This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

In a series G round, buy-now, pay-later company (BNPL) Affirm brought in $500 million, bringing the company’s total raised to $1.3 billion.

Leading the round were Durable Capital Partners LP and existing investor GIC. Other returning investors Lightspeed Venture Partners, Wellington Management Company, Baillie Gifford, Spark Capital, Founders Fund, and Fidelity Management & Research Company LLC also contributed.

Affirm Founder and CEO Max Levchin referred to the new round as a “vote of confidence” that will help the company advance its mission “to build honest financial products that improve lives.”

Along with the funding announcement, Affirm also unveiled an interest-free and fee-free bi-weekly payment product for transactions over $50. The new product aims to help Affirm’s tools compete with credit cards. “Affirm is now an even more attractive payment option for everyday wants and needs,” Levchin added. “We can also now better support merchants who offer smaller ticket items and bring their customers a more transparent, flexible way to pay.”

Affirm’s BNPL tools reach 6.5 million shoppers across the U.S. and Canada. The company has 6,000+ merchant partners in the U.S., including brands such as Walmart, Peloton, Oscar de la Renta, Audi, and Expedia.

Affirm’s funding comes days after Klarnaunveiled its $650 million raise, which brought its total funding to $1.4 billion and boosted its valuation to $10.6 billion.

Partnerships between nimble fintechs and trusted banks are essential as we look to build back our economy. Mary Kate Loftus, a panelist in our FinovateFall Strategic Partnerships session, knows this well. As head SVP, Director of Digital for M&T Bank, she fields potential partnerships each month. We sat down with her to discuss what M&T looks for in a partner and where she sees the industry going.

How do you determine your needs for a fintech partner?

Mary Kate Loftus: With all things, we start with our customer. Our teams dive deep into the customer experience through journey mapping, and from this, we can see the pain points and what we need to create. Going about our innovation and partnerships from this perspective, rather than looking at our competitors and building to parity, allows us to create a truly differentiated experience.

When it comes to partnerships, we consider if we are best suited to meet the needs of the client or if we need to turn to an outside source that’s already focusing on these needs very deeply. Banks, like M&T, are able to work closely with their clients in a way that many fintech organizations are not able to do. But often fintechs, free of a complex organizational structure or process, are able to innovate in a very focused way. This ying and yang – the bank’s customer expertise and the fintech’s area expertise – allows for a truly meaningful partnership.

Once we identify a partnership need, we see if we’re aligned in our corporate purpose. This step is critical – it ensures that our approach will be both effective and long-term. Our purpose is to improve the lives of our customers in a meaningful way, and we look for partners looking to achieve the same.

What makes you take a meeting with a potential fintech partner?

Mary Kate: Referrals from existing clients, friends, connections, or colleagues are always a great way to start a potential partnership. Beyond that, I get excited to meet those who come with a clear vision of the problem they’re able to address and a strong understanding of our corporate promise. For us, it’s not enough to simply have a capability, but rather, we build for measurable results and long-term partnership.

Once we’re in the meeting, it all comes down to talent. We want to work with creative, imaginative, curious people, and we’re looking to see those qualities on day one. Together we want there to be a good energy in the room and, equally as important, great ideas.

Lastly, we’re looking to learn from our partners. What can you teach us about what we’re not yet doing?

Can you discuss the PPP rollout and how you overcame the challenge?

Mary Kate: M&T’s successful PPP rollout was thanks to a strong set of existing partnerships and a creative team that was ready to scale nearly overnight.

Before the pandemic, we were working with Blend for our mortgage digital originations so we were already aligned in our purpose. The leadership teams from both organizations were just starting conversations on how we could work together more when the PPP program was announced, and so we knew they were the partner to tap. A cross-functional team brought in Salesforce and Docusign – two other existing partners – to complete the experience.

Within minutes of the program launching, we had thousands of applications. Together, we were able to lead the country in loan fulfillment– 96% of first round loans went through within days — giving $7 billion in funds to small businesses. More importantly, our partnership allowed us to still meaningfully vet the applications, and we’re proud to say that two thirds of the loans issued went to businesses with less than 10 employees.

Our PPP response was led by Eric Feldstein, M&T’s SVP who oversees Business Banking. It’s a success story about the importance of having strong leaders with digital expertise leading a line of business. I believe this successful rollout in a time of real crisis for many will create lasting loyalty in our customer base.

What near-horizon banking technology are you most excited about?

Mary Kate: I’m a big believer in the science behind behavioral analytics and how you motivate customers by understanding how people think.

Every customer is going through a different experience. If one client is going through a life change like having a child or going through a divorce, it’s important to be able to anticipate financially what that journey might look like for them. As we are able to embed more artificial intelligence and meaningful insights, we’ll be able to guide customers toward better decisions that then will improve the quality of their life.

This is why we’re so focused on experience mapping to identify customer journeys — from there we’re able to understand what the moments that matter most are for different segments of customers. When you apply data and insights against those experiences, you’re then able to build a personalized micro-experience. What we’re doing today is lightyears ahead of what we were doing in the past, and I can’t wait to see how much more we can do in this space.

The pandemic is only going to accelerate this. We’re seeing a blend of work and personal lives, and with this, I think the financial services industry will play an even bigger role in making a difference in people’s lives.

What role does the need for diversity play in banking partnerships?

Mary Kate: Diversity plays an absolutely critical role in these partnerships.

At M&T, we know the more diverse voices we have in the room the better decisions and outcomes you can drive for customers. As an institution, you must reflect your community and customers, so you need to draw from a broad range of experiences in order to drive the best business performance and outcome.

When choosing a partner, we look at who we’re working with. We look at what systems are in place and watch out for those that could create outcomes that we don’t want to drive, and, conversely, for those that will drive us further.

This goes back to what I was saying earlier about learning from a partner. Yes, we want cutting-edge technology that will solve customer pain points, but sometimes these pain points are solved through systems, processes, or approaches. We’ve found that by working with a diverse set of partners, we’re able to think in more comprehensive, customer-centric ways.

Mary Kate Loftus is the Senior Vice President, Director of Digital for M&T. She joined the Bank in 2018 as the Head of Strategic Planning for the Consumer & Business Bank. Mary Kate is a career banker with over 20 years in financial services with experience in Digital, Branch Management and Contact Center. Mary Kate holds an MBA from Canisius College, is a 2013 graduate of the Consumer Banker’s Association Executive Banking School and is a member of their Digital Channels Committee in addition to other industry forums

Secure messaging company Striataannounced this week it has been acquired by Doxim, a customer communications management (CCM) software company. Terms of the deal were not disclosed.

Doxim will use Striata’s technology to expand its CCM platform and provide personalized digital interactive experiences in a secure manner. Doxim CEO Mike Rogalski expressed that the global pandemic has accelerated the need for communications technologies. “Especially with the impact of COVID-19, which has meant fewer face-to-face meetings,” noted Rogalski, “organizations need to find scalable ways to orchestrate and distribute multi-channel communications that are both personalized and legally compliant.”

“The joint strength of Striata and Doxim will power a world-class digital CCM platform and expert team for enterprises and small to mid-sized businesses,” said Striata CEO Michael Wright (pictured). “We look forward to working with Doxim to integrate our technology, systems and culture. The value proposition of the combined organization promises to be a formidable force in the market.”

Striata was founded in 1999 and, with a focus on security and compliance, has worked heavily in the financial services industry. The company’s services include message design, generation, security, delivery, and storage across multiple channels.

Striata is headquartered in New York City, with operations in London, Johannesburg, Hong Kong, and Sydney and partners in North and South America, Africa, Europe and Asia Pacific.

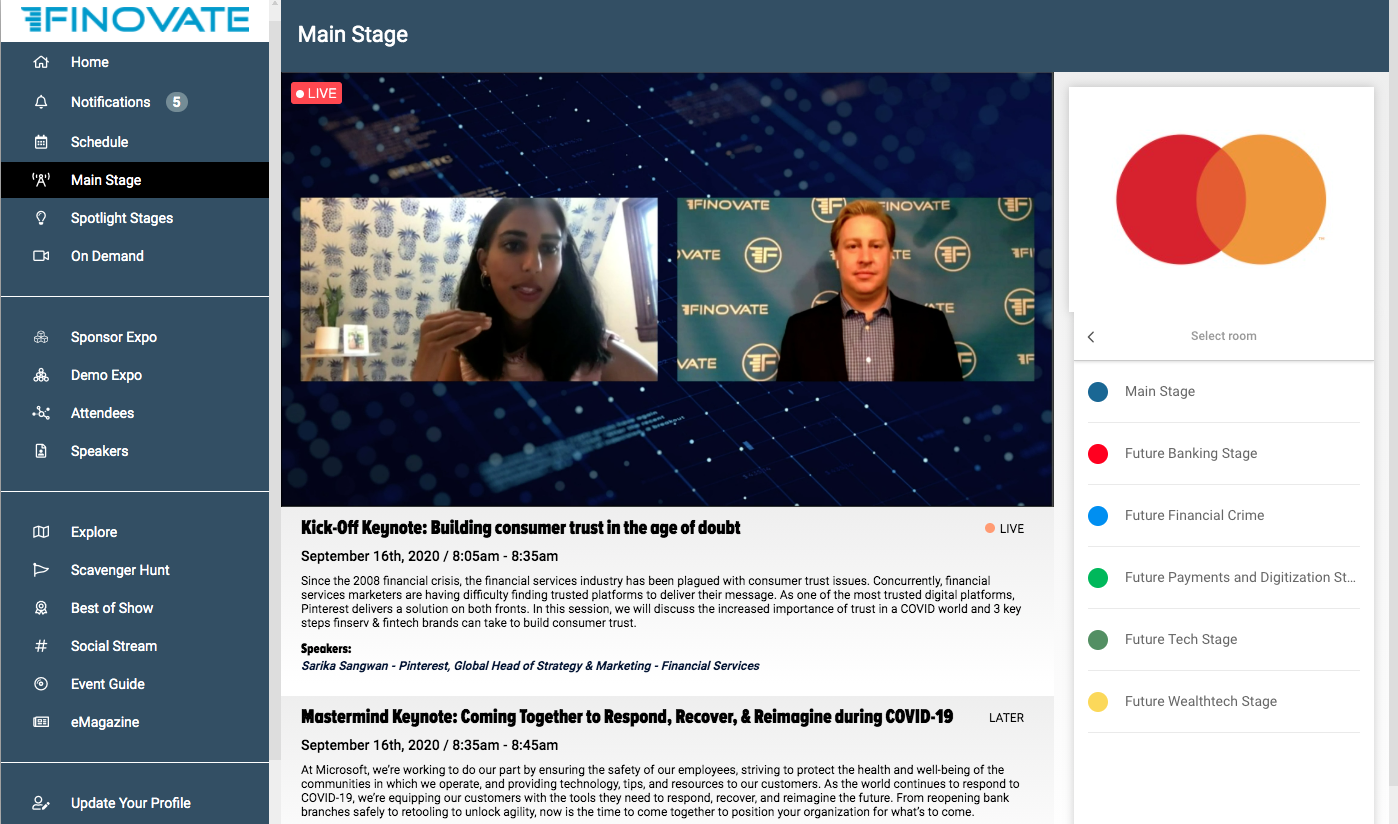

Finovate came back strong this morning, with excellent keynotes and a solid round of fintech demos.

Sarika Sangwan, Global Head of Strategy and Marketing- Financial Services at Pinterest kicked things off with her keynote on building consumer trust in the age of doubt. She illustrated that the best way to build trust is with intentionality and purpose. Sangwan encouraged banks to put the customer first and allow that to drive every decision they make.

The next keynote of the morning featured Tom Feher, Banking Industry Executive of U.S. Financial Services at Microsoft, who spoke on coming together to respond, recover, and reimagine during COVID-19. Feher showcased a range of solutions to help firms return to in-person operations in the midst of the pandemic. He pointed out that low code and no code solutions can not only help organizations respond to issues faster, but also reduce costs.

Today’s final keynote speaker was Paul Rohan, Head of Business Strategy- Finance at Google Cloud on how open banking is 21st century branch banking. Rohan’s discussion combined technology, sociology, and history to consider how banks can change their belief systems (as well as their computer systems) to move into a more open approach that embraces third parties.

Following this was the last set of demos:

Authoriti showcased the Authoriti Network that helps create new ways of preventing identity theft, fraud, and misuse of data.

Cirrus Secure demoed its cloud-based collaboration hub that impacts a lender’s bottom-line by creating efficiency in place of document chaos.

KioWare presented its touchless kiosk environment that enables kiosks to be converted to touchless operation without expensive new hardware.

Cinchy showed off its real-time Data Collaboration Platform that helps financial service providers solve data integration, data access, data governance, and solutions-delivery challenges.

Lenderfit demoed how it helps lenders close more commercial loans faster.

Glia showcased its digital customer service platform that connects financial institutions to their customers using chat, voice, video, cobrowsing and AI.

Illuma Labs demoed passive voice authentication for call centers to help banks elevate the user experience, enhance security against fraudsters, and improve operational efficiency.

Envestnet |Yodlee presented its data aggregation and analytics platform that provides innovation and insights for financial service providers.

Microsoft showcased tools to help firms protect their workforce during each phase of the return to the workplace — and beyond.

Horizn demoed how it helps financial institutions dramatically accelerate digital adoption with customers and employees.

Wrapping up today’s show were the Mastercard Priceless Pitches, three-minute pitches from Mastercard’s Start Path participants, including:

Previse showed how it leverages AI to power B2B payments and make B2B commerce more efficient.

Doconomy presented how it helps consumers calculate the carbon footprint of every transaction they make and offset and reduce their carbon footprint.

Enveil showed how it protects data-in-use to enable secure and private data sharing, search, and analytics.

vCita presented how it powers small business by offering them tools to manage their money, time, and clients to grow their business.

Tomorrow we’ll kick off our discussion days with another conversation at our interactive networking session, Meet at the Cafe. Afterwards we’ll feature insightful keynote presentations and breakout panels. Stay tuned!

Since its launch in 2009, Square has always catered to small business owners. The payment services company is best known for offering micro-to-medium sized merchants an easy way to accept payments and today Square is launching two services to make those business’ payrolls even more robust.

Explaining the problem, Square Payroll GM Caroline Hollis said, “The traditional payroll process is slow and rigid, creating cash flow constraints for employees and businesses alike. This is even more pronounced now given the current economic conditions.”

The new features include On-Demand Pay for employees and Instant Payments for employers. On-Demand Pay will allow employers to offer their workers early access to some of the wages they’ve earned, while Instant Payments helps businesses fund payroll faster than the typical time of three-to-four days.

There is a bit of a catch with these services, however. Both offerings hinge on Square’s Cash App, a mobile wallet that effectively serves as a checking account for P2P payments. With On-Demand Pay, employees can transfer up to $200 of their earned wages to Square’s Cash App for free. Transfering the funds to a third party debit card, however, incurs a 1% or $2 fee. As for Instant Payments, employees that elect to be paid via Square’s Cash App receive their pay within minutes, while those paid via direct deposit get paid “as soon as the next business day.”

The new features are not new to the fintech scene. They will, however, help Square compete with new offerings from other third party fintechs and serve as a way to help Square maintain its multi-million user base of sellers.

As the buy-now, pay-later (BNPL) craze explodes, some fintechs are in just the right place to catch the sparks. Payment services company Klarna is one of these players, and it has just landed $650 million in funding.

Today’s round adds to the company’s $1.4 billion in previously raised funds, bringing its total to just over $2 billion. The investment also boosts Klarna’s valuation to $10.6 billion, ranking the company as the highest-valued private fintech in Europe and the fourth highest worldwide.

The round was led by Silver Lake, GIC (Singapore’s sovereign wealth fund), and accounts managed by BlackRock and HMI Capital. Additional funds came from Merian Chrysalis, TCV, Northzone, and Bonnier, which have acquired shares from existing shareholders.

Klarna will use the funds to invest in product development, fuel global expansion, and build on its growth.

“We are at a true inflection point in both retail and finance,” said Klarna CEO and Co-founder Sebastian Siemiatkowski. “The shift to online retail is now truly supercharged and there is a very tangible change in the behavior of consumers who are now actively seeking services which offer convenience, flexibility and control in how they pay and an overall superior shopping experience. Klarna’s unique proposition, consumer preference and global retailer network will prove an excellent platform for further growth.”

As consumers seek alternative methods to finance their purchases, Klarna’s BNPL tool that enables users to pay in interest-free installments has gained impressive traction. The company’s shopping app has more than 12 million monthly active users worldwide, with 55,000 daily downloads.

And Klarna’s game is also strong on the merchant side of things, as many retailers have sought to increase online sales during stay-at-home orders. During the first half of 2020, the company added more than 35,000 new retailers to its existing merchant base of more than 200,000 partners including Sephora, The North Face, Timberland, and Ralph Lauren.

As a result of this growth, the company’s volume grew 44% over the first half of this year to more than $22 billion and its revenue increased 36% year-on-year to $466 million over the same period.

We were welcomed to the first day of FinovateFall 2020 by a familiar face: Finovate VP Greg Palmer. Greg kicked things off with a discussion of the importance of digital offerings, noting the increased accessibility to all.

The opening keynote was from Pablos Holman of Intellectual Ventures Lab who issued the friendly reminder that “nobody has ever invented a new technology by reading the directions.” Holman encouraged the audience to find real problems in the world and start innovating where there is a true need. He pointed out two keys to success in this type of innovation: first, form fintech-bank partnerships to give ideas the traction they need; second, run a lot of experiments by trying a handful of things to determine what works the best.

During his Mastermind keynote, Scott Gnau, VP of Data Platforms at InterSystems encouraged the audience to leverage the inflection point that is COVID-19 to focus on digital transformation and build technology that is resilient to change in the future. Part of the key to this, he explained, is to leverage partnerships but maintain ownership of your own data to remain agile.

After a round of virtual meet-ups and networking sessions, the demos began:

Yext kicked things off by showing how it can improve the search experience on company websites and across the entire search ecosystem.

Scientia Consulting presented FinTechInsights, a tool that analyzes digital banking competition in realtime behind their login screens.

Finzly showed its open banking platform, Finzly BankOS.

Lendsmart demoed its AI driven platform that solves for the lack of automation, transparency, and communication in the lending process.

Glance Networks presented its solution for transforming in-branch financial consultations into digital meetings.

NachademoedPhixius, a tool that enables the secure exchange of payment-related information via open APIs within a trusted network.

Icon Savings Plan showcased its portable, universally accessible, workplace retirement savings plan that serves as an alternative to the 401k.

Remitter presented its AI-powered, white-labeled digital communications platform that helps lenders maximize revenue by optimizing customer engagement.

XcooBee demoed its payment workflow automation tools that combine self-checkouts and remote pay to help reduce retail touch-points and boost transactions.

Today we’re announcing the winners of the 2020 Finovate Awards, recognizing excellence in fintech across 23 different categories. This is the second year of the Finovate Awards, which aims to highlight strong work done by the companies who are driving fintech innovation forward and the individuals who are bringing new ideas to life.

This year’s Finovate Awards may not come with ballroom gowns, confetti, and cocktails, but that doesn’t make the accomplishments any less compelling. In fact, the opposite is true. To be receive an award in the midst of a global pandemic-turned-economic crisis is often the result of putting the needs of others first.

Judges for the awards include media analysts, board members, bankers, fintech founders, and more. Each were given the difficult task of taking a record number of nominations and distilling them down to just a single winner in each category.

Best Alternative Investment Platform: CNote

Best Back Office / Core-Service Provider: MAXEX

Best Consumer Lending Platform: NF Innova and Raiffeisen Bank Serbia

Best Customer Experience: Commonwealth Bank of Australia

Best Digital Bank: STASH

Best Digital Mortgage Platform: LendingHome

Best Enterprise Payments Solution: PaymentGalaxy by Finzly

Best Financial Mobile App: TMRW by United Overseas Bank

Best Fintech Accelerator / Incubator: The Venture Center’s FIS and ICBA Accelerators

Best Fintech Partnership: PPP.bank (Citizens Bank of Edmond and Teslar Software)

Best ID Management Solution: buguroo

Best Insurtech Solution: Spire by Ernst & Young

Best Mobile Payments Solution: Nordic API Gateway

Best RegTech Solution: Facteus

Best SMB/SME Banking Solution: ANNA Money

Best Use of AI/ML: Socure

Best Wealth Management Solution: SoFi Invest

Excellence in Financial Inclusion: Current

Excellence in Sustainability: PayActiv

Executive of the Year: Renaud Laplanche, Upgrade

Fintech Woman of the Year: Lisa Kimball, Finicity

Innovator of the Year: Elena Ionenko, Turnkey Lender

Top Emerging Tech Company: Breach Clarity

While only one company can win each category, it’s also worth recognizing the quality of all of the finalists who made it to the last stage in the process.

We owe a huge thank you to the panel of judges, followers, and everyone who took the time to submit a nomination. Congratulations to the winners!

ABN AMRO is updating its Grip app this week by integrating Subaio’s white label subscription management feature for banks.

The integration comes at a time when users are spending more than ever before on subscriptions, especially digital subscriptions such as movie streaming services and cloud storage products. According to the New York Times, consumers spent an average of $640 on digital subscriptions in 2019, up 7% from 2017.

ABN AMRO’s Grip PFM app now leverages Subaio’s subscription management feature that enables users see all of their recurring payments in one place. The tool alerts users of any changes in subscriptions and even helps them cancel subscriptions from within the app. Subaio relies on an algorithm that uses machine learning to detect patterns in frequency, amount, merchant name, and more.

“Since the launch we’ve already seen tens of thousands of Grip users coming in to see their overview and also cancel subscriptions. It’s fantastic to help people get control of their subscriptions,” said Subaio CEO Thomas Laursen.

Today’s partnership with ABN AMRO is Subaio’s seventh bank partnership. Among the company’s other partners are Nordea and challenger bank Lunar. The company has found that the average user has eight different subscriptions, and that the users are saving $253 (€213) every time they use Subaio’s solution to cancel a subscription.

Founded in 2016, Subaio showcased at FinovateEurope 2020. The company has raised $2.4 million and has 20 employees.

You know that buy now, pay later (BNPL) has jumped the shark when even Cosmo is writing about it. After all, BNPL is basically millennials’ way of reverse engineering the layaway programs their parents grew up on.

Not only have we recently witnessed new fintechs launch their buy now, pay later technology, we’re seeing a large increase in incumbent players expand their existing services to include BNPL offerings, as well. Just yesterday, Fiservannounced its BNPL payment option in partnership with QuadPay, and today Standard Charteredpartnered with Amazon to offer installment payment plans for customers in the UAE.

While each of the now dozens of BNPL schemes operate a bit differently, most allow the consumer to split up a purchase into multiple installments and repay over a set period of time without incurring interest. As with everything that seems too good to be true, however, negative externalities exist. Here’s a breakdown of the hidden (and not-so-hidden) costs:

The BNPL company

If a consumer makes a purchase and fails to pay one or more of the installments, the BNPL company is generally the one who feels the loss. To mitigate their losses, however, companies generally won’t allow customers to make repeat purchases if they default on a repayment. Not only this, most charge late fees and high interest (some charge up to 30%) to reclaim what they can.

The consumer

The end consumer is always responsible for knowing the repayment arrangement. However, mistakes happen and if the buyer is unable (or forgets) to pay one of the installments, they face multiple costly consequences. As mentioned above, the consumer in default generally faces a late fee. Klarna, for example, charges $35 per month for missed payments. Additionally, while most BNPL offerings are interest-free, some charge high interest on missed payments.

Merchants

Merchants have a pretty good end of the deal when it comes to BNPL. Many offerings allow them to receive the full amount of the buyer’s purchase up-front, and they are not on the hook if the buyer defaults. Some, such as Splitit, allow the merchant to choose a lower fee if they receive the payment as the consumer repays their monthly installments.

The pricing model for merchants vary. Among some of the fees that BNPL companies advertise are: up to 6% plus $0.30 per transaction, 1.5% plus $1.50 per transaction, or 3% plus $1 per transaction.

Banks

While the banks typically aren’t a party to BNPL transactions, these new payment schemes are still costing them. How? Many shoppers are using BNPL to circumvent credit cards, which charge compounding interest each month. For users that are in the habit of financing large purchases, it makes more sense to pay for the purchase over the course of four months, interest-free, than to incur credit card debt by only paying the minimum balance.

Challenger banks have been slowly making their way into the mainstream banking sector. By offering competitive rates, unique services, and digital-first user experiences, this new breed of banks has disrupted the traditional banking scene, causing some incumbents to rethink their approach.

This certainly seems to be the case with Credit Suisse, a 164-year-old bank. The Switzerland-based firm is steeling itself against challengers by launching its own digital bank, CSX. The new offering aims to be a hybrid approach between challengers and incumbents, and “combines the flexibility and cost effectiveness” of a digital bank with “the comprehensive range of services and expertise” of a traditional bank.

“CSX is intended for all private clients in Switzerland who want to complete their banking business swiftly and easily and who value digital, professional financial advice,” said Anke Bridge Haux, Head of Digital Banking at Credit Suisse. “Of course, we are still available to serve our clients in person. CSX clients can decide for themselves how they want to interact with us, depending on their individual needs.”

In order to serve clients from a range of demographics, Credit Suisse’s new digital bank will be divided into two offerings, CSX and CSX Young. Both take a mobile-first approach, from onboarding to a virtual debit card. Credit Suisse will launch the two accounts at the end of next month. After launching, the app will add services including investments, pensions, and mortgages.

In conjunction with today’s digital banking announcement, Credit Suisse also unveiled plans for a new concept branch that focuses on personalized advice. The bank is piloting the new concept at a new branch in Zurich and is building out the idea with a Digital Bar that offers interactive, personalized advice via video conferencing. Branch locations will also include co-working spaces, multimedia group rooms, and an event zone that can be booked by third parties.

Cross-border payments platform Payoneerannounced a major development this week. The New York-based company unveiled Payoneer for Banks, a tool to help banks make and receive cross-border payments.

The company’s new bank partnerships will offer secure low-cost international payments made in real time using the banks’ existing infrastructure. “By integrating with our APIs, banks can offer a seamless cross-border payments experience to their customers with low investment, which offers the potential for additional revenues, enriched offerings for customers and a competitive advantage,” said Eyal Moldovan, General Manager of SMBs for Payoneer.

The company reports it has already signed on 10 banks, challenger banks, and eWallets in 10 countries and it is in the middle of launching more partnerships. Among the list of disclosed partners are ANNA Money in the U.K.; Bank Asia in Bangladesh; BSB Bank in Belarus; EasyPay in Armenia; GCash, the leading mobile wallet in the Philippines; eZ Cash in Sri Lanka; Faysal Bank and JazzCash in Pakistan; Kuda Bank in Nigeria; Privatbank and Monobank in Ukraine; and Prex in Argentina.

Payoneer noted that now is an ideal time for the bank-focused product since many operations are moving to digital channels and international payment capabilities remain slow and unreliable.

“We focus on creating a bank that customers would love, and that drives a lot of our decisions,” said Monobank Cofounder Michael Rogalskiy. “It was extremely easy to work with Payoneer, because we have the same shared values and the same ideas around money transfers. Our integration allows our customers to have a better user experience, lower fees, and faster access to their international earnings. It’s a relationship that brings value for us, for Payoneer, and for our shared customers.”