- Google launched Universal Commerce Protocol (UCP), an interoperability layer that lets AI agents discover products, authenticate users, and complete transactions.

- Unlike AP2, which governs how agents move money, UCP orchestrates the entire commerce flow.

- UCP will require banks to create new approaches to authentication, consent, liability, and trust as AI agents become active participants in commerce.

Google unveiled its Universal Commerce Protocol (UCP) today, which essentially serves as the plumbing for how AI agents buy things on consumers’ behalf. But what does it really do and how is it different from Google’s AP2 launched last fall? Here’s a simple breakdown of the newly launched protocol.

What does UCP do?

Co-developed with major retailers and ecommerce players, including Shopify, Etsy, Wayfair, Target, and Walmart, Google’s Universal Commerce Protocol is essentially a standardized way for AI agents to discover products, request prices, authenticate users, and complete transactions. You can think of it like HTTPS, which is a set of rules that serves as a standardized protocol that governs and encrypts how browsers request and servers send web content over the internet.

Similarly, UCP is an interoperability layer that allows many systems to talk to each other and enables AI agents to make purchases and decisions on a consumer’s behalf, instead of just making product recommendations. UCP is more than a marketplace or a wallet. The new protocol coordinates the various aspects of how agents, merchants, identity systems, and payment rails interact during a transaction.

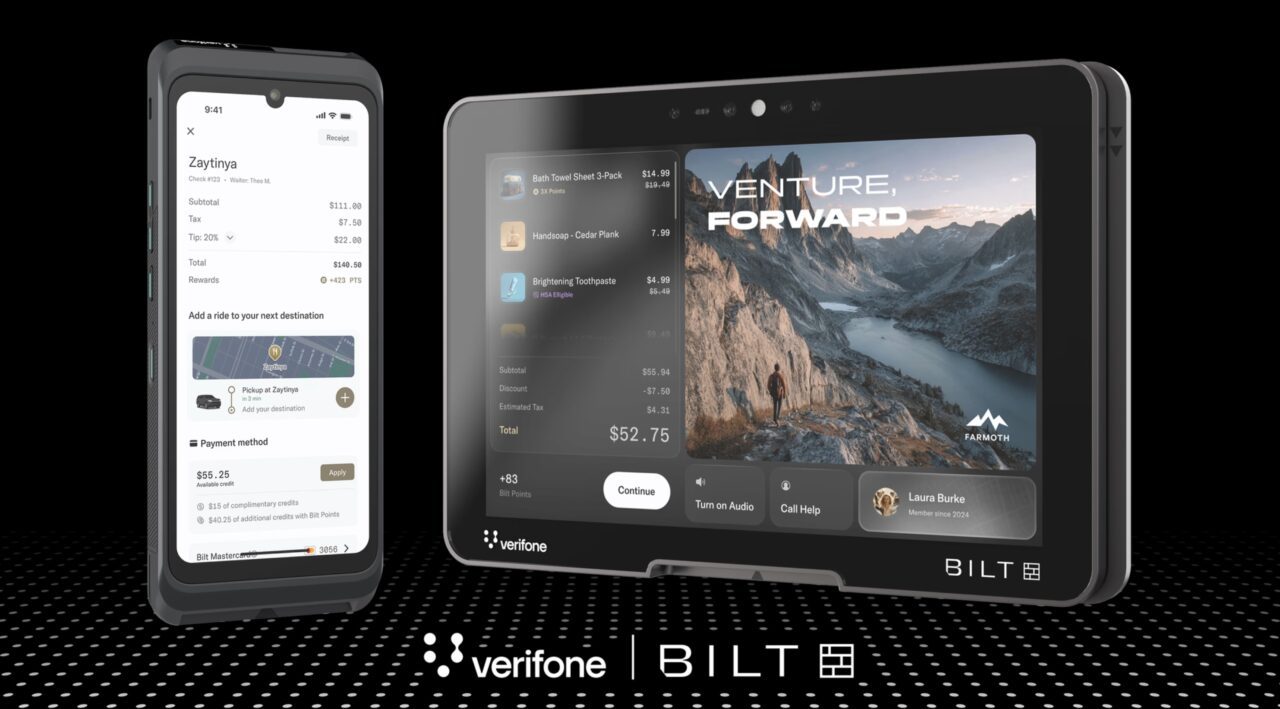

Google plans to use UCP to power a new checkout feature on select Google product listings that will allow shoppers to check out using Google Pay and PayPal from eligible retailers in AI Mode within Search and in the Gemini app.

From an end users’ perspective, this may seem similar to OpenAI’s partnerships with retailers like Walmart that allow shoppers to make purchases within ChatGPT. Google’s move, however, is markedly different. That’s because Google owns the payment rails. While the retailer remains the seller of record, Google controls the checkout experience as well as the protocol, which standardizes identity, payment credentials, shipping information, and consent.

How does UCP differ from AP2?

The final quarter of 2025 brought a deluge of new agentic commerce protocols to the market, creating confusion about the roles of protocols and the players involved. Among the protocols launched last year was Google’s AP2, its Agent Payments Protocol. AP2 is much narrower in scope than UCP, however, because while AP2 governs how an AI agent is allowed to move money, UCP orchestrates the entire commerce flow.

UCP handles product and service discovery, pricing and availability queries, merchant interaction, user intent and authorization checks, transaction confirmation, and fulfillment. AP2, on the other hand, is entirely payments focused. It handles payment initiation, authorization limits, credential handling, transaction execution, and settlement signaling.

What does all of this mean for banks?

Agentic commerce is moving fast and is set to change how transactions are initiated, authorized, and executed. As AI agents take on a more active role in purchasing, banks will need to rethink their role in the transaction stack and consider how to authenticate AI agents and create policies around who is liable when an agent transacts. Fortunately, protocols like UCP create auditability and can program trust into every transaction.