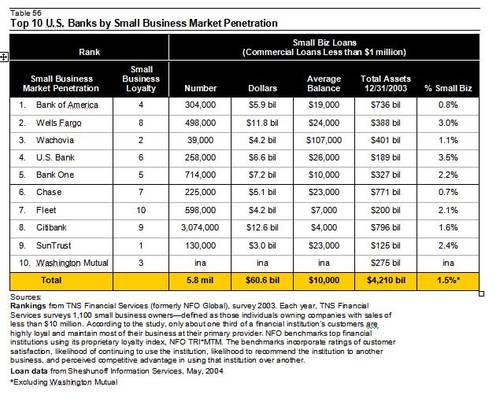

In the 2002 study of small business, TNS (formerly NFO Global Financial

Services) looked at which banks had the largest share of small businesses

relationships and which were ranked highest by small business clients.

SunTrust ranked highest in customer loyalty, followed by Wachovia

and Washington Mutual.

1. Bank of America

Pros:

· Three levels of business online banking: online banking with

bill pay, Business Connect for multi-users with varied levels of

access, and Bank of America Direct to manage all business finances

online.

· Good comparison chart of the three choices

· Resource center with informative articles on starting a

business and other topics

· Protect against online fraud link

Cons:

· Must scroll down to see all choices

· Hard-to-read small blue font for most links

· No separate URL or bookmark helper

2. Wells Fargo

Pros:

· Small business tab

· Excellent navigation and design, all viewable on a single

screen without needing to scroll.

· Clients can view personal and business accounts from a single

sign-on

· Single page, informative Small Business Newsletter

· Customers and non-customers can enter email address to signup

for newsletter

· Relevant and useful tips on product pages

· Product comparison pages as well as best product for your

business quiz

· Push a button to switch from English to Spanish and back again

· Link to Make this your first page at WellsFargo.com

Cons:

· No link to Security on the main page

· Not using liquid layout, so homepage appears small and

off-center at higher resolutions

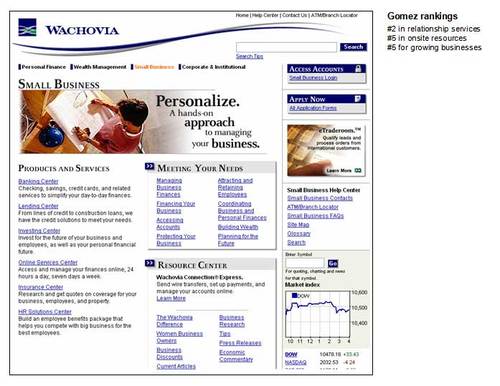

3. Wachovia

Pros:

· Small business is one of the four main navigation

choices on the top

· Copy and headlines are solutions-oriented, e.g., Meeting

Your Needs, Resource Center

· Excellent navigation and layout on a single page

· Separate small business FAQs

· Relevant products and services packaged into “centers”:

Banking Center, Lending Center, Investing Center, Online Services Center,

Insurance Center, and HR Solutions Center

Cons:

· Must scroll to see information on bottom of screen

· No link to Security

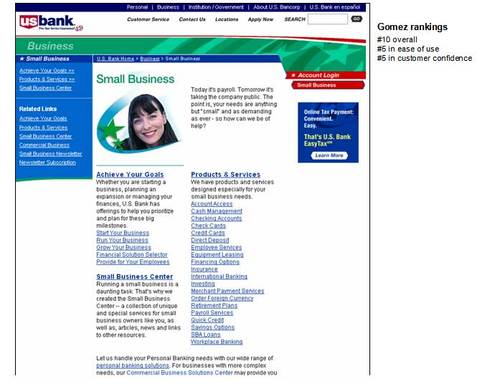

4. U. S. Bank

Pros

· All major links are contained on a single page without

scrolling

· The no-frills style is easy to read

· Two solutions-oriented sections: Achieve Your Goals and

Small Business Center

· Separate Small Business login

· Link to Newsletter subscription

Cons

· Layout and design could be improved

· No link to Security

5. Bank One

Pros

· Product-oriented layout makes it easy to find specific products

· Small link to Security on bottom (not visible on

screenshot)

Cons

· There is no small business section, in fact the term is

not used in any header, although it is mentioned in the opening paragraph;

choices are Business Banking and Commercial, that defies

industry conventions and could cause lost business

· No solutions-oriented areas or resources section

· Copy is cliché-ridden and not benefits oriented;

for example under Insurance:

“You’ve invested your heart in your small business.

We can help you find ways to protect it.”

6. Chase

Pros

· Small business is one of the four primary navigation

choices on the top

· Excellent design and layout that fits on one page without

scrolling

· Solutions-oriented sections: Plan and Learn,

Solutions, and Business Stages

· Link on left to Have Chase Small Business contact you

· Privacy & Security link on top

· Prominent Open an Account and Online Banking: Enroll

Now boxes in upper right

· Liquid layout

Cons

· No quick navigation or separate URL for the small business

page, you have to click on the Small Business section on the home

page, then move your cursor down the cascading menu to the Small Business

Home, it only takes a few seconds but it’s still unnecessary extra

effort

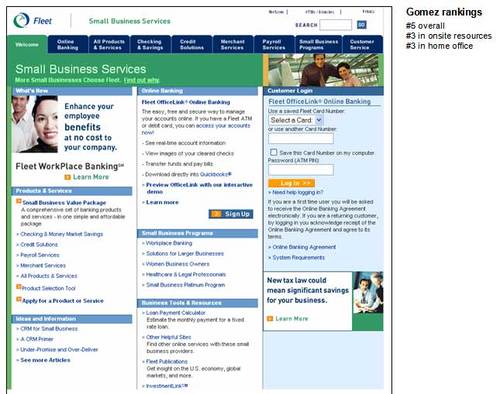

7. Fleet

Pros

· Separate URL

http://www.smallbiz.fleet.com/

· Tabs across the top help users find important subjects

· Link to Small Business Value Package (Note: Fleet also

offers a Small Business Platinum Program with a dedicated

relationship manager, faster funds availability, and priority phone service

· Solutions-oriented areas: Ideas and Information,

Business Tools & Resources

Cons

· Layout and design is a bit overwhelming

8. Citibank

Pros

· Using the drop-down menu you can navigate directly to relevant

business unit pages; the AAdvantage Business Card main page for

example is very well done

Cons

· Poor navigation off the home page: The only way to navigate to

the small business section is to use the drop-down menu on the right;

and because it doesn’t have a Go button, it took us 30 seconds before

we figured out you have to cursor down to Small Business at-a-glance

(screenshot above) in order to move to the small business section

· Poor navigation within the small business section: The four

main choices at the top of the page (Products, Planning, Investing,

and Special Offers) are NOT related to small business, they take you

back to consumer

http://www.citibank.com/ pages, and if you don’t use your back

button, you have to go through the full navigation routine to get back to

small business

· Must scroll down to see all the choices

· Main banking link (Checking, Savings, & Financial Services)

as well as the Online banking link cause a pop-up screen to load

which is dominated by an outdated self-promotion for online personal banking

with 2001 testimonial from Forbes magazine

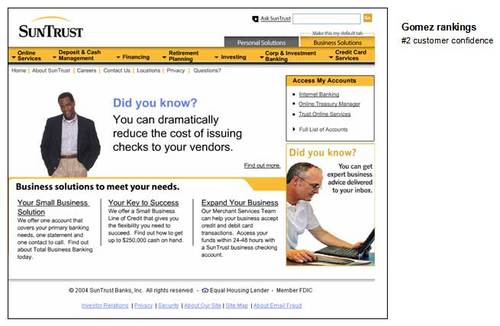

9. SunTrust

Pros

· Small Business Resource Center is a good area, although

it’s buried under the Online Services tab in the Business

Solutions area

· View only option for online banking, no money movement

allowed

· Ask SunTrust search box in upper right is handy, but it

doesn’t distinguish whether user in searching from business or personal

pages

Cons

· The top navigation bar is a mine field of cascading menus that

launch when the mouse travels over them, an out-of-date and annoying method

for primary navigation

· No dedicated Small Business homepage, other than the

Small Business Resource Center mentioned above and a mid-page link to

Your Small Business Solution which leads to a curious page entitled

Benefits that talks about Total Business Banking, but it’s not

clear if it’s geared to small businesses or not.

· Unclear and vastly different navigation/organization in the

various areas devoted to small business (e.g., Small Business Resource

Center)

10. Washington Mutual

Pros

· Link to content from StartupNation in upper-left corner; the

only bank in top 10 with headline targeting startups (see back page for more

information)

· Good online banking demo with audio highlights

· All the information shows on a single page without scrolling

· Liquid layout

Cons

· No link to Security

· Copy and headlines could be more solutions-oriented

· Layout is a bit sparse for a bank