This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

For the third Q3 in a row, Finovate alums have raised at least $1 billion in equity funding. This year’s third quarter is consistent with both the amounts raised ($1.1 billion) and the number of alums securing investment (14) from the same quarter last year.

Interestingly, August continues to be a strong month for alum funding during the third quarter; for a third consecutive year, August investment has exceeded that of both July and September for our Finovate alums.

Previous Quarterly Comparisons

Q3 2020: More than $1.2 billion raised by 14 alums

Q3 2016: More than $500 million raised by 30 alums

The third quarter of 2021 also saw one company, DriveWealth, become far and away the biggest recipient of investment dollars, topping the second biggest fundraiser by 3x. Three companies, M1 Finance, Alloy, and AuthenticID, secured triple-digit investments of at least $100 million.

The top ten equity investments, in a quarter with fourteen total alum fundraisings, represented the lion’s share of Q3’s investment total. Approximately 90% of the quarter’s total funding was represented by Q3’s top ten investments.

Top Ten Equity Investments for Q3 2021

DriveWealth: $450 million

M1 Finance: $150 million

Alloy: $100 million

AuthenticID: $100 million

Ocrolus: $80 million

Paystand: $50 million

Sezzle: $30 million

Dwolla: $21 million

Moneyhub: $18 million

Capitalise.com: $13.8 million

Here is our detailed alum funding report for Q3 2021.

July 2021: More than $469 million raised by seven alums

If you are a Finovate alum that raised money in the third quarter of 2021, and do not see your company listed, please drop us a note at [email protected]. We would love to share the good news! Funding received prior to becoming an alum not included.

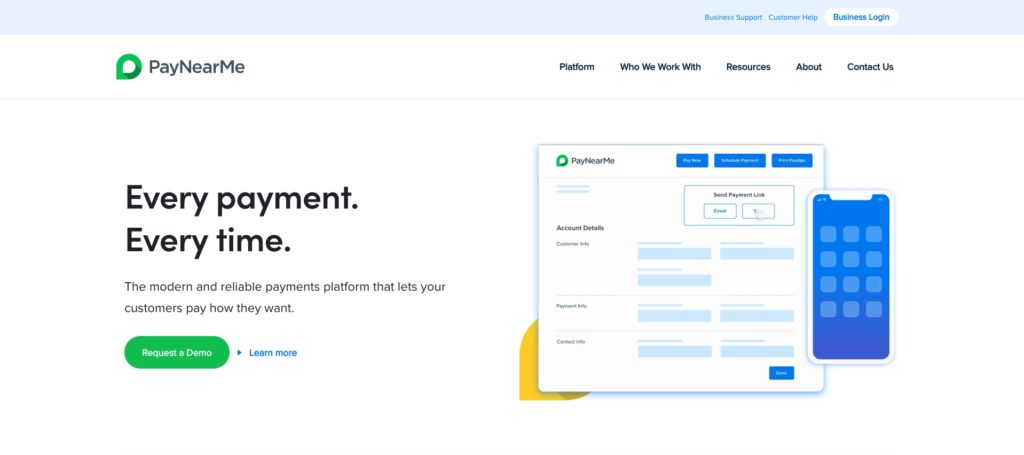

The payments space is one of the areas within fintech that has benefitted from the acceleration in digital transformation trends over the past year. And within the payments industry, innovation in billpay has been especially vigorous, as a growing number of individuals and businesses turned toward digital channels to make and receive transactions during the COVID-19 crisis.

We caught up with Anne Hay, Head of PayNearMe’s consumer research initiative, to discuss the company’s new collaborations with Green Dot and Walmart, as well as PayNearMe’s findings from a study of consumer payment preferences the company launched earlier this year. Have consumers become more or less interested in digital payment solutions since the pandemic? And what can financial services organizations do to take advantage of these trends? Anne Hay explains.

What problem in the payments space does PayNearMe solve? And for whom does it solve it?

Anne Hay: Today’s consumers are used to making quick, easy payments when shopping online or sending money to friends, and they now expect that same level of convenience for all their payment interactions.

PayNearMe clients are largely recurring billers, such as consumer lenders, mortgage companies, municipalities, and iGaming operators, and we are helping them bring that frictionless, flexible payment experience to their customers.

With PayNearMe, their customers can choose how, when, and where they want to pay. For instance, they can pay with all major payment methods including cards, ACH, and mobile-first payment methods including Google Pay and Apple Pay, as well as with cash at more than 31,000 retail locations, including 7-Eleven and Walmart.

This focus on the customer payment experience is crucial as it is often the most frequent touchpoint our clients have with their customers. Our modern payment experience platform is also the first to enable our clients to fully own the customer payment experience — from facilitating transactions across payment types and channels, to sending payment reminders, to analyzing data for business insights.

PayNearMe recently announced an expanded partnership with Walmart and Green Dot. Can you tell us more about this collaboration?

Anne Hay: PayNearMe is rethinking payments with an emphasis on the payment experience, customer satisfaction and, of course, increasing our clients’ ability to get paid reliably. This expanded partnership with Green Dot makes on-time bill payment more convenient by bringing easy cash payments to the same location where customers do their everyday shopping. Now millions of consumers who prefer to — or need to — pay in cash can quickly and easily pay their rent, car payments, and utility bills at Walmart.

Customers simply show their scannable PayNearMe cash barcode on their smartphone to an associate in the Walmart MoneyCenter, pay with cash, and collect a receipt confirming that the payment is complete.

The expanded partnership with Green Dot adds participating Walmart locations across the country to our ever-expanding electronic cash network, and we expect to launch additional retailers in the near future to extend the convenience of our cash pay experience to our clients and their customers.

Enabling cash payers is a strategy that can help retailers, such as Walmart, bring more shoppers into their stores on a regular basis. Each visit to Walmart to pay a bill presents an opportunity for these customers to make additional purchases.

PayNearMe recently took a look at consumer preferences with regard to modern billpay options. What were the top takeaways from that survey?

Anne Hay: With all the innovation going on in e-commerce and peer-to-peer payments, we wanted to better understand consumer expectations around bill payments. There’s already a lot of research and data out there about how consumers are paying bills, but we wanted to ask consumers about what would make their bill payment experience easier.

Overall, the study uncovered a significant disconnect between consumers and businesses regarding how consumers want and expect to pay their bills, and the current bill payment options offered by most businesses today. About 75% wish managing and paying bills were easier, with 38% even preferring to do laundry over paying bills.

We found three big issues that need to be addressed.

Billers are slow to offer bill payment choices consumers have come to expect in other facets of their lives, such as Venmo, PayPal, and Apple Pay.

Consumers are struggling with disorganization, and it’s causing bill payment problems, including late payments.

Accessing bill payment information and paying bills is a cumbersome and difficult process for a good portion of those surveyed.

A couple of interesting and surprising findings were the number of consumers, especially young adults, that call in, likely when they are not able to seamlessly complete their payment transactions on their own, and the number of respondents willing to use QR codes to make bill payments.

Respondents said that the billpay experience itself was a more significant stressor than the fear of not being able to pay the bill. What does that tell you? Where is the experience going wrong?

Anne Hay: According to the bill pay study, nearly 1 in 3 adults revealed that paying bills causes them stress and anxiety. Surprisingly, for 70% of them, it’s not because of money issues.

Remembering logins, passwords, and account numbers top the list of what makes bill payment cumbersome. Keeping track of payment due dates is challenging for 41% of those surveyed, especially for younger adults. 30% cite having to navigate poorly designed biller websites and 26% report manually entering payment information further add to consumers’ dissatisfaction with their current bill payment experience. This expectation mismatch is not only potentially damaging billers’ relationships with their customers, but it is also hurting their bottom line as these frustrations can lead to late or missed payments. In fact, more than half of the respondents paid at least one bill late during the past 12 months.

This finding shows just how important focusing on the customer experience is and how much that experience is shaped by expectations. Even though consumers have the financial ability to pay their bills, they are still stressed because the bill payment process is not as seamless as making an Amazon purchase or paying a friend with Venmo.

The survey suggested that nearly a third of respondents saw mobile payment options as key to easier billpay. What are the obstacles to broader mobile payment adoption?

Anne Hay: One of our survey’s key findings was that billers are slow to adopt new technology. Mindsets need to change. They are not just competing against other entities in their industry, but against the consumer experience expectations influenced by Amazon, Apple, and Uber. They are competing against fast, easy, frictionless innovation.

As payments software is not often a core capability for many billers, working with a modern, future-looking enterprise software platform partner like PayNearMe is key to meeting new customer preferences such as mobile. Not only do we offer a choice of mobile payment channel options, including pay by text, digital wallets (including Apple Pay, Google Pay and more to come soon) and QR codes, but we also incorporate the security features needed to protect mobile payments. With 38% of respondents saying they would be likely or very likely to use Apple Pay and Google Pay to pay their bills if they had this option, innovation matters. The right partner can help billers stay ahead of the latest trends and perfect the customer experience.

Given the rise of QR codes, cryptocurrencies, real-time payments, embedded finance, and more, which innovations in payments excite you most?

Anne Hay: More and more we’re seeing that the phone is primarily the way people interact with the web these days. So not only Apple Pay and Google Pay, but digital wallets as well. Apple just broke news that they signed agreements with eight states to embed driver’s licenses and IDs within their wallets; more and more, digital wallets are becoming the de facto way to handle important personal and financial matters.

Consumers are storing everything in their wallets, and this can include their bills. In fact, our survey found that if given the opportunity, 42% of consumers would be likely or very likely to use their digital wallet to store, view, and pay their bills from a single place. By storing bills in their digital wallets, consumers can access all of their billing information, including their history, which solves a key pain point our survey found.

For those living on their phones, digital wallets give them everything they need, including reminder notifications and payment channels. With a thumbprint or face scan, payment is done. It’s about meeting the consumer where they live. It’s more than just payments; it’s about making the experience as easy as possible for the customer and merchant.

It’s hard out here for a bank. Your clients are, to put in bluntly, getting older, while the world around you just seems to get younger and younger every year.

“You have to understand who your clientele really is,” Vincent Bezemer, SVP of Americas for Backbase, explained in a recent conversation for Finovate TV. “Let’s face it: most institutions have an aging clientele. And that is really not indicative of what the future of banking should look like. There is this digital divide.”

Financial institutions – from Tier 1 banks to the credit union around the corner – are all working to figure out how to bring a 21st century digital experience to their customers. We caught up with Mr, Bezemer, a technology veteran with more than a decade of experience innovating in the CX space, to hear his thoughts on what institutions need to do in order to not just keep the customers they have, but to attract, engage, and retain new customers, as well.

On the importance of self-directness and becoming the kind of bank that people love

“…(T)here is this need for self-directedness. There is a large part of the population – inclusive of all the demographics – that simply does not want to engage with a person and, if they engage, they want to engage on their own terms.

Supporting that self-directedness – and giving our customers, the banks, and the credit unions the tools to compete in an omni-channel fashion when it comes to digital – is key. The experience on mobile, web, should all be the same. But also the processes should be the same. Whether I’m in collection cycle, whether I’m in a self-service cycle, or maybe when I’m originating products, I want those experiences to be the same. And if I need help, the bank’s team member actually sees that same view that I do as a customer has seen and they can help me with as little friction as possible.

On balancing the unique innovation needs of Tier 1 institutions compared to those of community banks and credit unions

We approach both sizes of our customer base with the same principle that is that we are a platform. As much as Amazon is an e-commerce platform and Netflix is a content platform and Uber is a mobility platform, we really approach it from a banking platform perspective.

With our proposition, you can take the platform as is and build on top of that, which is what a lot of Tier 1s want to do. They have built everything themselves. They basically had unlimited innovation power. But they saw that 80% of their IT budget was there to basically keep their legacy systems afloat. They are now seeing that all of these non-functionals – whether its from an auditing or security or entitlements perspective. They say, “why don’t we just outsource that? Why don’t we just get a product with a roadmap that is supported by hundreds of thousands of people in the Backbase ecosystem, so we don’t have to worry about that any more. Then we can apply our resources to actually create the experiences and the innovations that actually matter in our competitive landscape.”

On the nature of personalization in banking

I think in financial services specifically, personalization falls into two categories: one, do you understand your customer? Do you understand the moments of truth that matter to that customer when they start engaging with you for a certain product? And this is where market data, behavioral data, any type of database you can procure can really help you have that understanding.

But then the second kind of personalization is really a “mass personalization.” Can you give your prospective customer – and also existing customers – the feeling that they can tweak the product ever so slightly? Because if you can, you are relating more with the needs of that person.

So you want personalization in the top of the funnel, driving them to the moment of truth where you want to be there for them. And then, subsequently, you want to understand how you are going to create that process so that the customer feels that you truly listened and that they can make those small customizations.

Is fintech’s final frontier the last chapter for banks?

A provocative new essay from Andreessen Horowitz General Partner Alex Rampell suggests that the way governments have directly intervened to provide financial support to citizens and businesses during the COVID-19 crisis could point the way to a new banking relationship between “people” and “We, the People” – with fintechs playing a starring role.

Rampell’s theme is disintermediation, which he calls the Internet’s greatest legacy. By enabling individuals to get access to the things they want – products, services, information – without a series of (often) fee-charging and rent-seeking gatekeepers, disintermediation has empowered users and rewarded those institutions that are best able to respond – quicker, safer, more accurately, and more completely – to customer demand.

The spectacle of governments – particularly the U.S. government – attempting to provide COVID-19 relief funding was for Rampell a dramatic example of what can happen when effective gatekeepers are NOT present. Because the U.S. government has few options to provide quick financing to its citizens and their businesses, a host of intermediaries were enlisted to help get relief money from Washington, D.C. to the American communities where it was needed. This, as we have since learned, has been time-consuming. Unfortunately, in some instances, it has also appeared to be wasteful in directing some funds to areas where none were needed and, in instances where support was needed, not distributing available funding, at all.

As Rampell put it: “The reason why things like the Paycheck Protection Program (PPP) have been such a disaster , or that stimulus checks still have to be mailed in 2021, is that there is no ‘direct connection’ between consumers and government for money. The government is the mainframe for money, but there’s not really an Expedia yet.”

And Rampell doesn’t see the point in waiting around for one, either. Instead, he asks why not use what the government already has access to, namely, social security accounts, and treat them like bank accounts?

“With an SSN as a permanent financial account with the government,” he writes, “the government could deposit money directly to consumers, or allow person-to-person transfers, or pay overnight interest on deposits directly.” Rampell imagines not only the ease of paying taxes (or receiving tax refunds) under such a regime, but also how much more efficient a government relief program might be with this SSN 2.0 approach.

Rampell is quick to insist that he is not interested in nationalized banking or what he called “postal banking” (generally, the idea of turning post offices into bank branches). Instead he argues that, in some instances, incumbent financial institutions are playing no more than a filtering role when it comes to facilitating savings in a country. And while this filtering has a role in modern capitalist economies, it is not exclusive and there is a good argument against treating legacy financial institutions as if it is.

“Fintech—’apps for money’—represents the most powerful tool that governments have to make their monetary services available directly to their own citizens,” Rampell writes, “helping accomplish monetary and policy goals and benefiting consumers equally.”

There’s more to Rampell’s discussion – including a key caveat on the role of private capital and risk-taking in such a system. But in a world that is getting increasingly comfortable with government playing an active role in the economy, a disintermediation that brings citizens closer to the government that rules in their name may be an idea whose time has arrived.

FinovateWest Digital is a wrap. And with our second, all-digital fintech conference now in the books, what have we learned about the state – and future – of fintech after three days of live demos, keynote addresses, and expert discussions?

Every Year is the Year of the Customer

The COVID-19 crisis has sensitized businesses to the speed at which consumer behaviors can shift. These shifts can both accelerate existing trends as well as to create new trends that had not been broadly anticipated. Whether this has meant embrace of digital technologies or improving the efficiency and security of incumbent solutions, businesses in have learned to listen more and move faster when it comes to responding to customer needs.

Maybe “The Era of the Customer” is a better way to describe the New Normal between businesses and consumers. With Big Tech, Big Banks, and a host of other financial and fintech providers increasingly competing over the same financial services turf, the most obvious and potentially enduring winners of this contest are most likely to be the consumers those firms are battling ferociously to serve.

Find a Friend!

There was a moment on the final day of FinovateWest when the moderator of a panel on challenger banking turned to his panelists and asked: “we hear a great deal about partnerships with incumbent financial institutions? What value do partnerships have for upstart institutions like challenger banks?”

The question took the neobanking innovators a bit by surprise, at first. But the idea of the innovators turning to innovators to help them add key elements to their offering, or to ensure that their solution is safe and secure is as much a part of the promise of fintech as is “disrupting” incumbents – if not more so. In the same way that our developers conferences helped shine a light on those professionals whose skills make everything from UX to back office operations that much better, so to do events like FinovateWest Digital provide a valuable space for all the players in the fintech ecosystem to meet and do business together.

Partnership is the fastest way to add competencies. You can’t innovate faster than someone who has already figured it out.

Live/Digital is Our Destiny

For those who fear a future of AI-powered robot overlords, the growing consensus among technologists is that AI will most likely and effectively be used in coordination with and support of human activity. In other words, rather than be replaced, human beings are more likely to be merely “enhanced”.

Similarly, even as news of a potential COVID-19 vaccine becomes more common and optimistic, we see a role for both digital-only and live-with -digital fintech conferences for the forseeable future. That’s not just for our upcoming Finovate Fintech Fulltime Review, December 7 through 11, but for our big events in 2021, as well.

For now, our upcoming events for European and West coast audiences are still slated to be digital-only affairs in March and May of 2021, respectively. But like those increasingly agile banks, financial services companies, and fintechs we praised above, we’re looking forward to engaging our audiences – live in-person or online and digital – wherever they are and every way we can.

FinovateWest Digital is still available On Demand for registered attendees. Check out live demos from our Best of Show winning companies, videos of our keynotes and panels, and more!

What is the impact of financial technology on what some might suggest is the most important “vertical” of all? With churches and other religious institutions joining other organizations in their embrace of technology, we wanted to take a look at how trends toward digitization – especially given the onset of the global health crisis – are impacting the way that faith institutions support and engage with their communities and congregations.

To learn more, we connected with Aaron Senneff, Chief Technology Officer with Pushpay. Founded in 2011 and headquartered in Redmond, Washington, Pushpay offers engagement and mobile commerce solutions, including payment solutions, to faith, non-profit, and educational organizations.

Finovate: With more than 10,500 customers and a total processing volume of $5 billion, Pushpay operates in a fascinating space within fintech: providing donor management and engagement solutions for faith communities. Can you tell us a little about the idea behind launching the company and the problem Pushpay solves for its customers?

Aaron Senneff: Pushpay was formed on the idea that church giving should be easier. When the company was founded, e-commerce through mobile devices and app was accelerating. You could order and pay for your coffee through the phone.

At the same time, churches were accepting donations via cash, check, and passing offering plates as they had done for years. Our founders saw an opportunity to use technology to help make giving easier for church members and make it much easier for church staff to track, manage, and encourage generosity through digital tools.

Today, Pushpay’s digital systems have built on the early success of digital giving, and expanded into donor development, custom mobile applications for churches and church management systems – a full complement of tools that aid churches. As our original founder was known to say, “Everything we do is driven by our purpose to bring people together by strengthening community, connection, and belonging.”

Finovate: How widely are services such as Pushpay used by churches and other religious institutions in the U.S.? Is this a rapidly growing opportunity for you?

Senneff: Many large, progressive churches use technology to their advantage today. It’s not uncommon for a church to use a wide variety of digital tools now, from streaming technology, to email marketing or CRM tools, to sophisticated custom websites. Many of those churches have added digital giving to their arsenal of tools, especially in the last five years. Particularly, large U.S. protestant churches – the so-called “mega-churches” – have significantly embraced the concept of digital giving.

The adoption of digital giving follows the adoption curve you might expect from other technologies. There are early adopters, early majority, late majority and laggards – churches span across all of these categories. While we’ve seen a lot of adoption in churches to date, we still see a number of churches and faith-based organizations using antiquated tools and processes to manage their giving. In addition, among our current customer base, the suite of tools is ever maturing, growing, and becoming more capable. There’s a great deal of opportunity to utilize those new capabilities, even for churches who adopted digital giving tools early.

Finovate: Who are Pushpay’s primary customers? Is this something that churches of varying congregation sizes can use – or is it mostly for larger institutions? Is there much geographic variation in terms of who uses Pushpay’s solutions?

Senneff: Pushpay serves churches of all types in the U.S. We have customers that rage from 20,000 in weekly attendance to less than 100, and every type of church in between. We have found that larger, progressive churches – the kinds of churches that might operate multiple campuses, have staff dedicated to digital technology, that have processes, systems and structures in place that support their complex and growing organizations – are often the first to adopt new technology and digital tools like Pushpay. However, we see very active interest in our tools across the spectrum of churches.

We’ve also seen an acceleration of adoption across the market as a result of COVID, as churches across the U.S. closed their doors, but still needed a way to engage their membership. The digital tools we provide can give churches a means to continue to communicate and engage with their membership, even while physical participation is on pause.

Finovate: You recently launched ChurchStaq, an end-to-end engagement solutions platform that includes a church management system. I think our readers would be especially interested to hear about the giving and donor management functionalities of the platform. Can you talk a little about this?

Senneff: ChurchStaq is a full suite of tools that enables churches to engage with their people on all levels. It includes a Church Management System – a back office system not unlike a CRM but customized for church staff – a customized mobile app that a church can deploy to their community, and a digital giving platform. These three core capabilities are combined into one product offer that work together to help churches know, grow and keep their people.

The strength of this platform isn’t the standalone donor management system or app or ChMS, but the combination of them all. A really good example of this is our suite of donor development tools. In addition to facilitating online giving, donor management system has some sophisticated reporting that allows church staff to easily identify changes in giving patterns among their community. A church might, for example, have a family that is experiencing financial distress as a result of a job loss and that is surfacing in their giving stopping or becoming more erratic.

The donor management system can easily identify those people who may be in need of care. From that point, the ChMS system can take those individuals and put them in automated workflows for the church that kick off a process of care that is designed by the church. Whether it’s assigning a staff member to call them and check in, sending them an encouraging email, or texting them with some resources, etc. They can also use the church app to push out content or push notifications to specific groups of people. The tools really work powerfully together to help churches big and small care for their people individually.

Finovate: How has COVID-19 impacted your customers? Have you seen the same eagerness to embrace new technologies as we’ve seen in among other institutions and organizations? Has Pushpay played a role in helping its customers manage the crisis?

Senneff: COVID has had a mammoth impact on U.S. churches. Many churches across the nation have been closed to physical attendance since early March. Even as they begin to re-open, we see hybrid models that combine in person and online attendance, and many church-goers and families continue to participate on-line. Digital tools like Pushpay’s have been vital for some churches. It’s allowed those who may have historically relied on physical engagements to connect with people – like written Connection Cards, booths in the lobby, new attendees meeting or classes – to replace those physical engagements with digital ones, such as invitations to give, to join groups, to interact with staff or see the churches calendar of events from a mobile app.

Many churches who were already investing in online tools actually saw attendance via viewership rise during COVID over their historic physical attendance, and the digital tools that Pushpay provides can help churches better engage with those individuals.

Finovate: What can we expect from Pushpay over the balance of 2020 and into next year?

Senneff: We continue to invest significantly in our entire product family: our digital giving platform, our church management systems, and our custom mobile apps. We’ll continue to move each of these products’ features and capabilities forward individually, but we have a significant emphasis this year and beyond on providing a seamless, full-suite solution where churches can gain a sharp 360-degree view of their people, which they can rely on to help know, grow, and keep their people.

It’s probably a good thing that many of us saw fintech’s Year of the Customer coming a mile (or at least several months) away.

There is no one who anticipated a year ago what the world would look like right now. But I suspect that fintech’s preoccupation with the customer experience going into this year has helped the industry make the necessary adjustments now that 2020 has actually arrived – in all its unpredictable craziness.

One of Europe’s most underrated fintech countries, Portugal, is home to this week’s latest Finovate webinar host: Celfocus, a company that is helping other companies offer a better customer experience. Founded in 2000 and headquartered in Lisbon, Celfocus is a system integrator and specialist in digital transformation that works with businesses in a number of verticals to enable them to enhance their operations using automation and AI.

On Wednesday, September 30th, Celfocus’ Henrique Cravo (Digital Lead) and Carlos Domingos (Digital Channels and Integration Lead) will lead an interactive conversation that looks at how cognitive data insights can be the key ingredient – along with automated AI – that enables financial institutions to build and deliver “tailored experiences that trigger new targets, portfolios, and customer lock.” With the demand for greater personalization growing, Cravo and Domingos will show how financial institutions that customize offerings to meet their clients’ needs are likely to develop the deepest and most meaningful engagement. And the key to being able to deliver this high level of customization is being able to effectively manage and interpret customer data.

“From risk takers, tech-savvy, and hungry for innovation customers to tech avoiders that value human touch,” Cravo and Domingos wrote earlier this year, “banks must accommodate different engagement approaches and insights to differentiate customer profiles. This happens,” they wrote, “not because they don’t have the data, but because they can’t mine it.”

Learn more about Celfocus’ approach: Customer Knowledge Augmentation and Activation from their July 2020 guest post. And then join us on Wednesday for an in-depth conversation on how banks and other financial institutions can not only gain new insights into their data, but also leverage that data into actionable knowledge to provide better, more consistent, personalized customer experiences.

A recent analysis by Brookings looked how technology, platform regulation, and China policy may be impacted by the policies of a future Joe Biden/Kamala Harris administration should President Trump fail to be re-elected. As might be expected, the review pointed to greater regulation – including anti-bias and worker rights advocacy – as one likely outcome if a new administration takes office next year.

Also interesting are the ways that the Brookings analysts – and others – see a Biden/Harris administration as an enabler of technological advancement and innovation, especially in the area of technology infrastructure. This is also one of the ways where a Biden/Harris administration could be most constructive for fintech.

As the Brookings analysts point out, the fact that the Democratic vice presidential nominee is a Senator from California (who represents Silicon Valley) suggests that there might be greater insight into the issues and challenges of the 21st century technology industry than exists in the current administration.

This likely cuts both ways. A Democratic administration would likely be more supportive of immigration policies that would enable tech firms to keep and attract more talent – as well as for international talent to decide to innovate and build in the U.S. rather than in Europe or Asia. This would benefit fintechs across the board as much as it would benefit technology companies generally.

At the same, there’s no doubt that regulation – especially financial regulation – would likely see a resurgence. While many are wondering about the prospects of an Obamacare 2.0 in a Biden/Harris administration, fewer are discussing the possibility of a CPFB 2.0 and the likelihood of a renewed attention on fintech’s lenders in particular. I think that the CPFB’s creator, Massachusetts Senator Elizabeth Warren, would probably not be headed to Treasury in the event the American people put Joe Biden in the White House, but her influence on the resurrection of the agency would be powerful.

At the same time, it is worth remembering that Joe Biden has a far different historical relationship to the world of finance, if not fintech, compared to Senator Warren. As a multi-decade senator of Delaware, Biden has been criticized – including by Senator Warren – for his “energetic work on behalf of the credit card companies.” A 19th century Delaware law allows any American company to incorporate in the state and not a few firms over the years have taken advantage of this to “place their profits in Delaware-based holding companies to avoid paying taxes in the places where they actually operate” as Tim Murphy described in Mother Jones last year.

It may be too much to suggest that the First 100 Days of a Biden Administration would feature a tug-of-war between the new president and Warren over the appropriate attitude toward consumer lending and credit. But the presence of both does suggest that any policy that emerges could be more moderate than might otherwise seem.

What are the challenges of launching a challenger bank in today’s environment? What do these neobanks offer that traditional banks do not? And what will the path forward look like for these newcomers in terms of disruption versus collaboration with both incumbent financial services companies, as well as fintechs?

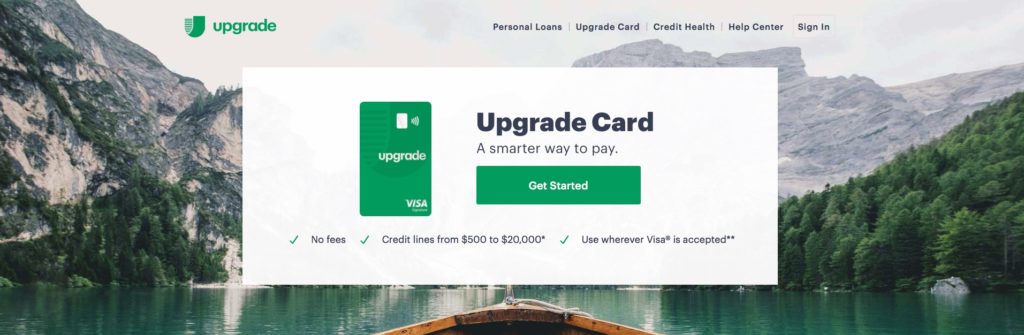

We caught up with Renaud Laplanche, co-founder and CEO of Upgrade. The San Francisco, California-based neobank, which recently announced a major fundraising, was founded in 2016 and specializes in offering credit solutions rather than savings products to mainstream consumers.

We talked with Renaud about what makes Upgrade different from other challenger banks and what the company has in store for the second half of 2020. We also drew upon his experience as the founder and CEO of LendingClub to discuss the challenges of fintech innovation in times of crisis.

Finovate: Most founders would consider themselves lucky to be responsible for bringing one company to unicorn status. With Upgrade’s most recent fundraising, we can now say that you’ve brought two companies to this level. How big of a deal was the June investment for the company?

Renaud Laplanche: Thank you, David, that was a big deal indeed. Reaching a billion-dollar valuation in just three years was an amazing achievement from the team, but more importantly we secured the backing of a formidable ally with Santander Group, a top 10 global bank, leading the round. We have been growing at a triple-digit rate in the last 12 months, and recently hit $100 million revenue run rate, so we would certainly have commanded a higher valuation from a growth-stage VC fund, but the strategic value of Santander was key to us. We believe this is the first time a top 10 global bank backs a neobank, which is a very positive development for the fintech industry as a whole as it shows that the largest banks in the world see tremendous value in fintech product innovation.

Finovate: One of the aspects about Upgrade that has attracted special attention is the idea of being a neobank “with credit at its heart.” What does that mean and why pursue this route?

Laplanche: Credit represents 70% of banks’ revenue in the U.S. and globally, and obtaining credit is often the number one reason consumers seek a bank relationship to start with. So credit is an essential component of any bank, and particularly a neobank that doesn’t benefit from a branch network and must establish trust and loyalty through other means. A credit relationship achieves that very purpose.

Our ability to deliver a mobile banking experience offering payments and deposit capabilities coupled with loans and credit cards at scale makes us unique in the neobank space. Credit is difficult to scale because it requires billions of dollars of capital, which means either a very large balance sheet and a capital-intensive model that doesn’t generally fit with a fintech framework, or outsourcing that balance sheet to investors, which itself requires a long track record of credit performance. Building the underwriting and servicing infrastructure to handle billions of dollars of credit is also challenging.

We started offering credit products in 2017, and have built the necessary track record, underwriting and servicing infrastructure, delivered billions of dollars of credit to consumers and are now about to roll out our full mobile banking experience.

Finovate: What are the signature offerings from Upgrade? How many users are taking advantage of them and what kind of growth has the company experienced so far?

Laplanche: Our signature offering is Upgrade Card, a credit card that delivers the low cost and responsible credit of installment lending through millions of points of sale. Instead of turning charges into a never-ending revolving balance like traditional credit cards, Upgrade Card turns each monthly balance into an installment plan that consumers pay down in monthly equal installments over 1 to 5 years. This approach encourages the discipline of paying the balance down every month, and eventually lowers the cost of credit for consumers.

Since launching in 2017, we have delivered over $3 billion in credit through both cards and loans. We launched Upgrade Card in October of 2019 and already passed half a billion dollars in annual origination run rate. Even through the crisis over the last several months we continued to record 20%+ monthly growth.

Finovate: One of the investors in Upgrade said that they were excited to support the company in its “next stage of growth.” What does that next stage look like? What are the goals, for example, over the balance of 2020?

Laplanche: We are doubling down on the existing strategy and will be using the new capital to fuel the continued rapid growth of Upgrade Card and launch Upgrade Banking, a full suite of mobile banking products and services. Overall we expect to add approximately $2.5 billion in credit origination this year, and launch what we believe to be the most innovative mobile banking product for mainstream consumers.

Finovate: What has the impact of the global health crisis had on Upgrade – both in terms of your relationships with customers and partners, as well as how Upgrade itself may have had to adjust internally to adapt to the “New Normal”?

Laplanche: With many bank branches being closed over the last few months, a lot of consumers have turned to online banking. This was generally a small adjustment to the “millennial” population, but a much bigger adjustment to the generations that grew up in a world of in-person banking. The COVID-19 crisis accelerated the digitalization of financial services, and gave many consumers an opportunity to discover online banking and online credit for the first time. I believe the corresponding changes in consumer behavior are here to stay.

The crisis also caused us to re-prioritize some of our product development, including the introduction of a contactless version and a mobile-payment version of Upgrade Card in April of 2020, several months ahead of the planned release date. Both features have helped our customers avoid surface contacts during in-store checkouts.

Internally, we made the decision early on to allow all of our San Francisco and Montreal employees to work from home. Everyone has stepped up to the challenge and we’ve seen no loss of productivity as a result.

Finovate: You co-founded LendingClub shortly before the Great Financial Crisis and managed to steer the company through that challenge to great success. Some people have compared our current situation – with the COVID-19 pandemic and growing social unrest worldwide – to that previous crisis environment. From the point of view of someone who has led a fintech company through a major crisis, what advice do you have for fintech entrepreneurs in terms of dealing with this one?

Laplanche: There are similarities and differences between the two situations. The economic crisis caused by COVID-19 is a lot more severe in terms of job losses, and came in more abruptly than the 2008 financial crisis. But the financial health of the U.S. consumer, the banking system and the overall economy immediately prior to the crisis was a lot better than in 2008. The monetary and fiscal policy response has also been stronger, and so far more effective this time around. It is still hard to know the exact economic and social impact of the pandemic, as so much is still in play.

That being said, some parts of the 2008 playbook remain relevant: cut costs early, conserve cash, raise more cash if you can, and always assume the downturn will be longer and more painful than initial estimates would have you believe. A prudent approach is generally rewarded in the early phase of a downturn. There will likely be opportunities toward the end of the downturn and early phases of the recovery, but these opportunities will only be available to those who weathered the storm in the first place.

In the middle of the first month of the year, one of the biggest names in the payments business acquired one of the most innovative fintech infrastructure companies in the industry, in a deal valued at more than $5 billion.

Six months later, Visa’sacquisition of Plaid almost seems like news from another time.

The arrival of the coronavirus to virtually every corner of the globe – and the worldwide response to the killing of a black man in police custody in the U.S. – have sent shock waves through the fintech industry – as they have the rest of the world. Now, at the same time, fintech is engaged in both the struggle to help businesses and consumers cope with the closures and shelter-in-place restrictions of the COVID-19 crisis, as well as the challenge of correcting decades of discriminatory practices against African Americans and members of other underrepresented ethnic groups. As we approach the middle of 2020, fintech is facing different kind of crisis that, while not of its own making, will require a response that is uniquely tailored to the world it operates in.

This is a world that is both heavily technical, relying on the latest innovations in machine learning, artificial intelligence, and distributed ledger technology, while simultaneously pledging to bring the benefits of 21st century financial services to the underbanked and underserved populations of both post-industrial and developing economies. This is a world that has grown tremendously through the contributions of people from diverse backgrounds, representing cultures from almost every corner of the globe. Yet, at the same time, it is a world that is still struggling to achieve true gender and ethnic diversity, particularly in the C-suite and in the boardroom.

There are many ways to value an industry: the quality of the goods it produces; the entertainment, education, or simple well-being its services provide; even just the degree of pure, gee-whiz innovation the industry may deliver, often seeming to grant us what we want even before we summon up the nerve to wish for it.

But as the fintech industry edges closer, inexorably, toward maturity, it now finds itself increasingly judged on the kind of criteria Corporate America – often to its own surprise and bewilderment – can find itself judged on from time to time. This is a judgement that has less to do with what Corporate America makes and sells, and more with who Corporate America is and what it values.

Both the global public health crisis and the renewed determination to fight racial inequality are providing fintech as an industry with an opportunity to show the world just what it’s made of. As we move into the second half of this historic year, I am hopeful and optimistic that fintech will rise to the challenge.

In the wake of the tragic killing of George Floyd at the hands of a Minneapolis police officer, people around the world are showing remarkable support for the cause of African American equality. From every corner of the globe, and in cities and towns across America, people from all walks of life are increasingly committed to making sure that the slogan “Black Lives Matter” evolves from being a mere rallying cry to a new reality for millions of black Americans.

With this in mind, we want to share again our thoughts on ethnic diversity in our industry, fintech, where we are in terms of inclusivity, and where we need to go.

When the discussion of diversity in the tech world comes up, the conversation is typically oriented around gender diversity. But the call for greater inclusion in the tech world is not limited to gender; diversity along ethnic lines is also a goal that technology companies have increasingly begun to strive toward.

Perhaps the international nature of many technology enterprises, with tech entrepreneurs and tech talent truly arriving in Silicon Valley from all corners of the globe, serves to mask the relatively small number of tech firms in general, and fintech firms, in specific, that are run by Americans who are ethnic minorities. Indeed, an online search for “African Americans in fintech,” for example, is almost as likely to produce entrepreneurs from Nairobi, Kenya as from Newark, New Jersey.

Importantly, there are tech firms that have won admiration for the diversity of their teams. Slack, for example, was widely praised for its diversity report which, released in 2017, showed that the company had achieved better gender diversity than its Silicon Valley peers. The report also revealed that Slack’s workforce had as much as 3x the number of underrepresented minorities (African American, Latino/Hispanic, and Native American) as its peers. An Atlantic article from 2018 pointed out that where Slack had minorities in 13% of all technical positions and 6% in leadership positions, companies like Google and Facebook had less than 4% of their technical positions filled by underrepresented minorities.

Clinc CEO and co-founder Jason Mars during his company’s Best of Show winning demonstration at FinovateFall 2016.

How has fintech fared when it comes to ethnic diversity in its technical and leadership ranks? Finovate has hosted a handful of fintech companies with African American leadership over the years – Clinc and its CEO and co-founder Jason Mars, DarcMatter and its COO and co-founder Natasha Bansgopaul, are two that come to mind. And the industry writ large may have more founders of color than many think: Forbes celebrated the release of its Forbes Fintech 50 roster last year by featuring Ryan Williams, the young, African American CEO of mortgagetech firm Cadre on the magazine’s cover. And venture capital firms like Backstage Capital have made investment in startups with founders of color – as well as women and members of the LGBT community – a priority.

Nevertheless, even as the number of African American and Latino/Hispanic tech founders and leaders has grown, it remains true that there are fewer African American and Latino/Hispanic founders and CEOs in fintech relative to other areas of technology, including education and health-related tech fields.

One of the biggest problems that companies lacking in diversity can face is that it can make them less capable of responding to the needs of diverse markets. Fintech analyst Mary Wisniewski wondered in a 2018 American Banker article “Are black millennials a blind spot for fintech firms?” and noted that while millennials in general have developed a healthy skepticism toward banks, this wariness is all the more pronounced in young people from communities of color. Among the solutions offered are more minority-owned financial institutions, and an increased emphasis on financial literacy and wellness as an engagement strategy for younger minorities.

In this regard, fintechs like GRIND may become more well-known and popular. Launched last year and based in South Central Los Angeles where it caters to the local African American community, GRIND offers FDIC-insured debit accounts, a mobile banking app, and the ability to get paid two days earlier if they set up direct deposit with GRIND. Another example of this kind of company is Finhabits, a bilingual (Spanish/English) mobile investment platform launched by Carlos Garcia in 2015. Garcia, an MIT graduate with experience with Merrill Lynch and Galileo Investment Management, explained that the issue for Latino and Hispanic communities was not their ability to save, but their lack of familiarity with investing. “Our day-to-day money management is good, but planning for 15 years ahead is not” he said in a 2017 profile.

As fintech continues to diversify itself as an industry, one good note is that it appears that fintech may be helping alleviate some of the issues in financial services caused, in part, by a lack of diversity. A recent report from the FDIC on consumer-lending discrimination in the fintech era, for example, suggested that technology may be playing a positive role in reducing the discrimination in credit faced by Latino/Hispanic and African-American consumers in particular. The report specifically pointed to “new entry of fintech platforms” as well as digital improvements by incumbents for increasing competition and declining rate discrimination.

Visa’sacquisition of Plaid for $5.3 billion at the beginning of the year set a high mark for mergers and acquisitions among Finovate alums in 2020. How have subsequent deals among our alums in the fintech space measured up?

Unfortunately, many M&A deals keep their financials well under wraps, which makes comparisons difficult. But we can take a look at some of the brighter lights in the merger and acquisition sky, and gain some sense of just how big some of these fintech stars truly are.

Looking at the first few months of the year, we have no figures for the four alums that were acquired in the first half of 2020. Of the acquirers, however, two deals stick out, rivaling the Visa/Plaid purchase in January: Intuit’s $7.1 billion buy of Credit Karma, and Worldline’s decision to put down $8.6 billion for Ingenico.

Below is our quick rundown of some of the biggest M&A action from our Finovate alums so far in 2020.

The Acquired

Emailageacquired by LexisNexis Risk Solutions. May 7.

Worldlineacquired Ingenico for $8.6 billion. February 3.

If you are a Finovate alum that was involved in a merger or acquisition in the first half of 2020, and do not see your company listed, please drop us a note at [email protected]. We would love to share the good news! M&A activity prior to becoming an alum not included.