit, and prepaid cards, Smart Basket will allow flexible healthcare spending accounts to be used as payment methods. FIS anticipates that this will lower payment costs while enabling customized loyalty and rewards programs at highly targeted levels.

“Smart Basket represents a significant leap forward in how money can be moved and put to work during the search and shopping experience,” said FIS President Jim Johnson. “By leveraging real-time, item-level intelligence, Smart Basket is seeking to deliver personalized value and frictionless savings to consumers while providing retailers and brands with increased sales and insights they need to optimize their strategies. This will be a game-changer for the industry, and we are excited to bring more value to buyers, sellers, and brands wherever money flows.”

Launching Smart Basket positions FIS within the emerging agentic AI payments landscape. In the past few months we’ve seen a handful of big tech and fintech companies, including Walmart, OpenAI, Google, and Splitit, launch payments capabilities that transform payments into an embedded capability rather than a separate checkout destination.

By leveraging real-time, item-level data to make proactive decisions about payment methods, loyalty redemptions, and savings opportunities, Smart Basket will optimize the checkout experience from a passive endpoint into a dynamic, automated decision engine. This shift aligns with growing consumer expectations around seamless, smart payments that anticipate needs, maximize value, and personalize outcomes.

Many businesses approach fintech in a fragmented way. They are forced to stitch together multiple payment systems, APIs, banking partners, and integrations just to achieve basic functionality.

Patricia Montesi, Founder and CEO of Qolo, explains in a FinovateFall video interview how her platform is solving that complexity for banks, fintechs, and enterprises. Qolo offers a unified payments stack through a single API that enables institutions to modernize their payments infrastructure without expensive and risky rip-and-replace of legacy systems.

In the video, Montesi delves into embedded ledgers, real-time rails, and how Qolo can overlay existing cores in under nine months while positioning clients for the next generation of payments, such as stablecoins and novel rails.

“We set out to build an entire, comprehensive payments stack that includes ledger, card, payments, virtual account management—everything all available through a single API served up to you so that you can then focus on your customers.”

Patricia Montesi is a seasoned payments veteran with over 20 years of experience across banking and fintech. Prior to Qolo, she held leadership roles driving innovation in payments and scaling complex platforms. Her deep domain expertise across card processing, FX, bank partnerships, and regulatory environments gives her insight into the pain points that banking partners face when retrofitting modern payments capabilities.

Qolo was founded in 2018 with the aim to simplify payments by offering a comprehensive payment stack, including an embedded ledger, card issuing, money movement, real-time reconciliation, and cross-rail connectivity on a single API. Rather than forcing banks to rip out their core, Qolo overlays its platform directly atop existing systems, enabling deployment in under nine months. This sidecar-oriented architecture lets institutions adopt new payment rails without disrupting core banking operations.

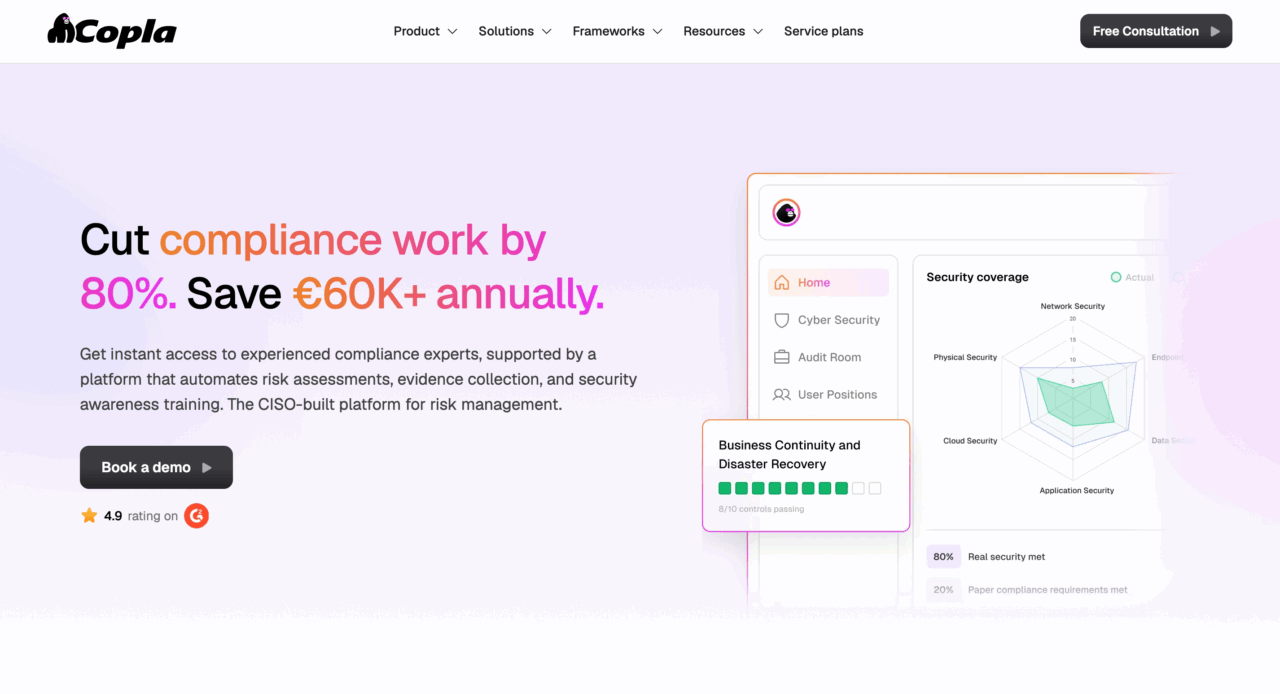

Lithuanian cybersecurity platform Copla has teamed up with Baltic-based bug bounty platform Buck4Bug.

The partnership will enable Copla clients to leverage Buck4Bug’s team of ethical hackers to identify cybersecurity vulnerabilities before attackers have the chance to exploit them.

Rebranding from CyberUpgrade earlier this year, Copla made its Finovate debut at FinovateEurope 2025 in London.

ICT security and compliance automation platform Coplaannounced a partnership with Baltic-based bug bounty platform Buck4Bug. The partnership will enable Copla customers to request and manage offensive testing directly inside the platform, launching scoped engagements for web, mobile, API, and cloud, or running continuous bounty programs.

“Real security isn’t just about controls, it’s about continuous proof,” Copla noted on its LinkedIn page announcing the partnership. “That’s why we’re partnering with Buck4Bug to bring together two powerful forces: automated compliance and monitoring from Copla and crowdsourced testing from a trusted network of ethical hackers. Together, we’re making it easier for companies to move beyond checklists and into real resilience.”

Buck4Bug combines deep manual expertise with focused tooling to discover security vulnerabilities that scanners often miss. The company connects organizations with ethical, “white hat” hackers to find and fix cybersecurity vulnerabilities before attackers do, validating and documenting each issue to ensure reproducible remediation. Courtesy of the newly announced partnership, Copla will convert Buck4Bug’s findings into action: prioritizing tasks, tracking fixes, scheduling retests, and providing evidence that enables teams to seamlessly move from discovery to demonstrable risk reduction.

“Modern security isn’t about snapshots, it’s about feedback loops,” Buck4Bug founder Paulius Šliavas said. “Together with Copla, we’re turning every pentest into actionable risk reduction and measurable compliance outcomes. Our hackers surface the hard-to-find issues; Copla makes sure fixes stick, risks trend down, and auditors see the story.”

Based in Vilnius, Lithuania, and founded in 2024, Buck4Bug offers bug bounty programs, penetration testing, and auction-based IT audits—all via a single platform. The company’s partnership news with Copla comes in the wake of Buck4Bug’s announcement that it has joined the Startup Lithuania Accelerator, powered by Plug and Play Tech Center, and launched its first public bug bounty program in collaboration with Fjord Bank.

Founded in 2023 and headquartered in Vilnius, Lithuania, Copla made its Finovate debut at FinovateEurope 2025. At the conference, the company demonstrated its ICT security and compliance automation platform that provides a full cybersecurity and compliance department at a subscription cost. The platform combines CoreGuardian, which ensures compliance with frameworks such as DORA; an AI-powered co-pilot to provide real-time education, assessments, and alerts to boost accountability; and VendorGuard, which simplifies vendor management by handling risk assessments, incident planning, and prioritization.

Formerly known as CyberUpgrade, the company rebranded earlier this year in a move designed to reflect its evolution beyond cybersecurity.

“After years of growing, evolving, and helping organizations secure their digital environment, we’re stepping into an exciting new phase,” the company noted on its LinkedIn page. “We are now Copla—our new name, our new vision, and our next stage of evolution. Why Copla? Because we’re no longer just about cybersecurity. COmpliance PLAtform reflects everything we do today: empowering organizations to manage compliance, risk, and security with one intelligent platform. Same team. Bigger vision. A name that matches our mission.”

Upgrade has raised $165 million in a Series G round, boosting its total funding to $750 million and valuing the fintech at $7.3 billion.

Founded by Lending Club pioneer Renaud Laplanche, Upgrade has served 7.5 million customers, facilitated $42 billion in credit, and continues to grow profitably with a multi-product strategy spanning loans, cards, BNPL, and savings tools.

The late-stage round positions Upgrade near a potential IPO inflection point, signaling strong investor confidence in alternative lending models and the company’s ability to compete with both challenger and traditional banks.

It’s time for mobile banking and lending fintech Upgrade to get an upgrade of its own. The California-based fintech announced today that it landed a $165 million equity investment to enhance its credit and banking products aimed at retail customers. The round boosts the company’s total funding to $750 million since inception.

The Series G Preferred Round, which was led by Neuberger, indicates that this is a late-stage financing event, given that Upgrade has matured significantly in revenue, consumer adoption, and market presence. LuminArx Capital Management also contributed, and existing shareholders, including DST Global, Ribbit Capital and others, also increased their investment. While this stage and type of round could indicate that Upgrade is preparing for an IPO, it could also signal that the company is planning to delay its IPO, offering liquidity to prepare for a later exit.

According to Upgrade CEO and Co-Founder Renaud Laplanche—who previously founded and led early fintech pioneer Lending Club—Upgrade’s valuation now sits at $7.3 billion.

Founded in 2017, Upgrade is a digital banking platform headquartered in California. The company offers checking and savings accounts, personal loans, credit cards, and rewards programs that focus on low fees and responsible credit usage to help consumers improve their financial lives. Upgrade has served 7.5 million customers and has facilitated over $42 billion in credit with tools such as its Upgrade Card, which encourages customers to pay off balances quickly and avoid revolving debt and build credit responsibly.

In 2024, Upgrade launched the Flex Pay brand, which it rebranded from Uplift. The BNPL tool serves 750 travel and retail brands, helping them to increase their customer engagement, loyalty, and consumer spending by offering more flexible payment options. Upgrade also offers cashback rewards, competitive savings rates, and credit monitoring tools, positioning itself as a customer-friendly alternative to traditional banks.

As part of today’s deal, Neuberger Head of Specialty Finance Peter Sterling is joining Upgrade’s Board of Directors.

“Upgrade presents an unmatched opportunity in fintech,” said Sterling. “As many companies in the space struggle with acquisition costs and monetization strategy, Upgrade has sustained profitable growth through a multi-product, multi-channel strategy that relies on low-cost, proprietary distribution channels to acquire new customers and its ability to monetize users through multiple products. We have known Renaud and the Upgrade founding team for over a decade and are very excited to expand our partnership.”

Upgrade’s growth momentum has continued to build, reflected in several major milestones. The company has surpassed $2 billion in cumulative home improvement financing just three years after launching the product, and has already exceeded $1 billion in auto financing within two years of that product’s debut.

“We are thrilled to expand our relationship with Neuberger and welcome Peter as a new board member,” said Laplanche. “We are planning to use the new equity capital to keep developing new products and expand distribution to achieve our goal of helping more mainstream consumers get the banking and credit products they need today, while improving their financial and credit standing in the long run.”

Upgrade’s raise is a great indication that there is still consumer and investor appetite for alternative consumer lending options. Upgrade has managed to sustain profitable growth while scaling to millions of users. The company’s diversified product lineup positions it to compete with both challenger banks as well as traditional banks. Upgrade’s $7.3 billion valuation, combined with leadership from a seasoned founder who helped define the early fintech era places Upgrade at an IPO inflection point.

This week I’m looking at a trio of stories from the wealthtech beat: SS&C’s completed acquisition of Calastone, the emergence of a new UK-based wealthtech, and a look at two, not-quite-contrasting interpretations of funding for wealthtechs in Q3 2025.

SS&C Technologies completes $1 billion acquisition of Calastone

Initially reported in July, SS&C Technologies announced this week that it has completed its acquisition of Calastone. The company purchased Calastone, a London-based, international funds network and provider of technology solutions to wealth and asset managers, from global investment firm Carlyle for a price of £766 million ($1.03 billion). The transaction was funded via a combination of debt and cash.

“Calastone’s network and technology further strengthen SS&C’s leadership across global fund operations,” Chairman and CEO of SS&C Technologies Bill Stone said. “Together, we will accelerate innovation for our clients, expand our reach, and continue to simplify the way the industry operates.”

The acquisition will bolster SS&C’s solutions for fund administration, transfer agency, AI, and intelligent automation. The union will also facilitate the launch of a unified, real-time operating platform to lower costs, complexity, and operational risk for fund industry participants while providing enhanced distribution, investor servicing, and operational scalability.

Founded in 1986 and headquartered in Windsor, Connecticut, SS&C Technologies provides mission-critical, cloud-based solutions to more than 22,000 companies in financial services and healthcare. A member of the Fortune 1000 and a publicly traded firm on the NASDAQ under the ticker SSNC, SS&C Technologies is the largest independent hedge fund and private equity administrator, and the largest mutual fund transfer agency, in the world.

Calastone runs the largest global funds network, linking more than 4,500 financial organizations worldwide across 57 markets. The company processes more than £250 billion ($334 billion) of investment value each month, and maintains offices in Luxembourg, Hong Kong, Taipei, Singapore, New York, and Sydney. With the completed acquisition, Calastone’s 250 employees will join SS&C Global Investor & Distribution Solutions, effective immediately.

“This is an exciting new chapter for Calastone,” company CEO Julien Hammerson said. “Joining SS&C gives our clients and employees access to greater scale, investment, and opportunity. We’re proud of what we’ve built and look forward to contributing to SS&C’s continued growth and global success.”

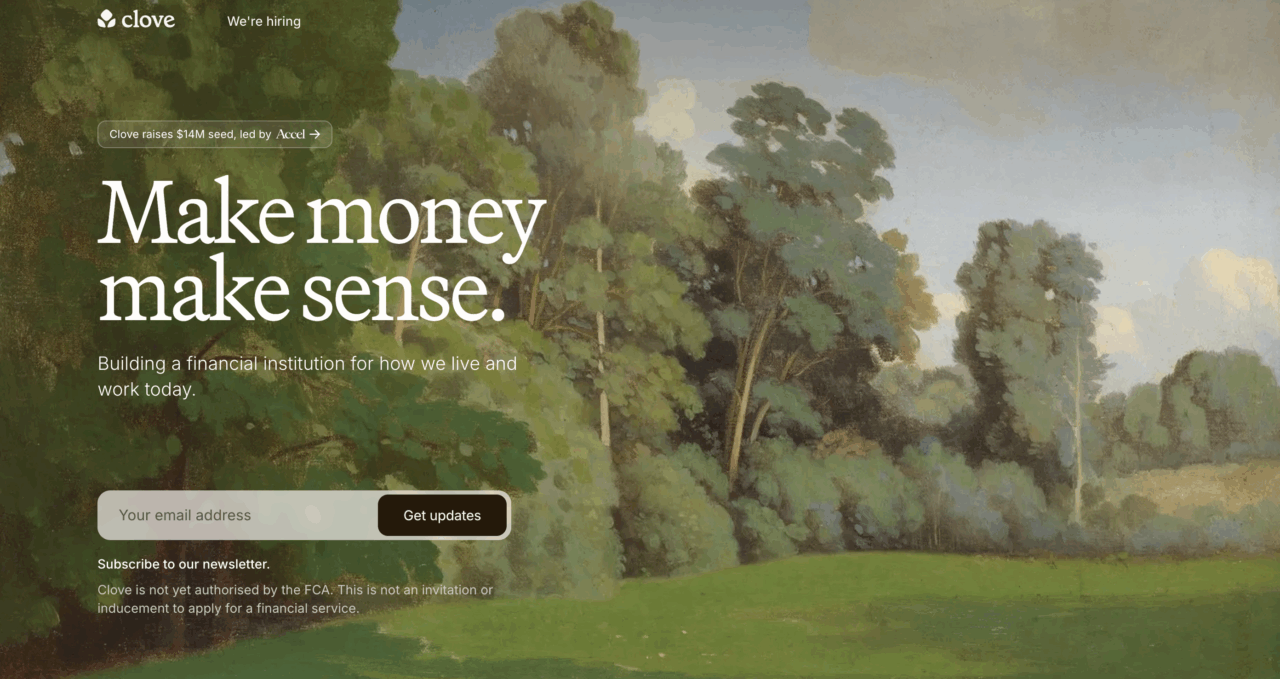

UK wealthtech Clove emerges from stealth

London-based wealthtech Clove has emerged from stealth with €12 million ($14 million) in pre-seed funding in its coffers. The round, which was led by Accel, is regarded as one of the largest early-stage financings for a European startup this year. Kindred Capital VC and Air Street Capital also participated in the investment, along with a handful of angel investors.

“With Clove, we are seeking to break the traditional economics of financial advice by combining the expertise of human advisers with the efficiency of AI,” Co-Founder Alex Loizou said. “Our goal is to make financial planning more accessible, affordable, and effective than ever before, for everyone from young professionals and aspiring entrepreneurs, to growing families and those starting to think about retirement.”

Clove was launched by Loizou and fellow founder Christian Owens at a time when the UK’s Financial Conduct Authority has determined that professional financial advice can make a significant difference—as much as 10%—in financial outcomes compared to those who do not have access to this advice. Loizou and Owens see an opportunity to provide this advice via a combination of human insight and AI intelligence.

“Our aim is to make it possible to deliver high-quality, personalized advice at an unprecedented scale,” Owens wrote on the Clove blog. “As we started exploring this problem we discovered that most of what financial advisers do isn’t actually advice, it’s admin. By using AI to reduce that burden, we hope to give advisers more time to do what they are trained to do: help people make better decisions.”

Clove will use the funding to hire additional talent ahead of a full launch in 2026, subject to FCA authorization.

Smaller, but busier? Wealthtech deal activity up, total funding down in Q3 YoY

According to FinTech Global Research, wealthtech investments in the US dropped significantly year over year in Q3 2025. Deal activity was robust by comparison, with 71 deals in Q3 2025 compared to 62 deals in Q3 2024, but total funding dropped to $861 million this year in the third quarter compared to $1.8 billion raised in Q3 2024. The average deal value also declined, falling to $12.1 million this year from an average of $28.8 million in Q3 2024.

The analysts cited “persistent macroeconomic uncertainty” and, interestingly, “evolving wealth management technologies” for what it said was a cautious, “lower-risk” approach by investors.

To that final point, there may be reason for optimism. Looking out over a longer time frame, the CB Insights State of Fintech Q3’25 Report noted that wealthtech funding was “maintaining momentum” and on track to double 2024 totals, having already topped 2024 levels. In fact, CB Insights highlighted “strong confidence in digital-first wealth management solutions” and vigorous hiring as positive signs. The report noted that financial advisor productivity tools, wealth management banking and lending platforms, and AI investment intelligence platforms were among the top sectors in fintech in terms of headcount growth year-over-year.

Data management and payments infrastructure company Basis Theory has raised $33 million in Series B funding in a round led by Costanoa Ventures, along with Stage 2 Capital and Moneta VC.

The investment, which takes the company’s total capital raised to $50 million, will be used to help expand its payment vault for merchants, as well as fuel the company’s innovations in agentic commerce.

Founded in 2020, Basis Theory made its Finovate debut at FinovateSpring 2022 in San Francisco. Colin Luce is CEO.

Data management innovator Basis Theory has secured $33 million in Series B funding. The round was led by Costanoa Ventures alongside Stage 2 Capital and Moneta VC. The investment also featured participation from existing investors including Bessemer Venture Partners, Kindred Ventures, Box Group, and Offline Ventures. The Series B takes Basis Theory’s total capital raised to $50 million, according to Crunchbase.

“This funding represents more than capital,” company Co-Founder and CEO Colin Luce wrote on the Basis Theory blog this week. “It validates our mission of giving merchants control over their payments data and the flexibility to innovate on their own terms.”

Basis Theory lives at the intersection of technology and commerce. The company’s PCI Level 1, SOC2 type II, and ISO 27001-compliant vault offers fintechs and merchants broad flexibility and customization as they build their payment infrastructures and create payment stacks that suit their individual needs. As merchants look for superior ways to manage payment data across a growing number of payment service providers, Basis Theory offers a technology that enables them to tokenize and manage sensitive payment data while maintaining complete control over how that data is accessed both within their own systems as well as when it is shared with third parties. This week’s funding will help Basis Theory expand its enterprise-grade payment vault for merchants around the world, as well as power the company’s work in agentic commerce.

“The payments ecosystem is changing rapidly, and merchants no longer want to be locked into rigid platforms,” Luce said. “We’re giving control back by making payments data as accessible and programmable as any other data type so it can fuel growth, intelligence, and automation across the entire business.”

Basis Theory’s payment vault, which is independent of any payment processor or orchestration layer, also serves as a foundation for agentic commerce and the Agentic Commerce Consortium. Launched last month by Basis Theory, the consortium is a network of more than 20 companies that are collaborating to define the standards and infrastructure that will enable AI agents to become trusted buyers. This will empower merchants to embrace agentic commerce safely and at scale.

In a statement introducing the consortium, Luce acknowledged that other entities have also articulated agentic AI standards, such as Google with its Agent Payments Protocol (AP2). At the same time, Luce suggested that the underlying infrastructure must be improved first. “Our view is that we must start by modernizing the existing underlying foundational infrastructure via APIs, but done in a way where AP2 or MCP or KYA or any other protocol can be built on top of or wrapped around it,” Luce wrote. “It’s too early to know which protocols will gain adoption or whether who is behind the protocol will dictate said adoption.”

Founded in 2020, Basis Theory made its Finovate debut at FinovateSpring 2022. At the conference, the company introduced its tokenization platform and showed how its data tokenization API offers a developer-first approach to ingesting and managing high-risk data such as credit cards or personally identifiable information (PII). The technology’s use cases extend from fintech, e-commerce, and the creator economy, to subscription platforms, vertical SaaS, and digital health.

Ethical, UK-based savings and loan Charity Bank announced a strategic partnership with digital banking solutions provider Sandstone Technology to power development of its mobile savings app.

Charity Bank and Sandstone Technology have been collaboration partners for more than a decade.

Headquartered in Sydney, Australia, Sandstone Technology made its Finovate debut at FinovateEurope 2012, and most recently demoed on the Finovate stage at FinovateEurope 2016.

Charity Bank has forged a strategic partnership with Sandstone Technology to power development of its new mobile savings app. The app will offer a variety of enhanced, self-service capabilities, feature robust security, and provide a suite of modern tools to help meet the needs of Charity Bank’s customers. The technology supports seamless updating, rapid product launches, and a consistent user experience. The app is expected to be available to Charity Bank customers in the spring of 2026.

“Partnering with Charity Bank on this initiative is both exciting and rewarding,” Sandstone Technology Chief Customer Officer Jennifer Harris said, “Mobile is now the channel of choice across all demographics, and this solution reflects the importance of delivering banking experiences that are intuitive, flexible, and future-ready. Our collaboration is built on trust and innovation, and this project showcases our shared vision for the next generation of digital banking.”

Charity Bank is an ethical savings and loan wholly owned by charitable foundations, trusts, and social purpose organizations. The institution uses savers’ deposits to provide loans to organizations in the UK that are working toward positive social change for individuals, communities, and the environment. Since 2002, Charity Bank has lent more than £600 million to charities and social enterprises across the UK.

Sandstone Technology is a long-time technology partner of Charity Bank, having collaborated for more than a decade. The current partnership to develop the institution’s mobile app represents the latest milestone in Charity Bank’s digital transformation journey designed to enhance the customer experience and make access to ethical banking available to more banking customers.

“We are thrilled to take this next step with Sandstone Technology,” Charity Bank Director of Operations and Savings Justin Hort said. “Launching a mobile app is a major milestone that reflects our commitment to evolving with our savers’ needs. We’re focused on delivering a seamless, modern and intuitive experience—and with Sandstone’s proven track record, we knew they were the right partner to bring this vision to life.”

Headquartered in Sydney, Australia and founded in 1996, Sandstone Technology made its Finovate debut at FinovateEurope 2012. The company, which offers solutions for loan origination, digital banking, and digital onboarding, most recently demoed on the Finovate stage at FinovateEurope 2016. Abhish Saha was appointed CEO in 2022 after previously serving as the Executive General Manager of the company’s Digital Banking & Elevate business unit. Saha replaced Michael Phillipou, who had been Sandstone Technology’s CEO since December 2020.

More recently, Sandstone Technology earned recognition for its partnership with UK-based Chetwood Bank, helping the institution deploy its digital savings platform that has contributed to a 39% increase in customers completing the application process and opening a savings account.

October is National Cybersecurity Awareness Month in the US—although those in fintech and financial services can be forgiven for feeling as if every month is cybersecurity awareness month.

This is not to say that the threat of fraud and financial crime is any less important in health care, consumer technology, or any other sector of the economy. But the facts are hard to ignore. According to the New York Federal Reserve, financial services companies face 300x more cyber attacks compared to companies in other industries. After all, that’s where the money is—to say nothing of a treasure trove of data on banking customers, borrowers, investors, and more.

Additionally, the impact of fraud and financial crime on financial services companies and their customers can be significantly greater, as well. Estimates indicate that the average breach cost in the financial sector is more than $6 million, compared to the global average of $4.9 million. In fact, the financial services sector is second only to healthcare when it comes to the average cost of a data breach.

Released in the first half of the year, Alloy’s 2025 State of Fraud Report noted that a sizable number (60%) of financial institutions and fintechs reported fraud growth across both consumer and business accounts over the past year. The good news is that, unlike in AI, where there remains some skepticism about the potential benefits versus costs and risks, Alloy observed that 87% of institutions queried believed that investing in fraud prevention—especially via deploying identity risk solutions, building in-house anti-fraud solutions, and adding talent to fraud teams—outweighed the costs.

More recent reports on fraud and financial crime underscore additional challenges. The Kroll 2025 Financial Crime Report, which surveyed 600 international executives, noted that a growing number of executives fear an acceleration in financial crime, with 71% believing financial crime risks will increase in 2025 compared to 67% in 2023. Alarmingly, the executives also confessed a sizable gap between their concerns about the accelerating pace of financial crime and their own organization’s preparedness to fight it, with only 23% of those surveyed believing their compliance programs were up to the task.

As for the question of whether AI is an effective tool to fight financial crime or a new and dangerous weapon in the hands of fraudsters, the answer, unsurprisingly, is “yes.” Just over half of those executives surveyed (57%) believe AI is a benefit to fighting financial crime while just under half (49%) believe AI represents a significant risk and vector for fraud.

Best of Show winners lead the fight against financial crime

With fraud and financial crime threats on the rise, it is no surprise to see a growing number of companies on the Finovate stage whose innovations are dedicated to fighting fraud, scams, and other financial crime. In fact, 2025 was the first year since COVID that featured a fraud fighter in every Best of Show winning cohort: FinovateEurope, FinovateSpring, and FinovateFall.

Here’s a look at some of our Best of Show winning alums from recent years who are innovating in the field of financial crime and fraud prevention.

Casap – Offers a co-pilot and collaboration platform that fully automates dispute management and empowers financial institutions and fintechs to more effectively fight first-person fraud.

Founded in 2022

Headquartered in New York

Shanthi Shanmugam is CEO and Co-Founder (LinkedIn)

Herd Security – Leverages AI-driven detections, training content, phishing simulations, and exercises to make users an active and engaged part of defending their companies and organizations from fraud and cybercrime.

Keyless – Equips companies with biometric authentication technology that reduces account takeover (ATO) fraud by up to 80%, and verifies a user’s genuine identity in addition to their device in 300ms or less.

Founded in 2019

Headquartered in London, UK

Andrea Carmignani is Co-Founder and CEO (LinkedIn)

Illuma – Offers a real-time voice authentication solution that replaces traditional knowledge-based authentication, enhances the caller experience, and improves operational efficiency while preventing fraud in contact centers.

Corsound AI – Leverages 200+ patents to provide voice-to-face and real-time deepfake detection. The company’s technology leverages the unique correlation between voice and facial features to authenticate identities accurately.

1Kosmos – Combines identity proofing, credential verification, and strong authentication to enable remote identity verification and passwordless multi-factor authentication to enable workers, customers, and residents to securely utilize digital services.

Trulioo – Covering 195 countries, Trulioo offers an identity platform that verifies more than 14,000 ID documents and 700 million businesses, while checking against more than 6,000 watchlists.

Founded in 2011

Headquartered in Vancouver, British Columbia, Canada

This article is brought to you in collaboration with Gregory FCA.

AI and personalization are redefining the rules of engagement in business banking. As Executive Vice President and Chief Product Officer for Business Banking at U.S. Bank, Shruti Patel (pictured) brings a unique lens to the discussion, drawing from her deep experience in banking, payments, and fintech.

Following her appearance at FinovateFall 2025, we sat down with Shruti to discuss the evolving needs of business customers, the transformative role of AI, and the growing importance of partnerships between banks and fintech.

Tell us a little bit more about your role at U.S. Bank, your title, and what you’re responsible for.

Shruti Patel: I am the Executive Vice President, Chief Product Officer for Business Banking at U.S. Bank. In this role, I oversee services for our small business customers, ranging from $100,000 to up to $50 million in annual revenues, across banking, payments and our full suite of digital capabilities.

You spoke on the panel about the customer experience revolution. In your view, what do today’s business banking customers expect from their financial partners that they didn’t expect five or ten years ago?

Patel: We consistently hear two key expectations from our small business customers. First, they want banks to deliver best-in-class, highly sophisticated digital capabilities. Nearly 80% of small business customers, including U.S. Bank customers, have time and again told us that they’re expecting their banks to give them a one-stop shop. Many are already banking with us across our deposit products. They engage a lot with our payment products, whether this is small dollar loans, large dollar loans, or credit card solutions, or operating lines of credit.

But beyond these core services, they increasingly expect seamless, integrated digital experiences. By that, I mean not just dashboards that track transactions, but robust features like money moment insights, best-in-class accounts payable and receivable tools, and embedded payroll capabilities. To address these needs, we recently announced two exciting developments: our new accounts payable solution in partnership with Melio and Fiserv, and embedded payroll capabilities in partnership with Gusto. Both are part of our broader commitment to delivering integrated, end-to-end experiences for small business customers.

AI is everywhere in the conversation this year. Beyond the hype, how are you seeing AI deliver real value to business banking customers, whether through engagement, personalization, or entirely new experiences?

Patel: We are still in the early stages of deploying AI, but we’re already seeing strong impact across several use cases. The first is fraud monitoring and detection—security is top of mind for our business banking customers, and AI has proven valuable for fraud monitoring early detection.

The second area is customer service. While not a new application for AI, we’re using it to transcribe interactions, synthesize information, and provide our service teams with a complete view of the customer relationship. Because business owners are pressed for time, they expect seamless, efficient support from us, and AI helps ensure our teams can respond quickly and effectively.

We’ve seen a wave of innovation in areas like billpay and payroll, often driven through partnerships between banks and fintechs. Why are these types of collaborations becoming so important for small business banking?

Patel: As I mentioned earlier, small business customers are navigating an unprecedented macroeconomic environment. They’re dealing with tariff pressures and uncertainty, persistent inflation, supply chain disruptions lingering from the pandemic, and ongoing challenges in accessing capital. In this context, anything financial institutions can do to help small businesses operate more efficiently and cost-effectively is critical—not only for their success but also for deepening engagement and trust.

That’s where fintech partnerships have become so important. Business owners often tell us they feel overwhelmed by the number of software options available. They’re looking for simple, integrated solutions that support core needs like cash flow management, accounts payable and receivable, and payroll. For example, if you’re a small business with fewer than 10 employees, you want easy-to-use payroll software that just works.

With this in mind, we’ve anchored our strategy on fintech partnerships and selective acquisitions to create a one-stop shop. We launched embedded payroll capabilities with Gusto, accounts payable solutions with Fiserv in partnership with Melio, and made strategic acquisitions such as talech, a point-of-sale solution, Bento for spend management, and TravelBank, which complements our corporate card offering. Together, these investments strengthen our ability to support small businesses end-to-end.

As you reflect on FinovateFall, what are the biggest themes or innovations you heard about that excite you about the future of business banking?

Patel: For me, the most exciting theme is personalization. I participated in a session on AI and personalization, and it reinforced that while banks and financial institutions have access to strong data, we still have a long way to go in harnessing it effectively. Accompanying customers through their end-to-end journeys and across different stages of the business lifecycle is critical.

For example, the needs of a startup are very different from those of a mature, established business. A startup might be focused on accessing small-dollar loans, while established businesses may require large operating lines to scale and expand. Small businesses need a very simple operating account with some benefits around digital transactions and money movement, but our large customers are looking for robust money movement capabilities and Treasury solutions.

The key is building personalization into these core jobs. Customers frequently ask us: “Should I be using Faster Payments or ACH?” That’s where AI can help, by serving as a product recommender that guides business owners to the right solution based on their specific needs.

As the week begins, we’re checking in on news of big funding in fraud prevention and cross-border payments, major developments on the crypto front for both Citi and JPMorgan, as well as new report from Alessa on how AI stands to enhance AML processes in 2026. Be sure to check back all week long for the latest in fintech news here on Finovate’s Fintech Rundown!

Payment solution provider and acquirer Paystraxacquires UK fintech Nochex.

International payments platform LemFiunveilsSend Now, Pay Later service combining credit and remittances.

Stax Paymentsgoes live with Stax Processing, a full-stack end-to-end payments processor.

Crypto and DeFi

Crypto payments company MoonPayintegrates with crypto trading, earning, and exploring terminal, Axion.

Crypto wallet Cake Walletannounces integration of xStocks, new functionality that enables users to invest in tokenized stocks and ETFs via Web3 self-custody.

Digital banking platform Bankjoy has teamed up with digital investment solutions provider InvestiFi.

The partnership will enable customers and members of community banks and credit unions to invest in stocks, ETFs, and cryptocurrencies directly from their checking accounts.

Michigan-based Bankjoy most recently demoed its technology on the Finovate stage at FinovateFall 2023. InvestiFi made its Finovate debut as CryptoFi at FinovateFall 2022 and rebranded in 2024.

Digital banking platform Bankjoy has forged a strategic partnership with fellow Finovate alum InvestiFi, a provider of digital investment solutions. The partnership will enable community banks and credit unions that use Bankjoy’s digital banking platform to offer their customers and members the ability to invest in stocks, ETFs, and cryptocurrencies directly from their checking accounts.

The partnership comes as a growing number of fintechs are empowering smaller, more community-focused financial institutions to directly offer investment services. Last week we noted the partnership between two-time Finovate Best of Show winner Eko and Brooklyn Coop FCU as another example of fintech/financial institution partnerships designed to make it easier for customers and members to invest without having to leave the comfort and familiarity of their digital banking platforms.

“With deposit outflows to platforms like Robinhood accelerating, community banks and credit unions must meet members where they already are: inside their banking app,” Bankjoy COO and Co-Founder Weiwei Duncan said. “By embedding wealth management tools directly into digital banking, they not only keep members engaged with their own products, but also strengthen loyalty and competitiveness in a fast-changing market.”

The threat to credit unions and community banks from these new platforms is not just that their members and customers will use them for their investments; many of these platforms are looking to grow by adding banking services to their digital brokerage offering. Partnerships between fintechs like Bankjoy and InvestiFi are designed to discourage individuals from transferring both their investments and banking business to these new platforms. Additionally, the addition of new services like investing enables community banks and credit unions to attract new customers and members by serving as a single location where they can do both their banking and their investing.

“At InvestiFi, we continue to strive to support financial institutions with cutting-edge, in-house investing solutions,” InvestiFi CEO Kian Sarreshteh said. “Partnering with Bankjoy, a well-respected and trusted platform that supports banks and credit unions, allows us to extend our reach and help more financial institutions across the US, providing them with the tools they need to offer seamless digital investing experiences.”

As CryptoFi, InvestiFi made its Finovate debut at FinovateFall 2022. The company rebranded in 2024 to reflect its growth into a comprehensive self-directed investing suite for credit union members. More recently, InvestiFi has forged partnerships with community-based financial institutions such as West Virginia Central Federal Credit Union ($303 million in assets), Horizon Utah Federal Credit Union ($180 million in assets), Illiana Financial Credit Union ($278 million in assets) and Ocala Community Credit Union ($29 million in assets). InvestiFi also introduced new Chief Product Officer Patrick McNally in August of this year. McNally was formerly Director of Data & Analytics at digital wealth tools provider Exodus Movement.

Founded in 2015 and headquartered in Royal Oak, Michigan, Bankjoy most recently demoed its technology on the Finovate stage at FinovateFall 2023. At the conference, the company showed how its digital banking platform is helping neobank Panacea Financial provide financial services to medical professionals.

Last month, Bankjoy announced that it was expanding its partnership with account activation specialist Pinwheel. A collaboration partner since 2024, Pinwheel has now expanded the number of solutions available on the Bankjoy digital banking platform to include its Switch Kit. This offering combines Pinwheel’s Direct Deposit Switch solution with its Bill Switch feature, unveiled earlier this year, to help solve pain points in the account activation process for consumers.

Splitit launched its Agentic Commerce Partner Program that enables AI agents to offer card-linked installment payment options directly within merchant checkout flows without requiring new lines of credit.

The program is designed to align with emerging standards like Google’s AP2 and OpenAI’s Agentic Commerce Protocol, ensuring interoperability as autonomous shopping ecosystems evolve.

As AI-driven commerce accelerates, Splitit aims to make flexible pay-later options a native part of agent-powered purchases starting with a pilot in the fourth quarter of this year.

Embedded BNPL solutions provider Splititannounced yesterday that it launched a partner program that will allow AI agents to take advantage of pay-later capabilities when making payments on behalf of their users.

Called the Agentic Commerce Partner Program, the new initiative will allow autonomous shopping agents to make payments using card-linked installments. AI agents that have registered with Splitit can request real-time installment options directly within the merchant’s checkout flow. The payments take place on existing payment rails using the users’ existing payment cards, and do not require new lines of credit.

While the agentic commerce landscape is still in its early days of development, Splitit built its Agentic Commerce Partner Program to align with emerging industry frameworks like Google’s AP2 and OpenAI’s Agentic Commerce Protocol to ensure flexibility and interoperability across future agent ecosystems.

“Agentic AI will fundamentally reshape how consumers and businesses buy,” said Splitit CTO Ran Landau. “Splitit’s mission is to ensure that seamless, transparent installments are built into this new paradigm from day one, not bolted on later. We look forward to partnering with leading merchants, platforms, networks, and banks in developing meaningful use cases that can be beneficial to shoppers and brands.”

Splitit’s new feature aims to keep up with the newest evolutions in agent-powered shopping. According to Adobe, 53% of consumers plan to use AI for product research and 40% plan to use AI for purchasing recommendations this holiday season, especially as shoppers are turning to Gen AI for deal-hunting, recommendations, and gift inspiration.

By embedding installment payment functionality directly into agentic commerce flows, Splitit is positioning itself at the cutting edge of autonomous shopping. As agentic ecosystems mature, the integration will allow merchants and platforms to offer more flexible, seamless payment options at the point of decision. Splitit’s Agentic Commerce pilot program will roll out in Q4.