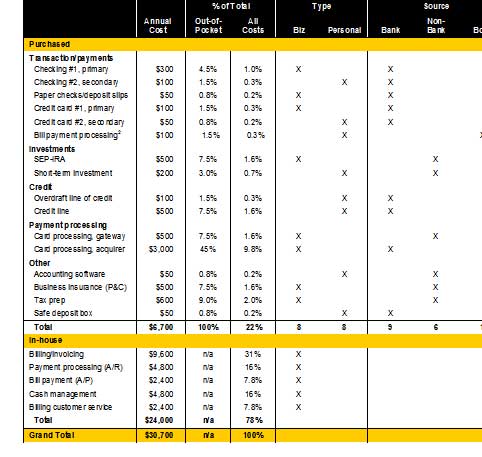

Case Study: Financial product usage at one small business

Microbusinesses typically purchase a hodgepodge of

services culled from both retail and commercial banking product lines. For

example, at our own small business, we purchase 16 financial products evenly

split between consumer and business products (see Table 52, below).

Nine are sourced from banks, six are from non-banks, and one is a combined

effort. Overall, we spend $6,700 annually in fees, interest paid, and

interest foregone (for checking). But the internal costs for managing our

billings, payments, and banking, are more than three times as much, an

estimated $24,000 per year. We would gladly outsource these to a

high-quality and VERY trustworthy third party, preferably someone with a

regulatory and fiduciary responsibility to safeguard our information and

assets, like a bank.

Table 52

Financial Products & Services Used by One Small Business

Source: Online Banking Report, 6/04 1Fees and net

interest foregone (deposits) or paid (loans) assuming 2% cost of funds

2Purchased through US Bank, but processed by CheckFree and user

interface by Microsoft Money

Package accounts targeted to business segments

Most banks offer small business bundles that include checking and

other basic transaction services. However, we believe the online platform

can be used to assemble more valuable offerings targeted to small businesses

with various financial management needs. Table 53 (below) shows ways

that the small business market could be segmented. Table 54 (p 53)

outlines major feature that could be included in package accounts targeted

to the financial management needs of the small business.

Table 53

Potential Business Segments to Target

Virtual financial management packages

Most banks offer small business account bundles that include checking

and other basic transaction. We believe that there is a significant

opportunity to expand into hosted financial and customer management systems

with monthly fees of $100 or more. Following are the pros and cons of moving

into the financial management arena:

Pros

- Profitable, incremental fee income

- Publicity and image enhancement from being the first in

your market to integrate banking functionality into an overall Web-based

small business management suite - Product differentiation and an impressive unique

selling proposition - Positive word-of-mouth within the local business

community - Powerful retention tool

- Potential for licensing to other financial

institutions

Cons

- Weak/uncertain demandd: Until recently, small

businesses have been slow to adopt new banking technology. It may take

several years of marketing, sales, and training before you begin to see

a payback. - Development costss: Building a robust, highly secure

new system will be pricey; you will probably want to partner with an

accounting software developer that already has code for the basic

functionality. - Uncertain ongoing servicing costss: Being on the

bleeding edge has its risks; it will be difficult to predict ongoing

costs for system maintenance, software development, and customer

support. - Lack of employee confidence: Financial institution

front-line personnel have been known to steer clear of discussing small

business and/or online banking subjects due to uncertainty with their

operation, cost, and overall value.

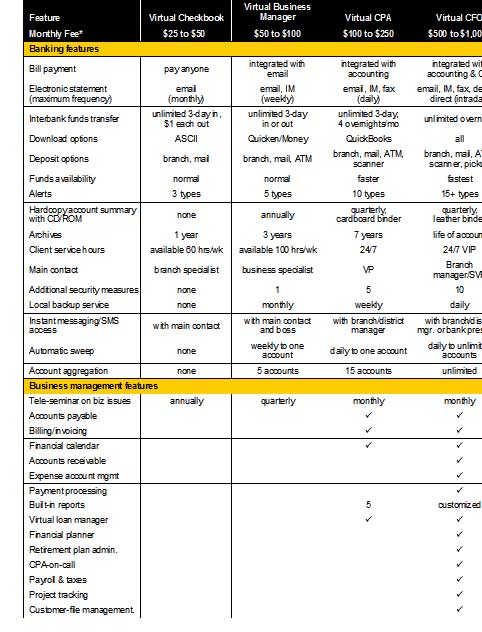

Table 54

Features of Virtual Accounting Package Accounts

*Approximate monthly subscription price; additional transaction fees

would apply for certain services.

Package Account Descriptions

Virtual Business Manager

Description: A secure place for small businesses to set up an

online home base, similar to corporate intranets. Possible names: virtual

office, virtual desk, virtual briefcase, or personal intranet. It could also

be marketed to the estimated 39 million U.S. households with a home office.

Functionality: For a financial institution, the key to making it

work is tight integration with banking and financial matters. A further

emphasis on local content/links could keep you ahead of the competition.

Banking and financial management feature are listed in Table 54 (previous

page), including:

- Financial calendar/datebook/reminder service

integrated with bill payment - Virtual safe deposit service that automatically

stores financial and other files in secure, encrypted, off-site back-up

files not accessible by anyone but the owner (not even bank personnel);

can be retrieved on CD for disaster recovery - Virtual receptionist that tells visitors how to get

in touch with someone at your business - Company message boards for internal users

- Company blogs for external users

- Ability to post documents to the Web, which can be

shared with everyone or just authorized employees and/or customers

Virtual CPAA

Description: As its name implies, the Virtual CPA provides

extensive accounts-receivable and accounts-payable services from a Web

interface.

Functionality: In addition to the Virtual Business Manager

features listed above and the banking/financial management features listed

in Table 54, the VirtualCPA could also provide the following features

(for more ideas, see the features built into Intuit’s QuickBooks

http://www.quickbooks.com/

- Billing statements and invoicing via email, fax, or

snail mail; includes reminders, and confirmations - Online, cash-based accounting functions including

data entry, categorizing, and basic report generation - Bill-payment/accounts-payable monitoring functions,

such as email notification when payment transactions are awaiting

authorization by business owner; email flags when payment transactions

don’t clear in a reasonable time - Autopay function that pays certain bills

automatically each month when preauthorized by the client - Virtual credit card terminal with integrated email

and accounting - Lock-box service for paper check processing with full

integration to client’s accounting system - Option to share selected information with outside

advisors, such as a CPA

Virtual CFOO

Description: This top-of-the-line service has it all. Just as in

the real world, the Virtual CFO takes the raw data and puts it into a

broader perspective that allows a business to be more profitable.

Functionality: The following features could be added to those

already offered in the Virtual CPA and Virtual Business Manager

modules:

- Online payroll with paper or direct-deposit paychecks

and electronic tax payments - Online federal and state tax return preparation and

filing - Full-fledged, double-entry online accounting

- Complete disaster-recovery services including a

redundant data center – an area in which banks’ inherent in-house

expertise could be turned into a profit center - Complete Web-based customer file management and

communications including:

– invoicing/billing with Web integration, e.g., bill presentmentt

– payment services/inquiry via the Web

– email/fax/voice messages automatically confirming payment - Access to a CPA-on-calll for accounting and tax

questions; advice could be delivered publicly on your Web, privately

through confidential conversations, or both. - Automatic excess funds allocation to minimize

interest expense and/or maximize interest income. For added value, the

funds “sweep” could go to investment and loan accounts at any financial

institution (not just yours). - E-commerce services for hosting secure transactions

- Accounts-receivable management that automatically

notifies the business owner and/or customers when accounts are past due;

includes linkages to a virtual payment window - Bank-branded virtual payment windoww, which clients

can display on their website to increase end-user confidence in paying

by credit card or electronic check (ACH); includes integrated messaging

confirming orders. - Extensive management reporting easily customizable

using drop-down menus; for example, revenue reports by customer,

accounts receivable aging, quarterly P&L; and so on. - Mail-merge capabilities that work across any medium,

email, fax, page, voice message, or snail mail; option to outsource

snail mail services to a mail house; includes label-printing utility. - Retirement plan administration including Web views

for participants - Project tracking module integrated with reminders and

other Virtual Officee services - Employee-expense reporting, cash advances and

reimbursement services - The ability to issue/reload prepaid credit

cards for customer rebates, expense account cash advances, and so on..