This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

If the future is digital –which it is– then the future must also be in real time. And while our industry typically thinks about real-time in terms of payments, there’s one fintech that’s working to bring information into the real time realm.

Banking technology company Plaid is launching instant account activity today. The new release allows financial institutions on Plaid Exchange to send user-permissioned transactions data to Plaid developers within seconds of the user’s activity. As a result, the consumer receives an up-to-date picture of their finances.

During a time when many consumers are working in the gig economy and budgeting for their expenses on a day-by-day basis, having the most recent information about their account balances is critical and could make the difference between overdrafting or staying afloat.

“Instant, real-time data has become standard for consumers today and it’s a critical piece of information that our users need to make sound financial decisions,” said Atif Siddiqi, CEO of Plaid client, Branch. “Plaid provides our users with the most current picture of their transaction history, empowering their daily financial decisions.”

Today’s development is the latest in a string of updates for Plaid, which recently launchedPlaid Exchange, an open finance solution that offers banks a way to provide open banking connectivity to their clients while keeping their clients’ data safe and giving them control of their data.

Last week, the company announced an addition to its suite of payment products with the launch of standing orders in the U.K. With standing orders, end users can make recurring payments with a single authorization for things like gym memberships and rent payments.

Plaid is an alum of Finovate’s developer conference. In 2014, the company’s CEO and co-founder, Zach Perret, showcased the Plaid API for financial institutions.

Many analysts predicted the latter half of 2020 would be flush with M&A deals. As the economic effects of the pandemic begin to take their toll, some fintechs are more open to exiting earlier than they had planned.

Additionally, volatile stock market conditions are making IPOs less appealing. This may be what swayed Kabbage, which had long-been rumored to IPO after becoming an early fintech unicorn, to agree to be acquired by American Express.

These factors have made August, which is typically a very sleepy month for fintech news, into a busy time for M&A activity. Here’s an aggregation of some of the top deals this month.

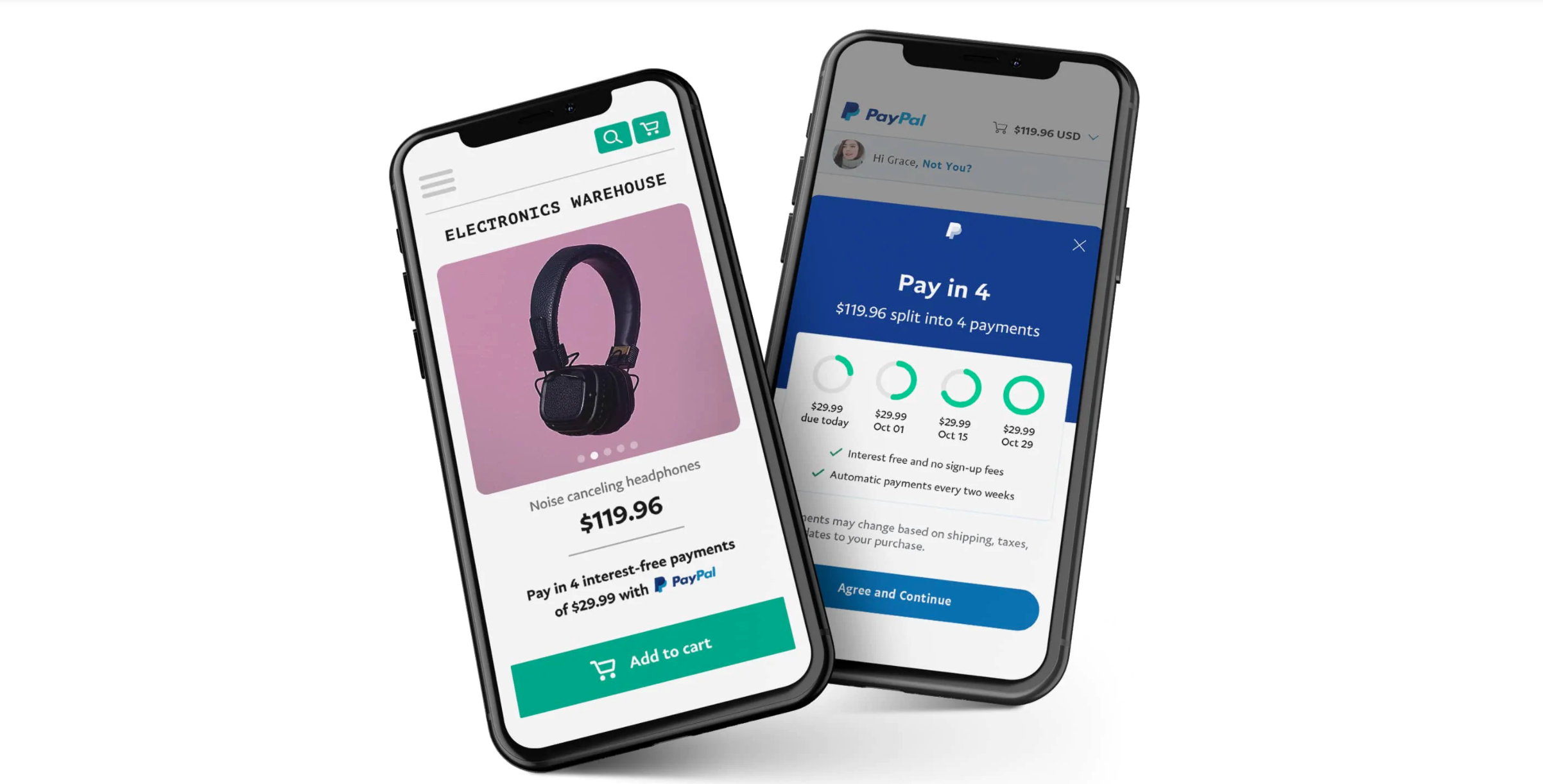

The buy now, pay later (BNPL) trend has been accelerating since the beginning of this year, and today PayPalannounced plans to get in on the action.

The payments giant is releasing Pay in 4, a short-term payments installment product for U.S. customers. When consumers opt to use Pay in 4, merchants receive payment upfront, and the buyer pays for the purchase over the course of a six week period. PayPal takes on the credit risk.

Consumers can use Pay in 4 for transactions between $30 and $600. Purchases do not incur interest and buyers can set up automatic repayments. Additionally, there are no fees for the buyer or the merchant.

“In today’s challenging retail and economic environment, merchants are looking for trusted ways to help drive average order values and conversion, without taking on additional costs. At the same time, consumers are looking for more flexible and responsible ways to pay, especially online,” said Doug Bland, SVP of Global Credit at PayPal. “With Pay in 4, we’re building on our history as the originator in the buy now, pay later space, coupled with PayPal’s trust and ubiquity, to enable a responsible and flexible way for consumers to shop while providing merchants with a tool that helps drive sales, loyalty and customer choice.”

Today’s release is the newest in PayPal’s line of Pay Later tools. The company’s other financing options include PayPal Credit, a line of credit with built-in promotional offers, Easy Payments, a BNPL service available in the U.S. and U.K. PayPal also offers Pay Later tools across the globe in Germany, France, Australia, Canada, Spain, and the Netherlands.

After the BNPL trend began burgeoning earlier this year, PayPal has joined the likes of Affirm, Sezzle, Klarna, and even Goldman Sachs, as well as a handful of others in offering BNPL options to online shoppers. The popularity of these services is attributed to an uptick in unemployment brought on by COVID-19. Not only are consumers making less money, some have maxed out their credit cards and are seeking alternative ways to keep afloat.

Pay in 4 will be available in the 4th quarter of this year.

In a new process called primary direct floor listing, the U.S. Securities and Exchange Commission (SEC) recently implemented a rule that will help companies raise capital through direct listings.

A direct floor listing will enable companies to issue new shares to the public via an auction that matches buy and sell orders, establishing the company’s offering price. This process differs from the traditional direct floor listing method, which was exclusive to existing investors and did not allow the company itself to raise funds via the offering.

The new listing method serves as an alternative to the traditional initial public offering process and eschews formal marketing and shareholder lock-up. Additionally, the new process doesn’t require underwriters to price shares.

“Allowing for multiple pathways for private companies to achieve exchange listing would encourage more companies to participate in public equity markets and provide investors a broader array of attractive investment opportunities,” explained a commenter to the SEC’s rule change.

In some ways, direct floor listings will benefit the company, rather than the shareholders. For example, after going public, first day gains will go to the company itself, rather than new investors.

Minimum market value requirements for direct floor listings, which are imposed to ensure sufficient liquidity, are $100 million and, for primary direct floor listings, $250 million. This is more than double the minimum value requirement for IPOs, which is $40 million.

According to the Financial Times, two technology companies have already expressed a desire to take advantage of direct listings. Both Palantir and Asana have filed paperwork with the SEC for direct listings.

Ever wonder what your favorite fintech CEO’s first job was? Or if they would rather invest in gold or bitcoin? Or what their best Halloween costume was?

While those are questions may have come up during a casual networking session, face-to-face (or mask-to-mask) networking isn’t possible this year, so it may be difficult to have such casual banter. Fortunately, I have two pieces of good news for you.

First, FinovateFall Digital, taking place September 14 through 18, is offering as much quality networking time as possible during the event. We’re offering lots of ways to communicate with your fellow audience members. And if you’re not a social butterfly (or if you prefer PJs over a polo shirt), you can make your opinion heard through polls or communicate via chat.

The second piece of good news: we’ve started a video series called 25 in 5 where we ask 25 questions to demo companies and they answer them all within 5 minutes. It is not only a great way to get to know the company, but also serves as an introduction to a CEO and the culture they’ve built.

Interviewing Glance CEO Tom Martin

All of the 25 Questions interview videos will be available as exclusive, on-demand content within the FinovateFall Digital event platform. If you’re registered, keep an eye out for early access to schedule meetings and curate your event-day agenda with the sessions that most interest you.

And don’t worry about missing out. There’s still time to register, and with no need to buy a plane ticket and book a hotel room, FinovateFall is more accessible than ever.

The health crisis and economic environment have shaken up the fintech industry. Some of the trends we saw at last year’s event have been placed on the back burner because firms are not only cutting costs but also are enhancing their focus on serving customers in a new way.

So while this year’s FinovateFall trends assessment isn’t a completely new set of ideas, it certainly doesn’t mirror our forecast from the beginning of the year. As you may have guessed, every trend at this year’s conference will be filtered through a COVID-19 lens.

Here is what you can expect to see:

Digital

By the end of 2020, every product and service must be accessible online. A solid digital customer experience has become table stakes. Because of this, at this year’s show, you can expect to hear the term “digital transformation” in every session.

AI

There’s something almost comforting about seeing AI as a top trend once again this year. While much of the world, the economy, and our working environments have changed, AI still brings technological advancements to every sub-sector in fintech. And since most services must take place 100% digitally, companies need every improvement possible to maintain superior customer service.

Remote

Again, since most of our interactions must take place remotely, we have to re-think and re-invent many of the ways we used to do business. Everything from internal communication and collaboration to customer authentication to payments must now incorporate remote-friendly practices.

Fighting fast-tracked financial crime

While security technology was already a hot topic in the pre-COVID environment, it is even more so now. Now that many employees are working from home, hackers have taken advantage of wifi networks with weak security standards. Aggravating the situation, hackers have implemented new phishing attacks that prey on human emotion to gather sensitive information.

Customer experience

Like AI, this is another trend that the industry had on its radar in 2019. It has now, however, been heightened by the onset of the public health crisis. Now that consumers of all ages are accessing products and services remotely, financial services companies have had to not only fast-track digital transformation efforts but also create new initiatives to serve customers that are not digital natives.

Banking-as-a-service

The “as-a-service” trend has been around essentially since the dawn of fintech. However, the offerings are starting to mature now with the onset of open banking; the increased flexibility; and mutual benefits across banks, third parties, and end customers.

Challenger banks

Because challenger banks were born in the digital realm, they were practically made to serve customers during a pandemic. In addition to their digital expertise, many of them offer products and services for consumers facing economic uncertainty. And investors have taken notice, challenger banks have been some of the top recipients of VC funds in 2020.

Communication

Because most people are dealing with the realities of a remote working environment and living situations, communication is extra challenging right now. Along with technologies that enable face-to-face conversations via video, many financial services companies are taking a second look at chatbots, their phone-based customer service, and other channels. In the end, we will not see a single communication channel come out on top as the winning one. Instead, we’ll see multiple winners as different consumer groups find the channel that suits their preferences.

Marketing services company Kasasa is partnering with BSI Financial Services to provide a new mortgage loan product that community banks and credit unions can offer their clients.

The new offering, Kasasa Mortgage, helps small financial institutions compete with large banks by offering a unique loan product. What’s distinctive about Kasasa Mortgage is that it uses the Take-Back concept the company piloted in 2018. Every month the borrower has the option to overpay on their mortgage payment. If, at any time in the future, they need to access cash quickly, they have the option to take back any portion of the overpayment.

Making the new launch possible, BSI Financial will conduct the loan servicing on behalf of community banks and credit unions using the new product, Kasasa Mortgage.

“Through Kasasa’s partnership with BSI Financial, we are enabling a greater number of local financial institutions to help their borrowers better understand their mortgage loan and get out of debt quicker,” said Kasasa’s EVP of Product Management, Chris Cohen. “By offering the most consumer-friendly loan available today, community banks and credit unions can achieve higher yields without the additional risk and maintain their fair share of the market.”

Earlier this month Kasasa improved on its Take Back loan by integrating Carleton’s insurance and debt protection calculations to help tailor loan limits.

Customer engagement specialist Digital Onboardingannounced its Series A round today. The amount of funding was undisclosed and adds to the company’s existing $4.3 million in seed funds. Contributors include Detroit Venture Partners and other institutional and individual investors.

Along with today’s investment, FINTOP Capital Partner John Philpott, Jack Henry Senior Managing Director Shawn Ward, and a founding member of S1 Corporation joined the Board of Directors.

The company plans to use the funds, along with the fresh influx of expertise on its board, to begin “accelerating the execution of [its] product roadmap, scaling account management, and expanding sales.”

Digital Onboarding’s SaaS offering helps banks deliver compelling services that keep customers around for the long-term. The company is especially effective in helping motivate accountholders to take action because it aggregates data across banks with similar business objectives.

“Banks have myopically focused on getting new accounts opened to meet aggressive sales targets and are now being forced to contend with the reality that new accounts are worthless if they’re not converted into engaged relationships,” said Digital Onboarding CEO Ted Brown. “The Digital Onboarding platform has been proven to drive the adoption of additional products and services like digital banking, direct deposit, and automatic payments which drive long-term profitability.”

The funding comes at a time of increased demand for digital services of all kinds. Since many non-digital native customers are now needing to conduct much of their banking activities remotely, maintaining connection with them through digital channels is more essential than ever.

Digital Onboarding was founded in 2015 and is partnered with 40+ financial institutions that together represent $160+ billion in assets. The company most recently demoed at FinovateFall 2018. You can catch an all-new round of demos at FinovateFall Digital next month. Stream the event from anywhere on the globe September 14 through September 18.

The following is sponsored content from LendingFront.

With Covid-19 on the minds of businesses and lenders alike, conversations about the capital needs of small businesses have revolved—with obvious justification—around the Paycheck Protection Program (PPP) and other forms of relief provided under the CARES Act.

Yet the capital needs of many small businesses don’t begin and end with the PPP.

Let’s start with a few facts

According to the U.S. Federal Reserve’s 2019 Small Business Credit Survey:

43% of small businesses sought external funding for their businesses in 2018

And more than half experienced a funding shortfall.

These funds—when small businesses can obtain them—are often used to purchase inventory, replace equipment, finance expansion, and hire new workers.

These needs will persist long after PPP lending has come to an end, yet even in a strong economy, up to 80% of bank-originated small business loan applications are rejected.

In the post Covid-19 environment, we can expect that percentage to be even higher

That’s because the conventional underwriting criteria for small business loans will no longer work. Traditionally, both bank- and non-bank lenders have relied on four criteria for underwriting small business loans:

Tax/Financial Statements

Credit Scores

Collateral

Owner Wealth

In a normal economy, these criteria are fine, but they’ll do little to show the true state of a business in the post Covid-19 environment. 2019’s tax/financial statements will be all but irrelevant. Credit scores will be damaged as a result of the inability to make payments during a forced closure. Collateral will have questionable value if bankruptcies spike. And owner wealth will have been tapped in an effort to keep many businesses afloat.

Are we headed towards a capital drought?

With traditional underwriting criteria no longer useful, are we headed toward a capital drought? We certainly don’t need to, but the answer largely hinges upon lenders doing two things:

Adopting new criteria that are more appropriate for the post Covid-19 environment

Adopting new product structures that enable the lender to manage risk

New credit criteria include information such as:

Real-time Cash Flow Cash flow helps you gauge how quickly the business is recovering from Covid-19. Is it in irreversible decline? Is it struggling but stable? Has it gotten back to normal? Insight into real-time cash flow helps lenders make better decisions about who to lend to along with the terms of any offers.

Consumer Sentiment Customers who vote with their reviews also vote with their wallets. Examine reviews from Google, Yelp, and other sources to answer, Is this a business that customers love? Businesses that are well-regarded by customers stand a much better chance of recovering than those that had problems before the pandemic shut them down.

New product structures also enable lenders to deliver capital efficiently while managing risk

Here’s how:

Shorter Terms First, lenders should emphasize shorter payback periods in the range of 6-12 months. Shorter terms get the lender paid back faster while enabling the business owner to show that he/she is creditworthy before seeking a larger amount of capital.

Daily ACH Payments Second, lenders should collect payments from the borrower on a daily—rather than monthly—basis. Monthly payments introduce unnecessary operational risk. Daily payments are smaller, consistent, and more predictable from the standpoint of the business’ cash flow.

Tie Payments to Performance Lastly, lenders should tie payment terms to current cash flow performance—and with visibility into cash flow, this is very easy to do.

A new economy needs new rules for lending

If the Great Recession taught us anything, it’s that opportunities exist for lenders to increase their assets, gain market share and, of course, to meet the capital needs of their borrowers. In the post Covid-19 environment, lending is only as risky as the information used to make decisions. With better underwriting criteria and more appropriate product structures, the most forward-thinking lenders will position themselves for success and reap the rewards.

Tandem Bank announced its latest acquisition this week. The U.K.-based bank has purchased Allium Money, an alternative lender that offers consumers financing to improve the energy efficiency of their homes.

Specific terms of the deal were not disclosed, but it is made possible by Tandem’s $78 million (£60 million) funding round that was led by Qatar Investment Authority and closed last week.

Tandem Bank will use Allium to enhance its existing in-house lending suite, tapping into Allium’s green lending solutions that help homeowners finance everything from insulation to efficient windows to solar panels.

“This is great news for our customers and the team that have worked tirelessly to develop the business focussing on financing improvements for our environment,” said Allium CEO Paul Noble. “The combination of Allium and Tandem will create the ability to rapidly scale a green banking proposition and help more customers access green finance products.” Noble will join Tandem’s executive team.

The partnership comes at a good time. With an increased focus on climate change and awareness of their impact on the environment, consumers have shown heightened interest in green initiatives. Along with home improvements, ESG (environmental, social, and governance) investing is also gaining interest.

Tandem Bank has raised $175 million (£134.3 million) since it was founded in 2013. The challenger bank’s 700,000 customers have access to Tandem’s accounts that include Autosavings technology, credit card, and, coming soon, cashback rewards.

This is a guest post by Sandeep Sood, CEO of Kunai.

Will Digital Behavior Affect Credit Scores in the Future?

Credit scores are about to take another leap forward—or backward, depending on how you see the future. People’s digital lives leave a trail of data “exhaust” that some countries are beginning to leverage to understand and better predict their behavior.

Assessing someone’s credit risk without traditional financial information is tricky business. Inevitably, concerns about privacy and credit-based blacklists arise.

For as long as there is debt, there will be debate about the subjective measures that determine who can be trusted to repay it. To understand how we got here and where we’re going, we’ll need to review the history of credit scoring as we know it.

Where Did the FICO Score Come From?

Formal credit reporting began in the U.S. in 1841. Ledgers in New York recorded borrowers’ creditworthiness, however these reports were extremely biased. Entries included advice such as “prudence in large transactions with all Jews should be used.” A more fact-based, alphanumeric system was developed in 1857 and used well into the 1900s.

Starting in the 1950s, computerized credit ratings used algorithms to automate scoring. FICO was born, and made rapid lending approvals possible.

In a world with Facebook and Google, it’s hard to think of an algorithm that has a greater effect on our day-to-day lives. It dictates the jobs we get and the places we can live. Yet, the algorithm is cryptic and occasionally biased, even if it works most of the time. FICO is far from perfect, but it’s the best system we’ve got—for now.

Alternative Scoring Methods Help Bankless Borrowers, at a Cost

Around the world, many people don’t engage in the banking and credit card transactions that feed the FICO algorithm. This has led to explorations of other credit scoring methods.

Fast-growing startup Tala, for example, is using the ubiquity of cell phones to bring credit scoring to unbanked borrowers. Applicants surrender their mobile data, and Tala monitors bill payment history, text messages, and behavioral data gleaned from their device to provide a unique “mobile credit score”.

For people who need loans, giving up personal information is worth the sacrifice. Tala arose out of the need for better information in countries without established credit systems, making credit available to people who otherwise would not have access to it.

China’s Social Credit and the Big Brother Debate

In parts of China, credit is returning to a reputation-based model. Various local programs measure social credit based on behavior. Some of this is tracked online, similar to Tala’s methods, but facial recognition and CCTV networks are also leveraged to ding people’s scores. Littering, failing to cede right of way to pedestrians while driving, and other actions deemed socially harmful can affect someone’s score.

While these pilot programs feel Orwellian, the Chinese system remains in a nascent stage of development. Perhaps one day soon, the West’s fears of Chinese social control will be justified. And then the question is, how will the rest of the world respond?

The Future of Credit Scoring

The credit score is a fundamental pillar of our modern financial system. But it’s difficult to define a universal set of attributes to determine every American’s credit risk.

Cryptocurrency may offer a viable solution. Finance startup Bloom is already leveraging the recorded financial history available on the blockchain. Since all transactions are permanently stored in a public record, cryptocurrency provides an immutable source of truth. While there is no history on the blockchain yet, it could be a game-changer once developed.

But data and its surrender aren’t going to suddenly change a system that’s been, more or less, working since the 1950s. In fact, too much data can lead to bad models that over-index for characteristics that work well in one population but do just the opposite for another.

As these experiments continue, they’ll likely bring a more stable, accessible credit system to countries in the wild west of credit scoring. In five to ten years, their successes and failures may very well lead to breakthroughs that influence how FICO evolves. But for now, FICO is proving it works well enough without the glut of invasive personal data.

Sandeep Sood is the CEO of Kunai, a product development company that has been building digital products for 20 years. See more of his articles at Kunaico.com along with Kunai’s work. Follow him on Twitter @sandeep_k_sood.

Starting this week, NatWest is making it easier for clients to get the help they need to make their banking experience easier. The initiative is called Banking My Way and provides a single place for customers of the U.K.-based bank to input their preferences so that they are addressed across all channels.

The preferences are divided into two sections, About me, which addresses vulnerabilities or disabilities such as being visually or hearing impaired, and Support me, which focuses on how the bank can support the user, such as speaking slowly and clearly or not assuming a gender when addressing them.

“Banking My Way will allow you to tell us more about your current circumstances and the difficulties that you are facing with your banking,” NatWest explained on its website. “This will allow you to also tell us about the support you require, and we will ensure that this information is shared with our teams to support any further interactions that you have with us.”

Clients can input or change preferences online, in a branch, or via phone. In order to ensure information is up-to-date, users will be asked to review their preferences on an annual basis.

This is an amazingly simple idea, but because it is a pull, rather than a push approach, it may be lost on some consumers. That said, NatWest will have the best response rates with this system if it is implemented as part of the onboarding process, instead of being structured as a separate item customers need to register for.