This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Payment and transaction services company Worldline and credit decisioning firm Algoan are joining forces.

The two are developing a credit assessment tool that will help lenders make better, faster, and more efficient lending decisions.

The credit assessment solution will leverage Worldline’s open banking experience as well as Algoan’s credit decisioning expertise.

Payment and transaction services company Worldlineannounced a partnership with credit decisioning firm Algoan. As part of the agreement, the two firms will work together to develop a credit assessment solution to help lenders and services providers make better credit decisions.

Specifically, the partnership will leverage Worldline’s open banking experience. “At Worldline we look for innovative partners who share our vision and enable us to enrich and expand our open banking services,” said Worldline Managing Director Financial Services Michael Steinbach. “As a lead and one of the largest Open Banking providers in Europe, we are committed to unlocking the full potential of Open Banking. With Algoan, we will be able to offer our customers an end-to-end and cost-efficient white-label solution to assess credit worthiness.”

According to Alogan CEO Michael Diguet, it is an ideal time to launch this solution. “Open Banking credit scoring is experiencing momentum that big players should embrace,” said Diguet.

Another key resource behind the credit assessment solution is Alogen’s four years of credit scoring expertise. Financial institutions can use the new tool to receive more accurate credit scoring and increased processing efficiency. Underwriting use cases include personal finance, consumer lending, auto finance and leasing, retail lending, BNPL, insurance, and utility providers.

The credit assessment solution will also bring benefits to borrowers. The enhanced data means that more borrowers may be approved and will receive their approval faster.

Having won its first contract to facilitate card transactions in 1973, Worldline currently has 20,000 employees in more than 50 countries and counts annual revenue of almost $4 billion. Gilles Grapinet is CEO.

There’s more to fintech innovation in Mexico than remittances. But this week’s fintech headlines from America’s nearest neighbor to the south have reminded of the major role that money transfer services play in the financial services landscape of nations like Mexico.

Late this week, Western Union announced that it was teaming up with Pagaphone SmartPay to offer its customers additional options when it comes to sending and receiving money from the U.S. to Mexico. Courtesy of the new arrangement, U.S. customers will be able to send money via a variety of Western Union channels, from WU.com to the company’s mobile app to any one of Western Union retail locations in Mexico. Recipients receive the funds on their phones by accessing their PagaPhone SmartPay accounts. Funds can then be transferred to bank accounts, withdrawn as cash from an ATM using their PagaPhone debit cards, or used to pay for products and services directly from the app.

“By teaming with Western Union, PagaPhone SmartPay users in Mexico have yet another way to receive money from friends and family cross-border, using a brand known and trusted for decades,” PagaPhone Smart Pay and Cloud Transfer Services CEO and founder Ulises Tellez said.

More than $51 billion was sent to Mexico in remittances last year, Head of Western Union Mexico and Central America Pablo Porro said, underscoring the major role of cross-border payments in the region. “With this surge in remittances, customers demand choice and added convenience for how and when money is sent and received,” Porro added.

Headquartered in Mexico City and founded in 2018, PagaPhone offers an e-Wallet that enables users to cash remittances directly from their smartphone – as well as conduct a number of other transactions ranging from payments to cash withdrawals.

Also this week, we learned that Mexican fintech Broxel has announced the availability of free remittances for Mexicans living in the U.S. As part of its commemoration of Cinco de Mayo on Thursday, Broxel will make it both easier and more affordable for more members of the Mexican-American community to send money to relatives in Mexico for free.

“Millions of families in Mexico depend on the hard work of people trying to achieve their dreams, sending money every week as an act of love, memory, and gratitude,” Brozel Client Services Supervisor Mario Lopez said. “So having a financial product that allows the Mexican community to send money for free, is proof that technology can change people’s lives.”

Available from the company’s website, the Broxell Pay App offers free remittances among a number of other features. These include a Mastercard debit card, the ability to have both a peso-denominated account issued in Mexico and a dollar-denominated account issued in the U.S. on the same app, and a travel discount service.

“Technology is erasing borders,” Broxel founder and President Gustavo Gutiérrez said. “The idea of having free remittances is an economical disruption for the North American region, and a game-changer for millions of potential users.”

What’s going in Mexican fintech other than cross-border payments? Why crypto, of course!

YoCripto, a Mexico-based bitcoin rewards credit card, is gearing up for a launch later this year. As reported in Fintech Futures this week, the company calls itself the first Latin American fintech to offer a credit card with bitcoin rewards. YoCripto plans to offer both a virtual and a physical Visa-powered credit card, with Bitcoin rewards of as much as 3% on all transactions. The card will also feature a low interest rate, no annual fees or commissions, and instant credit approvals.

Designed to serve the young and underbanked Latin Americans, Yo Cripto was founded by Julian Arber and Rafael Maya in January of this year. Both Arber and Maya have significant backgrounds in financial services; Arber at Merrill Lynch and Morgan Stanley, Maya at American Express. The company raised $4 million in seed funding in February in a round led by DILA Capital and, after launch, plans to expand to Colombia, Chile, Peru, and Argentina.

“Our main goal is to promote financial inclusion across Latin America,” the founders said in an interview with LABS (Latin American Business Stories), “allowing users to obtain the benefits of the crypto ecosystem without its complexity.”

ICYMI … Check out our coverage of the $15 million in funding raised by Indian fintech Kaleidofin this week.

India-based financial services provider Kaleidofin announced it has raised an additional $5 million in funding, adding to the $10 million investment the company received in January of this year. The $15 million round brings Kaleidofin’s total funding to just shy of $23 million.

Here is our look at fintech innovation around the world.

Tanzanian fintech NALA teamed up with Kenyan payments company Cellulant to faciliate remittance payments from the U.K. and U.S. to Kenya, Uganda, Tanzania, and Ghana.

In a world full of inequalities, it is no surprise to see an imbalance when it comes to finances, and investing in particular.

For more insight into this industry conundrum, we spoke with Rukayyat Kolawole, CFA. Kolawole is familiar with inequities in the financial world, given her role as Founder and CEO of PaceUP Invest, a new platform launching on May 15th that offers e-learning, financial coaching, investment strategy, and execution for women and underrepresented groups.

Our conversation below highlights not only tips on bridging the knowledge gap, but also on building diversity and her view on the future of the retail investing industry.

When it comes to retail investing, there is a significant knowledge gap. What are some practical ways the fintech industry can bridge this gap and ultimately increase the number of investors?

Rukayyat Kolawole: The fintech industry can bridge this gap by incorporating financial literacy into its solution. The main reason people, especially women and those from underrepresented communities, do not invest is because of the lack of knowledge and being underserved by the finance industry. Many robo-advisors stop the process if the client indicates they are a novice to investing. Even though they include information and definitions of financial terms on their platform, this is not provided with the aim of increasing financial literacy overall, irrespective of the product they sell.

This represents a missed opportunity by the current robo-advisors to provide learning products and improve financial knowledge. At PaceUP Invest, we provide a hybrid, jargon-free financial literacy and investment platform to bridge the gap, and we have seen the impact on different communities. Incorporating behavioral science is also key to helping educate and increase the participation of potential retail investors.

How does the industry stand to benefit when the number and diversity of investors increases?

Kolawole: The industry will benefit immensely from a retail investor’s perspective because we will start to see a lot of gaps. For example, we’ll see a pension gap, retirement gap, and racial wealth gap gradually narrowing. Policies are still needed to ensure all these gaps are narrowed. Underrepresented communities and minorities will be greatly impacted by making a financial decision that will increase not only the number but also the average financial assets that they will hold. The economic benefit for society would be even larger.

When we look at capital allocators, it is still very much the old boys’ club of white and male. Very little is going towards women and people of color. The only way that people can get funding to solve real problems affecting their communities is if more women and people of color are writing the cheques. Otherwise, it’s going to be the same boys’ club.

How has the state of retail investing and retirement planning changed from how it was just five years ago?

Kolawole: Across the globe, we saw a spike in retail investing due to easy-to-use investing and trading apps. 2020 was called the year of retail investors, and the pandemic has no doubt contributed to the spike in retail trading. People became more empowered than ever. Retail trading has taken off more in the U.S. than in Europe. Retail investing in Europe makes only around 5% to 7% of total investments in Europe, compared to 25% in the U.S. and 60% in China.

With the large pension gap in Europe still not changing much in the past five years, low-interest rates, and new online brokerages being built could help to propel enough momentum to increase participation in the capital markets to solve these problems. Retail investing is here to stay!

However, we need to make it more inclusive for women and underrepresented communities.

When you think about what the industry will look like 10 years from now, what do you think will be different? What role will decentralized finance play?

Kolawole: People will have more choices and be in more control of their finances. More people will be financially independent and empowered via choices of products that solve their problems. Fintech will revolutionize and help to reduce a lot of gaps we currently have when it comes to money and wealth.

Banks will have their place in the future financial system, requiring more flexibility and a customer-centric approach by partnering with fintech companies to solve real-life solutions.

However, our financial world will probably not become that decentralized due to regulations and governments wanting to retain monetary power.

New to FinovateSpring this year, we’re connecting startups raising early-stage capital with investors who can make it happen. And there’s still room at the table. If you’re a startup raising pre-seed/seed/series A funding, apply now. Interested investors should reach out to Heather Stowell.

To shed a little more light on our Advanced Startup Booster program on May 18, Greg Palmer, VP of Strategy and host of The Finovate Podcast, sat down with one of the investors, Garnet Heraman, who will be meeting these startups.

As Founder and Managing Partner at Aperture Venture Capital, Heraman not only has VC insight into startup funding in the fintech industry, but he also has years of entrepreneur experience, notably as the CEO of three tech companies acquired within years of each other.

“In a general sense, this is such a people business and such a leadership and management business, especially at the early stages of a VC-backed company,” Heraman said. “At the early stages of a startup, I think it’s all about personalities, personal discernment and rapport, leadership, and substance. Saying what you mean and meaning what you say. Tried and true maxims about what it takes to be a good, bankable person.”

Heraman added, “In our fintech world specifically, what Aperture looks for essentially is what we call ‘fintech adjacent’ or ‘fintech plus.’ We’re looking for those undiscovered intersections between traditional fintech and some compelling lucrative enterprise segment. A company that takes a problem-solving perspective and lives at that intersection.”

Below are some further insights from Heraman from his recent conversation with Finovate VP Greg Palmer.

On building networks and ecosystems

(The) Startup Booster Program looks like an awesome way to get the right companies in front of the right people at the right time. I (think) about where I was when I was a first- and second-time entrepreneur. (We) could have done a much better job of essentially getting out and about into the conferences and building networks and building ecosystems.

On delivering value to pre-seed fintech startups

We feel like there is an immense opportunity to deliver value to these pre-seed companies if you can make that alignment happen proactively. Beyond any kind of capital, things like product and technology support, sales and distribution support, logistics and supply chain guidance and resources (are critical). To the extent that those things can be more readily available to more pre-seed companies, what you’re going to see is . . . the overall ecosystem for pre-seed companies develop better and rise to the top.

On the importance of a healthy startup ecosystem

Without young startups being in channels that have them coming into contact with seed and later-stage VCs and/or corporations, a couple of things happen. They don’t get the funding they need and the smart money they need, like access to mission critical operational resources, at a critical time when they are still developing. Without the opportunity to refine, if not pivot, make mistakes and fix them, the overall market is going to be bereft of companies that could otherwise do well for themselves.

On the importance of diversity

If only a tiny portion of all of these billions of dollars in VC capital is going to people of color, you have to ask yourself what is the opportunity cost to the gross national product of this country? By not having more money go into the hands of innovators and entrepreneurs who are people of color and, maybe more importantly, female, what is the opportunity cost?

Advanced Startup Booster meetings take place on May 18 between 5pm to 6pm. For more information on how to get involved, visit our Startup Booster program hub today!

Cryptocurrency accounting firm Tactic raised $2.6 million in funding.

Leading the investment round were Founders Fund and finance automation company Ramp.

The new capital will help the company add talent and continue to build out its platform.

With more and more companies seeking to diversify their finances with cryptocurrencies, a new U.S.-based startup has arrived to help these businesses better manage their cryptocurrency holdings.

The company, Tactic, announced today that it has raised $2.3 million in seed funding. The investment was co-led by Founders Fund and Ramp, a finance automation company. Also participating in the funding were individual investors Elad Gil and Dylan Field, co-founder of Figma. Tactic said that, among other needs, the new capital will help the company hire additional talent.

Tactic helps businesses account for their cryptocurrency holdings by aggregating data across disparate sources – often multiple wallets across multiple blockchains – to provide a full treasury view of all balances and account activity. Tactic enables companies to automatically categorize their transactions and apply basic accounting logic and rules to calculate gain/loss and identify taxable events. Accounting teams can also use the platform to reconcile the cryptocurrency subledger to traditional accounting systems such as QuickBooks.

“Tactic solves a real pain point for businesses managing cryptocurrency finances and the product is already saving crypto accounting teams days each month,” Founders Fund Principal Leigh Marie Braswell said. “We believe Tactic has the potential to become a massive player as more companies move into web3.”

Founded by CEO Ann Jaskiw and launched in 2021, Tactic has since reeled in “dozens” of customers, from early stage startup companies to billion-dollar businesses. Jaskiw started Tactic after learning that many companies involved in web3 were using spreadsheets for their accounting because there were no other solutions available for them. By contrast, Tactic has developed its solution in part by teaming up with leading accounting firms to help them apply accounting guidelines to activities common in the DeFi world such as staking, NFT, minting, and airdrops.

Tactic VP of Strategy and Ops John Dempsey put Tactic’s platform in the context of other fintech solutions that leverage automation and other enabling technologies to make operations more efficient. “Businesses have come to expect back-office solutions that help them get started quickly and automate their manual tasks,” Dempsey said. “Tactic makes it easy for businesses to transact in cryptocurrency, knowing they can manage their financial activity in a clean, compliant way.”

Canada’s Neo Financial closed $145 million ($185 million CAD) in funding.

The round brings the three-year-old company’s total funding to almost $240 million ($299 CAD) and boosts its valuation past $785 million ($1 billion CAD).

Neo is now one of only a few Alberta-based tech companies to become a unicorn.

Canada-based Neo Financial’s newest funding round has boosted the company up to unicorn status in Canadian dollars. The $145 million ($185 million CAD) investment was led by Valar Ventures and saw participation from Tribe Capital, Altos Ventures, Blank Ventures, Gaingels, Maple VC, and Knollwood Advisory.

Today’s investment boosts Alberta-based Neo Financial’s total funding to almost $240 million ($299 CAD). It also marks the company as one of just a few tech companies in the region to become a unicorn.

Founded in 2019, Neo Financial differentiates itself with its user-friendly banking technology. The company boasts one million users of its four main products, which include a credit card, high-interest savings account, and investment tools. Additionally, Neo Financial is slated to launch a mortgage offering by the end of this year.

“We’re constantly challenging the status quo,” the company said in a blog post, “and asking the questions that should be asked: What if you only needed one loyalty card instead of 20? What if your financial services experience was as seamless as Netflix or Spotify? What if getting a mortgage could be a fully digital experience? What if the future of banking wasn’t a bank?”

With 650 employees under its roof, a number that has doubled in the past year, Neo Financial is growing. The company has added more than 11 products and features in the past year alone. To fuel this growth, the company adding 100 people to its workforce in Calgary and Winnipeg.

“The pace at which this team releases new products and grows its customer base is among the fastest we have seen in our careers,” said Valar Ventures Founding Partner Andrew McCormack.

Maple VC’s Andre Charoo echoed those thoughts. In an interview with TechCrunch, he said, “Neo is the fastest growing company I have seen in Canada… I believe Neo has a shot at owning at least 10% of the aggregated $550 billion banking sector in Canada (ie. $50 billion) due to the network effects it has created with its unique merchant loyalty program.”

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

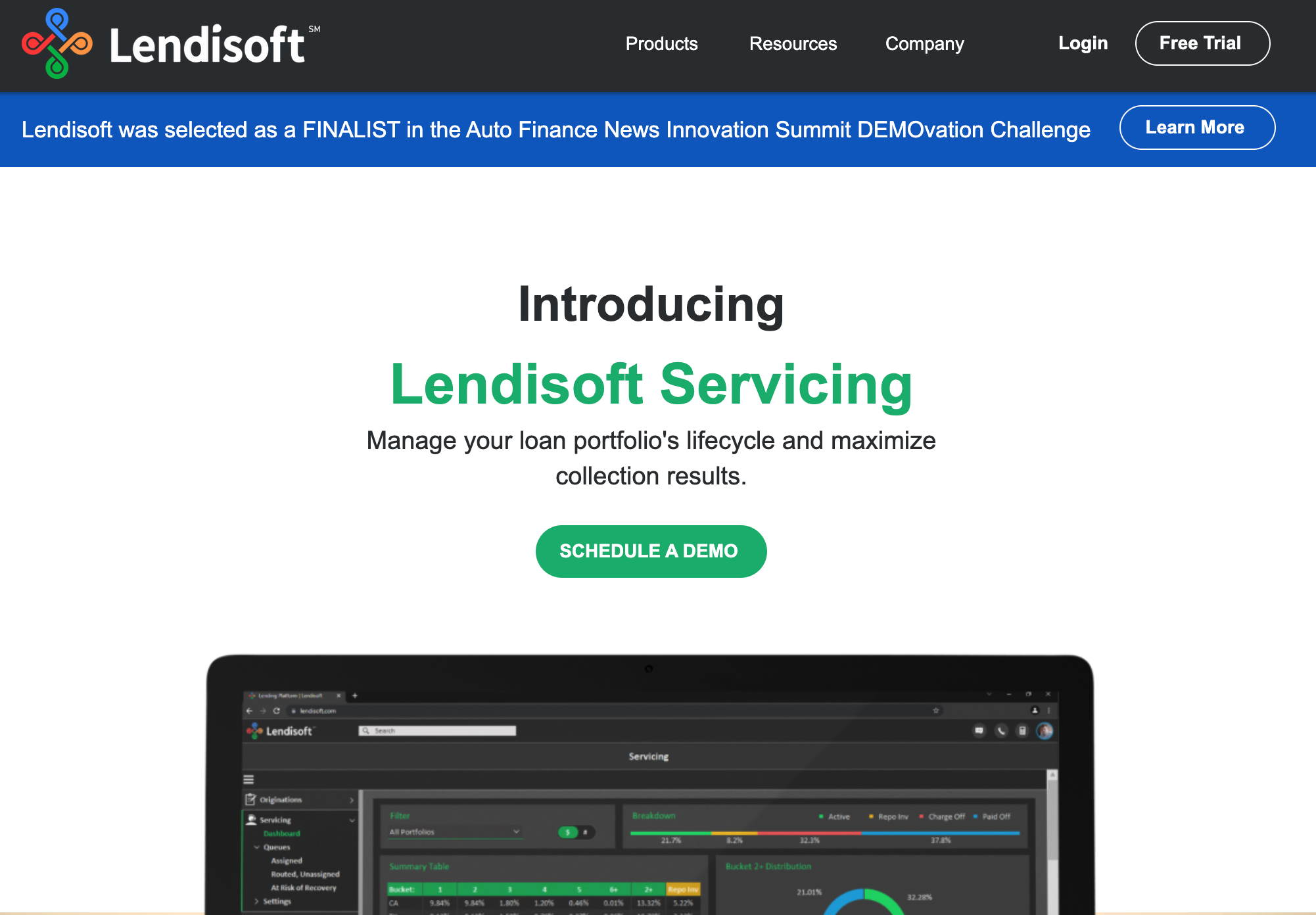

Lendisoft transforms the end-to-end loan management process with a SaaS suite integrating risk management and compliance IQ. Machine learning and AI automation result in workflow and performance differentiation.

Features

Workflow and process design with integrated risk management and compliance

Machine learning and AI automation

SaaS scalability, scoring models and easy UI

Why it’s great

Lendisoft transforms the loan portfolio management business with integrated risk management, compliance, machine learning, AI automation, and a process driven design resulting in ~30% lift in monthly performance.

Presenters

Rick Haskell, COO & Founder Haskell has over 30 years in lending excellence and leadership driving operational performance with repeatable and scalable processes. His workflow design and risk management strategies are key advantages. LinkedIn

Bill Gerber, CRO and Founder’s Circle Gerber has been on the bleeding edge of consumer engagement technology his entire career. He has driven, contributed and experienced 11 acquisitions. He is an agent of change and performance. LinkedIn

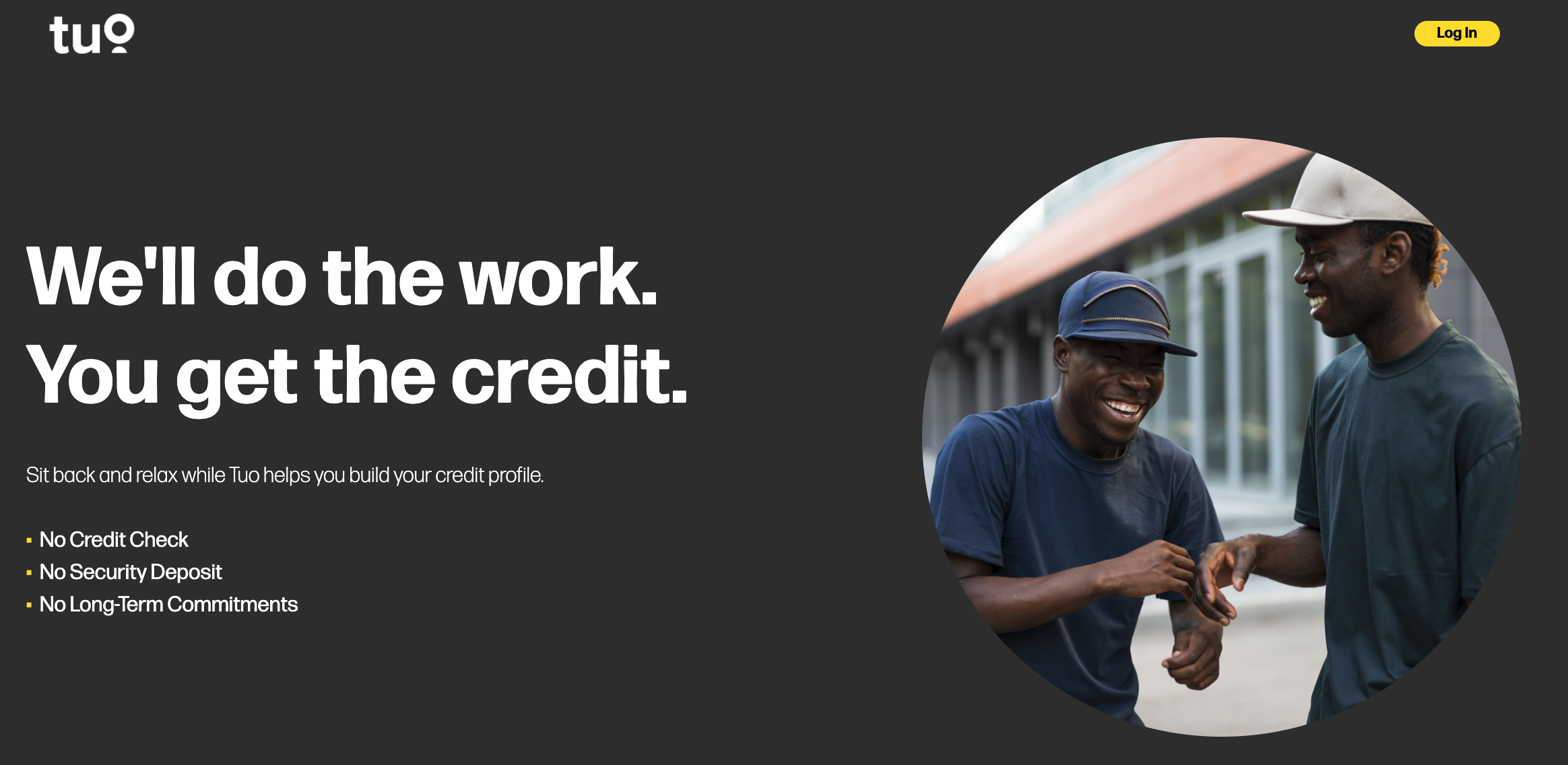

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

Tuo is a leading alternative data credit services company that creates industry-leading credit underwriting and servicing solutions to truly support the underbanked.

Features

Increase credit application conversions with the white-label Tuo Credit Builder that allows users to build credit on autopilot.

Why it’s great

A true “SET IT and FORGET IT” credit building solution. Tuo does the work. Their customers get the credit.

Presenters

Adam Finke, CEO Finke is a consumer finance expert and purveyor of financial inclusivity for all. LinkedIn

George Ulmer, CTO Ulmer is a premier full-stack developer with dynamic coding and successful founder experience. LinkedIn

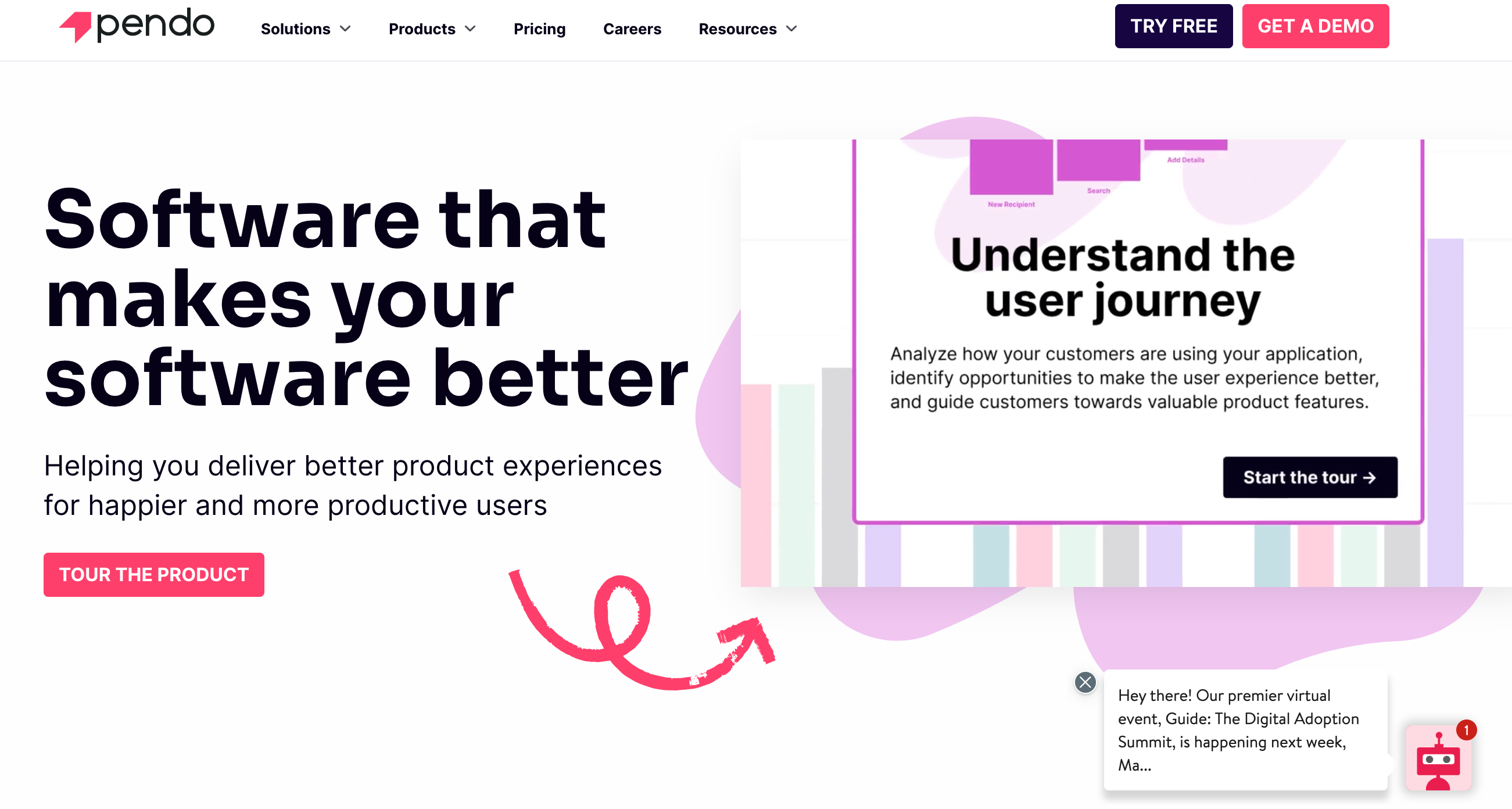

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

Pendo’s product experience and digital adoption solutions help companies become product-led and deliver digital experiences users love.

Features

Pendo Adopt includes:

Behavioral analytics

In-app messaging and guides

Actionable feedback

Why it’s great

Pendo Adopt can be deployed across an entire portfolio of workplace software, from proprietary software built by internal teams to customized off-the-shelf solutions

Presenter

Clay Miner, VP of Sales & Value Engineering Miner has a strong history of developing, implementing, and selling world class enterprise software. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

Hawk:AI’s AI-based, real-time AML and fraud surveillance detects patterns that purely rule-based systems miss.

Features

AI is explainable and auditable

Allows users to detect and prevent financial crime faster

One interface for maximum efficiency

Why it’s great

Efficient, effective, and explainable AML & fraud detection, powered by AI.

Presenter

Steve Liú, General Manager, North America Liú is a veteran in the fraud and regtech industry, with years of experience directing teams in operations and global expansions across the U.S. and APAC. LinkedIn

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

Basis Theory is a data tokenization platform used by organizations to quickly, securely, and compliantly use their sensitive data.

Features

Search encrypted data without decrypting

Build secure applications and workflows in minutes

PCI Level 1 compliant and SOC 2 certified environment

Why it’s great

Accelerate time-to-market and time-to-compliance.

Presenters

Colin Luce, CEO Luce brings over a decade of experience building and operating various fintech companies, including Yodlee, Klarna, and Figure. He is currently the co-founder and CEO of Basis Theory. LinkedIn

Brandon Weber, VP of Engineering Weber is an experienced engineer and leader with over 20 years experience in software development, cryptography, and network security at organizations ranging from the Air Force to Dwolla.

A look at the companies demoing at FinovateSpring in San Francisco on May 18 and 19. Register today and save your spot.

The Fundica funding search engine serves as a powerful business client acquisition tool for financial institutions by enabling them to truly democratize access to funding.

Features

Easily generate new business leads and retain clients with a complementary funding search engine

Gather firmographics and funding needs

Automatically promote diversity, equity, and inclusion

Why it’s great

Fundica makes financial intuitions a better and more complete funding destination by effortlessly extending their service offering at scale.

Presenter

Mike Lee, CEO & Co-Founder Lee is the CEO and Co-Founder of Fundica. He has held leadership roles in technology organizations, secured over $350 million in government funding, and holds Engineering, MBA, and CFA designations. LinkedIn