This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Greenlight Financial Technology unveiled its Greenlight Family Cash Mastercard this week.

The Greenlight Family Cash Mastercard helps teens build credit before they reach adulthood.

Headquartered in Atlanta, Georgia, Greenlight has raised more than $550 million in funding. The company has a valuation of $2.3 billion.

Greenlight Financial Technologylaunched its Greenlight Family Cash Mastercard this week. The new card fosters financial literacy by helping teens build their credit before they reach adulthood.

Available with all of Greenlight’s subscription plans, the Greenlight Family Cash Card enables families to earn up to 3% cash back on all purchases. Parents can add their teen children as authorized users on the card, and teens can track their credit card balances using the Greenlight app. At the same time parents can establish spending limits and receive real-time purchase alerts to help them monitor card activity. The addition of the Greenlight Family Cash Card means that Greenlight’s in-app financial literacy game, Level Up, now features instruction on the responsible use of credit, as well.

Greenlight subscription plans start at $4.99 a month. Other plans are available that add features such as identity theft, purchase, and phone protection (Greenlight Max for $10 a month), as well as family location sharing and crash detection (Greenlight Infinity for $15 a month). The Greenlight Family Cash Card is issued by First National Bank of Omaha.

In an interview with TechCrunch, Greenlight co-founder and CEO Tim Sheehan highlighted the company’s 3% cashback, Level Up financial literacy game, and parental controls as a trifecta that trumps offerings from other credit cards – including those that cater to families and youth. “Nobody has all three of these features,” Sheehan said.

Headquartered in Atlanta, Georgia, Greenlight was founded in 2014. The company has raised $550 million in funding, which includes a $260 million Series D round in 2021. This investment gave the fintech a valuation of $2.3 billion. The following year, Greenlight unveiled its Greenlight for Classroooms offering, a web-based financial literacy library. The library includes more than 100 animated videos, and a bank of thousands of vocabulary words and test questions. Additional features include quizzes, ideas for individual projects, discussion activities, and a teacher’s guide. Aligned with K-12 national standards, Greenlight for Classroom is available to schools, teachers, and students across the U.S. for free.

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

Effectiv’s fraud and compliance automation platform for fintechs, mid-sized banks, and credit unions automates compliance needs while helping manage fraud with a best-in-class solution.

Features

Effectiv’s unified fraud, risk, and automated compliance solution provides an omni-channel approach to:

Frictionless account opening

Loan application processing

Real-time transaction monitoring

Why it’s great

Effectiv is the modular, centralized risk hub that gets businesses compliant and fraud-free from day one, with AI & ML models that adapt to their organizational needs.

Presenter

Ritesh Arora, COO & Co-Founder Before becoming Co-Founder of Effectiv, Arora led the Fraud Data Science team at PayPal. He has decades of experience in fraud, data science, and technology and an MS in Management and Statistics. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

Savana unifies and orchestrates banks’ processes between the core, back-office, and digital channels to enable frictionless interactions between banks and their customers.

Features

Provides one experience for servicing customers across bank-assisted channels and products

Offers core-to-customer centralization and automation of processes

Leverages centralized processes via API for digital channels

Why it’s great

Savana enables banks to own business processes and channel experiences holistically, eliminate process silos on the back-end and the front-end, and launch or modernize quickly without risk.

Presenters

David Williams, CPO Williams leads the development and execution of Savana’s product strategy to bring value to banks and their customers. LinkedIn

Larry Edgar-Smith, SVP, Sales Engineering Edgar-Smith combines market intel with industry experience to help shape the strategic direction of Savana’s solutions. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

ClimateTrade is a pioneering climate-tech company, providing innovative solutions for large-scale corporate decarbonization and empowering individuals in the fight against climate change.

Features

Includes carbon-neutral financial products and services with a powerful API

Integrates climate action at the point of sale

Empowers customers and address scope 3 emissions

Why it’s great

ClimateTrade’s plug-and-play API calculates and offsets the carbon footprint of end users transparently, attracting sustainability-focused businesses and individuals.

Presenter

Francisco Benedito, CEO & Co-Founder Benedito was named among the “100 Latinos Committed to Climate Action” and “Top 22 Business Disruptors of 2022 – Forbes Spain”. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

IllumaShield Voice Authentication integrated with Glia’s Digital Customer Service platform for frictionless yet secure voice engagements.

Features

Better customer experience with frictionless account access

Improved operational efficiency by cutting minutes from each phone call

Better security with biometric voice authentication

Why it’s great

The Illuma Shield voice authentication integration with Glia improves operational efficiency, security, and customer experience for community banks and credit unions.

Presenters

Milind Borkar, Founder & CEO Borkar brings a background in R&D and more than 50 successful product launches to his role as Founder and CEO of Illuma Labs. LinkedIn

Greg Cummings, Director, Global ISV Partners Cummings has over 20 years of experience in the customer engagement space and currently serves as the Director of Global ISV Partnerships at Glia. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

Engage People is a loyalty network that enables program members to pay with points directly at checkout.

Features

Enabling Access Plus through a simple integration:

Converts loyalty points to cash

Increases redemption options

Drives customer acquisition and retention

Why it’s great

Access Plus is the evolution of Engage People’s pay with points payment technology, enabling program members to use their points like any currency directly at checkout or in-store.

Presenter

Len Covello, CTO Covello leads the long-term technology vision of Engage People and is responsible for driving continued technology innovation for customers. LinkedIn

Data analytics and insights platform ForwardLane launched a new generative decision intelligence platform this week.

The new offering, EMERGE, will enable financial professionals to create and interact with client insights while keeping private data private.

ForwardLane made its Finovate debut in 2016. Nathan Stevenson is founder and CEO.

Data analytics and insights platform, ForwardLane launched a new generative decision intelligence platform called EMERGE this week. The technology will help financial services professionals deal with issues of data transparency, privacy, and security within the wealth management and insurance space.

EMERGE gives financial professionals the ability to leverage generative AI to find, create, preview, publish, and interact with new and newly-uncovered insights and data in a manner that is private, secure, and accurate. The technology combines ForwardLane’s composite AI, EMERGE-GPT, with its Visual Insight Generator (ViGOR). Visual Insight Generator is a zero-code tool that enables users to create insights from data using natural language – without requiring any technical expertise in LLM. Along with ForwardLane’s Next Best Action platform, EMERGE provides a complete cycle from insight and orchestration to last-mile delivery, usage, and feedback.

ForwardLane founder and CEO Nathan Stevenson noted that his company has been leveraging AI for several years. “EMERGE is an applied Generative AI solution for financial services that brings together the best functionalities of ForwardLane’s ViGOR and privacy-friendly EMERGE-GPT,” he said. “It gives financial services firms the ability to rapidly activate their existing data and data science investments and deliver insights to their frontline advisory and sales professionals.”

EMERGE will enable financial services professionals to:

Identify opportunities and risks across their client base

Review up-to-date client intelligence and analytcs along with recommended Next Best Actions

Receive Next Best Action recommendations that are integrated via API with workflow links

Accelerate daily workflow with 100x increases in document reading ability

Summarize, interact, and extract insights from PDF, DOC, and other files up to 25,000 pages

EMERGE is available on a white label basis. The technology can be deployed on cloud platforms or hosted by ForwardLane. EMERGE is currently in limited beta testing; the company expects to offer wider availability in the second half of 2023.

Founded in 2015, ForwardLane made its Finovate debut a year later at FinovateSpring. The New York-based company has raised more than $8 million in funding from investors including SixThirty and SEI Ventures. ForwardLane began the year teaming up with InterGen Data to offer predictive life-event driven insights.

Chargeflow raised $11 million to build chargeback tools that help merchants automate card disputes.

The funding was led by OpenView and brings Chargeflow’s total funding to $14 million.

Chargeflow will use the funds to accelerate product development, fuel company growth, improve on its customer experience, and ultimately put a halt to fraud and illegitimate chargebacks.

Chargeflow is on a mission to simplify and increase profitability for companies processing online payments. Today, the Israel-based company received a boost toward that goal in the form of $11 million in Seed funding.

The VC funding, which was led by OpenView, brings Chargeflow’s total funding to $14 million. The company will use the investment to accelerate product development, fuel company growth, improve on its customer experience, and ultimately put a halt to fraud and illegitimate chargebacks.

“The funding will also allow us to build new products, just as our newest announcements, ChargeflowAlerts, and our all-new Stripe App, which has already gained amazing momentum and feedback from our customers,” explained Chargeflow Co-Founder, Marketing & Product Avia Chen.

Launched in 2021, the Chargeflow Alerts tool notifies merchants as soon as a customer files a dispute on a transaction, and allows the merchant to proceed with the transaction, offer a refund, or gather evidence for representment. The free Stripe App offers businesses a fully-automated chargeback management service.

Chen, along with his cofounder Ariel Chen originally launched Chargeflow as a Shopify app in 2021. The two have since added more processors, including Klarna, Braintree, Recharge, Stripe, and others. When integrating with these players, Chargeflow establishes a two-way data connection that facilitates the flow of information between the systems. The app offers merchants an overview of all fraud and disputes and autonomously fight chargebacks, disputes, and fraud with just a few clicks.

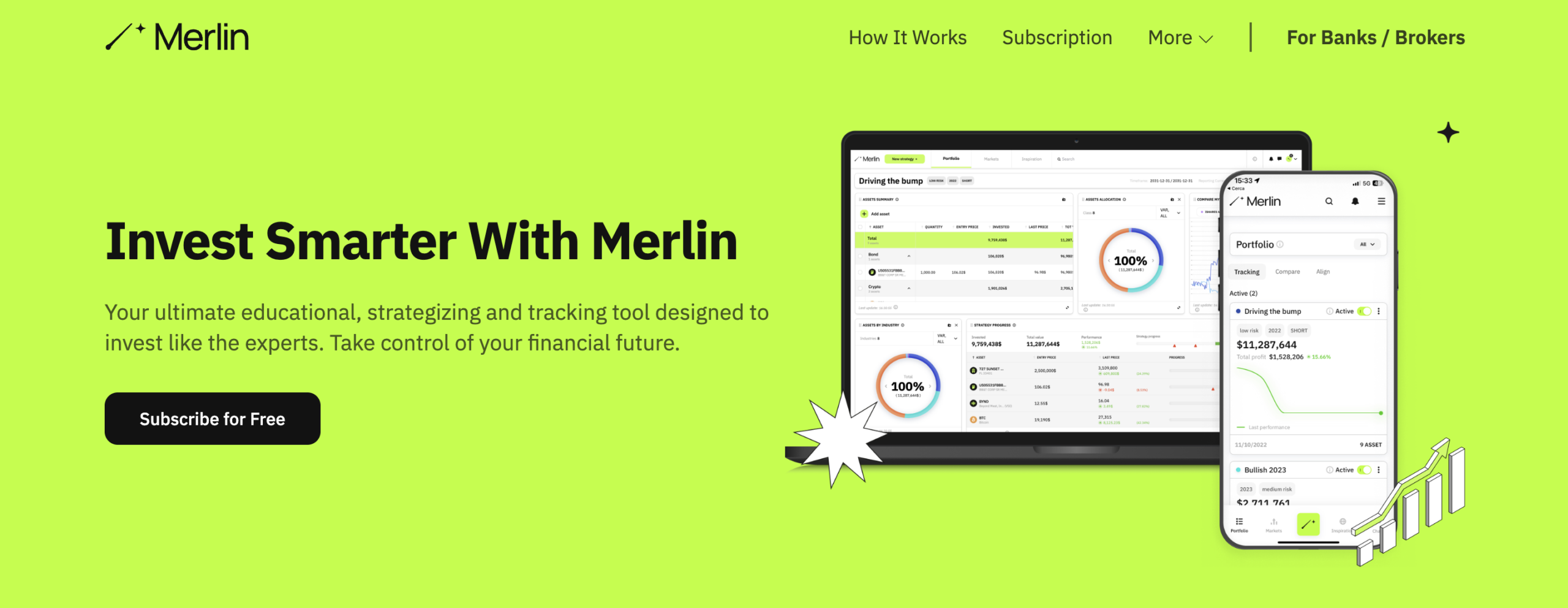

Launched in the fall of 2021, Merlin Investor is on a mission democratize access to investment strategies. The fintech offers a while label, multi-asset, educational, strategizing and tracking tool that helps investors accomplish two critical goals: building long-term positive results and limiting potentially catastrophic losses.

Merlin Investor’s technology is compatible with all trading platforms. The technology is suitable for both retail and professional traders, and is available for both the desktop and mobile. Merlin Investor enables users to retrieve market data and sentiment from multiple sources and apply that data to a massive range of tailor-made investment strategies.

With offices in both West Palm Beach, Florida, and Lugano, Switzerland, Merlin Investor made its Finovate debut at FinovateEurope earlier this year. The company returned to the Finovate stage in May for FinovateSpring. We caught up with Merlin Investor founder and CEO Guido Petrelli (pictured) this summer to learn more about the company, its mission to democratize access to investment strategies, and what to expect from the company in 2023 and beyond.

What problem does Merlin Investor solve and who does it solve it for?

Guido Petrelli: Merlin Investor was born as an intelligent protection and conscious guide for a more farsighted management of investments aimed limiting potential catastrophic losses while building long term positive results. Thanks to the Merlin platform, retail investors can educate themselves, study the markets, and create and track their own investment strategies to easily understand, balance and diversify investment risks.

In other words, we help and empower a new generation to invest with strategy in mind. This is the key to becoming successful and is the only factor distinguishing between gambling and investing. As we are on a mission to democratize financial inclusion and investment planning, our technology was built to allow anyone, regardless the level of knowledge or experience, to become independent and the one and only master of their own financial future.

How does Merlin Investor solve this problem better than other companies?

Petrelli: In the retail investor space, we see many companies focusing on execution, meaning focusing on the act of buying and selling assets. But executing without evaluating multiple sources of information first, combined with the lack of a diversified and balanced investment strategy, can lead to uncontrolled and unlimited potential losses because of the market’s ups and downs. While it may imply the chance for quick gains, it’s actually not the norm as wealth is usually built over time by managing a positive-sum game.

That’s why from the very beginning Merlin was designed as a complementary product to a trading platform and not as a substitute solution. Merlin Investor addresses the strategic essence of investing while the majority of the competition just focuses on enhancing the trading experience – which is already well supported by several financial institutions in a pretty similar way.

Who are Merlin Investor’s primary customers. How do you reach them?

Petrelli: Our primary customers are financial institutions focusing on educating a new generation of retail investors and offering the possibility to trade different asset classes through their digital banking platforms. We attend multiple fintech events in several countries that are attended by financial institution decision-makers responsible for delivering an innovative and digitalized experience to their clients. We also analyze the markets to identify those prospect clients we believe to be a fit in terms of services and client base. Then we look for the people focusing on retail digital products and platforms and reach out to them to introduce our company and technology. Last, we work to be featured in fintech-specialized magazines having financial institutions as target audience.

Can you tell us about a favorite implementation or deployment of your technology?

Petrelli: We offer our technology as a white-label solution that financial institutions can easily embed into their own digital platforms through API keys, while having the possibility to customize product’s appearance and features. As result, our product is delivered to the final users in the bank’s name and as a sub-section of the same app/e-banking they are already familiar with. Through our B2B partner’s portal, we grant to financial institutions the flexibility to choose from the full Merlin product those asset classes, sections, features, and contents they intend to integrate based on their own specific needs. In this way, they can design a tailored solution and experience for their own clients, while sticking to the overall structure and design of the banking platform they already offer.

What in your background gave you the confidence to respond to this challenge?

Petrelli: In a nutshell, it was the combination of my knowledge around investing and the problem I personally experienced as a retail investor that led to Merlin Investor. In fact, I was just a teenager when I first started to trade. Then I quickly realized that executing trades “per-se” – meaning the simple action of buying and selling assets – is the less strategic and relevant part to achieve long term positive results. Instead, studying different market sources, and then designing a diversified and balanced investment strategy, are what make the difference in the end. Still, (available) banking and trading platforms were not enough to educate me about investing, or to (help me) design and analyze my own investment strategies.

As a result, for years I was forced to create time-consuming and unfriendly spreadsheets to the point where I couldn’t accept it anymore – not in a world like today’s where we have an app for everything we do! At the same time with trading platforms booming basically everywhere, it became more and more clear that a new generation wants to invest autonomously and in the right way. As I couldn’t find any product in the market like the one I envisioned, I decided to create it. And that’s how Merlin Investor was born.

Merlin Investor founder and CEO Guido Petrelli demoing the company’s technology at FinovateEurope this year.

You recently demoed at FinovateSpring and will be demoing your technology at FinovateFall in September. What brings you back?

Petrelli: This year I’ve demoed the Merlin platform at FinovateEurope and FinovateSpring, so FinovateFall will be my third appearance. So far the experience has been great. We have been able to show our cutting-edge technology to major financial institutions in Europe and North America, while receiving much interest and establishing meaningful connections with decision-makers within the banking industry. The high visibility and key connections with prospect clients are the two main factors which bring us back to FinovateFall. The well-organized events and the team at Finovate are also a plus.

What are your goals for Merlin Investor?

Petrelli: Our goal is to be recognized by the major global banks as the innovative partner to work with when it comes to educating and empowering a new generation of retail investors. We focus on establishing solid and strategic partnerships with a limited numbers of players in the banking industry to achieve our mission of democratizing financial inclusion and strategic planning globally, while helping young investors to reach financial independence and to become the masters of their own financial futures.

What can we expect from Merlin Investor over the balance of 2023 and into next year?

Petrelli: We’ll continue to prioritize continuous and never-ending improvement of our technology by looking to upgrade the experience we offer either to financial institutions and to the final users to whom our product is deployed. We will also continue to work to boost our market presence to make the Merlin platform known to more financial institutions serving retail clients in several countries. We will eventually concentrate on scaling the team and operations to be able to manage expectations. We will accomplish all of this without forgetting our mission to make conscious and strategic investing accessible to anyone through strategic partnerships with financial institutions.

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

Connect Earth supports financial institutions in offering its retail and SME customers insights into the climate impact of their spending.

Features

Provides carbon footprint estimates based on spending

Includes CO2 analytics and chart breakdowns to better understand one’s carbon footprint

Delivers educational insights to enable action and engagement

Why it’s great

Financed emissions are 700 times greater than a bank’s direct emissions. By funding and investing in other businesses, indirect emissions become attributable to the financial institution.

Presenter

Alexander Lempka, Co-Founder & CEO Lempka co-founded Connect Earth by combining his experience in fintech with a passion for sustainability. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

Ocrolus plans to demo how a lender would use their full suite of capabilities end-to-end in an optimal way to be “the best SMB lender ever.”

Features

Delivers highly-accurate document capture data

Provides fraud detection with visual and programmatic identification of suspicious document edits

Includes cash flow analytics

Why it’s great

Ocrolus empowers lenders to digitize and automate their lending processes while making smarter decisions. Businesses can become “the best lender ever” with the company’s end-to-end capabilities.

Presenter

David Snitkof, SVP of Growth Snitkof is an accomplished technology entrepreneur and data/analytics leader who leads Ocrolus’ growth team, overseeing the company’s product, growth and brand marketing efforts. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

Nymbus SMB is a solution designed to augment the interactions between financial institutions and small to medium-sized businesses (SMBs).

Features

Fill the gap in self-service capabilities and integrated digital banking tools

Launch alongside existing banking systems, minimize disruptions and maximize efficiency

Fully support SMB growth goals

Why it’s great

Unlock SMB success with Nymbus SMB, seamlessly deploying tailored solutions alongside existing operations, optimizing efficiency and positioning businesses as a strategic partner for their clients.

Presenters

Drew Dizon, EVP of Partnerships Dizon is a fintech expert helping banks and credit unions overcome legacy technology limitations, enabling speed, time to value, accountability, and impactful innovation. LinkedIn

Brian Koenig, VP, Director of Business Solutions Koenig is a fintech professional specializing in digital banking, treasury services, risk management, and payments. He drives success for financial institutions at Nymbus. LinkedIn