Remote deposit capture is one of the most significant new technologies to hit online business banking since, well, online banking. According to Celent, 60 of the largest 100 banks, including 20 of the top 25, now offer it. In addition, hundreds of smaller community banks now offer it.

Remote deposit capture is one of the most significant new technologies to hit online business banking since, well, online banking. According to Celent, 60 of the largest 100 banks, including 20 of the top 25, now offer it. In addition, hundreds of smaller community banks now offer it.

So why can't I find it through Google? (see note 1)

For two years I've been coveting the service and waiting for my bank to offer it to small businesses such as ours. I'm still waiting.

Today, I happened to see it mentioned on the homepage of a local community bank here, First Mutual Bank (see screenshot below).

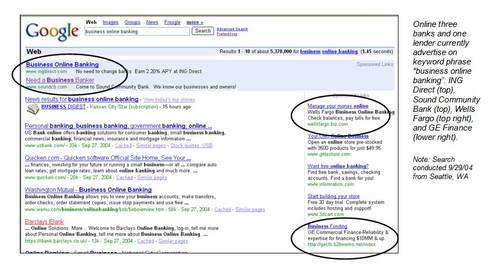

Not wanting the hassle of moving my account relationship, especially to a bank on the other side of Lake Washington (a major traffic hassle), I tried a little Googling to see what other banks in the area might have it.

It fails to show up in the organic results, and only two banks, Wells Fargo and Main Street Bank <mstreetbank.com> are advertising on "remote deposit capture" and the shorter "remote deposits." Main Street Bank is located out of state and Wells Fargo, while just up the street from my office, appears to target its remote capture to larger businesses. I'd be willing to pay $20 to $30 a month for it, but I'm guessing that's not even close to the Wells Fargo commercial customer price.

Action items (see note 2)

- If you offer remote deposit capture, make sure you have a dedicated page touting the features and benefits.

- On the dedicated page, make sure you use the term "remote deposit capture" in addition to any cute name you've branded it with. That will help users find it on search results.

- Market it through Google and other search engines. At this point, it doesn't appear that there's much competition for ads, meaning your cost per click should be low.

- Create a landing page that captures leads for your business banking officers. Check out Wells Fargo's approach at https://www.wellsfargo.com/com/boc_campaign

(see screenshot below)

Notes:

- I am searching from a Seattle IP address. In other markets, there may be financial institutions using Google to market remote deposit services.

- We will post an additional article on remote deposit marketing later today

Intuit's

Intuit's