This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

In 2020, banks will spend about $2.3 billion on core modernization just to satisfy customers and keep fintechs at bay. In the age of apps and the platform economy, do you know how to ensure your bank is ready to compete?

Watch this on-demand webinar to explore:

The future of cloud-first strategies

The future of platform-as-a-service strategies

How banks can accomplish these and achieve transformation goals more cost effectively

We close out 2019 with a deep dive into fraud prevention, cybersecurity, and regtech, as well as unique insights from FinovateAsia and Middle East. This quarter’s eMagazine includes insights into the micro-trends set to emerge in 2020, and interviews with some of the Finovate Awards winners about their innovations.

This week’s Finovate Podcast episodes are both focused on small and medium sized businesses, and the opportunities that fintech is creating for bankers, innovators, and small business owners themselves.

Our first guest is Karen Mills, former Small Business Administrator for the Obama Administration, and author of the book Fintech, Small Business & the American Dream. Greg caught up with Karen to talk about how the Great Recession hurt small businesses in particular, and how fintech has been able to step in and help.

Our second episode features Jeremy Berger of Arival Bank, a Best of Show winning demoer from FinovateAsia 2018. Arival is a challenger bank reaching out to unbanked/underbanked small businesses all over the world. The company is expanding from Asia into the United States and Europe, and Greg spoke with Jeremy about the company’s fintech-first solution to the challenges facing SMB banking.

Next week Greg will be speaking with Wayne Miller of The Venture Center, a fintech accelerator with ties to FIS and the ICBA.

The focus on the customer and their experiences has dominated the conversation within financial services over the past few years, but seems to have become especially pertinent in 2019. In our latest eMagazine, we examine the fintechs and institutions leading the way with excellent service and products that delight customers, both locally and globally.

This eMagazine features exclusive session recordings from the stage of FinovateFall– including insight and analysis on APIs, consumer lending platforms, and content and communication management. Over the course of reading you’ll find new ways of thinking about becoming truly customer-centric.

This is a guest blog post by Steve Boms, President of Allon Advocacy. Boms, a featured speaker and panelist at FinovateFall 2019 last month, takes a look at the current regulatory landscape in the United States when it comes to data privacy, and why he thinks we’re a long way off from having a one-size-fits-all approach.

Steve Boms, President, Allon Advocacy sits down with David Penn, Research Analyst at Finovate to talk regtech, open banking and the intersection of two within fintech & politics.

Data breaches have dominated the headlines recently, but a federal standard is still a pipe dream in the current political environment.

Why?

The answer is as old as the country itself: the tension between state and

federal power.

In

the current context, it is Republicans, typically strident defenders of states’

rights, who want a national system. House Energy and Commerce Committee Ranking

Member Greg Walden (R-Ore.) has said, “Your

privacy and security should not change depending on where you live in the

United States.” Industry advocates agree with the GOP, arguing for a national

standard because they worry compliance across 50 different state frameworks

would be impossible.

Though

several bills outlining national standards have been introduced in Congress,

including some with Democratic support, the two parties still cannot agree.

That’s because Democrats, along with consumer groups and privacy advocates,

repeatedly have said they will not support federal legislation that supplants current

and future state laws that may be stronger than a federal privacy regime.

Given

this ideological argument, federal action could still be years away.

If

you want progress fast, better to look to the states.

Data

privacy legislation has been introduced or filed in at

least 25 states. Maine and Nevada enacted significant legislation this year. Colorado and Massachusetts also did, and proponents

of data privacy legislation are active in New York. Connecticut lawmakers failed

to consider several data privacy bills, but did pass legislation to establish a

task force to examine what businesses operating in the state should have to

tell consumers about the data they collect.

This

trend – studying the issue – is evident in several states, and while such

“study bills” are sometimes viewed as bureaucratic inertia against more

powerful legislation, these mandates are quite often precursors to more

meaningful statutory changes. That certainly could be the case over the next

year.

The gold standard for state legislation is, of course, the California Consumer Privacy Act (CCPA) that is set to go into effect on January 1, 2020. In arguing against a uniform federal standard, it is the CCPA that Democrats are hoping to preserve.

Even

though it will take several months, even years, to reach consensus, it is

difficult to envision an eventual federal mandate that doesn’t look a lot like

the CCPA. The CCPA addresses numerous measures that empower consumers to

protect their data privacy, a common theme lawmakers, industry, and consumer

advocates all embrace.

Specifically,

the CCPA allows consumers to opt out of the sale of their information while

embracing their right to know, access, and delete what companies know about

them. The law also includes a 45-day grace period for businesses to comply with

consumers’ requests and imposes penalties on companies for privacy violations,

including the ability for consumers to exercise private rights of action for a

security breach.

California

lawmakers have introduced numerous bills since CCPA passage to clarify the

law’s prior to implementation. Amendments include the removal of certain

categories of data – namely employee and contractor information –and the need

to protect businesses’ preferred treatment of consumers who are part of loyalty

programs.

These

changes might not be enacted, but they present debates federal lawmakers should

watch.

Even with the CCPA as a guide, federal legislation must strike an appropriate balance between supporting consumer empowerment and supporting strong protection standards for consumers and businesses alike. Additionally, a major question still lingers in Washington over who should have authority over data privacy issues, and whether they should have the authority to establish rules or enforce current practices. A Government Accountability Office (GAO) report points to the Federal Trade Commission (FTC) as the most reasonable choice. Many in the industry agree, citing the agency’s authority to weed out “unfair or deceptive” consumer practices and the FTC’s existing authority to issue and enforce regulations on the collection of data on children under 13 years old.

In its

report, however, the GAO does question whether the FTC has the bandwidth to

oversee such an enormous issue, or if a new governing arm, similar to the

European Union’s European Data Protection Supervisor, should be established.

The most important issue facing federal lawmakers, though, is the need to protect innovation. The GAO urges Congress to consider how to “balance consumers’ need for internet privacy with the industry’s ability to provide services and innovate.” Strict privacy regulations may result in compliance costs that are too cumbersome for businesses, and consumer skepticism increases when privacy protections are too lax. Europe is starting to feel the effects of the General Data Privacy Regulation’s (GDPR) inability to balance the two (many U.S. businesses are not able to comply with the regulation’s excessively high bar or cannot pay the large fees and thus cannot offer their services).

Data

privacy is front and center on the global stage. The United States will fall

farther behind unless lawmakers focus on the common tenets of data privacy –

supporting consumer control, ensuring proper regulatory authority, and

embracing innovation – and pass a bipartisan bill.

Is your bank keeping pace with escalating customer expectations shaped by their mobile experiences? How are you addressing the perception that all banks are the same?

It’s tough when you have a product focus and outdated technology is holding you back. You know you need to modernize to win and retain demanding, empowered, and fickle customers. Customer loyalty and company revenue are at risk if you don’t.

In this webinar, featuring OutSystems and guest speaker Alyson Clarke, Principal Analyst at Forrester, you’ll learn how leading firms like Amazon, Nordstrom, USAA, and Zappos have made the shift to customer-centricity and are delivering world-class customer experiences.

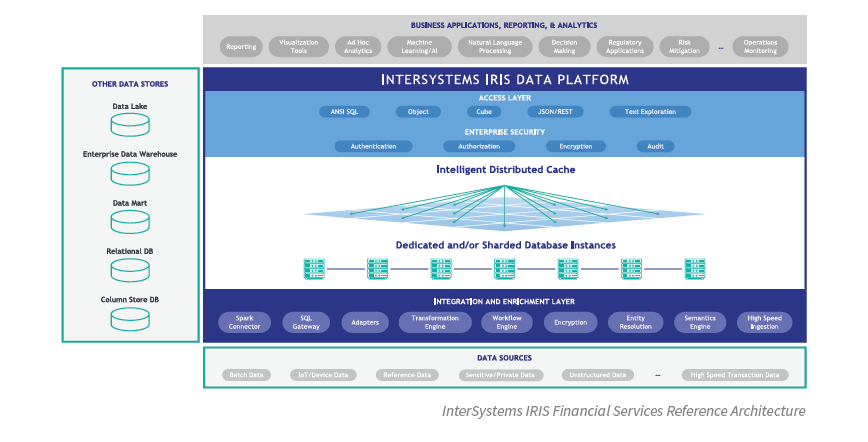

This is a sponsored blog post by InterSystems, a financial data technology company based in Cambridge, Massachusetts.

Successful financial services organizations today must be able to simultaneously process transactional and analytic workloads at high scale – accommodating billions of transactions per day while supporting thousands of analytic queries per second from hundreds of applications – without incident. The consequences of dropped trades, or worse – a system failure – can be severe, incurring financial losses and reputational damage of the firm.

InterSystems’ IRIS Data Platform is a hybrid transactional/ analytic processing (HTAP) database platform that delivers the performance of an in-memory database with the reliability and built-in durability of a traditional operational database.

InterSystems IRIS is optimized to concurrently accommodate both very high transactional workloads and a high volume of analytical queries on the transactional data. It does so without compromise, incident, or performance degradation, even during periods of extreme volatility and requires fewer DBAs than other databases. In fact, many installations do not need a dedicated DBA at all.

An open environment for defining business logic and building mobile and/or web-based user interfaces enables rapid development and agile business innovation.

For one leading global investment bank, InterSystems data platform is processing billions of daily transactions, resulting in a 3x to 5x increase in throughput, a 10x increase in performance, and a 75% reduction in operating costs. The application has operated without incident since its inception.

Traditionally, online transaction processing (OLTP) and online analytical processing (OLAP) workloads have been handled independently, by separate databases. However, operating separate databases creates complexity and latency because data must be moved from the OLTP environment to the OLAP environment for analysis. This has led to the development of a new kind of database. In 2014, Gartner coined the term hybrid transaction/analytical processing1, or HTAP, for this new kind of database, which can process both OLTP and OLAP workloads in a single environment without having to copy the transactional data for analysis.

At the core of InterSystems IRIS is the industry’s only comprehensive, multi-model database that delivers fast transactional and analytic performance without sacrificing scalability, reliability, or security. It supports relational, object-oriented, document, key value, and hierarchical data types, all in a common persistent storage tier.

InterSystems IRIS offers a unique set of features that make it attractive for mission-critical, high-performance transaction management and analytics applications, including:

High performance for transactional workloads with built-in guaranteed durability

High performance for analytic workloads

Lower total cost of ownership

InterSystems IRIS is enabling financial services organizations to process high transactional and analytic workloads concurrently, without compromising either type – using a single platform – with the highest levels of performance and reliability, even when transaction volumes spike.

Founded in 1978, InterSystems is a privately held company headquartered in Cambridge, Massachusetts (USA), with offices worldwide, and its software products are used daily by millions of people in more than 80 countries. For more information, visit: Financial.InterSystems.com

Thursday, October 17, 2019 | 2pm EDT | Register now

Technology advancements and the proliferation of consumer apps have created a new customer experience paradigm that is changing how people are using credit cards. Customers expect brand interactions to feel like a dialogue, one that is relevant, timely and personal to them; regardless of whether that’s online or offline.

Watch this webinar to learn more about:

The customer experience paradigm shift, from episodes to journeys

How to leverage the power of contextual marketing to enhance the cardholder lifecycle

How to optimize your cardholder lifecycle management

Featuring Jason Davies, VP, Enterprise Innovation, FlyBits and Rebecca Engelberg, Marketing Intelligence Manager, FlyBits.

This is a sponsored blog post by Randy Koch, CEO of ARM Insight, a financial data technology company based in Portland, Oregon. Here, he explores what synthetic data is, and why financial institutions should start taking note.

You’ve heard it before – data is invaluable. The more data your company possesses the more innovation and insights you can bring to your customers, partners and solutions. But financial services organizations, which handle extremely sensitive card data and personally identifiable information (PII), face a difficult data management challenge. These organizations have to navigate how to use their data as an asset to increase efficiencies or reduce operational costs, all while maintaining privacy and security protocols necessary to comply with stringent industry regulations like the Payment Card Industry Data Security Standard (PCI DSS) and the General Data Protection Regulation (GDPR).

It’s a tall order.

We’ve found that by accurately finding and

converting sensitive data into a revolutionary new category – synthetic data –

financial services organizations can finally use sensitive data to maximize

business and cutting-edge technologies, like artificial intelligence and

machine learning solutions, without having to worry about compliance, security

and privacy.

But first, let’s examine the traditional types of data categorizations and dissect why financial services organizations shouldn’t rely on them to make data safe and usable.

Raw and Anonymous Data – High Security and Privacy Risk

The two most traditional types of data

categorization types – raw and anonymous – come with pros and cons. With raw

data, all the personally identifiable information (PII) fields for both the

consumer (name, social security number, email, phone, etc.) and the associated

transaction remain tagged to data. Raw data carries a considerable risk – and

institutional regulations and customer terms and conditions mandate strict

privacy standards for raw data management. If a hacker or an insider threat were

to exfiltrate this type of data, the compliance violations and breach headlines

would be dire. To use raw data widely across your organization borders on

negligence – regardless of the security solutions you have in place.

And with anonymous data, PII is removed, but the real transaction data remains unchanged. It’s lower risk than raw data and used more often for both external and internal data activities. However, if a data breach occurs, it is very possible to reverse engineer anonymous data to reveal PII. The security, compliance and privacy risks still exist.

Enter A New Data Paradigm – Synthetic Data

Synthetic data is fundamentally new to the

financial services industry. Synthetic data is the breakthrough data type that

addresses privacy, compliance, reputational, and breach headline risks head-on.

Synthetic data mimics real data while removing the identifiable characteristics

of the customer, banking institution, and transaction. When properly

synthesized, it cannot be reverse engineered, yet it retains all the

statistical value of the original data set. Minor and random field changes made

to the original data set completely protect the consumer identity and

transaction.

With synthetic data, financial institutions

can freely use sensitive data to bolster product or service development with

virtually zero risks. Organizations that use synthetic data can truly dig down

in analytics, including spending for small business users, customer

segmentation for marketing, fraud detection trends, or customer loan

likelihood, to name just a few applications. Additonally, synthetic data can

safely rev up machine learning and artificial intelligence engines with an

influx of valuable data to innovate new products, reduce operational costs and

produce new business insights.

Most importantly, synthetic data helps fortify internal security in the age of the data breach. Usually, the single largest data security risks for financial institutions is employee misuse or abuse of raw or anonymous data. Organizations can render misuse or abuse moot by using synthetic data.

An Untapped Opportunity

Compared to other industries, financial

institutions haven’t jumped on the business opportunities that synthetic data

enables. Healthcare

technology companies use synthetic data modeled on actual cancer patient

data to facilitate more accurate, comprehensive research. In scientific

applications, volcanologists

use synthetic data to reduce false positives for eruption predictions from

60 percent to 20 percent. And in technology, synthetic data is used for

innovations such as removing

blur in photos depicting motion and building

more robust algorithms to streamline the training of self-driving

automobiles.

Financial institutions should take cues

from other major industries and consider leveraging synthetic data. This new

data categorization type can help organizations effortlessly adhere to the

highest security, privacy and compliance standards when transmitting, tracking

and storing sensitive data. Industry revolutionaries have already started to

recognize how invaluable synthetic data is to their business success, and we’re

looking forward to seeing how this new data paradigm changes the financial

services industry for the better.

In this sponsored blog post, Akshatha Kamath, Content Marketing at MoEngage, breaks down new privacy legislation which could impact financial institutions across the states.

Stronger

privacy protection and greater data transparency online are growing global

trends. The Cambridge Analytica scandal, in which the Facebook data of at least

87 million people were misappropriated, and other instances like this have

brought attention to how businesses collect, use, and sell consumer data.

Concern over the use and misuse of this data is widespread.

In many global jurisdictions, the response has been privacy legislation which forces businesses to comply with sometimes onerous regulations regarding consumer data and privacy. One of these pieces of legislation is the California Consumer Privacy Act. In its second section it lays out how pervasive privacy concerns have become and how “it is almost impossible to apply for a job, raise a child, drive a car, or make an appointment without sharing personal information.”

All of this data can be great for marketers, but businesses need to comply with privacy laws in order to avoid fines and stay up to date with consumer demand for privacy and data transparency online.

The California Consumer Privacy Act (AB-375)

The

California Consumer Privacy Act of 2018 (CCPA) is by far the strongest privacy

legislation enacted in the United States at this time. Businesses must be in

compliance by January 1, 2020 (the starting date on which the state can bring enforcement actions involving

noncompliance).

For marketers there are three major things to be aware of. First is that wherever personal information is collected businesses must disclose what information they collect and how they will use it. Secondly, businesses have to provide consumers with the ability to “opt out” of having their information sold to third parties. Thirdly, businesses must allow consumers to view and delete the information that has been collected about them.

Is My Company Affected by the CCPA?

If

your business (or for-profit entity) is located in California and meets any of the

following criteria, it has privacy requirements that need to be met under the

law. The criteria are:

Your business’ annual revenue is

over $25 million

Your business receives information

of over 50,000 consumers, households, or devices annually

At least half of your business’

annual revenue comes from selling personal information

The law doesn’t differentiate between brick-and-mortar and online companies. This means that even a company with no physical presence or employees in California could still do business there and therefore has obligations under the law. So your business doesn’t even need to be located in California for the California Consumer Privacy Act to apply to you. Like the GDPR, CCPA will affect businesses outside the law’s jurisdiction.

Consumer’s Rights Under the CCPA

Consumers have new rights under the CCPA that companies need to be aware of. These rights fall into three broad categories:

The Right to Knowledge – Under the CCPA, businesses must allow consumers to obtain, twice per annum at zero cost, all the information that the business has about them, how that information was collected, and who else has been given said information.

The Right to be Forgotten – The CCPA stipulates that consumers must be able to request the deletion of all of their personal information from a company. If the information has been shared with third parties then those parties must also delete said information.

The Right to Control who has Access to their Information -Businesses must allow consumers to be able to opt out of the resale of their information. Consumers under the age of 16 must affirmatively opt in to allow the resale of their data. Consumers under the age of 13 must have written permission from a parent or guardian in order to allow the resale of their data.

What Marketers Need to Do

First of all, marketers need to review their current procedures and understand their policies and procedures regarding the collection, storage and use of subscribers’ data and mailing preferences. They need to know how a user’s preferences about their data can be stored and how documentation would be provided if a user requests it.

Second of all, marketers need to think in the long term about how they set up their systems. For example, even though GDPR only applies to EU visitors, many companies have opted to implement the same higher standards across their entire platform in order to proactively prepare for similar legislations. In the same vein, marketers who prepare for the CCPA will have a leg up if privacy bills that are making their way through the legislature pass in New York, Mississippi, and Massachusetts.

Penalties for Non-Compliance of the CCPA

If,

because of a business’ negligence, a consumer’s information is improperly

disclosed, the CCPA makes it easier for consumers to sue (even if there is no

evidence that the data breach caused the consumer harm!).

What

could be very costly for businesses is the potential for class-action lawsuits

due to a data breach. Companies could be on the hook for between $100 and $750

per incident (or even more if the actual damages exceed $750).

Conclusion

The

California Consumer Privacy Act will go into effect on January 1, 2020.

Marketers should prepare in advance to make changes to comply with the

regulations. At the same time, CCPA presents marketers with an opportunity to

strengthen the relationship between consumers and your business. Educate

consumers on the data you are collecting and how you make use of it. Be sure to

tell them their rights under the CCPA and how you are compliant. This can build

trust with consumers and help you use the CCPA to your advantage.

Akshatha Kamath, Content Marketing at MoEngage, looks into the common challenges for enterprise marketing teams and asks whether automation is the answer.

Marketing for a large enterprise company is challenging. It is often the case that big organizations have multiple teams working on marketing that are each in their own silo. The data is segmented, the campaigns are segmented and the teams do not talk to one another. This can cause friction in your organization when your marketing messages may be broadcast to hundreds of thousands or even millions of consumers.

When your marketing teams are working in silos your brand suffers. One customer might receive multiple different disjointed marketing communications from your brand and this impacts the customer experience negatively, as well as being a waste of your marketing resources.

Expansion to New Frontiers

Another

current challenge of enterprise marketers is creating a seamless customer

experience on and offline. For brick and mortar brands building out digital is

an imperative (87% of executives say it is a “matter of survival”).

This is an especially taxing challenge for large enterprise brands who may have to juggle supporting local marketers with limited resources – be they a dealership or franchisee. Often, it may be that these local marketers do not have the same marketing experience as those working at corporate headquarters. They execute their campaigns without much background in marketing while also dealing with human resources, bookkeeping, inventory and all the other headaches that come with running a business.

Supporting these local marketers is also a challenge for brand managers. They can also be resource-strapped and often may not have enough to do all they need to accomplish. There’s a chance they also don’t have the campaign budget to produce all that they need and brand managers often don’t have dedicated staff to verify in-store compliance.

For an enterprise brand manager to overcome these challenges and successfully implement their marketing strategy, communication with local marketers is key. Brand managers must encourage success at the local level. Those who have high local marketer satisfaction have an active dialogue with local marketers to better appreciate how they are struggling. These brand managers also invest in easy-to-use tools in process, design, and technology. The higher quality the communication is, the better the outcome.

Solving Geographic Difficulties

A brand manager’s job is to make local marketing easy for affiliates. In a distributed organization it takes a lot of stakeholders to run just a single campaign. Something as simple as printing up a poster to be hung in a storefront window may require input and approval from design, brand management, compliance, and local marketers.

This is a natural part of enterprise distributed marketing as one’s business model is distributed so workflows are going to be complex. Despite the complicated approval processes and multiple stakeholders involved, these systems can be made more efficient with the right tools. Streamlining workflows for distributed enterprise marketing involves documenting the process of what needs to be done in order to make it easier for all involved to follow it. Often companies find it beneficial to use technology to do this.

Multi-geographic brands can also rarely monitor all field execution of marketing in person. This can generate concern that brand messaging is being modified in a way that is out of line with the brand’s standards.

Consumers typically do not distinguish between enterprise-owned and locally-owned businesses – they see just one thing: brands. 60% of millennials in the United States expect consistent experiences when dealing with brands whether online, in-store or by telephone. This highlights how important it is for distributed enterprise brands to keep their message consistent.

Education and knowledge about a brand are critically important for all stakeholders. Many distributed brands have affiliate on-boarding and training processes that place branding as a core subject. Other brands are finding value in marketing asset management technology in order to scale consistently. They use template tools for executing their local marketing strategies which allows brand management teams to “lock” certain design characteristics or messages and allow local marketers to input their information (such as address or local offers) in order to maintain brand consistency.

Is Automation the Solution?

What enterprise marketers may need is a system that streamlines their marketing channel in order to bring together marketers, campaign managers, and product managers under one system to efficiently manage marketing campaigns with input and collaboration between all of those involved.

MoEngage has developed some tools for enterprise marketing teams using extensive feedback from stakeholders. This unified approach to enterprise marketing can send out a clear signal amidst the noise. MoEngageTeams and MoEngage Campaign Approval Workflow are two such tools that enable brands to eliminate the silos within their teams and ensure a smooth flow of customer data and insights between teams. This can help enterprises eliminate the challenges that stem out large teams spread across geographies or multiple owned brands that need a unified customer view, and many more. Talk to MoEngage’s experts for a personalized walk-through of these enterprise-ready marketing tools from MoEngage.

The following guest blog post is written and sponsored by MoEngage.

MoEngage, an Intelligent Customer Engagement Platform built for the mobile first world, has been featured in the 2019 Gartner Magic Quadrant for Mobile Marketing Platform for the second time in a row. It is the youngest company to be featured in the report and has made the biggest leap in improvement in its position as compared to all the other vendors. You can read the complimentary copy of the report here.

In its initial years, MoEngage’s platform saw rapid adoption from mobile-first startups and mid-market brands. As these brands grew, with some even becoming unicorns, MoEngage’s platform also improved to match the growing complexity and scale of their customers. Building on this momentum, MoEngage made significant investments in customer experience and product innovation. Today, MoEngage has evolved into a robust mobile marketing platform that has seen significant adoption by enterprises across Asia, the U.S., and Europe. In the last 12 months, the company has added several large enterprise clients such as Future Retail, Deutsche Telekom, Mashreq Bank, Travelodge, Samsung, and more. Enterprise clients contribute nearly 50% of MoEngage’s total revenues, while mobile first brands and unicorns contribute the rest.

“Our progression in Gartner’s Magic Quadrant and adoption by large enterprises is a testament to our investments in product innovation and customer success. Consumer brands in 35 countries trust MoEngage to power their cross-channel customer engagement campaigns to improve adoption, retention, loyalty, and customer LTV. This recognition reinforces our vision to be the most trusted customer engagement platform for the mobile-first world. We place customers at the heart of everything we do and our customer obsession is reflected by not just our renewal rates, but also by the reviews on Gartner Peer Insights websites” said Raviteja Dodda, CEO and founder, MoEngage.

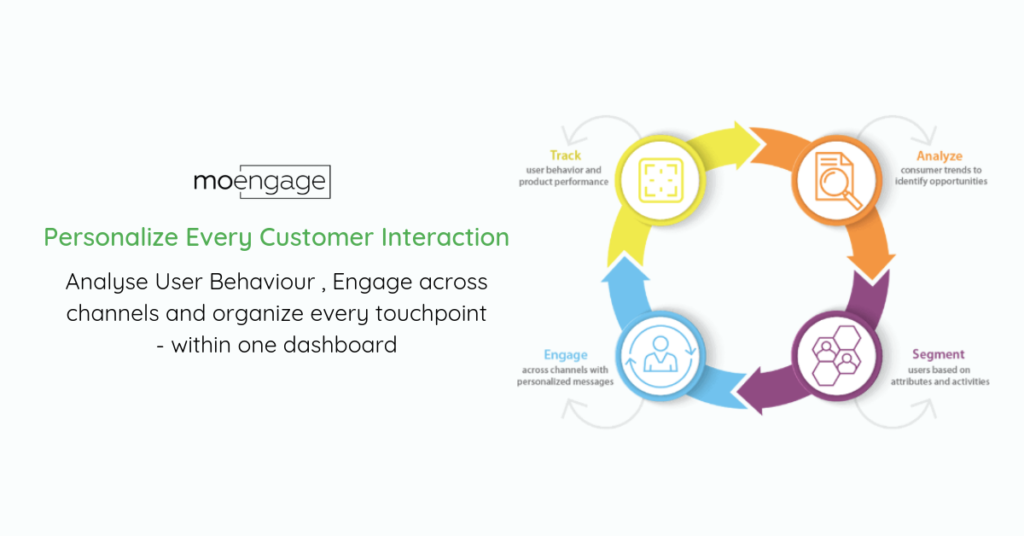

Designed for the mobile-first world, MoEngage provides one dashboard through which consumer brands can analyse user behavior, engage across channels and personalize every touchpoint. Processing over 45 billion user interactions and delivering over 25 billion messages to 400 million users every month, MoEngage is one of the fastest-growing companies in this space. To know more visit www.moengage.com

Gartner Magic Quadrant for Mobile Marketing Platforms, Mike

McGuire, Charles Golvin, 15 July 2019 GARTNER is a registered trademark and

service mark of Gartner, Inc. and/or its affiliates in the U.S. and

internationally, and is used here with permission. All rights reserved. Gartner does not endorse any vendor, product or service depicted in

its research publications, and does not advise technology users to select only

those vendors with the highest ratings or other designation. Gartner research

publications consist of the opinions of Gartner’s research organization and

should not be construed as statements of fact. Gartner disclaims all

warranties, expressed or implied, with respect to this research, including any

warranties of merchantability or fitness for a particular purpose.